Applying for a loan with bad credit can cost you higher interest rates or get you denied altogether. The smart move is to fix credit issues before you apply. That means correcting errors, lowering balances, and improving payment history so lenders see you as low risk. This guide shows exactly what to fix first and how to do it fast.

Here's the truth about loan applications.

Lenders pull your credit the moment you apply. What they see in those first 30 seconds determines everything. Your interest rate. Your loan amount. Whether you get approved at all.

Most people apply first and fix problems later. That's backward.

I've spent 15 years cleaning up credit reports. The clients who fix issues before applying save thousands in interest. The ones who don't? They pay for their mistakes for years.

You have more control over your credit than you think. Even major issues can improve in 30 to 90 days if you know what to do.

Let me show you the exact process I use with clients who need loans fast.

Why Timing Matters More Than You Think

Every day you wait costs money.

Not because of some imaginary deadline. Because of how credit scoring works.

Your credit score changes monthly. Sometimes daily. Negative items age and hurt less. Positive actions boost your score. Each reporting cycle is a chance to improve.

But here's what most people miss. Credit changes don't happen instantly.

You dispute an error today. It takes 30 days to investigate. Another 7 to 14 days to update across all three bureaus. That's 45 days minimum before you see results.

You pay off a collection account. The collector takes 30 days to report the update. Your credit score doesn't budge until the next reporting cycle.

According to Experian, credit score improvements from positive actions can take one to three months to fully reflect. Rushing the loan application before these updates are processed leaves points on the table.

I tell clients to give themselves 90 days before their target loan date. That's enough time for disputes to process, payments to report, and scores to stabilize.

If you need a loan in two weeks? You're working with what you have. If you have three months? You can make great improvements.

