Credit Karma can be useful, but it doesn’t show the full picture lenders see. The scores it displays often differ from real credit scores used by banks and loan companies. This article breaks down the truth behind Credit Karma, explains why the numbers don’t always match, and helps you understand which scores actually matter.

Credit Karma says you have a 720 score.

You apply for a car loan. The dealer says your score is 680.

You're confused. Angry. You think someone made a mistake.

Nobody made a mistake. Credit Karma just doesn't show you what lenders see.

As the owner of a leading credit repair company in Texas, I have this conversation at least three times a week. Clients walk in shocked that their "real" score is 40, 60, or sometimes 100 points lower than Credit Karma told them.

Credit Karma isn't lying. But it's not showing you the complete picture either.

Let me explain what's really happening with your credit scores and why that gap exists.

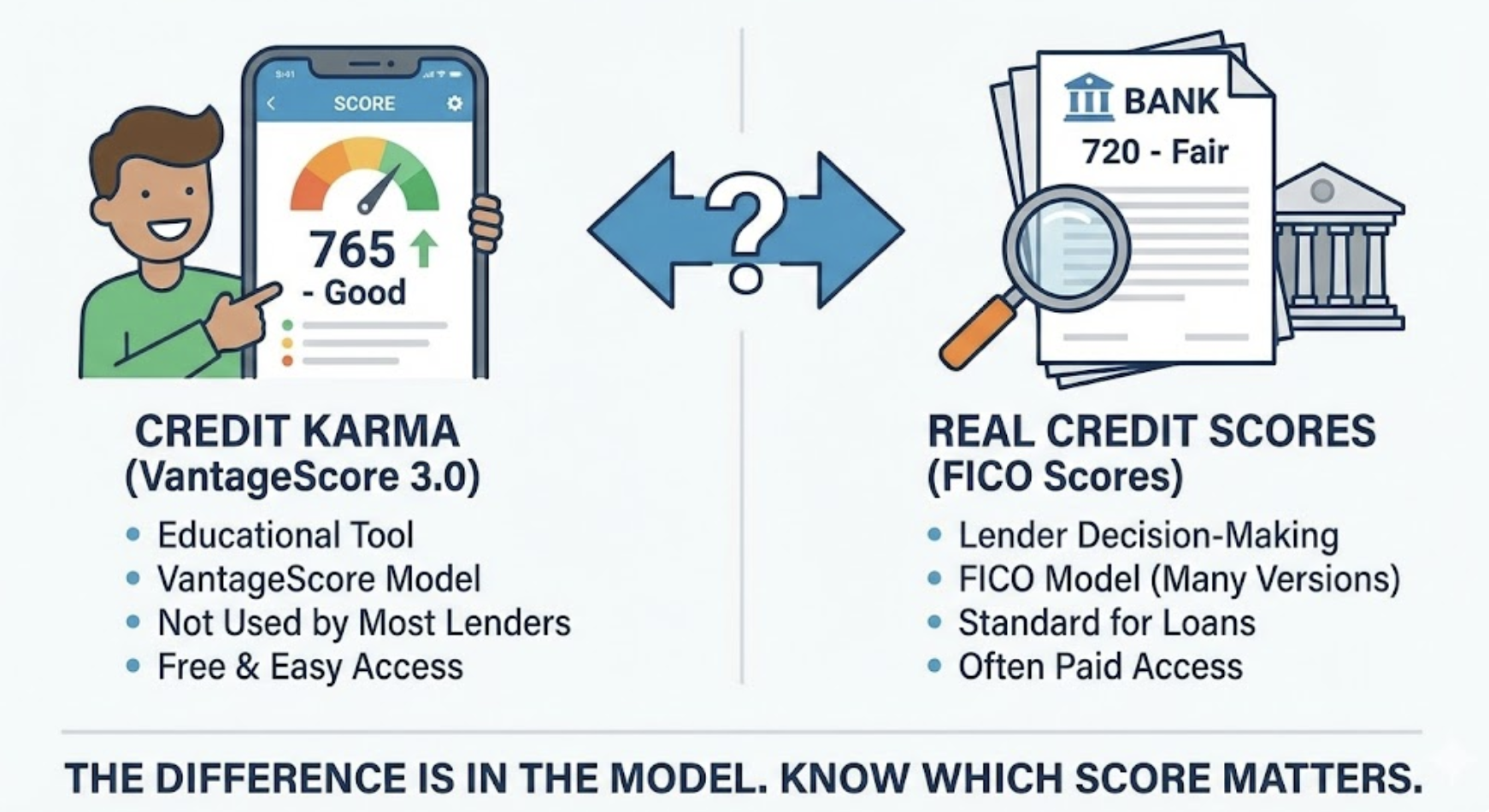

Credit Karma Shows VantageScore, Not FICO

Here's the thing that most people don't know.

