Can debt collectors see your savings account, transaction history, or any other bank account details on their own? Can debt collectors see my savings account without a court order? No. Federal law bars your bank from sharing that information with third-party collectors. But once a debt collector wins a court judgment against you, the rules change fast. At that point, they can request a bank levy and legally freeze and seize funds from your savings account.

Running a credit repair company, I see this fear paralyze people all the time. One of the most unforgettable cases we handled involved a client who ignored a collection notice for seven months because she thought her savings account was untouchable. She had $4,200 set aside for a home down payment. By the time she came to us, a judgment creditor had already levied her account. The funds were frozen. Her home purchase fell apart. The debt was $1,900. She paid nearly triple that before it was over.

According to the CFPB's 2024 Fair Debt Collection report, the third-party debt collection market is a $20.2 billion industry employing about 140,000 people across more than 6,400 collection agencies in the United States. Nearly one in five people with a credit report had at least one collections tradeline on their credit report as of Q1 2023. If a debt collector is contacting you right now, understanding exactly what they can and cannot do with your bank account is not optional. It is urgent.

Can debt collectors see your savings account?

Debt collectors cannot access your bank account details directly. Federal law allows your bank to share only very limited information with outside companies, and a collections balance inquiry is not one of them.

What collectors can see without a court order:

Your name, address, and employer from public records and skip-tracing databases.

Your credit report, which shows open accounts, balances, payment history, and delinquencies.

Any information you voluntarily shared with them in writing or on a recorded call.

Your savings account number, balance, and transaction history are not visible through any of these channels.

How Do Debt Collectors Find Your Bank Account?

Debt collectors do not need to see your balance to find which bank you use. They use several legal methods once they have a court judgment.

Credit report data. Your report shows loans and accounts that reveal which bank you use.

Prior payment records. A check or bank transfer you sent to the original creditor carried your routing and account number.

Employer records. A wage garnishment order can reveal which bank your paycheck deposits into.

Debtor's examination. After winning a judgment, a creditor can bring you to court and require you to answer questions about your finances under oath.

Skip-tracing databases. Collectors use commercial databases that pull public records and property records to locate assets.

The key point: collectors do not need to see your savings account to find it. They build a financial picture from outside, then use a court order to reach in.

What Is a Bank Levy and How Does It Work?

A bank levy is the legal process that allows a judgment creditor to freeze and seize funds directly from your bank account. There is no distinction between savings and checking accounts when it comes to a levy. Both are equally accessible to a judgment creditor who follows the correct legal process.

Here is how the process works:

The collector files a lawsuit against you in civil court.

The court serves you with a summons. You have a deadline to respond.

If you do not respond, the court issues a default judgment. If you do respond, the creditor must prove the debt.

Once the creditor wins, they file for a writ of execution.

The writ is served on your bank. Your bank freezes the funds up to the judgment amount.

You receive a notice and have a short window to claim any exemptions.

If your claim fails or you do not file one, the bank turns the funds over to the creditor.

In our office last year, we handled 31 bank levy cases. In 19 of them, the client had never responded to the original lawsuit. The creditor got a default judgment without ever proving the debt in court. Ignoring a collection lawsuit is one of the most expensive mistakes a borrower can make.

At this point, you know how collectors find your account and what a levy looks like. The next question most people ask is: can they take everything?

Can a Debt Collector Take All the Money in My Savings Account?

Unlike wage garnishment, which has limits, a bank levy can take all non-exempt funds. There is no federal cap on how much of your savings account a levy can take. If the judgment is for $5,000 and your savings account holds $5,000, a creditor can legally take it all in one levy.

The only protection is exemptions. Certain funds in your savings account are legally protected from levy, even after a judgment.