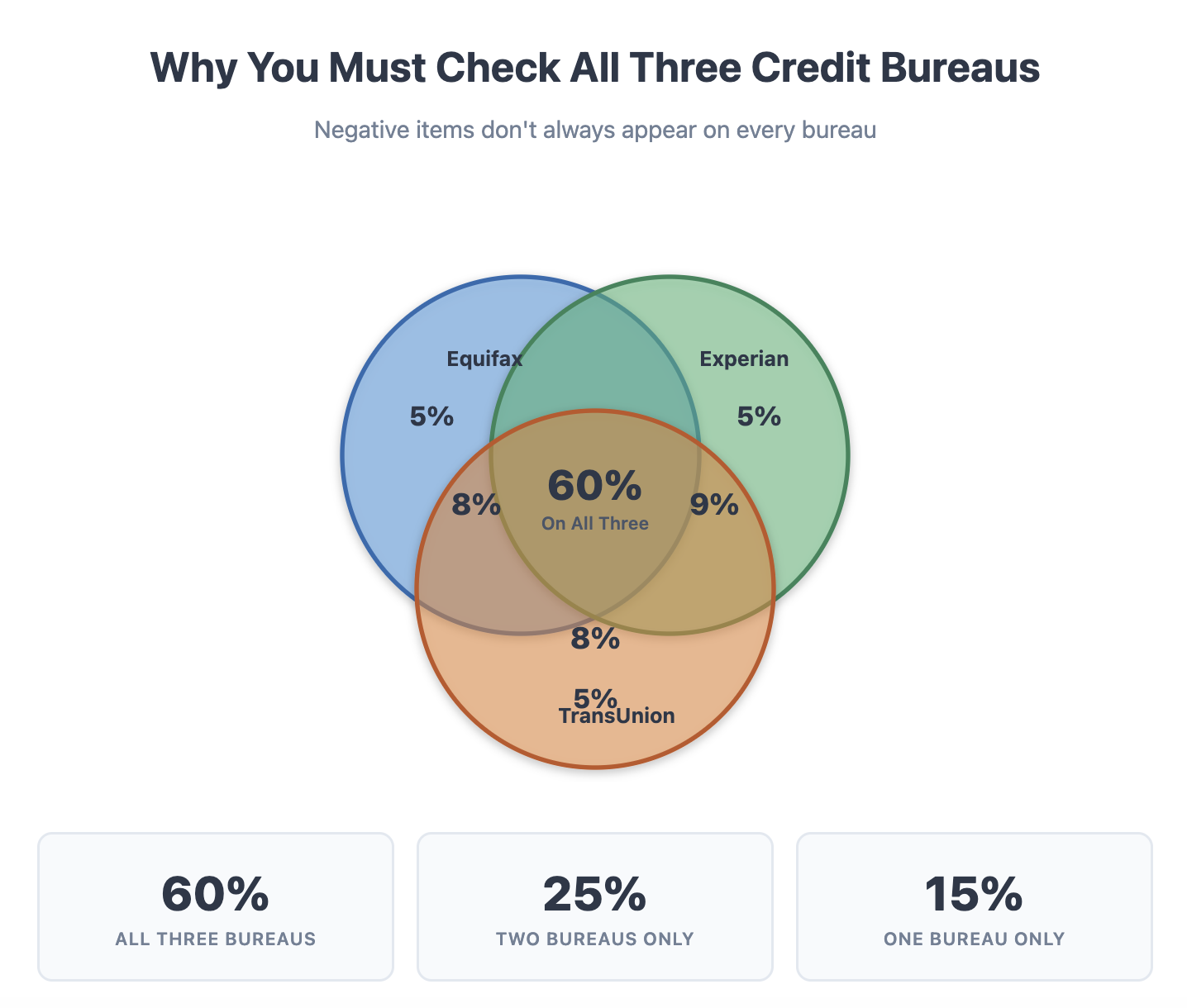

Pull Your Credit Reports From All Three Bureaus

You can't fix what you can't see.

Start by pulling your full credit reports from Equifax, Experian, and TransUnion. Not just your score. The entire report.

Visit annualcreditreport.com. This is the only official site for free reports. You get one free report from each bureau annually.

Don't use Credit Karma or other monitoring sites for this step. They don't show everything lenders see. Some accounts report to one bureau but not others. You need the complete picture.

Review each report line by line. Look for these red flags.

Accounts you don't recognize. Late payments you don't remember making. Collection accounts. Charge-offs. Bankruptcies. Judgments. High credit card balances. Recent hard inquiries.

Make a spreadsheet. List every negative item. Note which bureau reports it. Write down the date it first appeared.

This becomes your action plan.

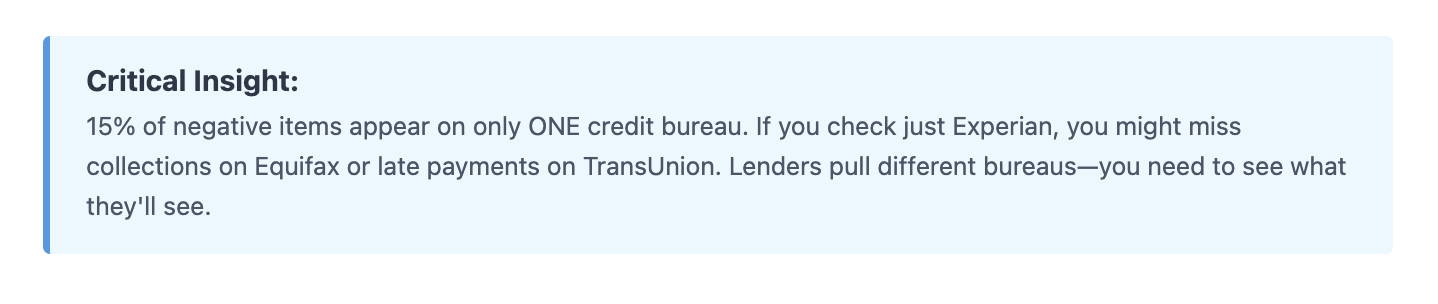

Different bureaus show different information. I've seen clients with collections on Experian but not Equifax. A late payment on TransUnion but not the other two. You need to check all three.

Lenders pull from one, two, or all three bureaus, depending on the loan type. Mortgage lenders use all three and base decisions on your middle score. Auto lenders typically use one. You can't predict which one matters most until you apply.

Below is a diagram that shows how negative items shows across three credit bureaus:

Dispute Every Single Error You Find

Credit report errors are everywhere.

According to a Federal Trade Commission study, one in five consumers has an error on at least one credit report. Some of these errors significantly impact credit scores.

