The average car loan interest rate for 730 credit score usually falls in the prime borrower range, which means lower rates than most buyers get, but not always the absolute lowest advertised offers.

In 2026 market data, borrowers in the broad prime tier often see rates around the mid-6% range for new cars, while used car rates are usually higher. Exact pricing depends on the lender, loan term, down payment, and vehicle age, not just the score alone.

I own a credit repair company, and before that, I worked in a car dealership finance environment. One thing I learned fast: a 730 score gets you in the door, but your full file decides the real rate. I saw buyers with a 730 get excellent financing because they had low debt, stable income, and money down.

I also saw buyers with the same score get weaker terms because they carried high balances or stretched the loan too long. Same score. Different file. Different outcome.

Real buyer discussions on Reddit show the same pattern. Many shoppers assume a 730 automatically gets the best rate. It often gets close, but lenders still price risk based on the full application. That includes debt-to-income ratio, recent inquiries, trade line depth, and whether the car is new or used.

The better question is not only what rate a 730 score gets, but how to make that 730 score qualify for the best possible offer.

So, let’s talk about it. What’s the average car loan interest rate for a 730 credit score.

I worked the finance desk at a dealership before starting ASAP Credit Repair. I know exactly how this works from the inside. When a 730-score buyer sits down with the F&I manager, that manager has discretion to mark up the rate by 1-3% above what the lender approved. It is legal. It is common. And buyers at 730 are prime targets because they qualify easily but often do not know their actual approved rate. A customer who walked in pre-approved at 6.2% from their credit union forced the finance manager to compete. That is the only move that works.

