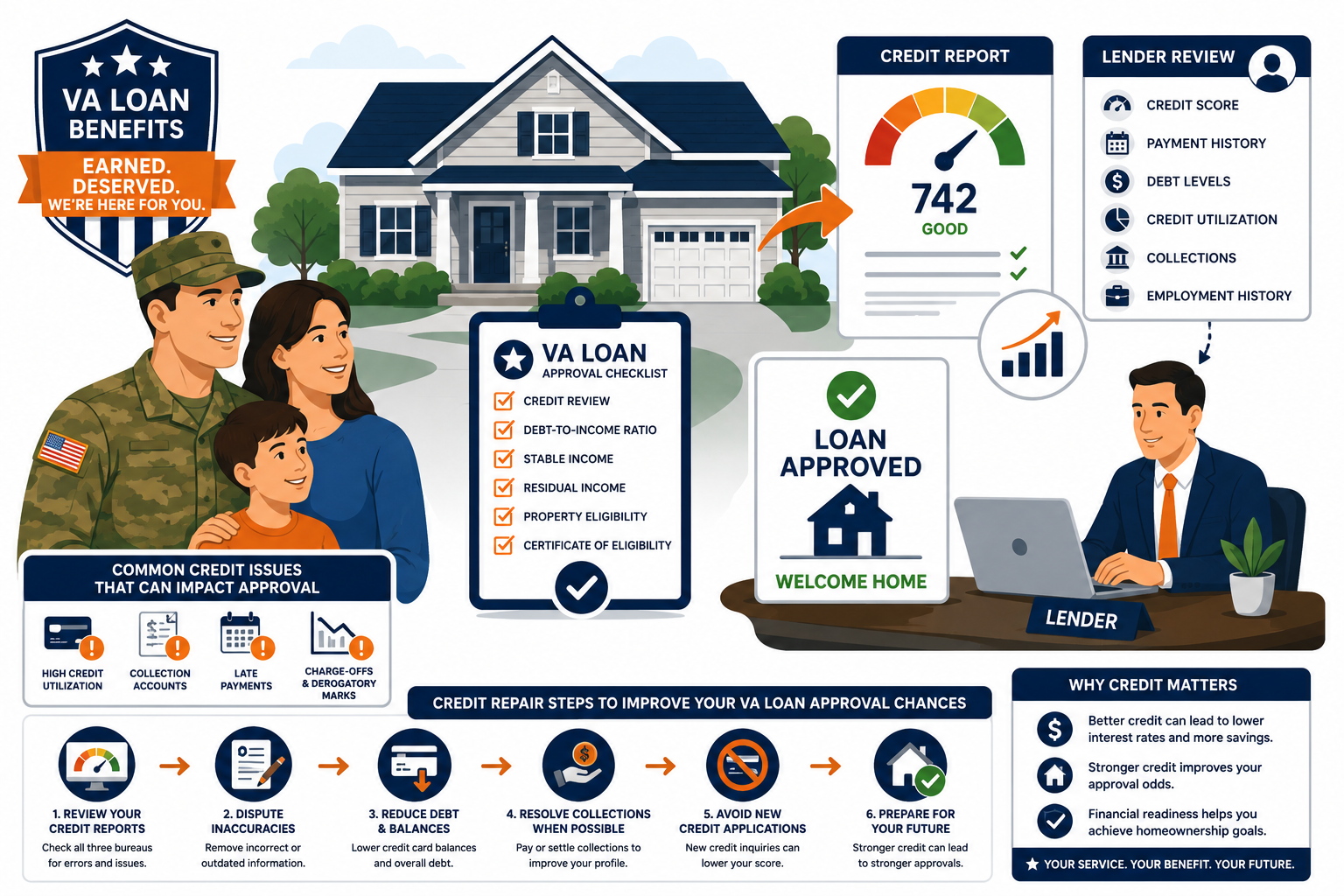

VA loans accounted for more than 490,000 home purchase loans in fiscal year 2024, according to U.S. Department of Veterans Affairs lending data. While the VA does not set a minimum credit score requirement, most lenders establish their own underwriting standards and review factors such as payment history, debt-to-income ratio, collection accounts, and credit utilization before approving a mortgage application.

