A debt collection agency is a company that tries to recover unpaid debt for creditors or purchases delinquent accounts and attempts to collect the balance itself.

If you've received a collection call, letter, text message, or noticed a collection account on your credit report, you're not alone. Millions of Americans deal with debt collectors every year over credit cards, medical bills, personal loans, auto loans, and utility accounts.

One of the biggest misconceptions is that the company contacting you is the lender you originally owed. Most like not. A delinquent account is usually transferred to a third-party collection agency or sold to a debt buyer that now owns the account.

Understanding how debt collection agencies work, what rights they have, and what rights you have under federal law can help you avoid mistakes that may damage your credit or cost you money.

Before responding to a collector, you must know who they are. Plus, whether the debt is accurate, and what options are available to you.

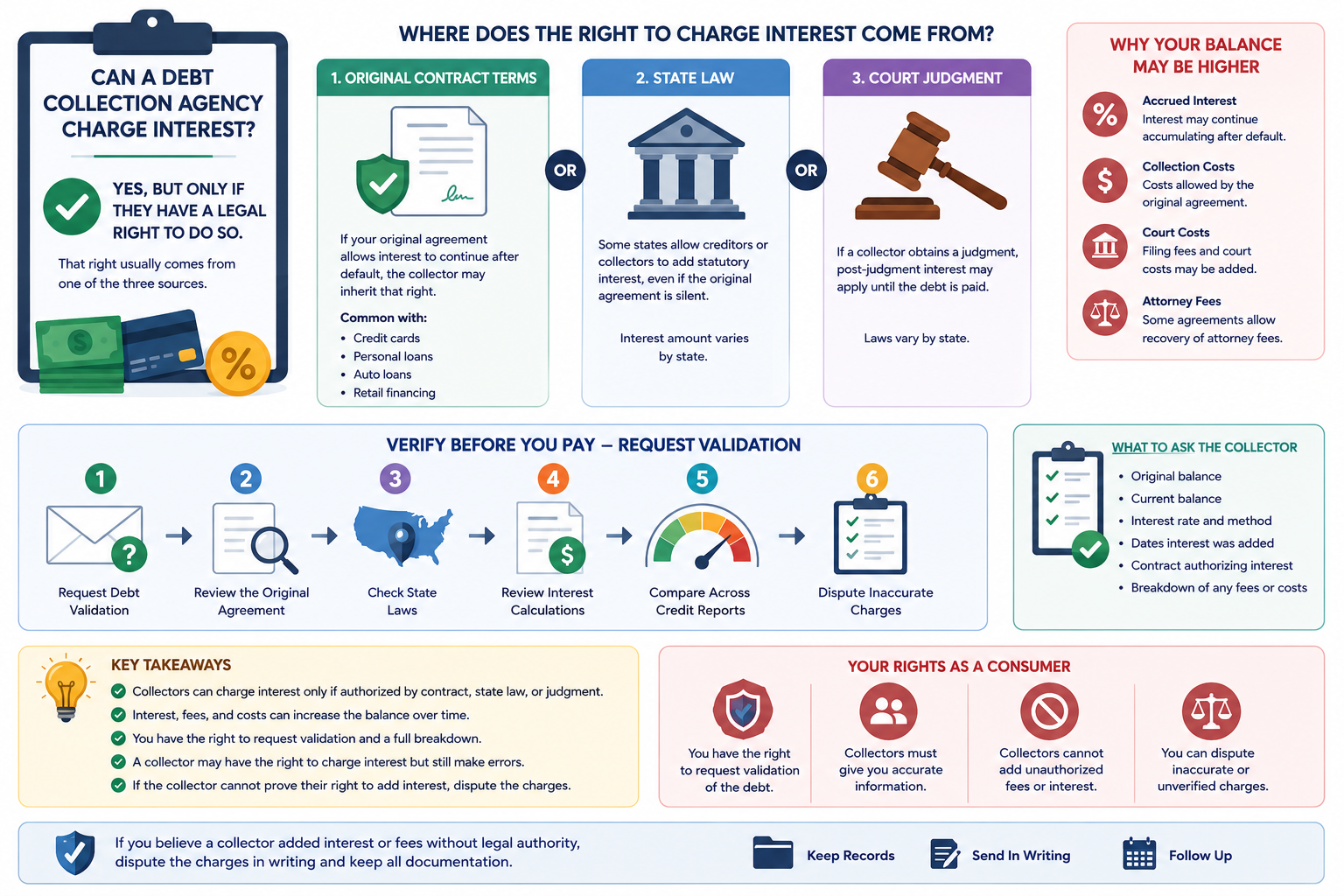

Yes, a debt collection agency may be able to charge interest, but only under certain circumstances. We created the infographic below about debt collectors charging interests.

TL;DR , Quick Answer

Yes. A debt collector can charge interest. But only when the law allows it. The authority to add interest must come from the original contract, state law, or a court judgment. Without one of those three sources, adding interest may violate the FDCPA. And even when a collector has the right to charge interest , the amount still has to be calculated correctly. Wrong rate or wrong start date is where most collection balance disputes actually win.

JM

Joe Mahlow | Founder and CEO, ASAP Credit Repair USA

20+ Years in Credit Repair | CROA Registered | FDCPA and FCRA Specialist | 100,000+ Files Reviewed

Founded ASAP Credit Repair

20+ Years Experience

FDCPA and FCRA Expert

100,000+ Files Reviewed

CROA Registered

Joe Mahlow | On Collection Interest Charges

"The consumers that comes to us about a growing collection balance usually haven't requested validation yet. They just see the number going up. They assume it's illegal. Sometimes it is. But often the collector had the right to acrue interest from the origional contract. The question I always ask is not 'can they charge interest.' The question is 'did they calculate it correctly.' That's where the real disputes are. We've had files where the collector had every right to charge interest under the credit agreement , but they applied the wrong rate. Or they started accruing from the wrong date. That miscalulation is an FDCPA violation even when the interest itself was legitamate."