There isn't just one credit score. There are dozens.

Credit Karma shows you VantageScore 3.0. This is a scoring model created by the three credit bureaus together. It's a real score. But it's not the score most lenders use.

Lenders use FICO scores. Over 90% of lending decisions use some version of FICO.

FICO and VantageScore calculate differently. They weigh factors differently. They treat the same information on your credit report and produce different numbers.

According to FICO, their scores are used in over 90% of lending decisions in the United States. VantageScore is growing, but nowhere near FICO's market share.

Think of it like different restaurants reviewing the same chef. One gives four stars. Another gives three stars. Same chef. Different standards.

Your credit report is the chef. FICO and VantageScore are the reviewers.

Credit Karma isn't wrong for showing VantageScore. But calling it your "credit score" without explaining it's not what lenders use? That's misleading.

I've seen clients delay major purchases by months because they trusted Credit Karma's number. They thought they were ready. They weren't.

Why Your Credit Karma Score Is Usually Higher

Most people notice their Credit Karma score is higher than what lenders tell them.

There's a reason for this pattern.

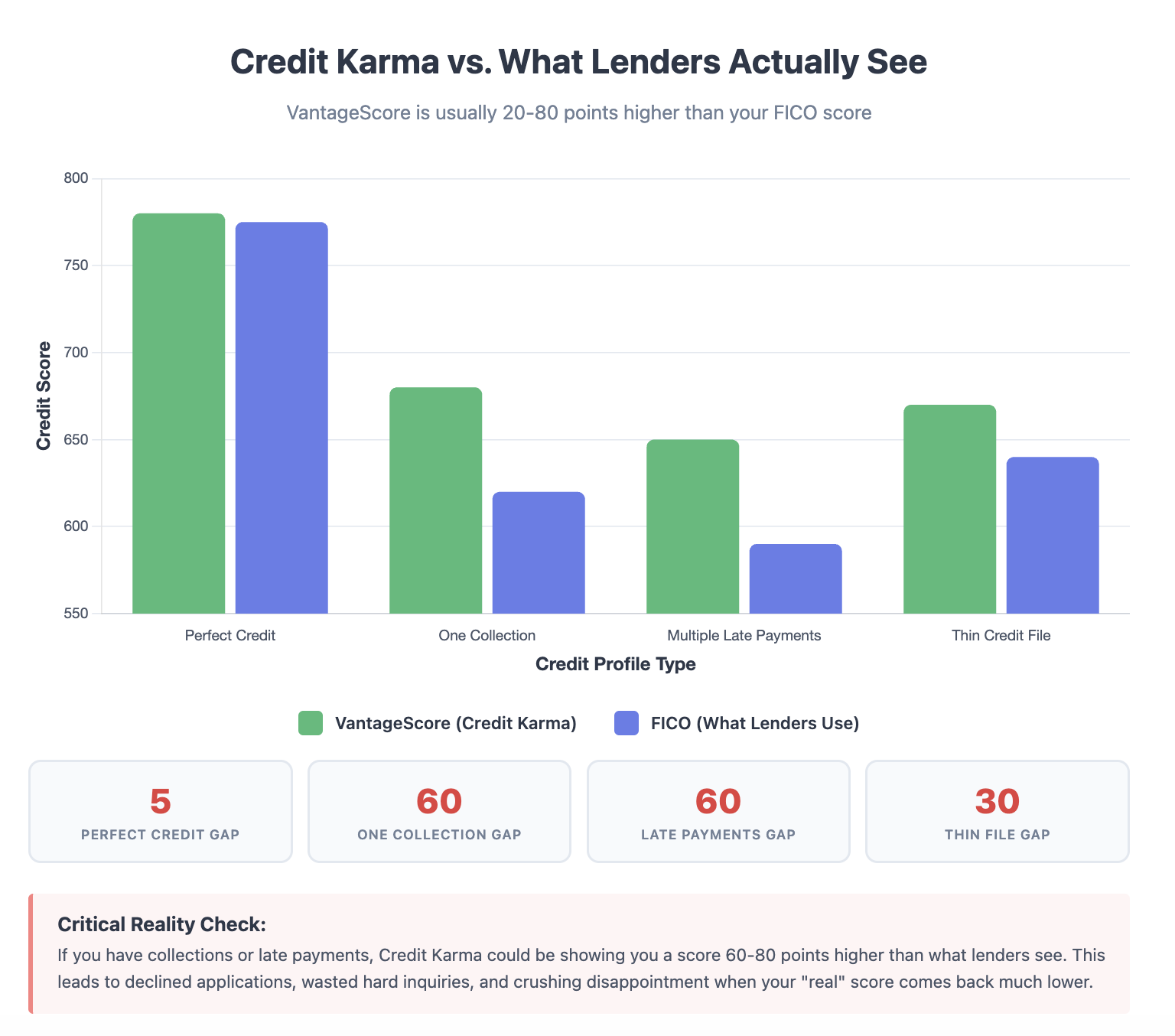

VantageScore 3.0 treats certain negative items less harshly than FICO. Paid collections hurt your VantageScore less. Medical collections get special treatment. Recent credit inquiries have less impact.

FICO penalizes these items more heavily. A paid collection still tanks your FICO score. Medical debt or not, collections hurt. Multiple inquiries cause bigger drops.

VantageScore also starts scoring people with thinner credit files. You can get a VantageScore with just one month of credit history. FICO requires at least six months.

This means VantageScore often gives higher scores to people just starting out. FICO sees insufficient history and scores lower or doesn't score at all.

The exact scoring formulas are proprietary. However, based on industry experience, VantageScore tends to be 20 to 50 points more lenient than FICO for consumers who have:

- Collections on their credit report

- Recent late payments

