Getting calls from 800-346-0775? You're on the right page. This number has been reported by thousands of people, and if you're here, you probably want straight answers about who's calling, why they're calling, and what you can do about it.

Quick Answer: Who is 800-346-0775?

800-346-0775 belongs to Central Financial Control, a legitimate debt collection agency. They're not a scam, but they are persistent debt collectors who may be calling about an unpaid debt from a credit card, medical bill, or other account.

Most Common Reasons They Call:

- Outstanding credit card debt

- Medical bills sent to collections

- Unpaid utility bills

- Student loan defaults

- Personal loan defaults

What should you do?

Don’t panic or admit anything right away. Ask for written debt validation, check your credit report, and understand your rights under the Fair Debt Collection Practices Act (FDCPA). You can negotiate a settlement, set up a payment plan, or send a cease and desist letter to stop calls.

👉 Keep reading below for step-by-step guides, letter templates, and ways to protect your credit.

Who is 800-346-0775?

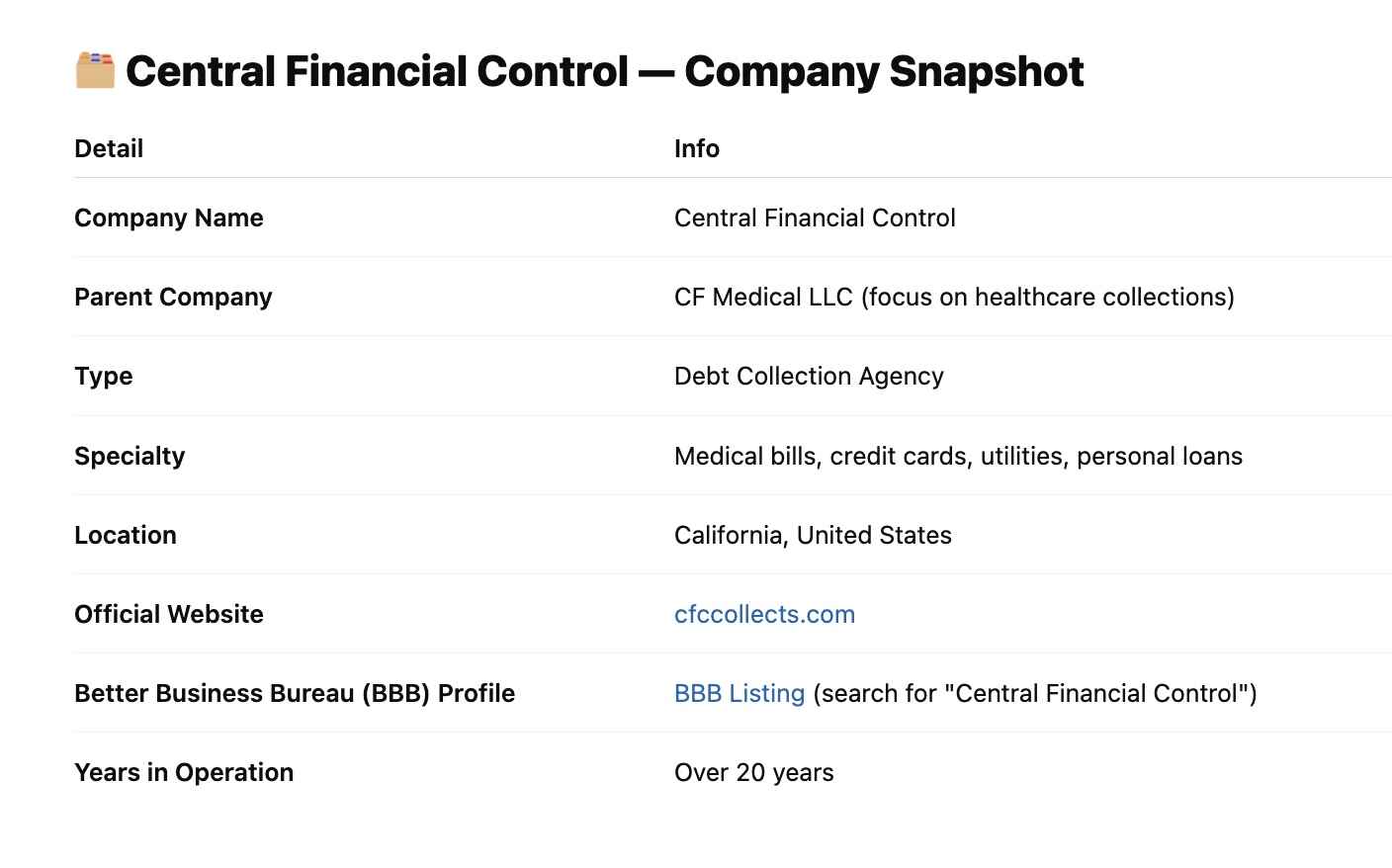

The number 800-346-0775 belongs to Central Financial Control, a legitimate debt collection agency based in California. They specialize in collecting unpaid debts on behalf of hospitals, clinics, credit card issuers, utility companies, and other creditors across the U.S.

Central Financial Control is not a scam; they are a real, licensed agency that’s been operating for years. They’re also registered with the Better Business Bureau (BBB) and are known for working mainly with medical providers and large service organizations.

"I was terrified when I first got a call from 800-346-0775. I thought it was a scam, but after checking, I realized it was a real medical bill I forgot about after my surgery. I negotiated a payment plan, and they actually worked with me."

— Emily R., Arizona

Even though they’re legitimate, you should always verify every detail when you receive a collection call. Scammers can spoof this number to impersonate Central Financial Control and trick you into paying fake debts.

About Central Financial Control

Central Financial Control is part of the CF Medical group, which focuses on healthcare-related debt collections. They often step in after a hospital or doctor’s office has tried and failed to collect your bill. If your debt has been turned over to them, it means your original provider no longer handles your payments directly.

