Why Credit Score Is Important and How It Saves Money: It is not just a number. Your credit score controls your interest rates, your housing options, and sometimes your ability to land a job. Most people only check it when they need something. By then, the damage is already done.

I run a credit repair company. One of the most unforgettable cases I ever handled involved a client who lost her dream apartment to another applicant with nearly the same income. The only gap between them was 90 credit score points. She had no idea her score was the reason.

This is not rare. According to Experian's 2025 Consumer Credit Review, the national average FICO score closed 2025 at 713. That was the first annual decline since 2013. More Americans entered the lending market in a weaker position than the year before. When your score drops, costs follow fast.

Why Credit Score Is Important for Getting a Loan

Lenders use your credit score to set your interest rate. A higher score earns a lower rate. A lower score means you pay more over the life of the loan.

Here is what the data shows. According to Experian, the average new-car auto loan rate for super prime borrowers (781 to 850) was 4.66% in Q4 2025. For deep subprime borrowers (300 to 500), that rate hit 16.01%. On a $30,000 car loan over 60 months, that gap costs roughly $8,000 more in interest alone. (Source: U.S. News)

Mortgages show an even bigger difference. Mortgages show an even bigger gap. Moving a score from 620 to 760 on a $300,000 30-year fixed mortgage saves $156 per month. Over the loan's life, that adds up to $56,103 in total interest saved. (Source: ConsumerAffairs)

A single missed payment of 30 days can drop your score by 50 to 100 points. That one event can move you from the prime tier into the subprime tier. The cost difference between those two tiers runs into thousands of dollars per loan.