Many veterans assume that VA loan eligibility guarantees mortgage approval.

In reality, approval depends on whether the lender believes the borrower can manage the new debt obligation. Recent late payments, high revolving balances, charge-offs, collections, and reporting errors can all create underwriting concerns, even when a borrower meets the VA's eligibility requirements.

Credit repair for VA loan approval focuses on identifying and addressing the credit factors that lenders evaluate during underwriting. Understanding which issues carry the most weight, and which can often be improved before applying, may help veterans strengthen their mortgage profile and increase their chances of approval.

Credit Repair for VA Loan Approval: What Veterans Need to Know

Credit repair can improve VA loan approval chances by addressing inaccurate credit report information, reducing credit card balances, resolving collections, and strengthening overall creditworthiness.

While the Department of Veterans Affairs does not set a minimum credit score requirement, many lenders establish their own underwriting standards and review credit history, debt obligations, and payment patterns before approving a mortgage.

"Veterans come to us after getting denied on a VA loan and they're confused. The VA doesn't have a minimun credit score requirement, so they assumed their service record and income would carry the application. What they didn't realize is the lender sets the score floor, and every collection account and late payment from the past 24 months still goes through underwriting. The file I see most often: a veteran with 640 score, two medical collections, and 72% utilization on one credit card. Fix those three things and the same lender who declined them will approve them."

How VA Loan Approval Works

A VA loan is a home financing benefit backed by the Department of Veterans Affairs for eligible active-duty service members, veterans, and surviving spouses. The VA does not lend money directly. It guarantees a portion of the loan made by a VA-approved lender. That guarantee reduces lender risk, which is why VA loans carry no down payment requirement and no private mortgage insurance. But it does not eliminate underwriting. The lender still evaluates the borrower's credit, income, debt obligations, and residual income before approving the loan.

Who Qualifies for VA Loan Benefits

VA loan eligibility requires a Certificate of Eligibility (COE) from the Department of Veterans Affairs, confirming that the service member meets minimum active-duty service requirements. Eligibility doesn't guarantee approval. It only confirms the VA benefit is available. The lender then applies its own underwriting criteria to the credit and financial profile.

What Lenders Review During Underwriting

VA lenders evaluate six primary factors alongside the credit score:

- Payment history. Every late payment from the past 12 to 24 months receives direct scrutiny.

- Debt-to-income ratio (DTI). VA guidelines suggest 41% maximum DTI, but lenders can approve above that with strong residual income.

- Residual income. This is unique to VA loans. It measures how much income remains after all monthly obligations are paid. Residual income requirements vary by family size and location.

- Collection and charge-off accounts. Lenders review type, age, and balance of each.

- Credit utilization. High revolving balances create risk signals even when the score clears the lender's threshold.

- Employment stability. Two years at the same employer or same field is the standard. Recent job changes require additional documentation.

Does Credit Repair Help With VA Loan Approval

Yes , specifically when the credit file contains inaccurate information, unverifiable collection accounts, or high utilization. Credit repair produces the most impact on VA loan approval odds when these three conditions exist simultaneously. Removing one inaccurate collection account can add 30 to 60 points to the credit score. Reducing a card from 80% to 10% utilization adds another 20 to 40 points in one billing cycle. Combined, these changes often move a veteran from a denial to an approval with the same lender and the same VA benefit.

What Credit Repair Can Improve for VA Applicants

- Removes inaccurate collection accounts through FCRA disputes with all three bureaus

- Corrects wrong payment dates, wrong balances, and duplicate entries

- Reduces credit utilization through targeted paydown strategy before statement close

- Sends FDCPA debt validation requests to collectors who cannot produce ownership documentation

- Challenges outdated items past the 7-year FCRA reporting window

What Credit Repair Cannot Change

- Accurate late payments from genuine missed obligations , these stay on the report until the 7-year window expires

- A recent bankruptcy or foreclosure , VA loan waiting periods (2 years for Chapter 7, 1 year for Chapter 13 with trustee approval) apply regardless of credit score

