A low-limit credit card builds your credit, protects your finances, and trains better spending habits, and most people underestimate how powerful one can be. The average American now carries $6,523 in credit card debt as of Q3 2025, according to TransUnion. High credit limits make that number climb fast. A low-limit card does the opposite.

I run a credit repair company, and one of the most common cases I see is this: someone gets approved for a $5,000 limit card on their first try, maxes it out within three months, and comes to us two years later trying to undo the damage. It is one of the most predictable patterns in credit mismanagement, and it is almost always preventable. A Reddit thread in r/personalfinance (source) put it plainly: "Start with a low limit. You can always ask for more. You can't undo a maxed card." That one comment has over 2,000 upvotes.

U.S. credit card debt hit $1.252 trillion in Q1 2026, per Motley Fool research (source). Nearly 46% of cardholders carry a balance from month to month. A low-limit credit card is one of the clearest structural defenses against becoming part of that statistic.

What Is a Low-Limit Credit Card?

A low-limit credit card comes with a credit ceiling between $200 and $1,000. Secured cards usually sit at the lower end of that range. Some starter unsecured cards go up to $500 or $750 for first-time applicants.

Credit card issuers set your limit based on your income, credit score, credit utilization, and payment history. A thin or damaged credit file gets a low limit. That is not a punishment. That is the system working as designed, starting you where you can prove yourself without taking on a large risk.

How Credit Limits Are Set

Lenders calculate your limit using your debt-to-income ratio, existing balances, and credit history length. A higher income and a clean credit file unlock a higher ceiling. A new borrower with no history gets a low one. Discover confirms that lower limits are generally easier to qualify for because they carry less risk for the lender (source).

Why a Low Credit Limit Card Actually Protects Your Credit Score

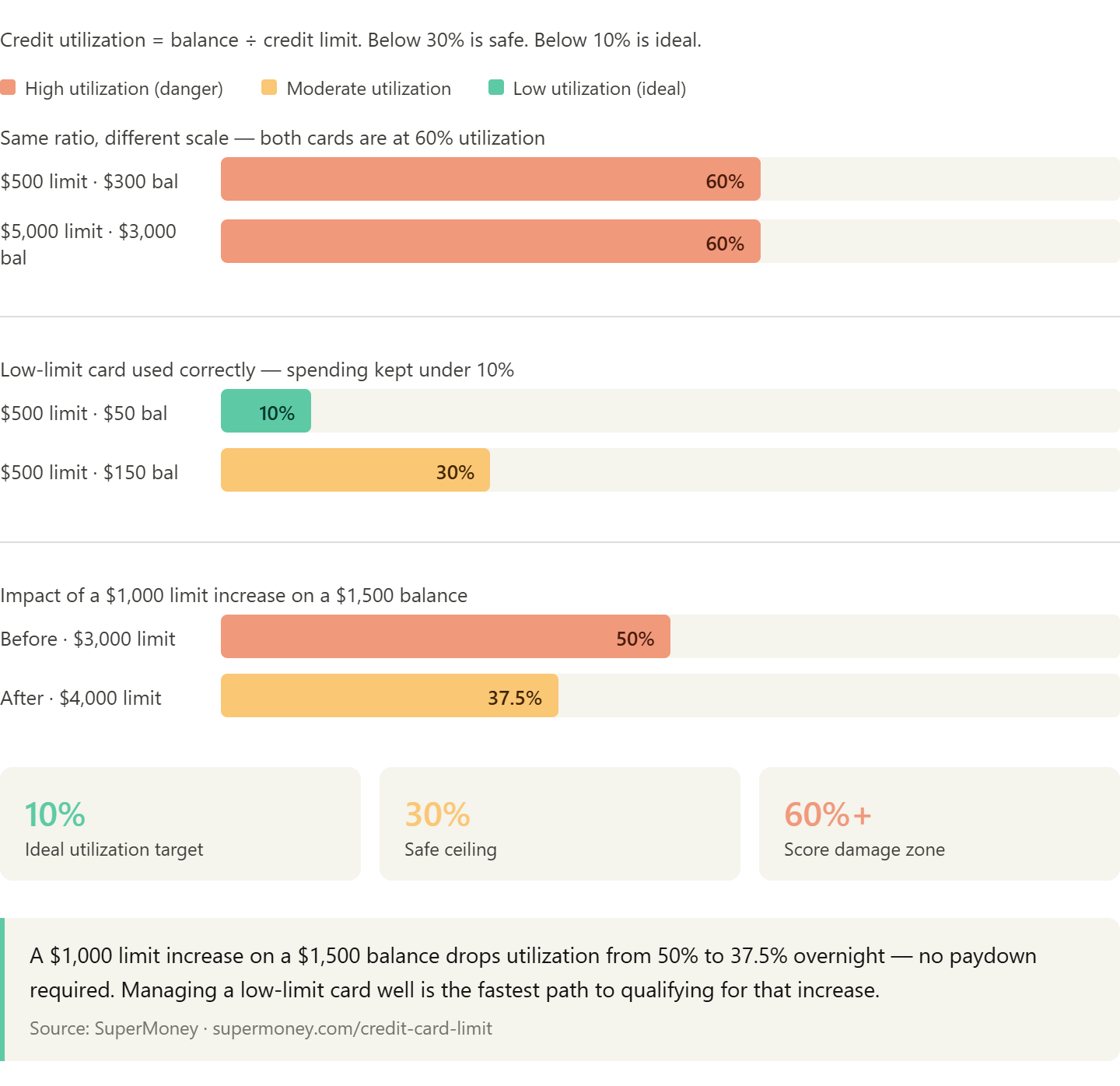

Credit utilization makes up 30% of your FICO score. Utilization measures how much of your available credit you use at any time. The recommended ceiling is 30%. The ideal target is below 10%.