- Thin or limited credit history

- High credit utilization

This difference can create confusion when comparing scores across platforms.

If your credit is pristine, the scores are usually closer. Maybe 5 to 15 points apart.

But if you have any blemishes, expect VantageScore to be significantly higher.

Lenders Use Different FICO Versions

Here's where it gets more complicated.

Even among FICO scores, there are multiple versions.

FICO 8 is most common for credit cards and personal loans. FICO 9 is newer but less widely adopted. FICO 2, 4, and 5 are used for mortgages. FICO Auto Score is used for car loans.

Each version weighs factors slightly differently.

Mortgage lenders pull FICO scores 2, 4, and 5 from all three bureaus. They use your middle score for decisions. If your scores are 680, 700, and 720, they use 700.

Auto lenders typically use FICO Auto Score 8. This version weighs your auto loan payment history more heavily than other debts.

Credit card issuers mostly use FICO 8. Some use FICO 9, which ignores paid collections entirely.

You could have a 680 FICO 8 score, a 700 FICO 9 score, and a 660 FICO Auto Score. All legitimate. All different.

Credit Karma shows none of these. It shows VantageScore 3.0 only.

When clients ask me, "what's my real credit score," I tell them there's no single answer. The real score is whatever the specific lender is looking at for your specific loan type.

Good Read: How to Fix Credit Issues Before Applying for a Loan

The Three Bureau Problem

Credit Karma pulls from TransUnion and Equifax only.

It doesn't show Experian at all.

This matters because information varies across bureaus.

Not every creditor reports to all three bureaus. Some only report to two. Some only report to one.

You might have a collection account on Experian that doesn't appear on TransUnion or Equifax. Credit Karma won't show it. You think your credit is clean. It's not.

Mortgage lenders pull all three bureaus. They see everything. Including the stuff Credit Karma doesn't show you.

I've had clients come in confident about their credit because Credit Karma looked good. Then we pull all three bureaus and find accounts they didn't know existed. All on Experian.

Always check all three bureaus before applying for major loans. Never rely on just two.