Direct Answer , Can a Debt Collection Agency Charge Interest?

Yes , but only when there is a legal basis. A debt collector can add interest if the original credit agreement permits it, state law allows it, or a court judgment creates that right. Without one of these three sources, adding interest may violate the FDCPA. And having the right to charge interest is not the same as charging the correct amount. Both need to be verified.

CFPB complaints about debt collection practices in 2025 , NerdWallet via CFPB Annual Report

400K

Nearly 400,000 consumers filed CFPB complaints about debt collectors in 2025. Balance disputes , including unexplained interest charges , are among the most common issues reported. Filing a CFPB complaint is a formal escalation option when a collector cannot explain the balance.

U.S. household debt in Q1 2025 , Bankrate via Federal Reserve Bank of New York

$18.2T

Household debt hit $18.2 trillion in Q1 2025 with a delinquency rate of 4.3%. More delinquencies mean more accounts going to collections , and more balances that may be growing through contract interest, fees, and statutory charges.

FDCPA section governing what collectors can charge , 15 U.S.C. § 1692f(1)

§808

FDCPA Section 808(1) makes it illegal for a collector to collect any amount, including interest and fees, that is not "authorized by the original agreement or permitted by law." This is the specific legal test for whether collection interest is lawful.

The Three Legal Sources That Allow Collectors to Charge Interest

Think of it this way. A collector cannot invent new charges. Every fee or interest amount needs a legal basis. That basis comes from one of three places.

📄

The Original Contract

Many credit agreements say interest continues after default. When a debt is sold to a collector, that right transfers with it.

Example: A credit card agreement with 29.99% post-default interest , the collector can apply that rate.

⚖️

State Law

Some states set a statatory interest rate for collection debts. This applies even when the original contract is silent on post-default interest.

Example: A state allows 6% per year on unpaid debts , a collector can apply that rate regardless of the contract.

🏛️

Court Judgment

When a collector wins a lawsuit, the judgment earns post-judgment interest in most states. This continues until the judgment is paid.

Example: A $5,000 judgment earning 8% per year adds $400 annually until paid in full.