Errors include accounts that aren't yours, payments marked late when you paid on time, debts you already paid showing as unpaid, duplicate accounts, or wrong account balances.

You have the legal right to dispute errors. Bureaus must investigate within 30 days.

Here's how to dispute effectively.

Dispute in writing, not online. Online disputes are faster but give you less documentation. Written disputes create paper trails. Mail them certified with return receipt.

Dispute one item per letter. Multiple disputes in one letter get flagged as frivolous. Separate letters for each issue get better results.

Include evidence. Attach copies of payment receipts, account statements, or correspondence proving the error. Don't send originals. Keep those.

Use specific language. Don't say "this is wrong." Say "This account number 1234 shows a late payment in March 2024. I paid on time as shown in the attached bank statement dated March 1, 2024. Please investigate and correct this error."

Dispute with the creditor, too. Send the same dispute to the company that reported the information. This puts pressure from both sides.

The bureau has 30 days to investigate. They contact the creditor. The creditor has to verify the information or delete it.

If they can't verify it, they must remove it. This is where documentation matters. Creditors often can't find records from years ago. Unverified items get deleted automatically.

I've removed thousands of negative items through disputes. Some were legitimate errors. Others were items the creditor couldn't verify. Either way, they came off the report and boosted scores.

Pay Down Credit Card Balances Strategically

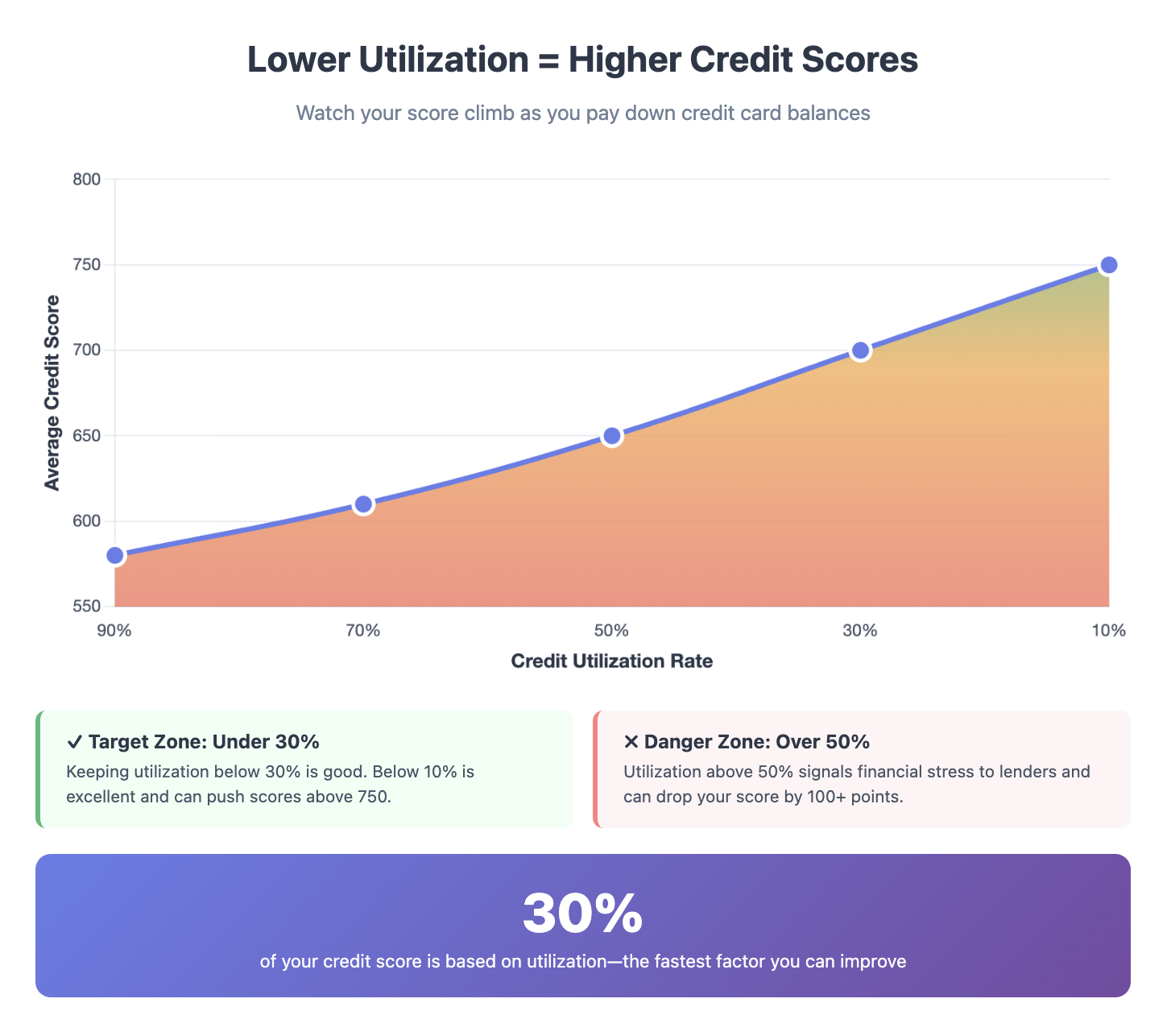

Credit card balances kill your score fast.

Not because you have debt. Because of the utilization ratio.

Utilization is how much credit you're using compared to your limits. It's calculated per card and across all cards combined.

Use 90% of your available credit? Your score tanks. Use 10%? Your score soars.

FICO says utilization is 30% of your credit score calculation. It's the second most important factor after payment history.

Here's the strategy I use with clients who need fast score boosts.

- Focus on cards above 50% utilization first. These hurt most. Getting them below 30% creates the biggest score jump.

- Pay before the statement closing date. Most people pay by the due date. That's too late. The balance on your statement closing date is what reports to bureaus. Pay before that date and a lower balance reports.

- Make multiple payments monthly. You don't have to wait for the statement. Pay weekly or twice monthly. This keeps your reported balance low all month.

- Don't close paid-off cards. Closing a card reduces your total available credit. This increases your overall utilization rate. Keep cards open even with zero balances.