Average Car Loan Interest Rate for 730 Credit Score

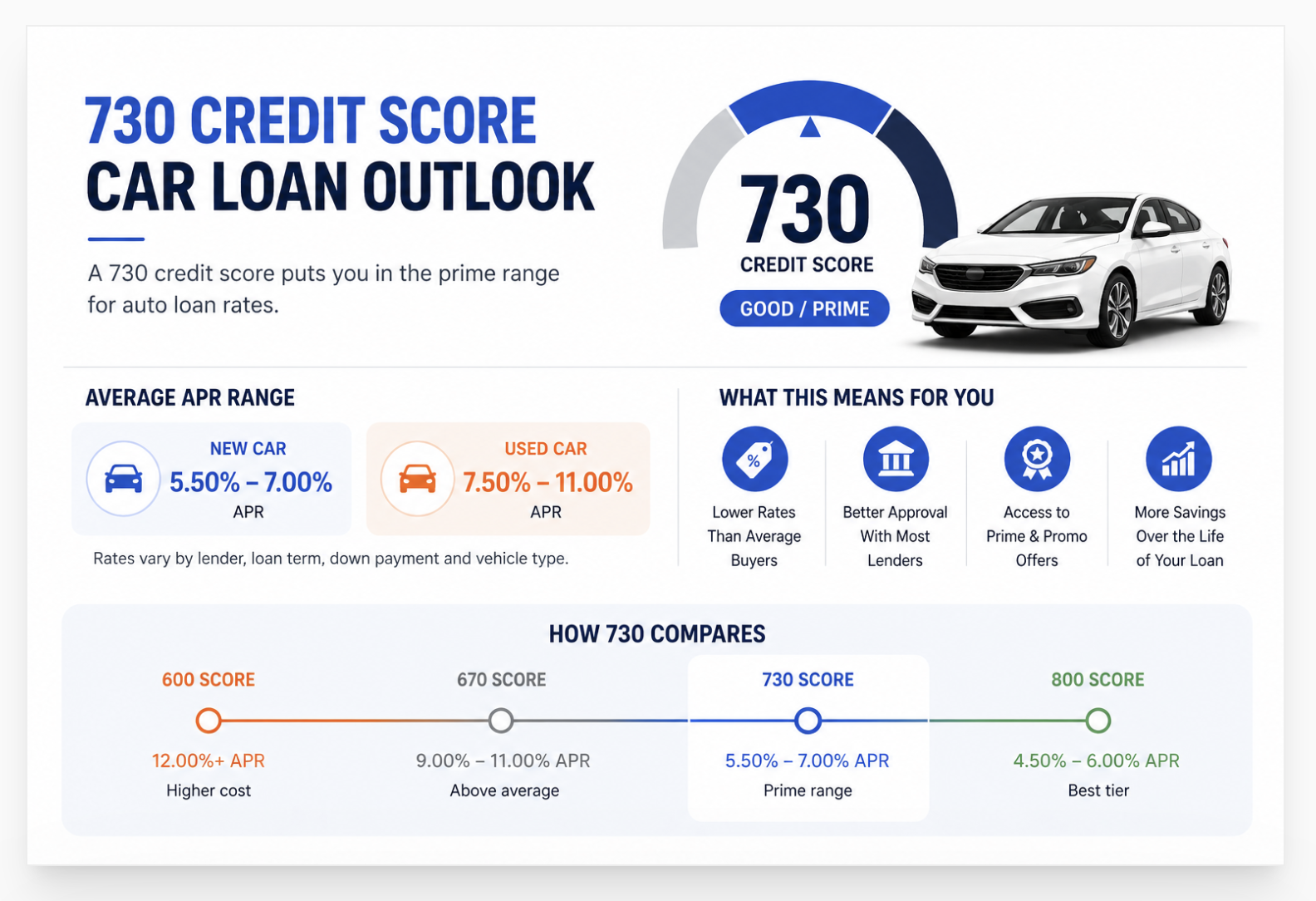

The average car loan interest rate for a 730 credit score is approximately 6.51% for a new car and 9.65% for a used car, based on Experian's Prime tier data (661-780 score range) for Q3 2025. At 730, you qualify for prime lending rates. Most banks and credit unions will offer you between 5.5% and 7.5% on a new vehicle depending on loan term and lender.

A 730 score falls squarely in the Prime tier. Experian's auto finance market data uses VantageScore bands, and the Prime tier runs from 661 to 780. At 730, you sit toward the upper half of that band. You are not at the super-prime level (781+), but you are significantly better positioned than the near-prime borrowers one tier below you.

Here is what that looks like in real rate terms across all five credit tiers for Q3 2025:

| Credit Tier | Score Range | New Car APR | Used Car APR |

|---|---|---|---|

| Super Prime | 781-850 | 4.88% | 7.43% |

| Prime (730 is here) | 661-780 | 6.51% | 9.65% |

| Near Prime | 601-660 | 9.77% | 14.11% |

| Subprime | 501-600 | 13.18% | 18.86% |

| Deep Subprime | 300-500 | 15.85% | 21.60% |

The rate gap between Prime and Near Prime is the most impactful in the chart. Going from 660 to 661 saves you 3.26 percentage points on a new car loan. On a $30,000 vehicle at 60 months, that single point boundary costs over $4,800 in total interest. Protecting a 730 score , keeping it above 720 , is a genuine financial priority before any auto purchase.

A 730 credit score places you in the Prime tier with an average new car rate of 6.51% and used car rate of 9.65% as of Q3 2025. You sit above the overall market average. The gap between your rate and Super Prime is 1.63 percentage points on a new car. The gap between your rate and Near Prime below you is 3.26 points , protecting your 730 score before applying matters enormously.

What Interest Rate Can I Get With a 730 Credit Score for a Car?

With a 730 credit score, expect 5.5% to 8% on a new car loan and 9% to 11.5% on a used car loan, depending on lender, term, and down payment. Credit unions offer the lowest rates at this tier , often 0.5% to 1.5% below dealership finance rates. Get pre-approved before visiting a dealership.

The 6.51% average is exactly that , an average. The rate you personally receive depends on several things beyond your credit score.

Loan term matters. Shorter terms carry lower rates. A 36-month new car loan at 730 may come in at 5.5-6%. A 72-month loan at the same score may run 6.8-7.5%. Lenders price longer terms higher because they carry more default risk over time.

Down payment matters. A larger down payment reduces the loan-to-value ratio. Lenders see lower LTV as less risky. Putting 15-20% down on a new car with a 730 score can push your rate toward the lower end of the prime tier.

Lender type matters most. This is where I want to be direct based on my experience on the finance desk. When a dealership quotes you a rate, that rate is usually higher than what the lender actually approved. The finance manager is authorized to mark up the buy rate , the actual lender rate , by up to 2-2.5% in many states. They keep the difference as profit. A 730-score buyer who qualified for 6.2% from the bank may be quoted 7.8% at the desk.

As NerdWallet's auto loan rate guide confirms, comparing lender offers is the single most effective way to reduce your rate at any credit tier. At 730, you have enough score to get multiple competing pre-approvals , use them.

Where to Get the Best Rate at 730

- Credit unions: Consistently offer the lowest rates for prime-tier borrowers. Members typically receive rates 0.5-1.5% below bank and dealer rates. If you are not a member of a credit union, joining one before a car purchase is worth the effort.

- Bank pre-approval: Apply for pre-approval with your existing bank. This gives you a baseline rate and a hard number to use at the dealer.

- Online lenders: LightStream, PenFed, and Autopay all offer competitive rates at 730 and allow pre-approval without hard inquiry in some cases.

- Dealer financing: Use only as a last resort or as a competing quote. Never accept the first rate offered. Ask what the buy rate was and what markup they added.

How Much Is a $25,000 Car Loan for 72 Months?

A $25,000 car loan at 72 months costs approximately $422 per month at the prime average rate of 6.51%. Total interest paid is approximately $5,372. At 8% APR, the monthly payment rises to $438 and total interest reaches $6,536. The difference between 6.51% and 8% on a 72-month $25,000 loan is $1,164 in total interest.

