TLDR: Credit cards borrow money from a lender and can help build your credit when used responsibly. Debit cards spend money directly from your checking account and help control spending but do not build credit. The best choice depends on your financial goals, spending habits, and the type of purchase you are making.

At ASAP Credit Repair USA, we have reviewed more than 100,000 consumer credit files. One pattern shows up more than almost any other. Clients who spent years using only a debit card, believing it was the responsible financial choice, and arrived at our office with a thin credit file and a score that did not reflect how carefully they managed their money. One client had used a debit card exclusively for fourteen years. His Equifax score was 581. His bank account was well managed. His credit file showed almost nothing because nothing he did with that debit card was ever reported to a bureau.

The decision you make at checkout every day. Debit or credit, is quietly shaping your financial future in ways most people do not understand until the damage is done or the opportunity has passed.

According to the Federal Reserve's 2023 Diary of Consumer Payment Choice, Americans made 52 billion debit card transactions and 47 billion credit card transactions in 2022. Most people use both without a clear strategy for when each one is the right tool. This article changes that.

Key Takeaways

Credit cards borrow money from a lender and report your payment behavior to Equifax, Experian, and TransUnion every month, which builds your credit history. Debit cards spend money already in your checking account and are never reported to credit bureaus.

Credit cards offer stronger fraud protection under the Fair Credit Billing Act, with a $50 maximum liability on disputed charges. Debit cards are covered by Regulation E, with liability up to $500 if you wait more than two business days to report fraud. The best long-term strategy uses both cards for their specific strengths: debit for cash management and budget control, credit for building credit history, earning rewards, and protecting large purchases.

What Is the Difference Between a Credit Card and a Debit Card?

A debit card spends money that is already in your checking account. When you swipe it, the bank pulls funds directly from your balance. You cannot spend more than you have without triggering an overdraft. No bill arrives at the end of the month. No interest accumulates. Nothing is reported to a credit bureau.

A credit card borrows money from a lender up to a preset credit limit. You spend first and pay later. The issuer sends a monthly statement. If you pay the full balance, no interest is charged. If you carry a balance, interest accrues at your annual percentage rate. Every month, the card issuer reports your balance, credit limit, and payment status to Equifax, Experian, and TransUnion.

That reporting difference is the single most important distinction between the two cards.

Everything else, rewards, fees, fraud protection, and purchase perks, flows from it.

Credit vs Debit Card: Which One Builds Your Credit Score?

Credit cards build credit. Debit cards do not. This is not a matter of degree. It is binary.

FICO and VantageScore, the two scoring models used in 95% of U.S. lending decisions, calculate scores entirely from data that appears on your credit report. Equifax, Experian, and TransUnion receive data from creditors who extend credit. Banks that issue debit cards are not creditors. They are custodians of your existing money. They have no obligation to report your debit activity to any bureau, and the vast majority never do.

This means that a person who deposits their paycheck, pays every bill on time, and manages a checking account flawlessly for ten years builds zero credit history from those actions. The FICO model does not see it. The VantageScore model does not see it. The mortgage underwriter does not see it.