- Debt-to-income ratio , DTI responds to paying down debt, not to disputing credit reports

- Residual income shortfalls , this requires increased income or reduced debt, not credit repair

Credit Issues That Can Affect VA Loan Approval

The credit issues that most often block or delay VA loan approval are: collection accounts from the past 24 months (especially non-medical), recent late payments on any account, high credit card utilization above 40%, charge-offs from the past two years, and bankruptcies or foreclosures within the VA waiting period. Medical collections under $500 are often treated with more flexibility. Collections above $1,000 from the past year receive the most underwriting attention.

| Credit Issue | VA Underwriting Impact | Credit Repair Approach |

|---|---|---|

| Collection accounts (recent) | High concern Collections from past 24 months draw direct scrutiny | FCRA dispute for inaccurate items; FDCPA validation for debt buyers |

| Medical collections | Moderate concern Often treated with flexibility, especially under $500 | Dispute for reporting errors; may not require payoff at many lenders |

| Late payments | High concern Especially any from past 12 months | Dispute wrong dates; goodwill letters for isolated events; wait for history to age |

| High utilization | Moderate concern Above 40% on any card raises DTI and risk questions | Pay to under 10% before statement close; score improvement in 30 days |

| Charge-offs | High concern Especially from past 2 years | Dispute for validation gaps; pay-for-delete if valid and recent |

| Bankruptcy (Chapter 7) | 2-year waiting period VA requires 2 years from discharge date | Focus on rebuilding positive history during the waiting period |

| Foreclosure | 2-year waiting period VA requires 2 years from completion date | Same as bankruptcy , positive history rebuilding during wait |

What Credit Score Do You Need for a VA Loan

The VA sets no credit score minimun. Lenders set their own floors. Based on NerdWallet's 2026 survey of VA lenders, most require scores between 500 and 620. Veterans United (largest VA lender by volume) requires 620. NBKC and First Federal Bank approve at 580. Some lenders use no score cutoff and review the full financial picture. The score tier still affects the interest rate offered, even without a minimum requirement , VA loans don't carry LLPA surcharges the way conventional loans do, but lenders adjust rates by risk tier regardless.

As NerdWallet's VA loan eligibility guide confirms, the VA doesn't set a minimum credit score to qualify, but lenders review credit, debt, and income to determine whether the borrower qualifies and what interest rate to offer. That lender-level evaluation is where credit repair produces its most direct impact.

One distinction worth knowing: VA loans don't carry the Loan-Level Price Adjustments (LLPA) that make lower credit scores expensive on conventional loans. A 620-score VA borrower doesn't face the same rate premium as a 620-score conventional borrower. But the lender's approval threshold , and their own internal risk tiering , still applies. Getting to 620 or above before applying opens access to the majority of VA lenders, including those with the most favorable rates.

What VA Lenders Usually Approve

Beyond the credit score, VA lenders approve applications that show: clean payment history for the past 12 to 24 months, DTI below 41% (or higher when residual income is strong), stable employment for at least two years, adequate residual income for the family size and geography, and no bankruptcy or foreclosure within the waiting period. Residual income is the VA's most distinctive underwriting factor , it's the reason some VA loans approve above the 41% DTI ceiling when conventional loans would not.

- Stable payment history. No 30-day late payments in the past 12 months. No 60-day or 90-day lates in the past 24 months. Isolated older delinquencies with a clean recent record carry less weight than recent delinquencies on an otherwise clean file.

- DTI below 41%. The VA uses 41% as a guideline, not a hard cap. Lenders can approve above this when residual income is strong. Strong residual income with 50% DTI sometimes approves. Weak residual income with 38% DTI sometimes gets conditioned or denied.

- Residual income. After all monthly obligations are paid, the veteran must retain a minimum monthly income based on family size and geographic region. This is unique to VA underwriting and is calculated separately from DTI. A veteran in the South with a family of four needs approximately $1,003 per month in residual income after all debts.

- Two-year employment history. Same employer or same field for two years. Recent job changes with higher pay can qualify if the field matches and documentation supports the income claim.