What the FDCPA says: Under Section 808(1), collecting any amount , including interest , that is not authorized by the original agreement or permitted by law is a federal violation. If a collector cannot point to one of these three sources, the charge may not be lawful.

Why Is My Collection Balance Higher Than What I Originally Owed?

A balance can grow for several reasons. Each one needs a legal basis to be valid.

What Makes a Collection Balance Go Up

Accrued interest

Interest continues to acrue after default when the original contract permits it. For credit cards, post-default rates are often 25% to 30% per year. That adds up fast. A $3,000 balance at 28% adds $840 per year.

Collection costs

Some contracts allow the creditor to recover collection expenses. These costs transfer to the collector when the debt is sold. Review the original agreement to see if this language exists.

Attorney fees

If the original agreement includes an attorney fee provision, legal costs for collection action may be added to the balance. This is more common in auto loans and commercial agreements than in credit cards.

Check: Does the contract say "attorney fees will be added if collection action is required"?

Court costs and judgment interest

If the collector filed a lawsuit and won, court filing fees and post-judgment interest are added to the balance. In most states, judgment interest runs automatically until the judgment is paid.

A consumer who ignores a lawsuit may face a growing judgment balance for years.

Contract Interest vs Statutory Interest vs Judgment Interest

Contract Interest

Source: Written terms in the original credit agreement

Rate: Whatever the contract specifies , often 25% to 30% for credit cards

Verification: Request a copy of the origional credit agreement and find the post-default interest clause

Transfers: Yes, to debt buyers when the account is sold

Statutory Interest

Source: State law , applies when the contract is silent

Rate: Set by each state , varies from 5% to 12% per year typically

Verification: Look up your state's civil interest statutes or contact a consumer law attorney

Transfers: Yes, state law applies to the debt regardless of who owns it

Judgment Interest

Source: Court judgment after the collector won a lawsuit

Rate: Set by state law for post-judgment interest , varies widely

Verification: Review the court judgment document , it states the interest rate

Transfers: The judgment belongs to whoever holds it; may be renewed in many states

Real Example: Collection Balance Grew by $2,000 Over Four Years

Case Study , From ASAP Credit Repair File Review

$7,500 Original Balance. $9,500 Four Years Later. Was It Legal?

1

The situation: A consumer defaulted on a $7,500 credit card balance. Four years later, a debt buyer reported a balance of $9,500 on all three bureaus. The consumer thought this was illegal.

2

What the consumer did: Sent a debt validation request to the collector. Asked for the origional credit agreement, the interest rate applied, and a full calculation showing how $7,500 became $9,500.

3

What the collector sent back: The origional credit card agreement with a post-default interest clause at 28% per year. A calculation showing four years of interest: $7,500 × 28% × 4 years = $8,400 in interest alone. The extra $2,000 was legitimate under the contract.

4

The lesson: The balance increase was legal. The consumer hadn't read the origional credit agreement closely enough to know the post-default interest clause existed. Requesting validation first revealed whether the charge was valid , before any dispute was filed.

"My $1,800 collection turned into $2,700 over three years. Sent a validation request. They sent my original credit card agreement , 29.99% post-default interest. They had the right. BUT they were charging 32%. The rate didn't match the contract. I pointed that out. They couldn't explain it. Removed all the interest charges and we settled for the original $1,800. The lesson: they had the right to charge interest. They just charged the wrong rate."

r/personalfinance · collection interest dispute thread, 2025

Contract rate: 29.99%. Collector applied: 32%. FDCPA violation on the rate, not the interest itself. Interest removed, settled at original balance.

Information Gain , What Most Consumers Miss

The question isn't "can they charge interest?" , it's "did they calculate it correctly?"

A collector can have the legal right to charge interest and still be charging the wrong amount. These are two separate questions. Both need to be verified.

Common calculation errors in collection interest charges:

- Wrong interest rate. The collector applied a rate higher than what the origional contract specifies.

- Wrong start date. Interest was calculated from the wrong date , often the charge-off date instead of the first delinquency date, or vice versa.

- Duplicate charges. The same fee appears twice in the balance breakdown.

- Charges not in the contract. Fees that the origional agreement doesn't authorize , like collection costs for calling you.