Free annual reports from annualcreditreport.com show all three. Use that instead of Credit Karma for pre-loan preparation.

What Credit Karma Actually Gets Right

Credit Karma isn't useless.

It's free. It updates regularly. It shows you what's on your credit report.

For monitoring purposes, it works fine.

You get alerts when new accounts open. You see when inquiries hit. You can spot identity theft quickly.

The credit report information Credit Karma shows is accurate. It pulls real data from TransUnion and Equifax.

The problem is only the score calculation and missing Experian data.

I recommend clients use Credit Karma for monitoring but not for loan preparation. Watch for changes. Check for errors. Catch fraud early.

Just don't trust the score number when you're about to apply for credit.

Credit Karma also offers useful tools. The simulator shows how actions might impact your score. The approval odds help you avoid unnecessary hard inquiries.

These features use VantageScore calculations, so take them with caution. But they're helpful for general guidance.

The company makes money when you apply for credit products through their site. That's their business model. Free credit monitoring in exchange for marketing opportunities.

Nothing wrong with that. Just understand what you're getting.

Where to Find Your Real FICO Scores

If you want the scores lenders actually see, you need to pay for them.

MyFICO.com sells access to your real FICO scores. They offer single bureau reports or three-bureau reports.

A three-bureau FICO report costs about $60 to $90 depending on the package. It shows you FICO 8 from all three bureaus, plus mortgage scores.

This is the most accurate picture of what lenders see.

Some credit cards now offer free FICO scores as a cardholder benefit. Discover, American Express, Bank of America, and others provide this.

Check your credit card benefits. You might already have free FICO score access.

Experian offers a free app with your FICO 8 score from Experian only. This gives you one of three scores for free.

Mortgage lenders often provide pre-qualification with soft pulls. This shows you exactly which scores they'll use for your application. Some lenders do this for free.

I tell clients planning major purchases to invest in a three-bureau FICO report six months before applying. This shows exactly where you stand.

Then monitor free with Credit Karma between paid checks. You get the best of both worlds.

How to Prepare When Scores Don't Match

You check Credit Karma. It says 720.

You check MyFICO. It says 670.

Now what?

Always plan based on the lower score. If you're applying for a mortgage, use your FICO scores for planning. Ignore Credit Karma's VantageScore.

Know which score matters for your goal. Buying a car? Check your FICO Auto Score. Applying for a credit card? FICO 8 matters most. Getting a mortgage? You need FICO 2, 4, and 5.

Give yourself buffer room. If you need a 680 for approval, don't apply when your FICO is 680. Get it to 700 first. Scores fluctuate. Give yourself margin for error.

Fix the issues showing on FICO, not just VantageScore. Collections might not hurt your VantageScore much. They crush FICO. Pay them off or negotiate deletion.

Pull real FICO scores before major applications. Don't guess. Don't assume. Know your actual numbers before applying.

According to Experian, consumers who check their real FICO scores before applying have 35% higher approval rates than those who don't. Knowledge is power.

I've saved clients thousands by having them delay applications until their FICO scores improved. Credit Karma would have told them they were ready. They weren't.

