A 630 credit score sits in an interesting spot when eyeing for home financing.

You're usually high enough to qualify for several mortgage programs.

But you're not high enough to access the best rates.

That gap matters more than most people realize.

Many borrowers focus on getting approved. The lender focuses on risk.

A difference of 20, 40, or 60 credit score points can change how much interest you pay over the life of the loan.

On my Houston credit repair company, I've seen buyers rush into a mortgage because they finally qualified. Six months later, they realized waiting and improving their score could have saved them thousands.

That does not mean you should always wait.

But it means you should understand what a 630 score buys you before signing loan documents.

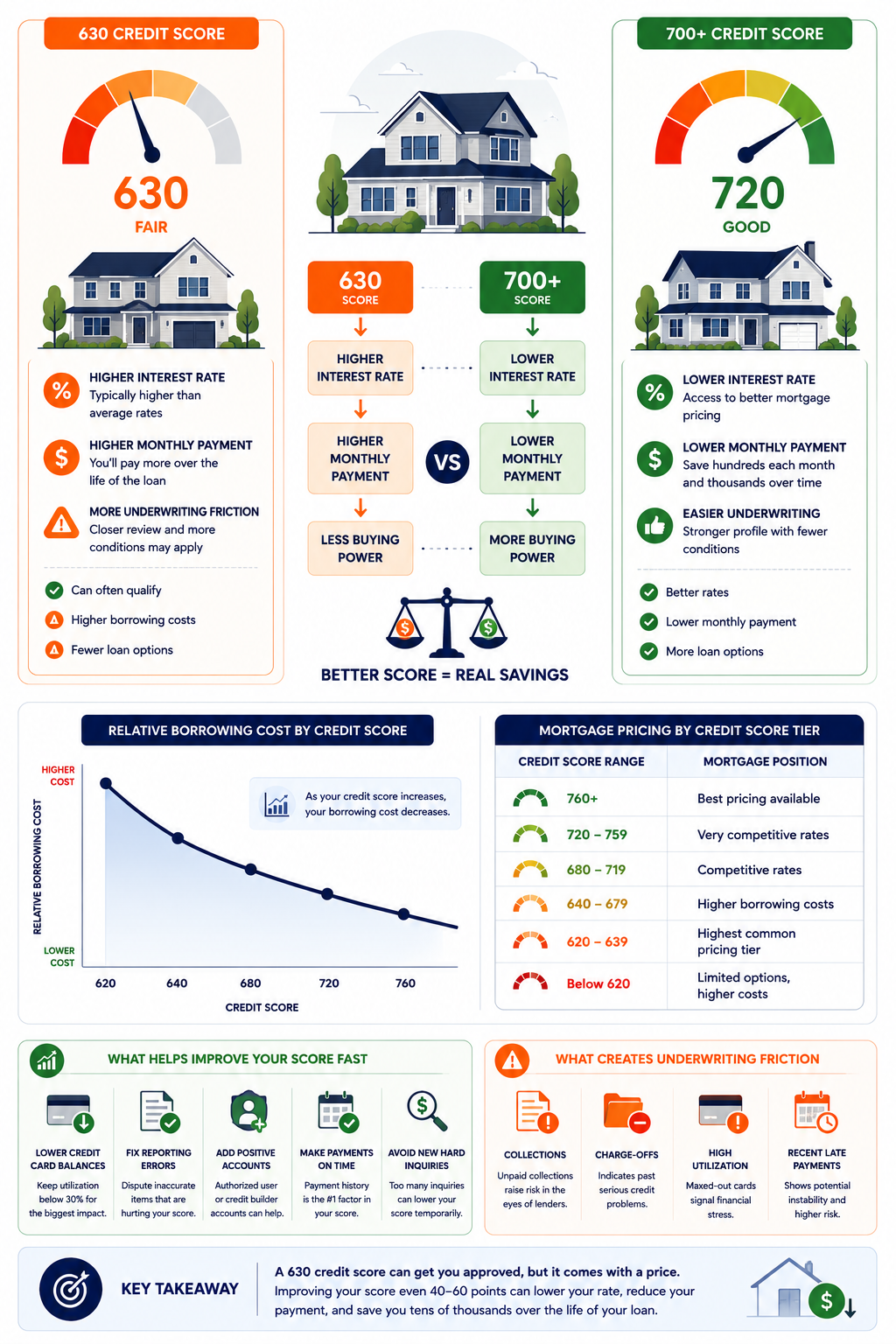

What Mortgage Interest Rate Can You Get With a 630 Credit Score?