The 72-month term is where I want to be honest with you. As someone who sat on the finance side of a dealership, the 72-month loan was always the finance manager's best friend. It lowers the monthly payment, which makes expensive cars feel affordable, while quietly adding hundreds more in interest and tying you to the loan for two extra years. If your vehicle depreciates faster than you pay down the loan , which is common on new cars , you end up underwater: owing more than the car is worth.

At a 730 score, you qualify for the 60-month term at a lower rate. The monthly payment is higher on a 60-month than a 72-month, but total interest drops significantly. On a $25,000 loan at 6.51% APR: 60 months costs $4,488 in total interest versus $5,384 at 72 months. That $896 difference comes just from the term, not the rate.

If the 72-month payment is the only way the car fits your budget, the car may be priced above what makes financial sense for your income. That is the honest answer the F&I manager will not give you.

A $25,000 72-month car loan at the prime average rate of 6.51% costs $422/month with $5,384 in total interest. At 8% APR , common when a dealer marks up the buy rate , the same loan costs $6,536 in interest. The 60-month term at 6.51% saves $896 in interest on the same loan amount. Always run the total interest number, not just the monthly payment.

Is 7% Interest on a Car High?

For a 730 credit score on a new car, 7% is slightly above the prime average of 6.51% , not ideal, but not a deal-killer. For a used car at 730, 7% is actually below the prime average of 9.65%, making it a strong deal. Whether 7% is high depends on the lender's buy rate at your score. If your approved rate was 6.2% and the dealer quoted 7%, they added 0.8% markup , that is worth negotiating down.

Context is everything here. The word "high" only has meaning relative to what you actually qualify for.

For new cars: at a 730 score, the prime tier average is 6.51%. Seven percent is 0.49 points above that. On a $25,000 60-month loan, the difference between 6.51% and 7% is $5 per month and $300 in total interest. It is not a disaster, but it is not the best you can get either.

For used cars: at a 730 score, the prime average for used vehicles is 9.65%. Getting 7% on a used car loan with a 730 score is an excellent outcome. Either your bank or credit union gave you a great deal, or the car qualifies for manufacturer certified pre-owned financing that carries a promotional rate.

The more important question than "is 7% high?" is "is 7% the best I can get?" Pull your credit score before you apply. Know what tier you fall in. Call your credit union and ask for their best rate at that tier. Then compare.

As Bankrate's 2026 auto loan rate analysis notes, borrowers who shop multiple lenders before visiting a dealership consistently secure lower rates than those who rely on dealer financing alone. At 730, you have strong enough credit to make every lender compete for your business. Make them compete.

What Is a Good APR for a 72-Month Car Loan?

A good APR for a 72-month new car loan in 2026 is at or below 6.86%, based on Experian market data. For a used car, a good APR is below 12.80%. For a 730 credit score specifically, getting 6-7% on a 72-month new car loan is competitive. Getting below 6.5% at a credit union is achievable. Anything above 8% on a new car at 730 worth negotiating down.

The 72-month term carries a natural rate premium. Lenders charge more for longer terms because default risk accumulates over time. Per Experian's auto loan rate breakdown, the average APR for a 72-month new car loan is approximately 6.86% as of 2025 across all credit tiers. For a 730-score prime borrower specifically, 6.3-6.8% is a realistic target on a 72-month new car loan from a competitive lender.

One important note on 72-month loans: lenders sometimes offer better rates on shorter terms as an incentive to reduce their own exposure. If you are choosing between a 60-month at 6.2% and a 72-month at 6.86%, the 60-month at a lower rate saves money two ways , lower rate and fewer months of interest. The only reason to choose 72 months is if the monthly payment genuinely requires it for your budget.

| Loan Term | Avg APR (730 score range) | Monthly (on $25K) | Total Interest |

|---|---|---|---|

| 36 months | ~5.5-6.0% | ~$758 | ~$2,288 |

| 48 months | ~5.8-6.3% | ~$587 | ~$3,176 |

| 60 months | ~6.2-6.7% | ~$484 | ~$4,040 |

| 72 months | ~6.5-7.0% | ~$422 | ~$5,384 |

| 84 months | ~7.0-8.0% | ~$381 | ~$7,004 |

How Your 730 Score Affects Total Car Cost , Not Just the Rate

Three things a 730-score buyer should do before any auto purchase:

1. Pull your actual mortgage-model FICO scores. Auto lenders use FICO Auto Score 2, 4, or 8 , not the score on Credit Karma (which is VantageScore 3.0). Your FICO Auto Score at 730 VantageScore may be 710 or 745 , the models weight auto payment history differently. A client who came to us with a 730 VantageScore had a 698 FICO Auto Score because of one old auto late payment that the auto scoring model weighted more heavily. That difference moved them from one rate tier to another. Pull myFICO.com for the auto-specific score before applying.