Here is where a low-limit card becomes a double-edged tool. If your limit is $500 and you charge $300, your utilization on that card is 60%. That one card can drag your score down fast. This is why low-limit cards require more discipline, not less.

The flip side: if you keep your spending low on a $500 card, say $50 per month, your utilization is 10%. That number tells every bureau you are a responsible borrower. Over six to twelve months, that behavior alone can move a score by 30 to 50 points, based on patterns we see regularly in our credit repair work.

Why Staying Below 30% Utilization Matters More Than Your Limit Size

Does a Low-Limit Credit Card Build Credit?

Yes. Any credit card that reports to Equifax, Experian, and TransUnion builds credit. The limit size does not determine whether the card reports. Payment history does the heavy lifting at 35% of your FICO score.

Secured cards with $200 limits build credit just as effectively as $10,000 rewards cards, as long as you pay on time every month. Credit bureaus do not reward size. They reward consistency.

How Long Does It Take to Build Credit with a Low-Limit Card?

Most people see measurable score movement within three to six months of opening a low-limit card and making on-time payments. A full credit profile takes twelve to twenty-four months to develop. U.S. News reports that credit expert Michelle Black describes low-limit cards as "a good option for people who have no credit history or damaged credit history" because they let borrowers prove themselves with lower risk to the issuer (source).

The key variables are payment history, utilization, and time. All three work in your favor when you use a low-limit card the right way.

Who Should Get a Low-Limit Credit Card?

A low-limit card fits four types of people well.

First-time credit users with no file. Banks see no history and offer a small limit to test behavior.

People rebuilding after debt or bankruptcy. A secured card restarts the credit clock without risking large new balances.

People with spending discipline problems. A hard ceiling on a card prevents the kind of runaway spending that creates long-term debt cycles.

People who want a dedicated budget card. Charge groceries only to a low-limit card, and you get automatic monthly tracking with a built-in spending cap.

In our practice, the third group is the one I see most often. Last year, over a third of new clients who came to us had their credit damaged not by missed payments but by consistently high utilization across multiple cards. A low-limit card used for one category, paid in full monthly, would have prevented most of that damage entirely.

Is a Low-Limit Card Good for People Recovering from Debt?

Yes. Gulf News spoke with UAE-based credit advisor Essam Kabeelali, who stated that for people recovering from debt, "a starter card with a low limit can be a great way to ease back in, helping you regain financial confidence while keeping risks in check" (source).

A low-limit card after debt recovery serves as a reset tool, not a restriction. You rebuild trust with lenders, prove new habits, and avoid re-entering the debt cycle that brought you there.

Can a Low-Limit Credit Card Hurt Your Credit Score?

Yes, if you misuse it. Two specific behaviors damage your score on a low-limit card.

Maxing it out: Charging close to or at your limit spikes utilization. A $500 card with a $480 balance is 96% utilization. That single number can drop a score by 50 points or more.

Missing payments: A payment that goes 30 days past due gets reported to all three bureaus. On a low-limit card, the dollar amount owed may be small, but the damage to your payment history is identical to a missed payment on a $10,000 card.

Experian confirms that keeping utilization under 10% is best for your scores, and that you should monitor each card's ratio, not just your overall ratio (source).

What Happens If Your Credit Limit Gets Lowered?

Issuers can lower your credit limit at any time, especially if you stop using the card or they perceive rising risk. VantageScore explains that a limit reduction spikes your utilization immediately, even if your balance and spending behavior have not changed (source). If your $1,000 limit drops to $500 and you carry a $400 balance, your utilization jumps from 40% to 80% overnight.

This is why you should use every card regularly, even for small purchases, and pay it off monthly. Active accounts rarely get their limits cut.

How to Get the Most Out of a Low-Limit Credit Card

Treating a low-limit card as a credit-building tool rather than a spending tool is the core strategy. Here is the approach that works:

Charge one recurring expense to the card each month. Subscriptions, gas, or groceries work well.

Pay the full statement balance before the due date every month. Do not carry a balance.

Keep your balance below 10% of the limit at statement close. If your limit is $500, keep the reported balance under $50.

Request a credit limit increase after six to twelve months of on-time payments. Most issuers allow this through the app or online.

Do not close the card after you get a higher-limit card. Keeping it open maintains your total available credit and your account age.

The average credit utilization rate across all American cardholders sits at 29% as of 2025, per Experian (source). That is right at the edge of the recommended ceiling. Dropping your personal utilization below 10% puts you ahead of the majority of cardholders, and lenders notice.

Start Small. Build Smarter.

Use a Low-Limit Credit Card the Right Way

A low-limit card can help you build credit, control spending, and avoid debt when you keep balances low and pay on time.

Check Your Credit Report NowSee what is helping or hurting your credit before you apply.

When to Move Past a Low-Limit Card

A low-limit card is a starting point, not a permanent home. Once your score crosses 680 to 700, most rewards cards become accessible. Once you have twelve months of clean history on your low-limit card, request a limit increase from your issuer first. Many will grant it without a hard inquiry.

If your issuer denies the increase, apply for a second card with a different issuer. Two cards with low limits and clean histories build credit faster than one card with a high limit and erratic usage. Credit mix and total available credit both factor into your score, and two cards with separate issuers' addresses do.

A low-limit credit card is not a ceiling on your financial life. It is the foundation you build from. Start there, use it correctly, and the rest of the credit system opens up on your terms.