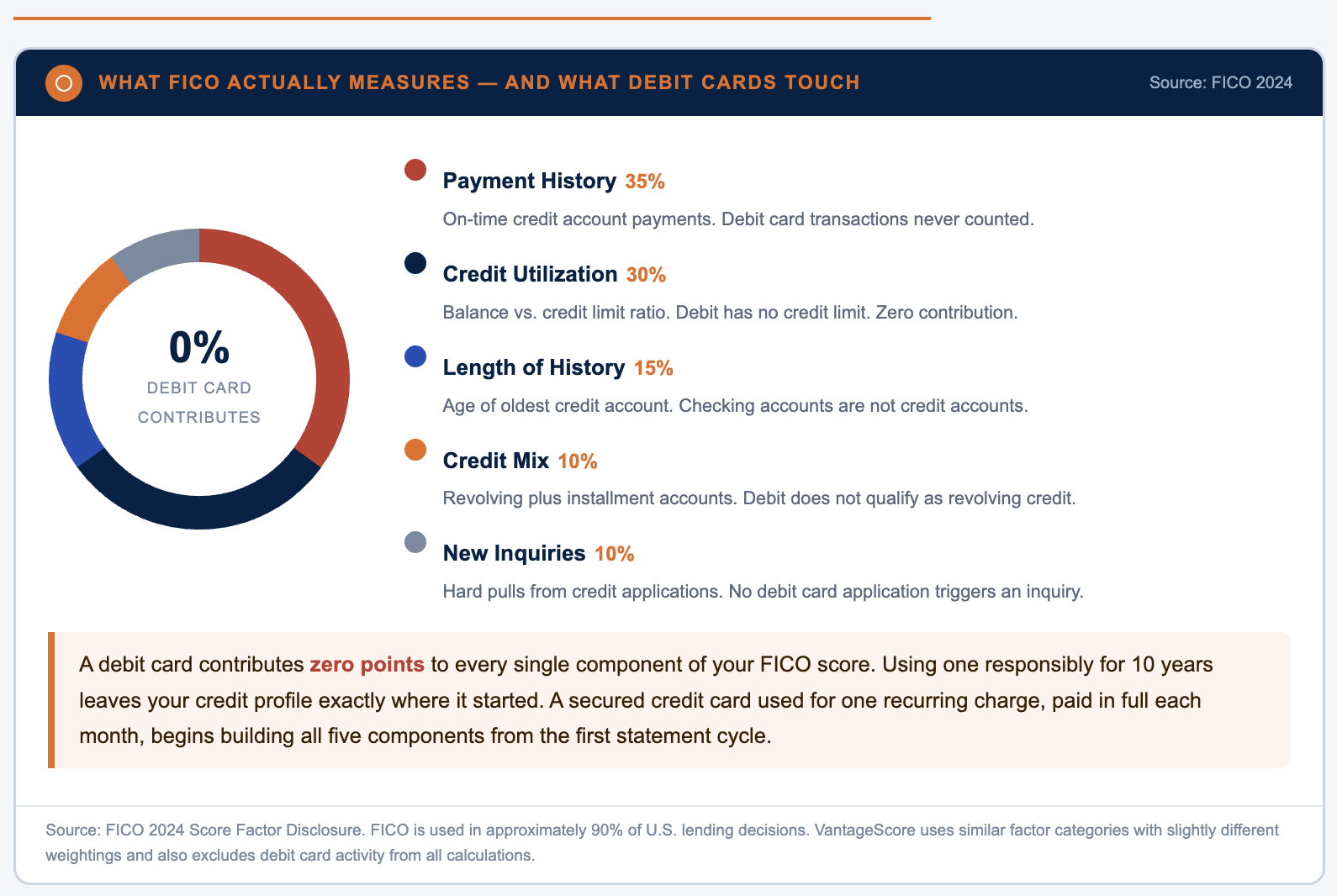

What credit scoring models measure when calculating your score:

Payment history (35% of FICO score): Whether you made minimum payments on credit accounts on time. Debit card transactions are not credit account payments and are never counted.

Credit utilization (30% of FICO score): The ratio of your total revolving balances to your total credit limits. Debit cards have no credit limit and no revolving balance. They contribute nothing to this calculation.

Length of credit history (15% of FICO score): How long your oldest credit account has been open and the average age of all accounts. Debit accounts are not credit accounts and are not included in this calculation.

Credit mix (10% of FICO score): Whether you have a mix of revolving credit and installment credit. Debit cards do not count as revolving credit.

New credit inquiries (10% of FICO score): Hard inquiries from credit applications. Debit card applications involve no hard inquiry and contribute nothing.

