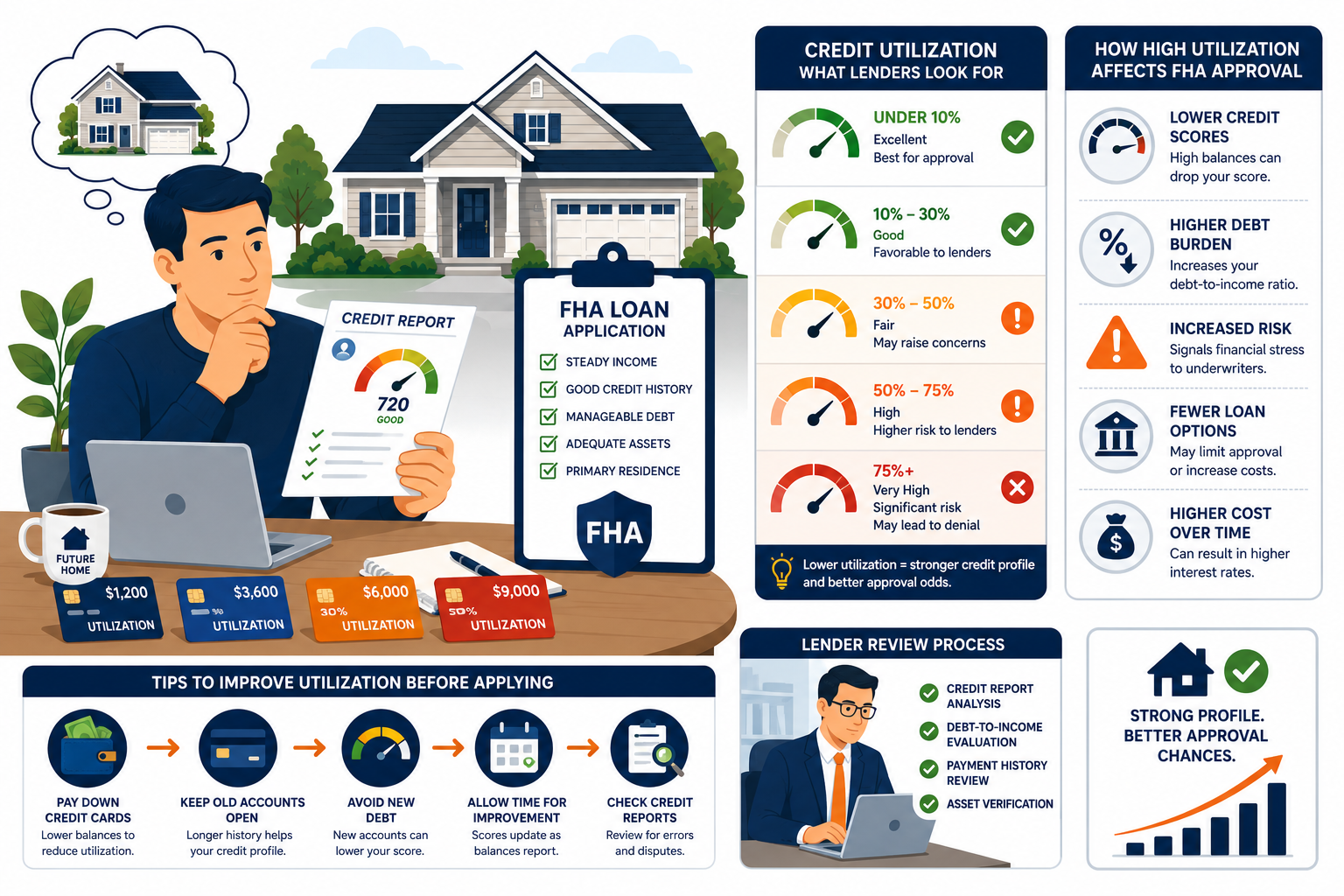

Credit utilization is one of the most overlooked factors affecting FHA mortgage approval. While FHA loans are often considered more flexible than conventional mortgages, lenders still evaluate how much of your available revolving credit is being used before approving a loan.