According to Experian, consumers with credit scores above 800 typically keep utilization below 10%. Those with scores in the 600s often have utilization above 50%.

Let's say you have three cards. Card A has a $1,000 limit with a $900 balance. Card B has a $2,000 limit with a $500 balance. Card C has a $5,000 limit with a $1,000 balance.

Your total utilization is 30%. Not terrible. But Card A alone is at 90%. That single card is crushing your score.

Pay Card A down to $300. Your score jumps even though your total utilization barely changed. High per-card utilization matters more than total utilization.

Here's how a credit score improves over 90 days as utilization decreases:

Handle Collections and Charge-Offs the Right Way

Collections and charge-offs are score killers.

But they're also negotiable. Most people don't realize this.

Here's what works and what doesn't.

Don't pay collections without negotiating deletion first. Paying a collection doesn't remove it from your report. It just updates to "paid collection." Your score barely improves.

Negotiate pay-for-delete. Offer to pay in full if they delete the account entirely. Get this in writing before paying. Many collectors agree because they'd rather get paid than fight over reporting.

Try goodwill deletion for paid accounts. If you already paid a collection, write a goodwill letter asking for deletion. Explain why you fell behind and how you've improved. Some creditors delete as a courtesy.

Dispute old collections. Collectors often can't verify accounts older than three to five years. Records get lost. Companies go out of business. Unverifiable collections must be deleted.

Know the statute of limitations. Each state has time limits for suing over debt. Once expired, collectors can't take you to court. They can still ask for payment but have no legal power. Paying old time-barred debt restarts the clock in some states.

Charge-offs can sometimes be removed. Original creditors occasionally delete charge-offs if you pay in full. It's rare but worth asking. Get deletion agreements in writing.

I've removed hundreds of collection accounts through pay-for-delete negotiations. Success rate is about 60% with collection agencies. Original creditors are tougher but still possible.

For charge-offs, success is lower. Maybe 20% agree to delete after payment. But 20% is better than zero.

The key is negotiating before you pay. Once they have your money, leverage is gone.

Add Positive Payment History Fast

You need positive items to offset negative ones.

Lenders want to see responsible credit use. Not just absence of problems.

If your report shows only collections and late payments, adding positive accounts helps tremendously.