In Q1 of 2026, we reviewed 312 client files where the primary reason for a low score was a thin credit file. Of those 312 clients, 74 had used only debit cards as their primary payment method for more than three years. Their checking accounts were healthy. Their scores averaged 561. Clients in the same cohort who had used a secured credit card responsibly for the same period averaged 672. The difference was entirely traceable to the presence or absence of reported credit account data.

The practical path: if you are using a debit card because you want to be responsible with money, that instinct is correct but the tool is wrong for credit building. A secured credit card, used for one recurring monthly charge and paid in full each month, builds payment history, establishes a revolving account, and creates a credit history length that compounds over time. The debit card builds none of those things.

When Should You Use a Credit Card Instead of a Debit Card?

The credit card is the superior tool in every situation where the risk of fraud, the value of purchase protection, or the benefit of credit building outweighs the risk of carrying a balance.

Travel and Hotels

When you check into a hotel with a debit card, the hotel places an authorization hold on your account. That hold is not a charge. It is a reservation of funds that can reach $200 to $500 above your room rate to cover incidental charges. That cash leaves your checking account immediately and may not be released for three to seven business days after checkout. If your account balance is close to the hold amount, your other bills may be rejected or overdraft fees triggered.

When you check in with a credit card, the same hold is placed against your available credit. Your checking account is untouched. Your cash remains available. The difference in outcome for the same hotel stay is not cosmetic. It is the difference between having $400 in your checking account and having zero.

Car Rentals

Rental car companies apply similar holds, often $200 to $500. Some rental companies require a credit card entirely and will not accept a debit card for the rental itself, though they may accept debit for the final payment. Beyond the hold issue, credit cards issued by Visa and Mastercard typically include secondary collision damage waiver coverage, which can eliminate the need to purchase the rental company's expensive daily coverage option.

Online Shopping

Debit card fraud in online transactions requires the fraudster to drain money already in your account. Recovery takes days, during which your rent payment, utility autopay, and grocery purchases may fail. Credit card fraud in an online transaction never touches your checking account. The disputed charge is removed from your statement immediately upon filing, and your cash is never at risk. A 2023 Javelin Strategy and Research report found that credit card fraud resolution averaged 3.1 days compared to 7.8 days for debit card fraud resolution.

Large Purchases

Many credit cards include purchase protection that covers items against damage or theft for 90 to 120 days after purchase. Extended warranty benefits on many Visa Signature and Mastercard World cards add one to two years to the manufacturer's warranty at no additional cost. A television purchased on a debit card has no such coverage. The same television purchased on an eligible credit card may have an additional year of warranty coverage that the manufacturer does not provide.

Subscriptions and Recurring Bills

Placing subscriptions on a credit card rather than a debit card prevents a failed subscription payment from triggering an overdraft. It also creates a clean dispute mechanism. If a subscription charges you after cancellation, a credit card chargeback resolves the dispute within days. A debit card dispute requires the bank to investigate and may take up to ten business days, during which your money is gone.

When Is a Debit Card the Better Choice?

ATM Withdrawals

Credit cards assess a cash advance fee, typically 3 to 5% of the amount withdrawn, plus a higher APR that begins accruing immediately with no grace period. Debit cards are the correct tool for any ATM transaction. Cash advances on credit cards are one of the most expensive borrowing mechanisms available and should be avoided in almost all circumstances.

Day-to-Day Grocery and Small Purchases for Budget Control

For consumers who have struggled with credit card debt, using a debit card for routine grocery and household spending enforces a hard spending limit. You cannot spend money you do not have. This is not an advantage of the debit card itself. It is an advantage of the constraint it creates. If you have the discipline to pay credit card balances in full each month, the credit card is better for groceries because it builds credit history and earns rewards. If you do not have that discipline yet, the debit card is safer.