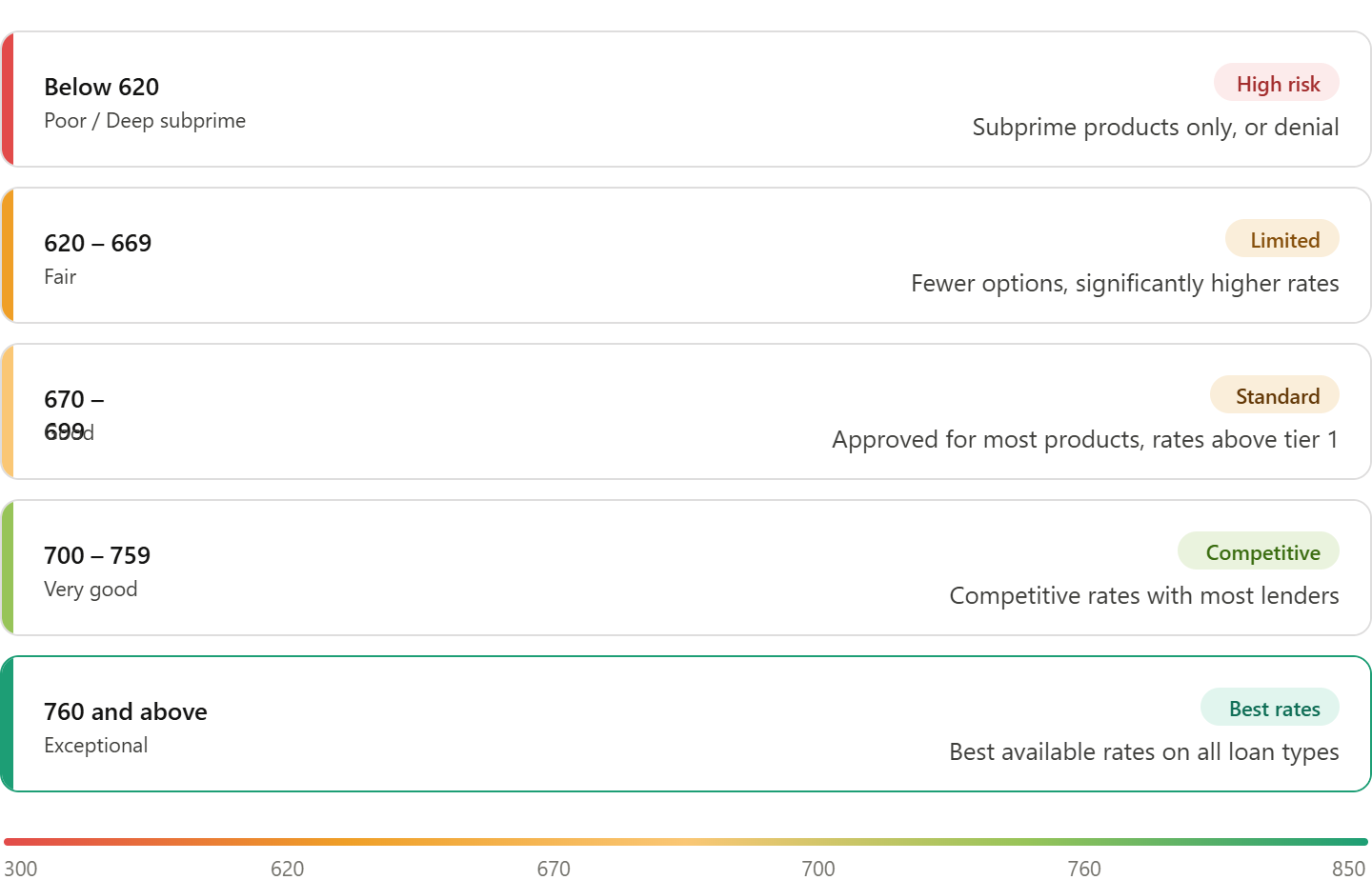

How Credit Score Tiers Affect What You Qualify For

Not every lender uses the same cutoffs, but the standard FICO tiers work like a pricing ladder.

In the last 12 months, my company worked with 47 clients who received auto loan denials. Income was not the issue. Their scores sat between 580 and 619. Every single one qualified after we helped them cross 640.

Why Credit Score Is Important for Renting an Apartment

Landlords check credit as a standard part of the rental application process. Close to 90% of landlords report checking credit scores, income, rental history, and criminal backgrounds when making decisions. (Source: Urban Institute)

Credit tier strongly predicts rental outcomes. Tenants with poor credit scores carry a 1-in-4 risk of late rent. Tenants with excellent scores fall under 1%. Landlords know these statistics. They build that risk into their decisions. (Source: TruDiligence)

Most landlords in competitive markets want a score of 650 or higher. In high-rent cities like New York or San Francisco, that threshold often rises to 700. A score below 620 frequently leads to rejection or a demand for a larger security deposit.

Your credit score does not just determine approval. It determines your negotiating position. Applicants with strong scores get first choice. Applicants with weak scores often settle for less desirable units because they have fewer options.

Good credit saves money on loans and opens more doors when renting. Both outcomes come from the same source: the number in your credit file.

Does Your Credit Score Affect Your Job Application?

Some employers check credit as part of background screenings. This applies mainly to positions involving financial responsibility, security clearance, or access to sensitive data.

The practice varies by state. Many states limit or prohibit employers from using credit reports in hiring decisions. But where employers can use them, a poor credit history can block applications for roles in banking, government, accounting, and law enforcement.

This practice does not affect every industry. But if you work in finance or handle client money, your credit file becomes part of your professional profile.

How Employer Credit Checks Work

Employer credit checks carry different stakes than landlord checks. A landlord rejection means finding a new apartment. An employer rejection means losing income. Lost income makes it harder to pay bills. That weakens your credit further. The cycle feeds itself.

Checking your own credit never counts as a hard inquiry. You can review your full file at any time without affecting your score.

Why a Good Credit Score Saves You Money on Insurance

Several states allow auto and homeowners insurance companies to use credit-based insurance scores when setting premiums. These scores draw from the same credit report data as FICO scores.