- Interest on interest. Some collectors compound interest in a way the contract didn't authorize.

A collector may have every right to charge interest under the contract , and still violate the FDCPA by calculating it incorrectly. The dispute is in the math, not the principle.

Medical Debt , Different Rules Apply

Medical debt collection follows different rules than credit card or personal loan debt.

A hospital or healthcare provider may charge interest before sending the debt to collections. But the collection agency that buys the medical debt may have less authority to add new interest on top.

State laws on medical debt interest vary. Some states limit what collectors can charge on medical debt. Some hospitals include interest language in their patient billing agreements. Others don't.

If you have a medical collection with a growing balance, request the origional patient billing agreement from the healthcare provider , not just the collector. That document shows what interest authority exists at the source.

Medical collections under $500 are excluded from credit reports under rules that took effect in 2023. VantageScore 3.0 and 4.0 ignore all medical collection debt. If your growing collection is medical, check whether it should even appear on the report at all before disputing the interest amount.

Is Your Collection Balance Growing and You Don't Know Why?

Joe Mahlow's team at ASAP Credit Repair reviews collection balances against the origional agreement, the interest calculation, and applicable state law to identify whether the increase is valid or disputable.

Get a Free Credit Review →

How to Dispute Interest Charges on a Collection Account

As Experian confirms, both state and federal laws regulate the fees a collection agency can charge , and if you disagree with the amount, you have the right to contact the collector for clarification and documentation.

Send a written debt validation request

Write to the collector and ask for: the original balance, the current balance, the interest rate applied, the legal basis for the interest (contract clause or state statute number), and a full calculation showing how the current balance was reached. Send by certified mail with return receipt. The

debt validation guide covers exactly what collectors are required to provide and what to do when they don't.

Review the origional credit agreement

Find the post-default interest clause. It may say something like "after default, interest will continue at the contract rate." Note the exact rate. Compare it to the rate the collector applied. If the rates don't match, that difference is your dispute.

Check your state's interest laws

If the contract is silent on post-default interest, the collector can only charge what state law allows. Look up your state's civil interest statute , most state attorney general websites have this. If the collector is charging more than the statatory rate, that excess is not authorized.

Dispute inaccurate balances with all three bureaus

If the collection balance on your credit report doesn't match the documentation the collector provided, dispute the balance discrepancy with Equifax, Experian, and TransUnion. Attach the collector's own balance documentation showing the discrepancy. A balance the collector itself reported differently in different places is a strong dispute.

File a CFPB complaint if the collector can't explain the balance

As

NerdWallet confirms, the CFPB received nearly 400,000 debt collection complaints in 2025 , making it one of the largest consumer complaint categories. File at consumerfinance.gov/complaint. Reference FDCPA Section 808(1) and explain that the collector cannot document the legal basis for the interest charges.

As Bankrate's FDCPA guide confirms, the FDCPA limits how collectors can contact you and allows you to dispute debts , and having records of all communication with the collector is one of the most important protections you have if a balance dispute becomes a legal matter.

Decision Framework , What to Do Based on Your Situation

What Are You Dealing With? Here Is Your Next Step.

Balance is higher than expected and I don't know why

Send a debt validation request immediately. Ask for the full balance breakdown, interest rate applied, and legal basis for every charge. Don't dispute or pay until you have the documentation.

Collector provided documentation , the interest is in the contract

Verify the rate in the documentation matches what they applied. Verify the start date. Verify no fees appear twice. If everything matches the contract, the interest is likely legitamate. If anything doesn't match, dispute that specific discrepancy.

Collector cannot explain the balance or refuses to provide documentation

File a CFPB complaint at consumerfinance.gov. Dispute the balance with all three bureaus under FCRA. If the collector cannot validate the interest calculation, the charge may be an FDCPA violation.

The balance is from a court judgment

Request a copy of the judgment from the court. Note the judgment date, the judgment amount, and the state's post-judgment interest rate. Calculate what the balance should be based on those numbers. If the collector is charging more than that calculation shows, the excess may not be authorized.