Teenagers and Young Adults Learning to Budget

A debit card attached to a checking account with a modest balance teaches spending awareness without the risk of accumulating debt. Prepaid debit cards go further by limiting available funds to an exact amount. For a 16-year-old learning to manage money, a debit card is the appropriate first financial tool. The first credit card should come later, once the habit of not spending more than you have is established.

Avoiding Debt During Financial Recovery

If you are actively recovering from credit card debt, paying off collections, or building an emergency fund, debit is the appropriate spending tool while that work is underway. Adding revolving credit during a period of financial instability increases the risk of adding to the problem. Once the foundation is stable, a secured credit card used conservatively is the right next step.

Which Card Offers Better Fraud Protection?

This is one of the most consequential differences between the two cards and one that most consumers misunderstand until they experience fraud firsthand.

The Federal Law Behind Each Card

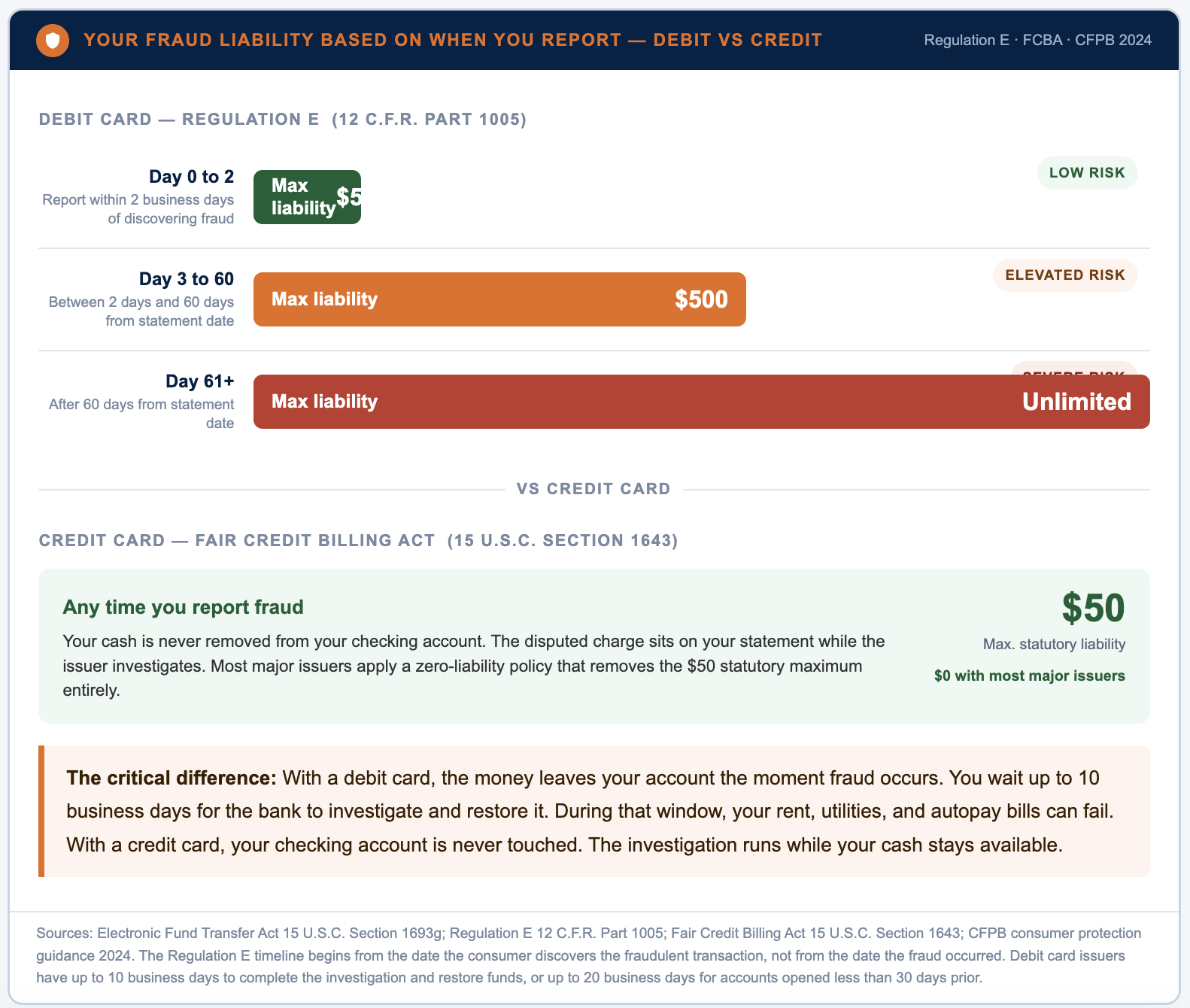

Credit cards are covered by the Fair Credit Billing Act (FCBA), 15 U.S.C. Section 1643. Under the FCBA, your maximum liability for unauthorized credit card charges is $50. Most major issuers have zero-liability policies that eliminate even that $50 exposure. When you dispute a charge, the issuer removes it from your statement while investigating. Your cash is never affected.

Debit cards are covered by the Electronic Fund Transfer Act and Regulation E, 12 C.F.R. Part 1005.

Your liability under Regulation E depends entirely on how quickly you report the fraud:

With a debit card, the money is gone from your account the moment the fraud occurs. You get it back after the bank investigates, which under Regulation E can take up to ten business days, or up to twenty business days for new accounts. During that window, your rent, mortgage payment, and utilities may fail because the stolen funds are not in your account.