Credit Repair Strategies Before Applying for a VA Loan

The highest-impact credit repair actions before a VA loan application, in order: (1) pull all three bureau reports and identify every collection account, late payment, and reporting error, (2) send FDCPA debt validation requests to all active collectors, (3) file FCRA disputes for every inaccurate or unverifiable item, (4) pay all credit cards to under 10% utilization before the statement closes, (5) avoid all new credit applications for 90 days before applying.

Review All Three Credit Reports

Equifax, Experian, and TransUnion each maintain seperate credit files. The same collection account may appear with different balances, different dates, or different collector names across the three. A VA loan pulls all three. Every negative item on any bureau shows up in underwriting. Pull all three at AnnualCreditReport.com before starting any credit repair strategy.

Dispute Inaccurate Information

One deleted collection account can add 30 to 70 points. A corrected payment date can change the 7-year removal timeline on an outdated account. A removed duplicate entry eliminates two negative marks for one underlying event. These changes happen through written FCRA disputes sent to each bureau, with 30-day investigation windows. No attorney required for the dispute process itself.

Reduce Revolving Debt

High credit card utilization suppresses the score and raises the DTI that lenders calculate during underwriting. Paying a card from 75% to under 10% before the statement closes adds 20 to 40 score points in one billing cycle. The full mechanics of how available credit affects credit scores explain why crossing below 10% produces the largest single gain and why statement timing matters.

Address Collection Accounts Strategically

Don't pay a collection before disputing it. If the collection deletes through the FCRA process, no payment is needed and the entire entry disappears. If the dispute fails and the account is valid, negotiate a pay-for-delete agreement , payment in exchange for bureau deletion , before sending any money. Paying without a deletion agreement leaves the collection on the report for the full seven-year window and produces minimal score improvement.

For VA loan purposes, the timing and approach to collections matters. Understanding when and how to address debt before a mortgage application covers the sequencing that keeps options open during the pre-application period.

Understanding what the credit file shows before applying may identify issues that change the approval outcome. Joe Mahlow's team at ASAP Credit Repair reviews all three bureaus and identifies what to address before a VA loan application goes in.

Get a Free Credit Review Before Applying →What Joe Mahlow and the ASAP Team See in Mortgage Preparation Files

"The pattern I see most among veterans seeking VA loan approval is the same. The score is close but not quite there. Usually 600 to 620. There's a collection from 18 months ago that the veteran doesn't even recognize because the original debt changed hands. There's one credit card at 80% utilization that the veteran thinks doesn't matter because they always pay on time. Fix the collection through dispute. Pay the card down. The score goes to 640 in 45 days. The same lender who denied them now has a file that clears underwriting. That's not unusual. That's what we see happen on a regular basis."

Patterns from reviewing credit files submitted for VA loan mortgage preparation:

- Most common issue: a collection from 12 to 24 months ago that the veteran didn't know existed. Medical billing, utility, or a fintech lender from a card opened briefly. Small balance. Went to a debt buyer. Shows on all three bureaus. Often disputable through validation.

- Second most common: one credit card at over 60% utilization. The veteran pays the minimum. The balance barely moves. The score gets suppressed every month. A single paydown before the statement closes moves the score 20 to 40 points without touching anything else.

- Third most common: a reporting error on the original delinquency date. The date reported is 8 months later than the actual event. The 7-year removal clock runs from a wrong start date. Correcting it can result in the account dropping off the report entirely if the actual date makes it obsolete under FCRA.

How Long Before Applying Should You Start Credit Repair

Pay all credit cards to under 10% before the statement closes. This is the one credit action that produces score improvement in 30 days or fewer. Do not apply for new credit, open new accounts, or close any existing accounts in this window. Any dispute filed now won't complete before the application goes in , the FCRA investigation window is 30 days minimum.

Pull all three reports. File FCRA disputes for every inaccurate item. Send debt validation requests to all active collectors. Reduce card utilization. First dispute cycle results come back in 30 to 45 days , leaving 45 to 60 days for follow-up disputes and for the score to reflect any deletions before the application. Most veterans who are 10 to 30 points short of the lender's threshold reach approval within this window when the file contains disputable items.