A 630 credit score can qualify for a mortgage, but qualification and pricing are not the same thing.

The image below shows how credit score tiers affect borrowing costs, underwriting friction, and overall home affordability.

Can You Get a Mortgage With a 630 Credit Score?

Yes, you can. A borrower with a 630 credit score can qualify for FHA loans and some conventional mortgages. But interest rates are usually higher than those offered to borrowers with scores above 680 or 740. The exact rate depends on lender guidelines, down payment, debt-to-income ratio, and market conditions.

Can You Get a Mortgage With a 630 Credit Score

Yes. A 630 credit score qualifies for FHA loans and conventional loans. FHA requires 580 minimum for 3.5% down. Conventional requires 620 minimum. A 630 sits above both. The issue is not approval. The issue is rate. Getting approved at 630 is the easy part. Getting a competitive rate at 630 is the harder conversation.

- FHA loans: Minimum 580 for 3.5% down. A 630 qualifies comfortably. FHA rates are often lower than conventional for lower-score borrowers. But mandatory mortgage insurance premium (MIP) adds 0.55% to 0.85% annually to the effective cost. MIP does not cancel until the loan is refinanced or paid off if the down payment was under 10%.

- Conventional loans: Minimum 620. A 630 qualifies. Rates are higher than FHA for lower-score borrowers due to LLPA pricing adjustments, but PMI cancels at 78-80% LTV , unlike FHA MIP. For buyers with 10-20% down, conventional may still make sense depending on the specific rate offered.

- VA loans: No agency minimum. Lenders set their own overlays, often around 580-620. A 630 score qualifies at most VA lenders. VA rates are typically the lowest available regardless of score tier. No monthly mortgage insurance.

- USDA loans: No agency minimum score requirement, but streamlined processing typically requires 640. A 630 may require manual underwriting , possible but with more documentation requirements.

Why Mortgage Rates Increase as Credit Scores Drop

Mortgage rates are not arbitrary. They are priced by risk. Fannie Mae and Freddie Mac , who back most conventional mortgages , charge lenders additional fees based on borrower credit scores. Those fees are called Loan-Level Price Adjustments (LLPAs). Lenders pass them directly into the interest rate. A lower score means a higher LLPA. A higher LLPA means a higher rate. This happens automatically, in 20-point pricing brackets, whether or not you know it is happening.

Approval and pricing are not the same thing.

A lender who approves you at 630 is not doing you a favor. They are pricing for the risk you represent. Every LLPA surcharge above the 760+ tier is a calculation. It reflects the statistical probability that lower-score borrowers default at higher rates. The rate compensates the investor holding the loan for that additional risk.

The 630-score borrower and the 760-score borrower may get the same loan amount. They do not get the same product. The pricing , and therefore the total lifetime cost , is fundamentally different.

As myFICO's mortgage rate analysis confirms, the total interest difference between the highest and lowest credit score tiers on a $250,000 loan is approximately $60,980 over 30 years , with a monthly payment difference of $169. Scaled to $300,000, that gap exceeds $72,000.

What Mortgage Rate Range Can a 630 Credit Score Expect

Rate tables change daily. What does not change is the relative position. A 630 score sits in the second-lowest pricing tier for conventional loans. That means significantly higher rates than the market's best offers. The table below shows relative rate positioning based on credit score tier using current market conditions as a reference.

| Credit Score | Typical Rate Position | vs Best Tier |

|---|---|---|

| 760+ | Lowest available rates , best LLPA tier | Baseline |

| 740-759 | Very competitive , minimal rate premium | +0.10-0.15% |

| 720-739 | Competitive , moderate rate premium | +0.25% |

| 700-719 | Good , noticeable rate premium begins | +0.40-0.50% |

| 680-699 | Fair , rate premium meaningful on large loans | +0.55-0.70% |

| 660-679 | Higher , significant monthly cost difference | +0.75-0.90% |

| 620-639 (includes 630) | Significantly higher , near maximum LLPA | +0.90-1.10% |

| Below 620 | Conventional not available , FHA/VA only | N/A |

How Much Can a 630 Score Cost You Over Time

This is the number most borrowers never calculate before signing. On a $300,000 30-year fixed mortgage, a 630-score borrower pays approximately $150 to $200 more per month than a 760+ borrower. Over 30 years, that difference is $54,000 to $72,000. That is real money. It does not show up on the monthly statement as a separate line item , it is baked into the rate. But it compounds every single month for 30 years.