With a credit card, the fraudulent charge sits on a statement. Your checking account is untouched. The investigation runs while your actual cash remains available.

Chargeback Rights

A chargeback is the process of disputing a charge and having the issuer reverse it. Credit card chargebacks are governed by card network rules from Visa, Mastercard, and American Express that are separate from and stronger than Regulation E. The chargeback process covers not only fraud but also goods not received, items significantly not as described, and merchants who refuse legitimate refunds. Debit card chargeback rights are narrower and depend more heavily on individual bank policy than on a federal statutory framework.

Does Using a Debit Card Hurt Your Credit Score?

No. Using a debit card has no effect on your credit score in either direction. Debit card transactions are not reported to Equifax, Experian, or TransUnion. Your credit score cannot go up or down based on debit card activity because the credit bureaus have no visibility into your debit card usage.

The misconception that debit card use somehow harms credit comes from confusing credit utilization with spending behavior. Credit utilization measures the ratio of your credit card balance to your credit card limit. It has nothing to do with how much you spend in total or which payment method you use for non-credit purchases.

The only indirect way debit card use can affect your credit is if it leads to overdraft, which can cause other credit obligations like autopay credit card minimums to miss their payment date, triggering a late payment report from the credit card issuer. That late payment affects your credit score. The debit card overdraft itself does not.

Can a Debit Card Improve Your Credit Score?

No. A standard debit card cannot improve your credit score under any circumstances currently recognized by FICO or VantageScore. To improve your credit score, a positive payment behavior must be reported to at least one of the three major credit bureaus. Debit card issuers do not report to the bureaus.

Two partial exceptions exist and both are limited.