FICO data shows that consumers with the highest credit scores maintain lower credit utilization rates than borrowers with lower scores. Even when monthly payments are made on time, carrying high credit card balances can reduce credit scores and increase concerns during mortgage underwriting.

For FHA applicants, credit utilization can affect more than a score. It may influence debt-to-income calculations, mortgage pricing, lender overlays, and overall approval odds.

If you know how lenders evaluate revolving debt, it will help you determine whether paying down balances before applying could strengthen a mortgage profile.

How Credit Utilization Affects FHA Mortgage Approval

Credit utilization affects FHA mortgage approval because it influences both credit scores and lender risk assessments. High revolving balances can lower credit scores. Also, increase debt-to-income concerns and signal financial stress to underwriters.

Reducing utilization before applying may improve mortgage readiness and expand financing options.

"The most common pattern I see before FHA applications is a borrower with a 680 score, one credit card at 85% utilization, and no late payments anywhere. That is not a collections problem. That is not a dispute problem. That is a paydown problem. Pay the card to under 10% before the statement closes. The score moves 25 to 40 points in one billing cycle. The file that was borderline is now clearly in the approval band. High utilization on one card are often the single factor separating an FHA approval from a denial, even when everything else in the file is clean."

What Is Credit Utilization

Credit utilization is the percentage of revolving credit in use at any given time. It is calculated by dividing the current balance on each credit card by the card's credit limit. A card with a $5,000 limit and a $4,000 balance sits at 80% utilization. FICO evaluates utilization on each individual card and as an overall portfolio average. Both matter. A single card at 90% suppresses the score even when other cards sit at 0%.

How Utilization Is Calculated

Two calculations run simultaneously inside the FICO score:

- Individual card utilization. Each card's balance divided by its limit. A card at $1,900 of a $2,000 limit is at 95%. FICO scores this card separately from others in the portfolio.

- Overall portfolio utilization. Total balances across all revolving accounts divided by total available credit. Three cards totaling $3,000 in balances against $10,000 in limits equals 30% overall utilization.

Improving the overall average doesn't always fix the score if one card is near its limit. Both measures need attention before a mortgage application.

When Utilization Updates

Utilization resets every billing cycle. Card issuers report the balance on the statement close date. Pay the card to under 10% before that date and the lower balance reports to the bureaus within days. The credit score reflects the change at the next scoring cycle, which typically happens within 30 days of the statement close.

This is the mechanic that makes utilization the fastest available score improvement tool for FHA applicants. No dispute process. No waiting period. No new accounts. Just the payment before the right date.

Does FHA Consider Credit Utilization

The FHA does not publish a utilization limit in its underwriting guidelines. But FHA lenders pull FICO scores that already incorporate utilization at 30% of the calculation. Lenders also review the full credit report, which shows every card balance and limit. High utilization is visible to underwriters even when it is not a standalone rule violation. Lenders with stricter overlays note heavy revolving balances during manual underwriting, especially for files near the DTI ceiling or the score threshold.

FHA underwriting looks at two dimensions where utilization creates risk signals.

Credit score impact. The FICO score the lender pulls is already affected by utilization. A borrower with a 650 score may carry a 680-equivalent payment history but a 65% utilization rate pulling the score down. The lender sees 650 and prices the loan accordingly, without necessarily knowing the specific utilization figure is the primary cause.

DTI contribution. Minimum monthly payments on high credit card balances increase the debt-to-income ratio the lender calculates. A card at 90% utilization on a $5,000 limit may require a $150 minimum monthly payment. That $150 counts in the DTI alongside the mortgage payment, car loan, and student loan payments. For borrowers near FHA's 43% DTI ceiling, minimum credit card payments sometimes push the ratio past the approval threshold.