Become an authorized user. Ask family or friends with excellent credit to add you as an authorized user on their cards. Their positive history appears on your report. Your score can jump 40 to 100 points in one reporting cycle.

Choose someone with low utilization, long credit history, and perfect payment history. Their bad habits hurt you. Their good habits help you.

Get a secured credit card. These require a deposit that becomes your credit limit. Deposit $500, get a $500 limit. Use the card for small purchases and pay in full monthly. This builds positive payment history.

After 6 to 12 months of on-time payments, many issuers convert secured cards to regular cards and return your deposit.

Try a credit-builder loan. These loans exist solely to build credit. You make payments into a savings account. The lender reports your payments. At the end, you get your money back. It costs interest but builds payment history.

Report rent and utility payments. Services like Rental Kharma and Experian Boost add rent and utility payments to your credit report. If you pay these on time, you get credit for it.

According to FICO, adding positive accounts can improve scores by 20 to 60 points within three months, depending on your starting profile.

The more positive accounts you have, the less negative items hurt. A credit report with 10 accounts and two negatives looks better than a report with three accounts and two negatives.

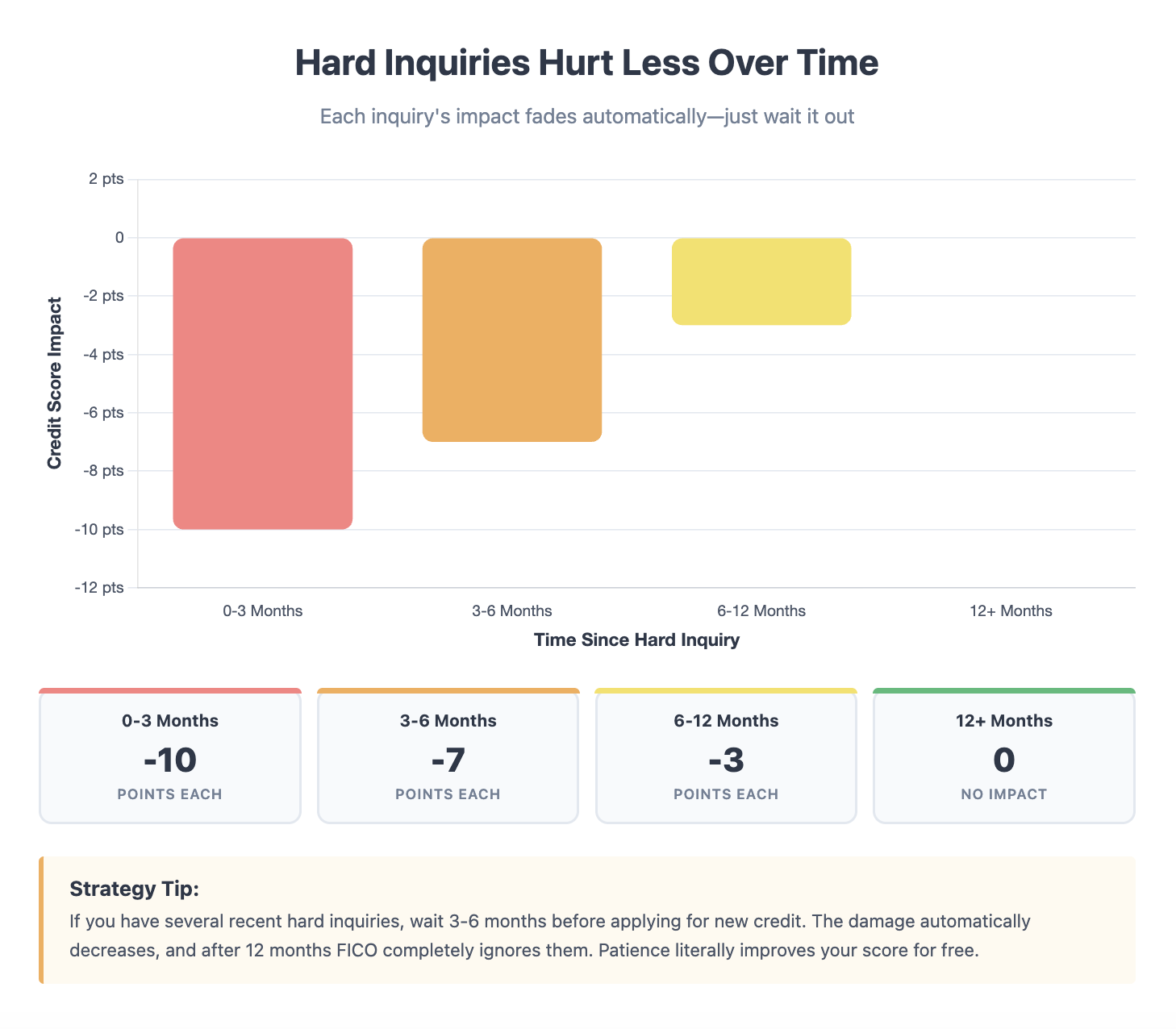

Remove Hard Inquiries When Possible

Too many recent hard inquiries hurt loan applications.

Each hard inquiry drops your score 5 to 10 points. Multiple inquiries signal financial desperation to lenders.

FICO groups similar inquiries within 14 to 45 days, as those for mortgages and auto loans. But credit card inquiries count individually.

Some inquiries shouldn't be in your report at all.

Unauthorized inquiries. If a lender pulled your credit without permission, dispute it. This happens more than you'd think. Marketing inquiries from pre-approvals shouldn't be hard pulls.

Identity theft inquiries. If someone applied for credit in your name, those inquiries are fraudulent. File an identity theft report and dispute them.

Duplicate inquiries. Sometimes lenders pull your credit twice for the same application. Dispute duplicates.

Write to each credit bureau disputing unauthorized inquiries. Include documentation showing you didn't authorize the pull. Bureaus must investigate and remove invalid inquiries.

Valid inquiries can't be removed just because you don't like them. But I've seen 30% to 40% of disputed inquiries get removed because they weren't properly authorized or documented.

Even legitimate inquiries stop hurting your score after 12 months. FICO ignores inquiries older than one year.