Experian Boost is a free Experian product that allows you to self-report certain utility, phone, and streaming service payments to your Experian credit file. These payments are often made via debit or checking account. Experian Boost can raise your Experian FICO score by a modest amount for some consumers. It affects only your Experian report, not Equifax or TransUnion, and is not recognized by all lenders.

```htmlReady to Take Control of Your Credit?

ASAP Credit Repair has helped thousands of consumers understand their credit reports, dispute inaccurate information, and build a stronger financial future. Explore our educational resources or speak with our team to see what options may be available for your situation.

Visit ASAP Credit Repair Get Your Free Credit ReviewSome fintech products including Chime Credit Builder and Extra Debit Card report debit-linked spending as installment-like credit activity to some bureaus. These are niche products and not standard debit cards issued by traditional banks. They work differently from conventional debit cards and are specifically designed to bridge the credit-building gap.

Neither exception replaces the credit-building power of a secured or unsecured revolving credit card with a traditional issuer reporting to all three bureaus.

Recommended Read: Best Credit Card for Military Members (2026)

Why Do Financial Experts Recommend Credit Cards Over Debit Cards?

The recommendation from financial advisors, personal finance educators, and credit professionals is almost universally the same: use credit cards for the majority of purchases and pay the balance in full each month. The reason is not the debt capacity of a credit card. The reason is the stack of structural advantages that come with responsible credit card use.

Credit building: Every on-time payment on a credit card is recorded in your payment history, which is the single largest component of your FICO score at 35%. Fourteen years of on-time debit transactions builds nothing. Fourteen years of on-time credit card payments builds a credit profile that opens doors to mortgages, auto loans, business credit, and rental approvals.

Rewards value: The average cash back rate on U.S. credit cards in 2024 was approximately 1.5% to 2% on general purchases and up to 5% on category bonuses. A household spending $2,000 per month on a 2% cash back card earns $480 per year in cash rewards. A debit card earns nothing. Over ten years that is $4,800 in unrealized value from the payment method alone.

Purchase protection and extended warranty: Many Visa Signature, Mastercard World, and American Express cards include 90-day purchase protection against damage and theft and one to two additional years of warranty coverage beyond the manufacturer's warranty. These benefits apply automatically to eligible purchases charged to the card.

Fraud protection structure: As covered above, the FCBA gives credit card users a $50 maximum liability. More importantly, disputed charges are removed from the statement immediately. Your cash is never at risk.

Travel benefits: Many credit cards include trip cancellation insurance, travel delay coverage, lost baggage reimbursement, and rental car collision damage waiver. These benefits can replace hundreds of dollars in travel insurance purchases annually for frequent travelers.

The responsible use requirement is not optional. Carrying a balance at 20% to 29% APR eliminates every reward and benefit listed above and then continues to cost money on top of them. The credit card advantage is real only when the balance is paid in full each month.

For consumers who cannot yet do that consistently, the debit card is the safer tool until the spending discipline is established.

How Do Banks and Credit Scoring Models View Each Card?

FICO and VantageScore are the two primary credit scoring models used by lenders in the United States. FICO is used in approximately 90% of lending decisions according to FICO's own 2024 disclosure. VantageScore is used in approximately 12.3 billion credit decisions annually per the VantageScore 2024 industry report.

Both models use only data from the credit bureau files at Equifax, Experian, and TransUnion. Neither model receives data from banks about checking account management, debit card transactions, or savings account balances. A consumer with $100,000 in a savings account and no credit history has a lower FICO score than a consumer with $100 in savings and three years of on-time credit card payments, because the scoring models evaluate credit behavior, not wealth.

What credit card issuers report each month to the bureaus: the account open date, the credit limit, the current balance, the minimum payment due, whether the minimum payment was received on time, whether the account is in good standing or delinquent, and whether the account has been charged off or sent to collections.

What debit card issuers report each month to the bureaus: nothing. Standard bank checking accounts are not credit accounts and the banks that issue debit cards have no reporting obligation to any credit bureau for checking account activity.