What Credit Utilization Ratio Is Best for FHA Approval

Under 10% per card produces the strongest credit scoring signal for FHA mortgage applications. Under 30% is the commonly cited threshold, but FICO research shows the largest single score improvement comes from crossing below 10% on each individual card. For FHA applications, every point matters , the difference between 579 and 581 changes the available down payment from 10% to 3.5%. Getting utilization as low as possible before the statement closes produces the best result.

The Threshold That Matters Most

The largest single score gain from utilization reduction comes from crossing below 10% per card, not below 30%. This is the key insight that separates a 15-point score improvement from a 40-point improvement. A card at 31% and a card at 8% produce measurably different FICO scoring outcomes even though both are technically "under 30%."

For FHA applicants within 10 to 20 points of the 580 threshold, this distinction is the difference between needing 3.5% down and needing 10% down.

Why High Utilization Can Hurt FHA Approval

High utilization hurts FHA approval through four channels: it lowers the credit score that determines the down payment requirement and rate tier, it increases minimum monthly payments that raise the DTI calculation, it signals financial stress to manual underwriters reviewing the full credit report, and it reduces available compensating factors when the lender is evaluating a borderline file.

- Lower credit score. Every point below the approval tier changes the lender's decision. A score at 578 with 3.5% down is different from 582 with 3.5% down. Utilization is the fastest way to move those four points without touching anything else in the file.

- Higher DTI from minimum payments. A credit card at $4,500 of a $5,000 limit requires approximately $135 to $180 in minimum monthly payments. That amount goes into the DTI calculation alongside the mortgage, auto loan, and other obligations. For borrowers near 43% DTI, one maxed card sometimes pushes the ratio past the FHA ceiling.

- Manual underwriting scrutiny. When a file goes to manual underwriting, the underwriter sees the actual card balances, not just the score. High revolving balances on multiple cards raise questions about spending patterns and financial management that don't appear in an automated approval system.

- Reduced compensating factor strength. FHA allows DTI above 43% with compensating factors , large down payment, high cash reserves, strong income history. But a file with high utilization, borderline DTI, and minimal reserves has fewer compensating factors to offer. Reducing utilization strengthens both the score and the available compensation pool simultaneously.

Can You Get Approved With High Credit Utilization

Yes, in certain situations. FHA approval with high utilization is possible when: the credit score still clears the lender's minimum despite the utilization damage, DTI stays below 43% even with the minimum payments factored in, and the borrower has compensating factors , larger down payment, cash reserves, stable income history, or low overall debt outside of the high-utilization card. The approval with high utilization is guarenteed to come with a worse rate and more underwriting conditions than a file with the same score and lower utilization.

When high utilization doesn't block approval but still costs money:

- A 620 score driven partly by 80% utilization gets FHA approval but at a higher rate than a 650 score borrower , even though paying down the card before applying might have reached 650 in 30 days.

- A borrower who qualifies at 43% DTI with the maxed card included could have qualified at 37% DTI after paying the card , opening lenders with stricter overlays and producing a lower rate offer.

The question is not just whether approval is possible with high utilization. It's whether applying with high utilization is smarter than waiting 30 days to reduce it first.

What Joe Mahlow and ASAP See Before FHA Applications

"After reviewing hundreds of mortgage-preparation credit reports, one pattern stands out above all others for FHA applicants. Borrowers focus on disputing collections. They spend two or three months working through the dispute process, which is neccessary when inaccurate items exist, but they completely overlook the one credit card sitting at 78% utilization. The collection dispute produces a 25-point gain after 45 days. Paying the card to under 10% before the next statement close produces a 30-point gain in 30 days with no letters, no investigation window, and no risk of the bureau reverifying something. Both strategies matter. The order in which you do them determines how quickly you reach FHA qualification."