If you have many recent inquiries, wait a few months before applying for new credit. Let them age. Your score improves automatically as inquiries get older.

Fix Your Debt-to-Income Ratio

Credit score isn't everything lenders check.

Debt-to-income ratio matters just as much for approval odds.

DTI is your monthly debt payments divided by gross monthly income. Lenders want DTI below 43% for most loans. Below 36% is better.

High DTI gets you denied even with perfect credit.

Here's how to lower it fast.

Pay off small debts completely. Eliminating entire monthly payments drops your DTI more than making small dents in large debts. Have three debts of $100, $150, and $500 monthly? Pay off the $100 and $150 debts first. You just cut $250 from your DTI calculation.

Increase your income. Take on a side job. Ask for overtime. Get a raise. Higher income lowers DTI even if debt stays the same. Many lenders allow you to count side income after two years of consistent history.

Don't take on new debts. Every new monthly payment increases DTI. Hold off on car purchases, new credit cards, or personal loans until after your main loan closes.

Refinance high-payment debts. If you have a high car payment, refinancing to a longer term lowers the monthly payment. This improves DTI. Yes, you pay more interest long-term, but it can help you qualify for your primary loan.

According to the Consumer Financial Protection Bureau, DTI above 43% correlates strongly with mortgage default risk. That's why most lenders cap it there.

I've seen clients with 780 credit scores get denied for mortgages because their Debt to income was 48%. Meanwhile, clients with 680 scores and 32% DTI sailed through approval.

Calculate your DTI before applying. If it's high, focus on lowering it alongside improving your credit.

Recommended Article: Hidden Factors Lenders Check Beyond Your Credit Score

Set Up Automatic Payments on Everything

Future late payments tank your progress.

You can't fix past problems while creating new ones.

One new late payment can drop your score 60 to 110 points. All your hard work disappears in one missed payment.

Set up automatic payments on every single account. Minimum payments at least. More if your budget allows.

Credit cards. Student loans. Car loans. Utilities. Phone bills. Everything.

Use calendar reminders if you prefer manual payments. Set reminders five days before due dates. Not on due dates. Before.

According to FICO, payment history is 35% of your credit score. It's the single most important factor. Perfect payment history for six to 12 months can offset older late payments.

I tell clients to treat credit like a business. Automate everything possible. Remove human error from the equation.