Six months allows two complete dispute cycles, time for collection deletions to register across all three bureaus, and six months of continued perfect payment history to build. For veterans with scores between 580 and 600, this window typically produces the score improvement needed to reach the 620 threshold that opens access to the majority of VA lenders.

Files with multiple collections, a recent bankruptcy discharge within the waiting period, or scores below 580 need 12 months to build the payment history and dispute results that produce VA loan qualification. A secured credit card opened at month one reports 12 months of positive history by application time. A dispute win at month two reflects in the score for 10 months before the application. This timeline produces the strongest file for veterans with the most credit damage.

Common Reasons Veterans Get Denied for VA Loans

The most common VA loan denial reasons are: excessive DTI (monthly obligations exceed 41% of income and residual income is insufficient to offset), recent late payments in the 12 to 24 months before application, unresolved collection accounts with large balances from the past two years, insufficient residual income for the family size and geographic region, and credit scores below the lender's specific threshold even when the VA has no official requirement.

As Money's 2026 review of VA loan lenders confirms, some lenders apply no minimum credit score and review the full financial picture , but this doesn't mean any credit profile qualifies. Those lenders still evaluate payment history, collections, and residual income through manual underwriting, and files with multiple recent delinquencies still face denial.

The most occured issue in VA loan denials at the credit level is not a score that misses by 50 points. It's a score that misses by 10 to 20 points because of one collection and one high-utilization card that nobody addressed before the application went in. The denial letter says "insufficient credit history" or "derogatory credit" when the real cause is two fixable items that credit repair would have addressed in 60 days.

As Bankrate's VA lender guide confirms, even VA-focused lenders like Veterans United and Newrez apply credit score minimums , 620 and 580 respectively , and these thresholds remain fixed regardless of the VA benefit or service record of the applicant.

VA Loan Approval Checklist

Can I get a VA loan with bad credit?

Yes, depending on how "bad" means in this context. A score in the 580s with stable income and no recent late payments can qualify at several VA lenders including NBKC and First Federal Bank. A score in the 500s limits options to specialty VA lenders and typically requires manual underwriting with strong residual income and clean recent payment history. A score below 500 with recent collections and late payments will find very few lenders willing to approve , credit repair during a 6 to 12 month preparation window is the path most likely to produce a fundable application.

What happens if a VA loan application gets denied?

The lender is required to provide a reason for the denial. Read that reason carefully , it identifies the specific credit or financial factor that triggered the decision. For credit-related denials, the typical path is 60 to 180 days of targeted credit repair addressing the named factor, followed by a reapplication. Some veterans work with a mortgage broker who can match the improved file to lenders with appropriate thresholds. A denial from one lender does not permanently close the VA loan path , it identifies what needs to change before the next application.

-

Should You Pay Off Debt Before Applying for a Mortgage? VA loan underwriting evaluates DTI and residual income alongside credit score. This covers the pre-mortgage debt strategy that applies directly to VA applicants: which debt to pay first, when to reduce revolving balances vs installment balances, how the DTI calculation works for VA underwriting, and the 90-day plan that produces the strongest VA loan file. The sequencing decisions here directly affect VA loan approval odds when DTI is close to the 41% threshold.

-

649 Credit Score and Mortgage Approval: What to Expect A 649 credit score sits near the VA lender threshold that opens access to the majority of programs including Veterans United. This covers what mortgage approval looks like at the 640-660 score range, which loan programs are available, what rate tier applies, and the specific credit actions that move a score from the high 640s into the 660-680 range where the strongest VA loan terms become available. Directly relevant for veterans in the near-prime score band preparing for application.

-

Improving a 593 Credit Score: Steps to Reach 650 Faster Many VA loan applicants start credit repair from the 580-600 range, where the goal is reaching 620 to access the majority of VA lenders, then 640-650 to access the most competitive rates. This covers the exact actions, timelines, and point estimates for moving a 593 score to 650, including the ASAP Credit Repair client data on what produces the fastest improvement: utilization reduction in 30 days and collection deletion in 30 to 90 days. The most actionable improvement guide for veterans starting from this score range.