The practical implication: every month the score stays at 630 instead of 700 costs approximately $100 to $200. That is before any discussion of whether a refinance is possible or affordable later.

As Experian's mortgage rates by credit score data confirms, a score of 760 or higher is where borrowers access the best rates. The current average for a 700-score borrower is 6.76% (Curinos, May 2026). A 630-score borrower sits approximately one full percentage point above that.

Should You Buy Now or Improve Your Score First

Sometimes the right answer is buy now. Sometimes the math says wait. The decision depends on what caused the 630 score. If utilization is the problem, a 30-60 point gain is possible in a single billing cycle. A short wait could save $30,000 or more in lifetime interest. If the score is depressed by multiple collections that take 12-18 months to dispute, the wait is longer , and home price appreciation in the target market becomes part of the calculation.

- Home prices in the target market are rising faster than the rate savings would justify waiting

- Relocation is required , job move, family situation, lease ending

- Income is stable and the higher payment is affordable without financial stress

- The score improvement path is long (collections, charge-offs) and would take 12+ months

- Refinancing later is the plan , and income trajectory supports a refi in 2-3 years after score improves

- The primary cause of the 630 is high credit card utilization , fixable in 30-60 days with a 30-60+ point gain

- Reporting errors exist that can be disputed and corrected in 30-90 days

- One collection account is in dispute and likely to be deleted within 90 days

- Getting to 660+ or 680+ is realistic within 90-180 days , saving $25,000-$45,000 over the loan life

- Home prices in the target market are stable or flat

The Fastest Ways to Improve a 630 Credit Score Before Applying

From 630, the fastest improvements come from reducing credit card utilization, disputing reporting errors, and adding authorized user accounts. All three can move the score 20-60 points within 30-90 days. These actions do not require new accounts or hard inquiries. They work on the existing credit file.

- Pay credit card balances to under 10% of each card's limit. This is the fastest high-impact action available. If utilization is causing the 630, this fix alone can add 30-60 points in one billing cycle. Do it before the statement closes , that is when balances report to the bureaus.

- Dispute any inaccurate items. Pull all three bureau reports at AnnualCreditReport.com. Look for wrong dates, wrong balances, accounts not yours, and collections where reporting information does not match original documents. One corrected inaccuracy can add 15-50 points in 30-45 days.

- Add authorized user status on a low-utilization, long-history account. A family member with a 10+ year card at under 10% utilization and perfect payment history adds that account's weight to your credit file. Score improvement shows in 30-60 days. Impact: 20-40 points depending on the file.

- Avoid all hard inquiries for 60-90 days before applying. Each inquiry costs 5-10 points. Mortgage rate shopping is an exception , multiple mortgage inquiries within 14-45 days are treated as one inquiry by FICO. But opening credit cards, auto loans, or personal loans during this window damages the score you are trying to protect.

- Do not close old accounts. Closing an old account reduces available credit (hurts utilization) and may reduce average account age (hurts the account age factor). Both lower the score. Leave old accounts open even if unused.

For a complete timeline of how much each action can move a score , and how long each one takes to show up , the guide on realistic score improvement timelines breaks down the process by action type and starting score.

Why Some Borrowers With 630 Scores Get Better Rates Than Others

A 630 credit score is one data point. Lenders price the full picture. Two borrowers at 630 may receive meaningfully different rates based on down payment, debt-to-income ratio, reserves, employment stability, and whether collections appear on the file. The score triggers the LLPA tier. Everything else determines whether the lender applies additional overlays or compensating factors.

- Down payment size. A 20% down payment reduces LLPA charges compared to 5% down. A 630-score borrower who puts 20% down gets significantly better pricing than one putting 3.5% down. The down payment addresses the risk the score signals.