Specific patterns from FHA pre-application reviews at ASAP Credit Repair:

- Most common finding: one card above 70% on an otherwise clean file. The borrower has no late payments, no active collections, and a score of 600 to 620. One card at 82% utilization explains most of the gap between their actual score and what their payment history alone would produce. Paying this card to under 10% is the highest-ROI single action available before the application.

- Second most common: overall DTI borderline after including minimum card payments. The borrower qualifies at 42% DTI. One card at 90% utilization adds $165 in minimum monthly payments to the calculation. Paying the card balance down by $3,000 drops the minimum payment requirement, reduces the DTI to 38%, and opens more lender options simultaneously.

- Third most common: borrower opened a new card during the preparation period. A new card opened six months before applying added a hard inquiry, a new account (shortening average account age), and a card sitting at 40% utilization from the first month of use. Three negative signals from one account opening that was meant to "build credit" before the mortgage.

Understanding the utilization picture across all three bureaus before applying may reveal score improvement that takes 30 days instead of months. Joe Mahlow's team at ASAP Credit Repair reviews every card balance, every limit, and every bureau report before making a recommendation.

Get a Free Credit Review Before Applying →Should You Pay Off Credit Cards Before Applying for an FHA Loan

Yes , pay them down, not necessarily all the way to zero. Target under 10% of each card's limit, not a zero balance. Closing paid cards or bringing them to zero doesn't always help and sometimes hurts. Zero balance on all cards can trigger a "no recent utilization" signal in some scoring models. Under 10% demonstrates active use with responsible management. Time the paydown before the statement closes , the score reflects the new balance within 30 days.

The Right Timing

The statement close date is the neccessary target, not the application date. Paying a card three days before applying has no scoring benefit if the statement already closed with the high balance showing. Pay before the statement close and the lower balance reports to all three bureaus within days of that date. The scoring update follows within 30 days.

For FHA applicants with a specific closing timeline, work backward from the expected application date to identify which statement close dates fall within the 30-day improvement window. Pay before those specific dates , not just before the application submission date.

What Not to Do

Three mistakes that accomodate a paydown strategy but undermine the FHA application:

- Closing the card after paying it off. Closing an account reduces available credit and can raise the overall utilization ratio on remaining cards. It also shortens the average account age, which affects the length of credit history category. Pay the card to under 10% and leave it open.

- Opening a new card to "lower overall utilization." A new card adds a hard inquiry and a new account. Both suppress the score temporarily. The utilization improvement from the new limit comes with two new negatives. For FHA applicants within 90 days of applying, no new accounts.

- Transferring balances between cards. Balance transfers move debt, not eliminate it. Shifting $3,000 from one card to another doesn't change overall utilization. It changes individual card utilization , sometimes creating one card at 0% and another at 95%, which the FICO model scores differently than two cards at lower percentages.

The full mechanics of how available credit and utilization affect credit scores , including why crossing below 10% produces the largest single score gain and why statement timing changes the outcome , covers every element of the pre-mortgage utilization strategy in detail.

As NerdWallet's credit utilization guide confirms, keeping utilization under 30% is the standard recommendation, but borrowers seeking the highest possible score before a mortgage application should aim for under 10% on each individual card , not just the portfolio average.

How Much Can Lower Utilization Improve a Credit Score Before FHA Application

The point improvement from utilization reduction varies by how much other negative information exists in the file. A clean file with one high-utilization card and no other negatives typically gains 30 to 60 points from paying that card to under 10%. A file with collections, late payments, and high utilization sees a smaller utilization-only gain , typically 15 to 30 points , because other negatives continue suppressing the score. Both gains are meaningful for FHA approval when the starting score is within 20 to 50 points of the threshold.