The Specific Score Differences That Matter Most

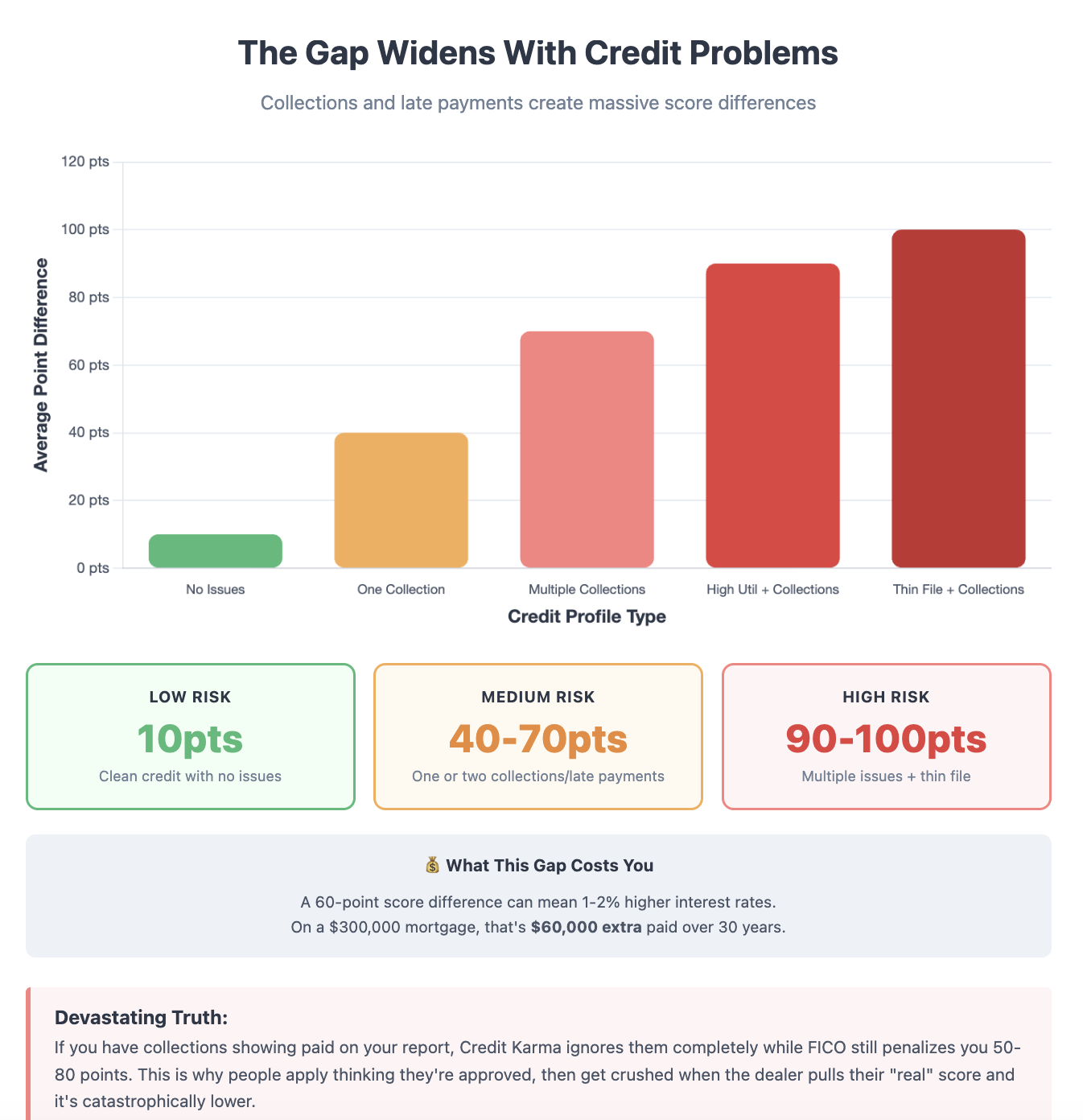

Some credit issues create bigger gaps between VantageScore and FICO than others.

- Collections. VantageScore 3.0 ignores paid collections entirely. FICO counts them. If you have paid collections, your FICO could be 50 to 80 points lower than VantageScore.

- Medical collections. VantageScore gives these less weight. FICO treats them like any other collection until FICO 9, which few lenders use. Gap can be 30 to 60 points.

- Thin credit files. VantageScore will give you a score with minimal history. FICO requires more data. New credit users might see 40 to 70 point differences.

- Recent inquiries. VantageScore is more forgiving. FICO penalizes harder. Multiple recent inquiries create 15 to 30 point gaps.

- Credit utilization over 30%. Both scores hate high utilization. But FICO penalizes it slightly more. Gap widens to 20 to 40 points when utilization exceeds 50%.

If none of these apply to you, your scores are probably close. Maybe 10 to 20 points apart.

But if you have any of these issues, the gap widens significantly.

What Happens When You Apply Based on Wrong Score

Real-world consequences happen when you trust Credit Karma and ignore FICO.

You get declined entirely. Credit Karma says 720. You apply for prime credit cards or best mortgage rates. Your FICO is 660. Declined. Now you have a hard inquiry hurting your score for nothing.

You pay higher interest rates. You qualify for the loan but at worse terms. That 1% to 2% interest rate difference costs thousands over the loan life.

