If you have ever looked at your credit report and seen a company name you do not recognize in the inquiries section, your first reaction was probably panic. You thought someone pulled your credit without permission. You worried your score dropped. You wondered if someone stole your identity.

Here is what most likely happened: a soft credit check showed up on your report. And this type of check never hurts your score. Not by one point. Not ever.

I run a credit repair company and have worked with over 22,000 clients. I see this reaction every week. Someone stares at their report, points to an inquiry, and says, "I never applied for anything. What is this?" Nine times out of ten, it is a pre-approval screening triggered it, an insurance review, or a credit monitoring service they signed up for and forgot about. Once I explain it, the stress disappears immediately.

What Is a Soft Pull on Your Credit?

This type of credit check is not connected to a formal application for new credit. It gives whoever is checking a limited snapshot of your credit history. It does not trigger any impact on your score.

When you check your own credit score on Credit Karma, that is a soft pull. When a credit card company mails you a pre-approved offer, they run a soft pull first to see if you qualify. When your landlord checks your background before handing you a lease, that check is also soft.

Here is the part that matters most to you: other lenders cannot see your soft pulls. They only appear on your personal copy of your report. No lender reviewing your credit for a mortgage or car loan will ever see a soft inquiry. It does not factor into their decision at all.

The CFPB defines soft inquiries as reviews of your credit file that are not tied to a specific application for new credit. That definition alone tells you everything. No application means no scoring consequence.

What Does a Soft Pull Show on Your Report?

When a company runs a soft pull on your credit, they do not see everything. They get a limited view. Here is what a soft pull typically reveals about you:

Your general credit score range

Your payment history overview

Whether you have any accounts in collections

A summary of your open accounts and account types

Any public records, such as a bankruptcy

What they do not see: your full account numbers, the exact credit limits on each card, or the detailed account history a mortgage lender reviews in a full credit report. SoFi's 2025 lending guide describes soft inquiries as a "basic snapshot," not a complete financial picture. That limited view is exactly why companies cannot use a soft pull to make a final lending decision. For that, they need a hard pull.

What Causes a Soft Pull on Your Credit Report?

These checks happen all the time, often without you doing anything. Here are the most common situations:

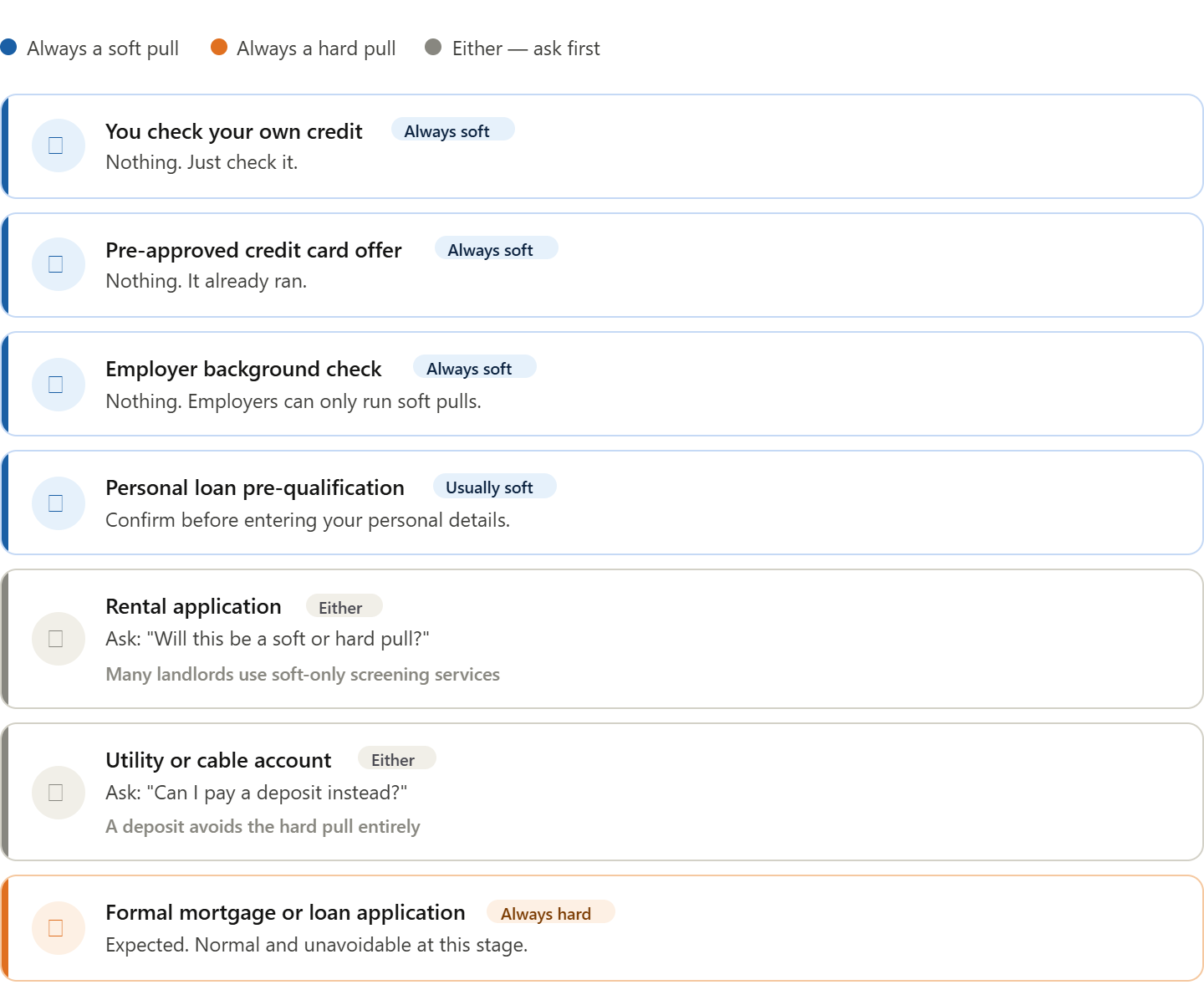

You check your own credit. Any time you pull your own report or check your score through a free tool, that is a soft pull. Do it as often as you want.

You receive a pre-approved credit offer. Before a card issuer mails you that offer, they run a soft pull to screen whether you qualify.

An employer runs a background check. If you apply for a job that involves finances or security clearance, the employer may review your credit. It is always a soft pull. Employers cannot run hard pulls.

Your landlord screens you as a tenant. Many rental applications include a soft credit check before they ask you to formally apply.

An insurance company reviews your profile. Auto and home insurers use this type of check to help set your premiums. This is legal under the FCRA.

A lender pre-qualifies you for a loan. When you ask "what rate could I get?" without formally applying, the lender runs a soft pull to give you an estimate.

Your existing card issuer monitors your account. Credit card companies periodically review your credit to manage their risk on your open accounts.

A Buy Now Pay Later service screens you. Many BNPL providers check your credit before approving a purchase. Most use soft pulls.

Soft Pull vs. Hard Pull: What Is the Difference?

The difference between these two inquiry types is simple once you see it laid out.

Soft credit check:

This check happens when someone reviews your credit for informational or pre-screening purposes. It does not require your formal authorization. It has zero impact on your credit score. Only you can see it on your report.

Hard pull:

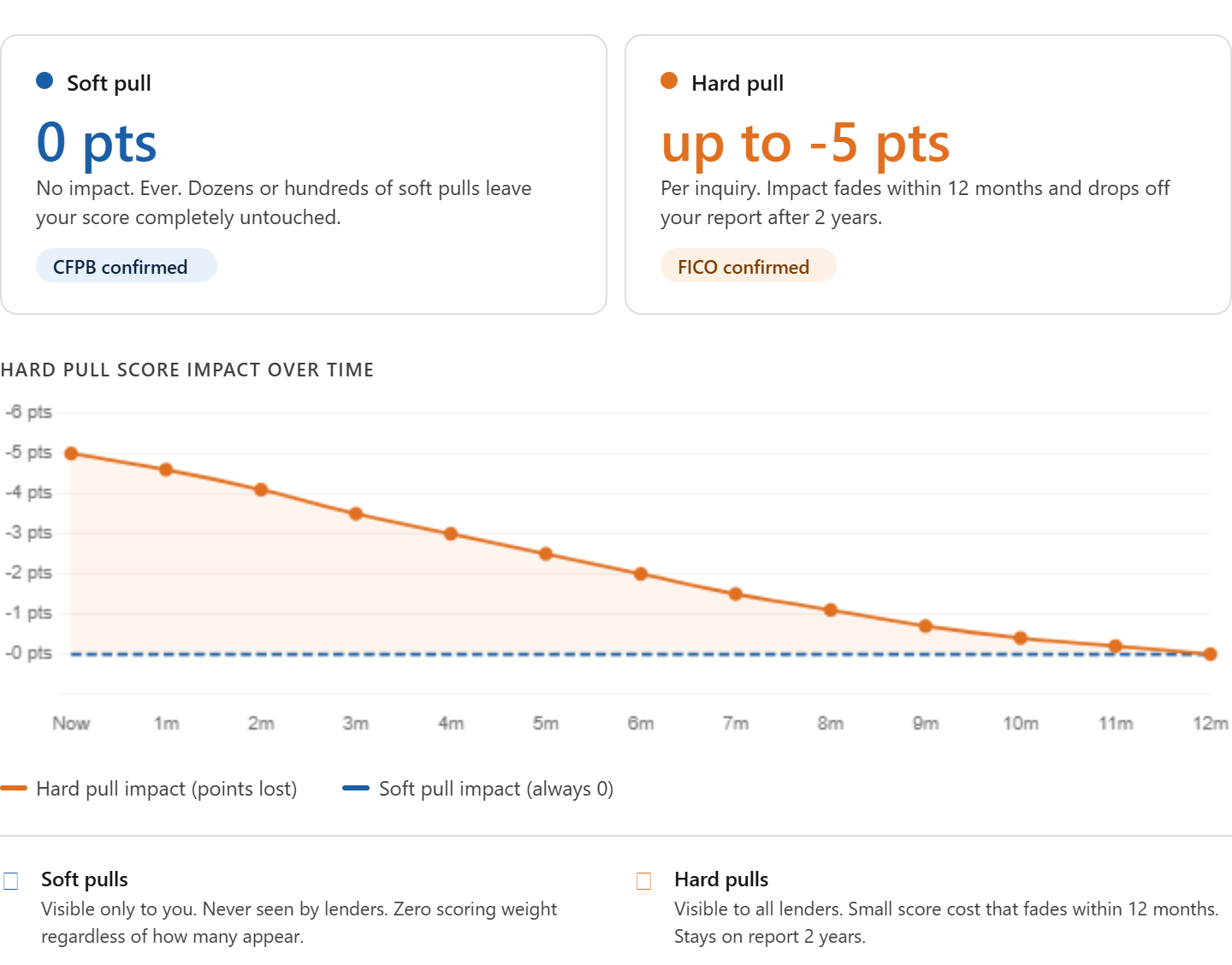

A hard pull happens when you formally apply for new credit, like a mortgage, car loan, or credit card. You must authorize it. It can drop your score by up to five points. Every lender who pulls your full report can see it, and it stays visible for two years.

Both types of inquiries pull from the same credit data. The difference is the purpose and the consequence.

One thing worth knowing: some situations can go either way. Renting an apartment, opening a utility account, or applying for a cable plan can result in either a soft pull or a hard pull, depending on the company. Before you agree to any credit check in those situations, ask one question: "Will this be a soft pull or a hard pull?" That question takes five seconds and can protect your score when you are preparing for a major loan application.

Experian recommends asking this before any non-loan credit check, especially when you are in the 60 to 90 days before applying for a mortgage.

Does a Soft Pull Hurt Your Credit Score?

No. This type of check does not hurt your score. At all. This is one of the most definitive rules in all of credit. There are no exceptions.

You can check your own credit every single day. You can receive 30 pre-approval mailers in a month. You can switch insurance providers, apply for three rentals, and let your employer run a background check, all in the same month. None of those soft pulls will touch your score.

The confusion comes from not knowing what type of inquiry you are looking at. When you see an unfamiliar name in the inquiries section of your report, your instinct is to assume something bad happened. So before you worry, find out whether it is a soft pull or a hard pull. If it is soft, move on. If it is a hard pull you never authorized, that is the one worth investigating.

⚠️ An unauthorized hard pull is the only inquiry worth disputing. Under the Fair Credit Reporting Act, a lender needs your permission to run a hard pull. If you find one on your report that you never authorized, dispute it with the bureau that shows it. An unauthorized hard pull can signal identity theft and can be removed through the FCRA dispute process.

How Long Does a Soft Pull Stay on Your Credit Report?

A soft inquiry can stay on your report for up to two years. But since it carries no scoring weight and only you can see it, its presence makes no difference to your financial life.

One small detail from TransUnion worth knowing: some soft pulls are visible to companies within the same industry. If you switched auto insurers twice in a year, other insurance companies can see those soft pulls. But a mortgage lender or credit card issuer cannot. The FCRA controls exactly who can see what, and it is designed to protect you from companies using that data in ways that do not apply to their relationship with you.

Can You Remove a Soft Pull from Your Credit Report?

You cannot dispute or remove a soft pull from your credit report in most cases. And you do not need to. A soft inquiry has no negative impact. Removing it would change absolutely nothing about your score or how lenders see you.

If you want to clean up your inquiries section, focus only on unauthorized hard pulls. Those have a real effect and can be legitimately disputed. A soft inquiry from a pre-qualification check or a card company's pre-approval screening is harmless and not worth your time to challenge.

When to Ask if It Is a Soft Pull Before You Agree

Here is a practical table you can use the next time someone wants to run a credit check on you.

Your Soft Pull Checklist

Before you let any company run a credit check on you, go through this list:

Ask whether they plan to run a soft pull or a hard pull

Use pre-qualification tools first when you shop for loans. They use soft pulls

Check your own credit as often as you want. It is always soft and never costs you points

Review your inquiries section every few months to spot unauthorized hard pulls

Dispute any hard pull you did not authorize with the bureau that shows it

Do not worry about soft pulls. They cannot hurt you

A soft inquiry is not a threat. It is a routine part of how your financial data flows. The faster you understand what a soft inquiry is, the faster you stop worrying about it and start focusing on the things that actually affect your score. Soft inquiries tell the story of who looked. Hard pulls tell the story of what you applied for. Only the second one has any cost, and even that cost is small and temporary.