- Debt-to-income ratio. A 630-score borrower with a 28% DTI looks very different from one with a 48% DTI. Low DTI is a compensating factor that some lenders use to offset score concerns in pricing decisions.

- Cash reserves. Two months of mortgage payments in savings after closing signals financial stability. Six months of reserves is a strong compensating factor. Lenders view reserves as a buffer against missed payments.

- Employment history. Two or more years at the same employer , or in the same field , is a positive underwriting signal. Frequent job changes or recent self-employment transition raise underwriting concern at any score level.

- Collection accounts. A 630 with no collections looks very different from a 630 with three recent collections. The score may be the same. The underwriting risk is not. Collections create additional friction , some lenders require them paid before approval regardless of the credit score.

How Underwriters View a 630 Credit Score

To an underwriter, a 630 credit score is a yellow flag , not a red one. It requires explanation but does not automatically trigger denial. Underwriters look at the credit history behind the score, not just the number. A 630 from two years of rebuilding after one missed payment looks different from a 630 with three active collections and a recent charge-off. The score starts the conversation. The full file finishes it.

- Automated Underwriting Systems (AUS). Most loan applications go through Fannie Mae's DU or Freddie Mac's LP before a human sees the file. A 630 score often passes AUS with a "Refer with Caution" or conditional approval. The conditions become the underwriter's job.

- Manual underwriting. When AUS declines or issues significant conditions, the file goes to a human underwriter. At 630, manual underwriting is common on conventional loans. Manual underwriting requires more documentation , bank statements, employment letters, explanation letters for negative items , and takes longer to process.

- Compensating factors. An underwriter at 630 is looking for reasons to approve. Low DTI, large reserves, stable employment, low utilization, no recent lates, and a clean 12-month payment history all help. Collections , especially housing-related collections , work against the file significantly.

- Collection policy by loan type. FHA gives lenders discretion on collections. Many FHA lenders require collections over $1,000 to be paid or placed in a payment plan. Conventional lenders may ignore smaller non-medical collections under certain guidelines. Lender overlay rules override agency guidelines , and overlays at 630 are often strict.

630 Credit Score vs 680 Credit Score

| Factor | 630 Credit Score | 680 Credit Score |

|---|---|---|

| Conventional loan eligibility | Qualifies (above 620 minimum) | Qualifies comfortably |

| FHA loan eligibility | Yes , straightforward approval | Yes , stronger approval position |

| Estimated rate (30yr fixed) | ~7.55% (620-639 tier) | ~7.05% (680-699 tier) |

| Monthly payment ($300K loan) | ~$2,100 | ~$2,010 |

| Monthly difference | ~$90 less per month at 680 | |

| 30-year difference | ~$32,000 less total interest at 680 | |

| Underwriting friction | More , closer to minimum thresholds | Less , inside comfortable approval range |

| PMI cost (5% down, conventional) | Higher PMI rate | Lower PMI rate |

| Timeline to reach 680 from 630 | Typically 2-6 months with utilization reduction and clean payment history | |

What Credit Score Gets the Best Mortgage Rates

760 or higher. That is the threshold where LLPA surcharges drop to their minimum and lenders offer the most competitive pricing. Going above 760 to 800 or higher produces minimal additional rate improvement. The biggest rate gains come in the 620-760 range. Every 20-point tier crossed in that range reduces the rate meaningfully. Going from 630 to 680 saves more than going from 760 to 800.

There is a misconception that a perfect 800 score is necessary for the best rates.

It is not. The threshold is 760. Everything above that is in the same pricing tier. The rate improvements between 760 and 850 are negligible.

The real work is in the 600s. Getting from 630 to 680 saves real money. Getting from 680 to 720 saves more. Getting from 720 to 760 saves the most. After 760, the savings on rate pricing stop compounding significantly.

As the ConsumerAffairs mortgage rate analysis confirms, improving from 620 to 760 saves approximately $156 per month and $56,103 in total interest on a $300,000 loan , and the biggest jumps happen in the lower tier crossings.

Understanding what each score tier actually means for real borrowing decisions , including which rate and approval tiers open at 580, 620, 660, 700, and 740 , is covered in detail in the guide on what each credit score range means financially.