The collection is medical debt

Request the origional patient billing agreement from the healthcare provider. Check whether it authorizes interest. Check whether the collection is for under $500 , those are excluded from credit reports entirely. Check whether your state has medical debt interest restrictions.

Joe Mahlow | Pattern Observation , Collection Interest Disputes

"We see two types of growing collection balances at ASAP. The first type: the collector had the right to acrue interest under the contract, they applied the correct rate, and the math checks out. The consumer didn't like it but the balance was valid. The second type: the collector had partial or no authority , maybe they applied a rate above the contract rate, or started the interest clock from the wrong date, or added charges not in the origional agreement. That second type is where disputes produce results. The challenge is that you can't tell which type you have until you request the documentation and check the math yourself. Most consumers skip that step. They either pay without checking or dispute without documenting. Neither approach is optimal."

Related Questions

Does interest continue after a charge-off?

Yes, in many cases. A charge-off is an accounting event , the original creditor writes the debt off their books as a loss. It doesn't erase the debt. It doesn't stop interest from accruing if the original contract or state law permits it. The debt still exists. The collector who bought it still has the rights the original creditor had. That includes the right to charge interest if the contract allows it. So a charge-off that happened at $3,000 may be collected as $4,200 several years later.

Can a debt buyer charge more interest than the original creditor?

No. A debt buyer acquires the same rights the origional creditor had , not more. If the contract specified a 25% post-default rate, the debt buyer can charge 25%. They cannot charge 30% simply because they purchased the debt. The terms of the origional agreement set the ceiling. Any charge above that ceiling may violate the FDCPA.

Can I settle a collection for less than the full balance including interest?

Yes. Most collection accounts , including those with substantial accrued interest , are negotiable. Debt buyers purchase accounts for cents on the dollar. They have room to settle for less than the full balance. Settlements at 40% to 60% of the total balance are common for older debt or accounts where validation documentation is incomplete. Always get any settlement agreement in writing before making a payment.

Key Takeaways

- Collectors can charge interest only when authorized by the original contract, state law, or a court judgment

- FDCPA Section 808(1) prohibits collecting any amount , including interest , not authorized by the original agreement or law

- A collection balance can grow through accrued interest, collection costs, attorney fees, and court costs , all require legal authority

- Having the right to charge interest is not the same as calculating it correctly , rate errors and date errors are common dispute grounds

- Medical debt collection interest often follows different rules than credit card or personal loan debt

- Requesting debt validation is the first step before disputing or paying , documentation reveals whether the balance is legitamate

- Nearly 400,000 CFPB complaints about debt collection were filed in 2025 , the CFPB is a formal escalation path when collectors can't explain a balance

Free Credit and Collection Review

Get a Free Review of Collection Accounts With Unexplained Balance Increases

Joe Mahlow's team reviews collection account balances against the origional credit agreement, state interest laws, and court judgment records to identify whether balance increases are properly documented and calculated. Free, no obligation.

Get My Free Credit Review →

CROA Registered | 20 Years in Business | Free, No Obligation | Not Legal Advice

Related Posts

-

Debt Validation: When Collectors Must Prove the Debt Is Yours

Step one for any growing collection balance is requesting debt validation. This covers exactly what collectors are required to provide, what happens when they can't produce documentation, how to write a validation request letter, and what FDCPA rights apply when a collector refuses or provides incomplete documentation. The essential companion guide for disputing collection interest charges.

-

How to Dispute Identity Theft Collections

A growing collection balance is sometimes the first sign of identity theft , an account opened in your name that you never created. This covers how to identify fraudulent accounts, file an FTC Identity Theft Report, and dispute collections you didn't create using your FCRA and FDCPA rights. The step-by-step guide for anyone who notices a collection account they don't recognize, with or without a growing balance.

-

Collection Removed But Score Didn't Increase? Here's Why

After successfully disputing a collection , whether the interest was invalid, the balance was wrong, or the account couldn't be validated , the score may not move as much as expected. This covers every reason a removed collection produces minimal score movement: remaining high utilization, late payments on the original account, charge-offs, and thin credit files. What to address after the collection dispute is resolved.