This structural difference means that two consumers making identical financial decisions, same spending, same discipline, same income, will have vastly different credit profiles if one uses credit cards and the other uses debit cards exclusively.

Good Read: What Is a Soft Pull on Your Credit?

What Are the Biggest Mistakes People Make With Each Card?

Debit Card Mistakes

Using debit for online purchases is one of the most common and costly errors. The fraud liability gap between Regulation E and the Fair Credit Billing Act is largest when fraud occurs online, where card-not-present transactions are easiest for fraudsters to execute and hardest for the bank to reverse quickly. Using debit for online purchases means your real money is at risk the moment the fraud happens.

Using debit for hotels and rental cars creates the authorization hold problem described earlier. A $300 hotel hold on a debit card that takes seven days to release is effectively a seven-day zero-interest loan to the hotel at your expense, with your own money unavailable to you in the meantime.

Relying on debit exclusively to avoid credit card debt solves the debt problem but creates a credit invisibility problem. A consumer who is invisible to the credit bureaus cannot get a mortgage, often cannot rent a competitive apartment, and pays higher insurance rates in states that use credit-based insurance scoring.

Ignoring overdraft fees adds up faster than most people realize. The median overdraft fee in the United States was $35 in 2023 according to the CFPB's annual banking fee study. A consumer who triggers three overdrafts per year pays $105 in fees for the privilege of spending money that was not there, which is a higher effective cost than most credit card annual fees.

Credit Card Mistakes

Carrying a high balance relative to the credit limit is one of the fastest ways to damage a score that credit card use should be building. A credit card with a $1,000 limit carrying an $800 balance is reporting 80% utilization. FICO scoring research indicates that consumers with utilization above 30% see measurable score reduction. Above 50%, the reduction is significant. Above 90%, it is severe. Keeping utilization below 10% produces the best scoring outcomes.

Missing a payment is the single most destructive credit card mistake. A single 30-day late payment reported to the bureaus can lower a credit score by 60 to 110 points depending on the starting score and credit profile. Payment history at 35% of FICO means that consistent on-time payment is the single most valuable credit behavior a consumer can demonstrate.

Closing the oldest credit card account harms the age component of the score. Account age is 15% of FICO. Closing an old account reduces the average age of all accounts and removes the oldest date from the calculation. Many consumers close their first credit card when they upgrade to a better rewards card, unknowingly damaging the age metric they have been building for years. Keep the oldest account open and use it for one small purchase per quarter to keep it active.

Taking cash advances on credit cards carries a 3% to 5% upfront fee and a higher APR than purchases, with interest beginning immediately and no grace period. A $500 cash advance at 29.99% APR with a 5% fee costs $25 immediately plus compounding interest from day one. The debit card and ATM is the correct tool for any cash withdrawal need.

Related Content: Why a Low-Limit Credit Card May Be the Smartest First Card

Which Card Should You Use in Different Situations?

The right card depends on what you're buying, how you manage money, and the protections you need. In some situations, a credit card offers better security and rewards. In others, a debit card helps you stay within your budget.

Credit vs Debit for Your Specific Financial Goals

It also depends on you financial goals...

Should You Use Both a Credit Card and a Debit Card?

Yes. The strongest financial position uses both cards for their distinct strengths rather than choosing one and abandoning the other.

The practical framework used by the credit professionals at ASAP Credit Repair USA with clients rebuilding their financial lives:

Use a debit card linked to your primary checking account for ATM access, budgeted grocery spending, and any category where seeing the real-time balance helps control spending. Keep the debit card for cash management.

Use one or two credit cards for categories where the credit card provides clear advantages: online purchases, travel, hotels, rental cars, gas, and any recurring subscription that benefits from autopay. Set the credit card to pay the full statement balance automatically each month so the balance never carries. This builds payment history, earns rewards, and keeps utilization low simultaneously.

Over time, the credit card builds the credit profile while the debit card maintains the spending discipline. Neither card alone does both jobs well. Together they serve different functions in a single financial ecosystem.