Is a 630 Credit Score Good Enough to Buy a House

Yes. Many people buy homes with 630 credit scores every year. The approval is real. The mortgage is real. The house is real. What is also real: the rate premium. The question is not whether 630 is good enough to qualify. The question is whether improving the score first would save enough money to justify the wait. For many borrowers, even a 30-60 day delay for a 30-point score improvement saves $25,000-$40,000 over the life of the loan.

| Mortgage Readiness Factor | Why It Matters | 630 Score Borrower Checklist |

|---|---|---|

| Credit score | Rate pricing and LLPA tier | 630 qualifies , but carries rate premium |

| Debt-to-income ratio | Primary approval factor | Keep under 43% (36% is better) |

| Down payment | Reduces LLPA and PMI cost | More down = lower rate , even 1-2% more helps |

| Collections on file | Underwriting concern , especially housing | Address before applying if possible |

| Cash reserves | Compensating factor | Aim for 2-6 months of mortgage payment in savings |

| Employment history | Repayment confidence | 2+ years same employer or same field preferred |

What mortgage rate can I get with a 630 credit score?

In the current rate environment (May 2026), a 630 score places a borrower in the 620-639 LLPA tier for conventional loans. This typically produces a rate approximately 0.75 to 1.10 percentage points higher than the best rate tier (760+). With a 700-score conventional rate of approximately 6.76% (Curinos/Experian, May 2026), a 630 borrower is looking at roughly 7.30 to 7.65% on conventional. FHA rates at 630 may be 0.25-0.50% lower before mortgage insurance is factored in. These rates change daily , get quotes from multiple lenders.

Can collections affect mortgage approval at 630?

Yes , significantly. At 630, underwriters are already scrutinizing the file. Collections add friction. FHA lenders commonly require collections over $1,000 to be paid or in a payment plan before closing, regardless of the credit score. Conventional lenders may ignore individual small collections under $2,000 per Fannie Mae guidelines, but many apply their own stricter overlay policies. Apartment and housing-related collections receive the heaviest scrutiny because they directly signal prior housing payment failure. Address collections before applying when possible.

Does debt-to-income matter more than credit score for a mortgage?

They serve different functions. Credit score determines the rate. DTI determines whether the payment is affordable at that rate. A 630 score with a 30% DTI may get approved and receive a high rate. A 630 score with a 49% DTI may get declined regardless of the rate offered. Both factors are necessary , but they control different parts of the mortgage decision. Lenders approve applications where the DTI works at the rate the score tier produces. If the rate from a 630 score makes the DTI too high, the application fails regardless of score.

How fast can I raise a 630 credit score for a mortgage?

If high credit card utilization is the cause, 30-60 points are achievable in a single billing cycle , 30 to 60 days. That alone could move a 630 to 660-690 and change the rate tier. If the score is depressed by collections, the timeline extends to 3-12 months for dispute resolution. The fastest path from 630 to 680 (saving approximately $32,000 over 30 years) typically takes 2-6 months with utilization reduction and one or two dispute wins. Get a full three-bureau report first to understand the specific cause before planning the timeline.

-

How Long Does It Take to Increase a Credit Score? Realistic Timelines If a 60-90 day score improvement makes financial sense before applying, this covers the exact timelines for each action , utilization reduction, dispute wins, authorized user additions, and credit builder accounts. The same framework applies at 630. If utilization is the cause of the 630, a 30-60 point jump in one billing cycle is realistic , and the difference between 630 and 680 saves approximately $32,000 over the life of a $300,000 mortgage.

-

Credit Score Ranges , What Each Tier Opens and What It Costs 630 is one score. This covers what changes at 660, 680, 700, 720, and 740 in terms of real-world rate pricing, loan program access, and approval odds. Knowing the specific financial difference between each 20-point tier makes the "buy now or wait" decision concrete rather than abstract. The rate savings at each tier crossing are documented with estimated dollar impact on a $300,000 mortgage.

-

Good Credit Building Cards and Accounts for 2026 For borrowers who decide to wait 60-90 days and improve the score before applying, this covers the specific accounts that produce the fastest credit improvement from the 600s , installment builders that report to all four bureaus, secured revolving accounts, and authorized user strategies. The goal before a mortgage application is not long-term building. It is the fastest possible jump within the 60-90 day pre-application window.