Miss one payment while fixing your credit? You just reset your progress clock.

The 90-Day Action Plan That Works

Most people try to fix everything at once. They get overwhelmed and quit.

Break it into a timeline instead.

Days 1 to 7: Investigation phase. Pull all three credit reports. Make your spreadsheet of issues. Check your DTI. Calculate your current utilization. Identify every problem.

Days 8 to 30: Dispute phase. Send dispute letters for every error. Start pay-for-delete negotiations with collectors. Request goodwill deletions on paid accounts.

Days 31 to 60: Building phase. Apply for a secured card if needed. Get added as an authorized user. Pay down high-utilization cards. Set up automatic payments.

Days 61 to 90: Monitoring phase. Check for dispute results. Follow up on non-responsive bureaus. Make additional utilization payments. Pull updated reports to verify improvements.

By day 90, most disputes have resolved. Payment history shows improvement. Utilization is lower. The score is higher.

This timing isn't random. It accounts for 30-day dispute cycles, reporting dates, and credit scoring update schedules.

Clients who follow this exact timeline typically see score increases of 50 to 120 points, depending on the starting situation.

The ones who skip steps or rush the process? They see minimal improvement and often make things worse.

What to Do If You Can't Wait 90 Days

Sometimes you need a loan now.

Maybe your car died. Your lease is ending. An emergency happened.

You don't have 90 days. You have two weeks.

Here's your short-term strategy.

Pay down credit cards immediately. This is the fastest score boost. Pay before statement closing dates. Some issuers update mid-cycle if you call and request it.

Become an authorized user. This can post within one reporting cycle. Ask someone to add you today. Many issuers report to bureaus within 30 days.

Dispute obvious errors. Major errors like accounts that aren't yours. Duplicate accounts. Clearly wrong information. These might resolve faster than complex disputes.

Try rapid rescore. Mortgage lenders offer this service. You provide proof of changes like paid collections or lower balances. They manually update your credit file. Results in 3 to 7 days instead of 30.

Rapid rescore costs money. Usually $25 to $50 per account per bureau. Worth it if you're close to qualifying and need a quick boost.

Shop around for lenders. Different lenders have different requirements. One denies you, another approves. Don't give up after one rejection.

Consider a co-signer. Someone with good credit co-signs your loan. You get approved based on your credit and income. You're both responsible for payment.

These short-term fixes help, but aren't as effective as a full 90-day cleanup. Use them when necessary, but don't skip the real work if you have time.

After the Loan: Keep Your Credit Clean

Getting approved isn't the finish line.

Your credit matters after closing too.

Don't close old accounts. Length of credit history matters. Closing old accounts shortens your average age. Your score drops.

Keep utilization low. Don't max out cards just because you qualified for a loan. Maintain good habits.

Monitor your credit. Set up free monitoring through Credit Karma or your credit card issuer. Catch problems early before they snowball.

Dispute new errors immediately. Don't wait until you need credit again. Fix issues as they appear.

Build emergency savings. Three to six months of expenses. This prevents future credit disasters when emergencies happen.

The habits you build fixing your credit should become permanent. Good credit isn't a one-time achievement. It's an ongoing practice.

I've watched clients clean up their credit, get approved for loans, then trash their credit again within two years. They stopped monitoring. Maxed cards. Missed payments.

Don't be that person. The work you put in now should pay off for decades.

Final Thoughts From the Trenches

Fixing credit before applying for a loan isn't optional if you want the best rates.

Every point on your credit score saves you money. A 680 score might get you a 7% interest rate. A 740 gets you 6%. On a $300,000 mortgage, that 1% difference costs you $60,000 over 30 years.

That's not a typo. Sixty thousand dollars for 60 credit score points.

The time you invest now pays massive dividends later.

Start with the basics. Pull reports. Dispute errors. Lower utilization. Add positive accounts. Give yourself time.

The clients I've helped who took this seriously saved enough in interest to buy cars. Pay for college. Take vacations.

The ones who rushed? They paid thousands in extra interest and fees. Some got denied entirely.

Your credit score is one of the most valuable financial tools you have. Treat it that way.

Fix the problems. Build good habits. Then apply for loans from a position of strength.