```htmlReady to Take Control of Your Credit?

ASAP Credit Repair has helped thousands of consumers understand their credit reports, dispute inaccurate information, and build a stronger financial future. Explore our educational resources or speak with our team to see what options may be available for your situation.

Visit ASAP Credit Repair Get Your Free Credit ReviewA client who came to ASAP Credit Repair USA in January 2026 with a 592 score and no open credit accounts had spent nine years using only a debit card out of a genuine belief that avoiding credit was financially responsible.

We helped her open a secured credit card with a $500 limit and set a $40 streaming subscription to charge to it each month with full autopay. By October 2026, her score had reached 671 without any other changes to her financial behavior, simply from the addition of twelve months of reported on-time payment history and a low utilization rate on one account. The debit card she had used for nine years contributed nothing to that improvement. One credit card, used conservatively, contributed everything.

Credit vs Debit: Frequently Asked Questions

Does a debit card build credit?

No. Debit card transactions are not reported to Equifax, Experian, or TransUnion under any standard banking relationship. Your payment behavior with a debit card is invisible to credit scoring models. To build credit, you need an account that a creditor reports to at least one bureau. Standard debit cards issued by traditional banks do not meet that requirement.

Can I improve my credit score with a debit card?

Not through a standard debit card. Experian Boost allows you to self-report certain utility and phone payments that may be made via checking account, which can modestly improve your Experian FICO score. Fintech products like Extra Debit Card and Chime Credit Builder are designed specifically to bridge this gap but are not conventional debit cards. A secured credit card remains the most straightforward and widely recognized path to building credit from scratch.

Why do hotels prefer credit cards?

Hotels prefer credit cards because the authorization hold affects available credit rather than actual cash. This protects the hotel's ability to collect for damages or incidentals while not stranding the guest without access to their money. Many hotel brands will decline a debit card for the hold portion of the reservation entirely and require a credit card at check-in even if debit is accepted at checkout.

Should teenagers have debit cards or credit cards?

Start with a debit card or a prepaid debit card. The spending discipline of living within a visible balance is a foundational skill. A credit card for a teenager is appropriate only when the teen demonstrates consistent spending discipline and has a clear understanding of how interest accumulates and how payment history affects credit. Many financial advisors recommend adding a teenager as an authorized user on a parent's credit card rather than giving them a card with their own credit limit.

Can I dispute debit card fraud?

Yes, under Regulation E. Contact your bank immediately. Your liability is $50 if you report within two business days of discovering the fraud. Waiting two to sixty days raises potential liability to $500. Waiting more than sixty days from the statement date removes the statutory liability protection entirely. The bank has ten business days to complete the investigation and restore the funds, or twenty business days for newer accounts.

Do debit cards earn rewards?

Rarely and in small amounts compared to credit cards. A minority of banks offer modest debit card rewards programs. Credit unions sometimes offer more competitive debit rewards. The average cash back on debit is well below 0.5% where programs exist at all, compared to 1.5% to 5% commonly available on consumer credit cards. The reward gap is a structural reason financial advisors recommend credit card use for reward-earning spending categories.

Should I use debit for online shopping?

No. Online purchases represent the highest fraud risk category for debit cards. Card-not-present fraud is easier to execute and harder to reverse. Your checking account balance is directly at risk. A credit card online purchase carries the same products and services with the FCBA's $50 maximum liability and the ability to dispute charges without your cash being touched. The credit card is the correct tool for online shopping in every practical scenario.

Can using a credit card hurt my credit score?

Yes, under specific conditions. Carrying a balance above 30% of your credit limit hurts your utilization score. Missing a payment creates a late payment record in your payment history. Applying for multiple new cards in a short window creates multiple hard inquiries. Closing old cards reduces your average account age. None of these are consequences of using a credit card. They are consequences of using one carelessly. Responsible use, paying on time, keeping balances low, and not applying for many cards simultaneously, produces the opposite effect and builds your score over time.

Why do rich people use credit cards more than debit cards?

High-income consumers use credit cards for the same structural reasons any disciplined consumer should: fraud protection, rewards accumulation, purchase protection, and credit history maintenance. Consumers with high liquidity face the least risk from credit card usage because they are positioned to pay balances in full each month. The behaviors that make credit card use beneficial, paying in full, keeping utilization low, and maintaining accounts long-term, are the same behaviors that compound financial stability over time.