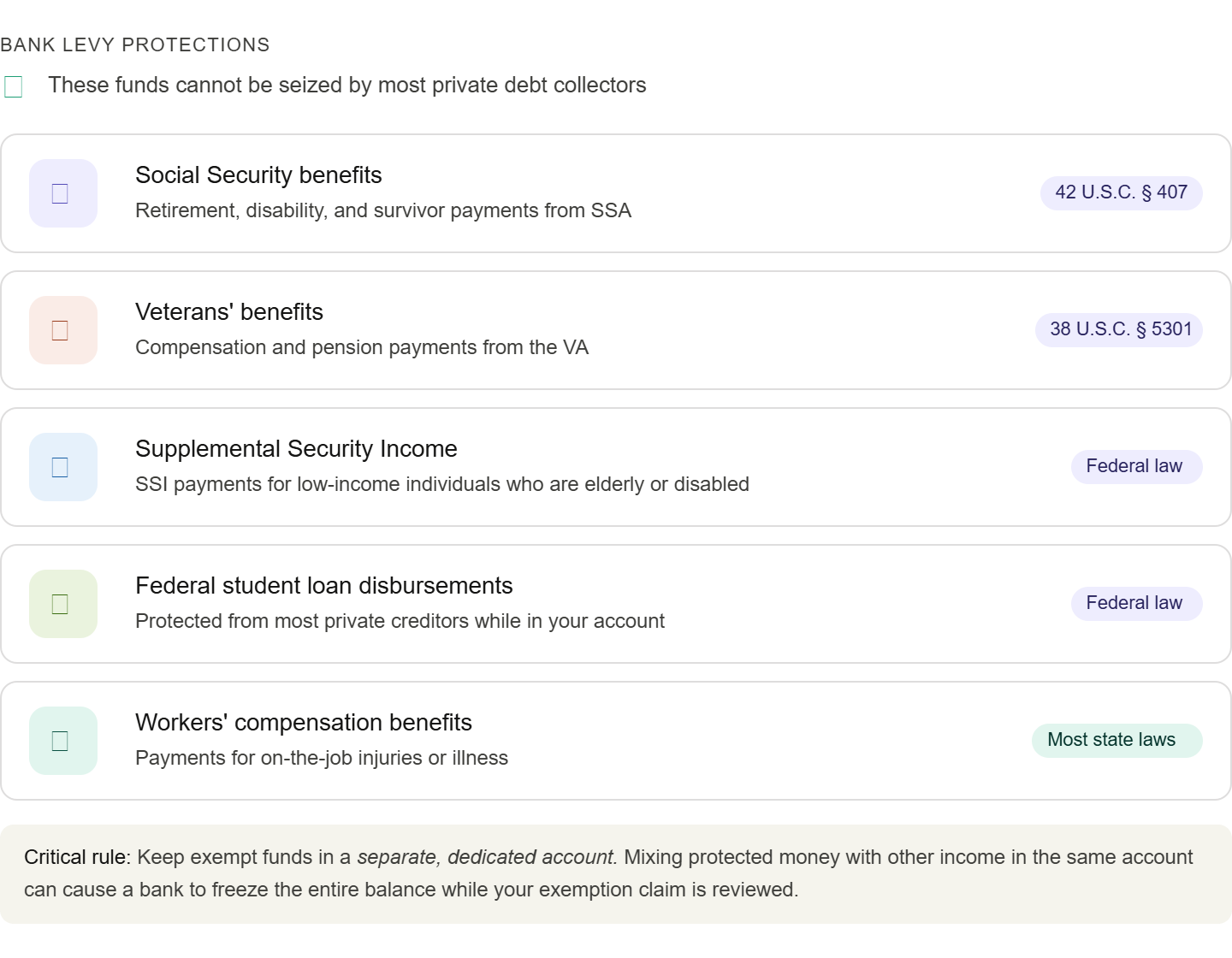

What Funds Are Protected From a Bank Levy?

Federal law protects specific types of income even after they land in your account:

The critical condition: keep these funds separate. Open a dedicated account that holds only exempt income. If protected funds mix with other money in the same account, the bank may freeze the entire balance while your exemption claim is reviewed. That process can take days or weeks, blocking all access.

What Is the Difference Between a Bank Levy and Wage Garnishment?

These are two separate legal processes, and a creditor can pursue both at the same time.

Wage garnishment intercepts a portion of your paycheck before it reaches your bank. Federal law caps garnishment at either 25% of your disposable earnings or the amount by which your weekly income exceeds 30 times the federal minimum wage, whichever is less. Some states set lower caps.