You waste time. You shop for houses or cars thinking you're approved. Then real scores come back lower. You scramble to improve credit while deals fall through.

You lose negotiating power. Car dealers see your real score. They know you won't qualify for advertised rates. You lose leverage in negotiations.

You damage your credit further. Multiple applications based on wrong score assumptions create multiple hard inquiries. Each one drops your score more.

I've watched clients lose their dream homes because they trusted Credit Karma. They thought they had the score needed for their loan. They were 40 points short on FICO. By the time they fixed it, the house sold.

Another client applied for five credit cards in one month. Credit Karma said his score could handle it. His FICO couldn't. All declined. His FICO dropped another 30 points from the inquiries.

These aren't rare cases. This happens constantly.

The Credit Score Landscape Is Changing

VantageScore is trying to gain market share.

Some lenders are adopting it. Government-backed loan programs are testing it. The gap between VantageScore and FICO might shrink in coming years.

But today, right now, FICO dominates.

Federal Housing Finance Agency announced in 2022 they're considering VantageScore 4.0 for Fannie Mae and Freddie Mac loans. This would be huge for VantageScore adoption.

But implementation is years away. And it would be VantageScore 4.0, not the 3.0 that Credit Karma shows.

Even if VantageScore becomes more common, you'd still need to know which score your specific lender uses.

The scoring landscape won't simplify anytime soon. It's getting more complex with new FICO versions launching and lenders using proprietary internal scores.

The best strategy is knowing what score matters for your specific goal and checking that score specifically.

How I Help Clients Navigate This Confusion

At my credit repair company, we pull actual FICO scores for clients.

We don't make decisions based on Credit Karma. We get the real numbers that lenders will see.

Then we create improvement plans targeting FICO scoring factors. Not VantageScore factors.

We dispute errors on all three bureaus. Not just the two Credit Karma monitors.

We negotiate with creditors to remove items that hurt FICO most. Collections. Charge-offs. Late payments.

We time applications for when FICO scores are optimal. Not when VantageScore looks good.

This approach gets results. Clients qualify for loans they wouldn't have gotten otherwise. They save thousands in interest.

The difference between success and failure often comes down to checking the right score.

Credit Karma is a tool. A useful one for certain purposes. But it's not the ultimate answer for loan preparation.

What to Do Right Now

If you're planning to apply for any loan in the next six months, take these steps today.

Stop relying only on Credit Karma. Check your actual FICO scores through MyFICO or your credit card issuer.

Pull all three credit reports. Visit annualcreditreport.com. Review Experian alongside TransUnion and Equifax.

Identify which FICO score matters for your goal. Mortgage? Check FICO 2, 4, and 5. Auto loan? Check FICO Auto Score. Credit card? FICO 8.

Fix issues that hurt FICO most. Collections, late payments, high utilization. These create the biggest gaps.

Give yourself time. Don't apply until your FICO scores meet the lender's requirements. Add buffer room for score fluctuations.

Consider professional help. If the gap between Credit Karma and FICO is huge, you might need expert guidance to close it.

The cost of checking your real scores is tiny compared to the money you save on better loan terms.

A 1% better interest rate on a $300,000 mortgage saves you $60,000 over 30 years.

That's worth spending $90 on a FICO report.

Final Thoughts From a Texas Credit Repair Expert

Credit Karma serves a purpose. Free monitoring. Fraud alerts. General credit education.

But it's not the tool for serious loan preparation.

Over my years running a credit repair company in Texas, I've seen too many people hurt by this score confusion.

They trust the wrong number. They apply too early. They get declined or pay higher rates.

Then they come to me frustrated and confused. Why did the lender see something different? Why wasn't Credit Karma accurate?

I explain what I've explained here. Different scores. Different calculations. Different uses.

The problem isn't you. The problem is a confusing credit scoring system that nobody explained properly.

Now you know. Credit Karma shows VantageScore. Lenders use FICO. They're different. Sometimes very different.

Check the right score for your goal. Plan accordingly. Apply when you're truly ready.

That's how you get approved for the credit you want at the rates you deserve.

Don't let a misleading score number cost you thousands. Know your real numbers. Make informed decisions.

Your financial future depends on it.