2. Get pre-approved at a credit union or bank the week before you shop. The pre-approval takes 10 minutes and gives you a rate the dealership must beat. The pre-approval also limits your hard inquiries , multiple auto loan applications within 14-45 days typically count as one inquiry under FICO's rate-shopping rules.

3. Check your credit report for errors before applying. Inaccurate late payment notations, wrong balances, or duplicate collection accounts can suppress your auto-specific FICO score below where your VantageScore suggests the score suggests. Disputing and removing inaccurate entries before a car purchase can move your qualifying score up enough to cross into a better rate tier. Our guide on the complete guide to car loan requirements covers exactly what auto lenders check beyond the credit score , including employment verification, income documentation, and the vehicle inspection process that affects your rate.

For buyers who want a car now but have a score lower than 730, our article on getting a car loan with bad credit and no down payment covers the lender landscape for subprime and near-prime borrowers, and what compensating factors (income, employment history, references) move the needle when the score alone does not qualify for prime rates.

And if you have ever missed payments on a prior vehicle , or if you are concerned about what happens to your credit if you face payment trouble on the current loan , our breakdown of voluntary surrender vs repossession explains how each affects your credit report, your deficiency balance, and your ability to get future financing.

What interest rate can I get with a 730 credit score for a car?

With a 730 credit score, expect rates of 5.5% to 8% on a new car and 9% to 11.5% on a used car, depending on the lender and loan term. The prime tier average as of Q3 2025 is 6.51% new and 9.65% used (Experian data). Credit unions consistently offer the lowest rates in the prime tier. Always get a pre-approval from your bank or credit union before visiting a dealership , the pre-approval letter forces the finance desk to compete rather than markup freely.

How much is a $25,000 car loan for 72 months?

A $25,000 72-month car loan at the prime average rate of 6.51% produces a monthly payment of approximately $422 and total interest of $5,384. At 7% APR, the monthly payment rises to $427 and total interest to $5,744. At 8% APR, the payment is $438 and total interest is $6,536. The 72-month term carries higher rates and more total interest than shorter terms. At 730, a 60-month loan at a lower rate saves approximately $1,300-$1,500 in total interest compared to 72 months.

Is 7% interest on a car high?

For a new car loan with a 730 credit score, 7% is slightly above the prime average of 6.51% , negotiable but not alarming. For a used car, 7% is well below the prime average of 9.65% , that is an excellent deal. Whether 7% is high depends on what rate your lender actually approved. Ask the dealer for the "buy rate." If your lender approved you at 6.2% and the dealer quoted 7%, they added 0.8% markup. That is $600-$1,000 in extra interest on a $25,000 loan. Push back.

What is a good APR for a 72-month car loan?

A good APR for a 72-month new car loan in 2026 is at or below 6.86% based on Experian market data. For a used car, a good APR on a 72-month loan is below 12.80%. With a 730 score, getting 6% to 6.8% on a 72-month new car loan from a credit union is achievable. Anything above 8% on a new car at 730 is a sign either of a dealer markup or a lender pulling a less favorable FICO Auto Score than your VantageScore suggests. Shop multiple lenders before accepting any single quote.

Your FICO Auto Score May Be Lower Than Your Credit Karma Number

Auto lenders pull FICO Auto Score 2, 4, or 8 , not the VantageScore you see on free apps. If your actual auto-scoring FICO is suppressed by an inaccurate late payment or old collection, you may qualify for a worse rate than your score suggests. A free 3-bureau audit shows every entry across Equifax, Experian, and TransUnion , including what drags your auto-specific score below your prime-tier rate.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

Carter Young Inc.: What This Debt Collector Can Do and How to Fight Back Collection accounts , especially housing debt , lower your FICO Auto Score the same way they lower your general credit score. Before applying for a car loan, any active collection on your report will affect your rate tier. This covers how to validate, dispute, and negotiate deletion of collection accounts before they cost you thousands on an auto loan.

-

796 Credit Score: You're Already in the Top Tier. Here's the Proof. A 730 score places you in the Prime tier at 6.51% new car APR. A 796 score places you near the Super Prime boundary where rates start dropping below 5%. This covers exactly what the rate difference looks like between 730 and 796, which specific score thresholds produce rate changes at auto lenders, and the fastest ways to move from Prime to near-Super-Prime territory.

-

Auto Loan Defaults in Phoenix: What's the Timeline Before Repo Understanding what happens if you miss payments on an auto loan is as important as getting a good rate. This covers Arizona's self-help repossession law, the exact day-by-day timeline from missed payment to tow truck, what a deficiency balance means for your finances, and how the credit damage from a default affects your ability to get another car loan within the next 2-7 years.