| Utilization Reduction | Approximate Score Gain | FHA Approval Impact |

|---|---|---|

| 80% to under 10% (one card, clean file) | 35-60 points | May move from 500s to 580+ tier, changing down payment from 10% to 3.5% |

| 60% to under 10% (one card, clean file) | 20-40 points | May move from 570s to 600+ tier, opening more lenders and rate options |

| 40% to under 10% (one card, clean file) | 10-25 points | May improve from a borderline approval to a clear approval with fewer conditions |

| Any reduction (file with other negatives) | 10-25 points | Partial improvement; other negatives continue suppressing. Combine with dispute strategy. |

As Bankrate's FHA loan guide confirms, FHA loans are government-backed mortgages that help borrowers who might not qualify for conventional financing , but the lender still evaluates the full credit profile, and score improvements from utilization reduction directly affect which FHA program tier the borrower qualifies for.

FHA Loan Approval Checklist , Credit and Utilization

And as NerdWallet's FHA loan requirements guide confirms, FHA borrowers must have a minimum credit score of 500 to qualify and 580 for the 3.5% down option , underscoring why every point gained from utilization reduction matters before a file goes to underwriting.

The pre-mortgage debt strategy guide covers the sequencing in full: which debt to prioritize, how the DTI calculation changes when specific balances drop, and the 90-day timeline that produces the strongest FHA file without creating new credit concerns during the preparation period.

Can FHA deny a loan because of high credit card balances?

Not directly , FHA doesn't set a utilization limit. But high balances affect two factors that can produce a denial: the credit score (high utilization lowers it, potentially below the lender's minimum) and the DTI ratio (minimum payments on high balances push the ratio above the 43% ceiling). When both effects combine on a borderline file, the practical result is denial , even though the stated reason may be "insufficient credit score" or "excessive debt-to-income ratio" rather than "high credit card utilization" specifically.

Is 50% credit utilization too high for an FHA mortgage?

50% utilization suppresses the credit score and raises underwriting concern, but it doesn't automatically block FHA approval. The score impact at 50% varies by the rest of the credit profile , a file with no other negatives loses fewer points from 50% utilization than one with collections and late payments. For FHA applicants at borderline scores, 50% utilization on one card may be the difference between approval and denial. The strategic question: can this card be paid to under 10% before the next statement close? If yes, do that first before submitting the application.

How long before applying for an FHA loan should I lower utilization?

Pay the card to under 10% before the statement close date that falls 30 to 60 days before the planned application date. This gives one full billing cycle for the lower balance to report to the bureaus and the score to update before the lender pulls the file. For borrowers with multiple high-utilization cards, prioritize the card with the highest individual utilization percentage first , that produces the largest single score gain. If budget allows, pay all cards in the same cycle to maximize the combined effect before the application date.

-

How Available Credit Can Raise Your Credit Score Faster Than You Think This is the foundational mechanics article for everything covered above. Why the score updates within 30 days when balances drop, why paying before the statement close date is what actually matters (not the application date), and why crossing below 10% produces a larger gain than crossing below 30%. For any FHA applicant who wants to understand the exact scoring mechanics behind the paydown strategy before executing it, this is the article to read first.

-

Should You Pay Off Debt Before Applying for a Mortgage? Credit card utilization reduction is one part of the pre-FHA debt strategy. This covers the full picture: which debt produces the most DTI relief when paid down, when to prioritize utilization reduction versus installment loan payoff, how the DTI calculation changes at each balance threshold, and the 90-day sequencing plan that produces the strongest FHA file. Directly relevant for borrowers near the 43% DTI ceiling where minimum card payments are the difference between qualifying and not qualifying.

-

Credit Repair for VA Loan Approval: What Veterans Need to Know The utilization strategy that applies to FHA applicants applies equally to veterans pursuing VA loan approval. The VA has no minimum score, but VA lenders require 580 to 620 and evaluate the same credit signals. This covers the VA-specific version of the same preparation framework: which credit issues matter most for VA underwriting, how the residual income calculation differs from FHA DTI, and the timeline for getting a VA-eligible file to the approval tier that opens the most lenders. A parallel read for veterans deciding between FHA and VA loan options.