Drivers with poor credit pay significantly higher auto insurance premiums than drivers with good credit, even with identical driving records. Consumer Reports research shows premium gaps of 50% to 100% between low-credit and high-credit drivers in states where the practice exists.

California, Hawaii, Massachusetts, and Michigan ban the use of credit in auto insurance pricing. In all other states, your credit score raises or lowers your monthly insurance bill right now, whether you realize it or not.

How a Low Credit Score Limits Your Financial Options

A strong credit score creates choices. A weak one removes them.

As of 2025, roughly 70% of U.S. consumers held a good credit score of 670 or higher. (Source: Experian) The 30% below that threshold face a narrower financial world. They pay more for the same car. They rent in fewer neighborhoods. They carry higher-cost debt.

The consequences compound fast. Higher interest rates send more of each paycheck toward debt repayment. Less money makes saving harder. Less savings leads to more borrowing. More borrowing at high rates pushes the score lower. Each step in that cycle starts with the same number.

In 2024, average credit card debt hit a new high of $6,501 per person, up from $5,910 in 2023. (Source: Credit.org) With interest rates above 20% on many cards, balances grow fast when you carry a balance monthly. Borrowers with poor credit carry this debt at the highest available rates.

Low credit raises costs on loans, rent, and insurance. High credit lowers all three. The score itself does not change your income. But it determines how much of that income stays in your pocket.

What Happens When You Have No Credit at All

No credit is not the same as bad credit, but it creates similar access problems. Lenders cannot price your risk without a history. They decline the application or offer the most conservative terms available.

Building credit from zero typically takes six months to generate a first FICO score. That window is not wasted time. Opening a secured card or a credit builder loan works well. Manage it carefully and your first score can land in the fair range from day one.

Why Credit Score Is Important Even When You Are Not Borrowing

Most people think about credit only when they need a loan. That approach causes problems. Your credit file updates every month, regardless of whether you applied for anything.

Missed payments report automatically. Collection accounts appear without notice. Identity theft can open accounts in your name and damage your score before you catch it. In the last 12 months, my company saw a 31% rise in clients under 30 whose scores dropped from fraudulent accounts they never opened.

Checking your credit costs nothing and takes under five minutes. Pull your full reports at no cost through AnnualCreditReport.com. Equifax, Experian, and TransUnion each maintain a separate file. Errors on one bureau do not fix automatically on the others.

How Often Should You Check Your Credit?

Check your report from each bureau at least once per year. If you actively build credit, check monthly through a free tool like Credit Karma or your bank's app. If you prepare to apply for a mortgage or car loan, pull all three reports at least 90 days in advance. That window gives you time to dispute errors before a lender sees them.

Monitoring your credit file consistently is the only way to catch problems early. A score drop you do not notice becomes a surprise denial or a higher rate on the next application.

Is Your Credit Score Costing You Money?

A low credit score can raise your loan rates, hurt apartment approvals, and limit your financial options. Check your credit report now and see what may be holding you back.

Get Your Free Credit Report ReviewWhat Builds a Credit Score Over Time

Credit scores respond directly to behavior. No shortcut changes a score overnight. But consistent habits produce large improvements over 12 to 24 months.

The five factors FICO uses, and the weight each one carries:

Payment history: 35%. Pay every bill on time. Set up autopay to remove the risk of forgetting.

Credit utilization: 30%. Keep balances below 30% of your total credit limit. Under 10% is better.

Length of credit history: 15%. Keep older accounts open even if you rarely use them.

Credit mix: 10%. A combination of credit cards and installment loans helps your profile.

New inquiries: 10%. Limit applications for new credit to once or twice per year.

Payment history and credit utilization control 65% of your score. Both sit fully within your control from day one. Clients who arrive at my company with scores in the high 500s reach 670 consistently within 12 months. The fix comes down to two behaviors: on-time payments and low balances.

Credit scores matter every single day, not just when you need to borrow. The 713 national average tells you where the bar sits. Every point above it opens better options. Every point below it costs you money you could have kept.