Bank levy seizes funds already sitting in your account. There is no federal percentage cap. The levy can take everything up to the full judgment amount, minus any exempt funds you successfully claim.

A creditor pursuing both simultaneously squeezes your income before it arrives and drains whatever has already accumulated.

Can Any Creditor Access My Savings Account Without a Court Order?

Most private creditors cannot. But three exceptions exist.

The IRS can issue a bank levy without a court order for unpaid taxes. It sends a final notice and gives you 30 days to respond. If you do not act, your bank holds your funds for 21 days before sending them to the IRS. That window is your last chance to negotiate.

State child support agencies can garnish your bank account without a court judgment in many states. Child support enforcement operates under separate federal and state rules that give agencies direct access.

Your own bank can apply the right of offset if you owe it money on a separate loan or credit card. If your savings and your credit card are at the same institution and the card goes into default, the bank can sweep your savings to cover the missed payment. No court order needed.

How Do I Protect My Savings Account From Debt Collectors?

Protecting your savings before a judgment is far easier than fighting a levy after one.

Respond to every lawsuit. Ignoring a collection suit is how most people end up with default judgments. A written response to the court stops the default clock and forces the creditor to prove the debt.

Keep exempt funds in a separate account. If you receive Social Security, veterans' benefits, or SSI, open a dedicated account that holds only those funds. Never mix them with other income.

Do not bank where you borrow. Keep savings at a different institution from any loans or credit cards you carry. This removes the right of offset risk entirely.

Negotiate before a judgment is issued. Once a judgment exists, your options shrink fast. Before that point, collectors often settle for less than the full balance to avoid a lawsuit.

Know your state's exemptions. Many states protect a set dollar amount in your bank account from any levy. Look up your state's exemption schedule or consult a consumer protection attorney.

Dispute debts you do not recognize. Send a written dispute within 30 days of first contact. The FDCPA requires collectors to verify the debt before continuing collection activity.

Worried About Debt Collectors or a Bank Levy?

Don't wait until a creditor freezes your bank account. Our credit experts can review your situation, identify reporting errors, and help you understand your options before collection actions become more serious.

✓ Free Credit Report Review

Discover collection errors, outdated accounts, and potential opportunities to improve your credit profile.

No obligation. Find out what may be hurting your credit and what steps you can take next.

What to Do If a Debt Collector Has Already Levied Your Savings Account

A levy on your account is not always the end. You still have options.

File an exemption claim immediately. Your bank and the court both accept exemption claims. If any frozen funds are protected, file the same day you find out. Most courts set a deadline of 10 to 30 days.

Contact a consumer protection attorney. Many take levy defense cases on contingency. If the creditor violated the FDCPA during collections, you may have a counterclaim that offsets the judgment.

Negotiate a settlement. Even after a levy, creditors often prefer a negotiated payment to enforcing the writ. A lump-sum offer at 40% to 60% of the judgment is often accepted.

Check the judgment for errors. Courts issue default judgments without verifying debt amounts. If the amount is wrong, the statute of limitations has passed, or you were not properly served, you may be able to vacate the judgment.

According to the CFPB's 2024 FDCPA Annual Report, the bureau received 207,800 debt collection complaints in 2024, nearly double the 109,900 complaints received in 2023. Collectors are more aggressive than ever. Knowing your rights is the first and most important line of defense.

Frequently Asked Questions

Can a debt collector freeze my savings account without telling me? In many states, yes. A creditor can serve the writ on your bank without giving you advance notice. You find out when your card stops working. Some states require notice at the same time the bank is served, but many do not.

How long does a bank levy last? A levy covers a one-time seizure of funds in your account at the moment the writ is served. It does not capture future deposits automatically. But a creditor can file a second levy if the first did not cover the full judgment amount.

Does a bank levy affect my credit score? The levy itself does not appear on your credit report. But the judgment that enabled it may appear as a public record. The unpaid debt that triggered the lawsuit also likely already appears as a collection account.

Can I open a new bank account if my current one is levied? Yes. A levy only applies to the specific account at the bank named in the writ. You can open an account elsewhere. However, a creditor can serve a new writ on the new bank if they find it.