While they are allowed to contact you to try to collect a valid debt, they must follow strict rules under the Fair Debt Collection Practices Act (FDCPA). That means they can’t harass you, lie about the amount, or threaten illegal actions.

Before you pay anything or give out personal information, always:

- Request written debt validation

- Check your credit report for any collection entries

- Contact Central Financial Control directly through their official phone number or website to confirm

Knowing who they are — and your rights — helps you handle the situation calmly and avoid costly mistakes.

Is 800-346-0775 a Scam or Legit?

It's 100% legitimate. Central Financial Control is a licensed debt collection agency registered with the Better Business Bureau.

However, scammers sometimes spoof this number, so you need to verify any caller claiming to be from Central Financial Control.

Red Flags That Indicate a Scam:

- They demand immediate payment via gift cards or wire transfers

- They threaten arrest or legal action within 24 hours

- They won't provide written verification of the debt

- They ask for banking information over the phone

- They use aggressive or threatening language

How to Verify It's Really Central Financial Control:

- Ask for their name, company, and callback number

- Request written verification of the debt

- Call Central Financial Control directly at their official number to confirm

- Check if the debt appears on your credit report\

Why is 800-346-0775 Calling Me?

Central Financial Control typically calls when:

1. Your Original Creditor Gave Up

After 90-180 days of non-payment, many creditors sell or assign debts to collection agencies. This is when Central Financial Control gets involved.

2. You Have a "Charged-Off" Account

When a creditor marks your account as "charged off" (usually after 6 months), it doesn't mean the debt is forgiven. It often gets sold to collectors like Central Financial Control.

3. Common Debt Types They Collect:

- Credit Card Debt (most common)

- Medical Bills from hospitals and clinics

- Utility Bills (electricity, gas, water, internet)

- Personal Loans and payday loans

- Student Loans (federal and private)

- Auto Loans and deficiency balances

Real Example:

"I had a credit card with a $2,500 balance that I couldn't pay after losing my job. After 6 months, 800-346-0775 started calling. Turns out my bank sold the debt to Central Financial Control for probably $250, and now they're trying to collect the full amount." - Sarah, Chicago

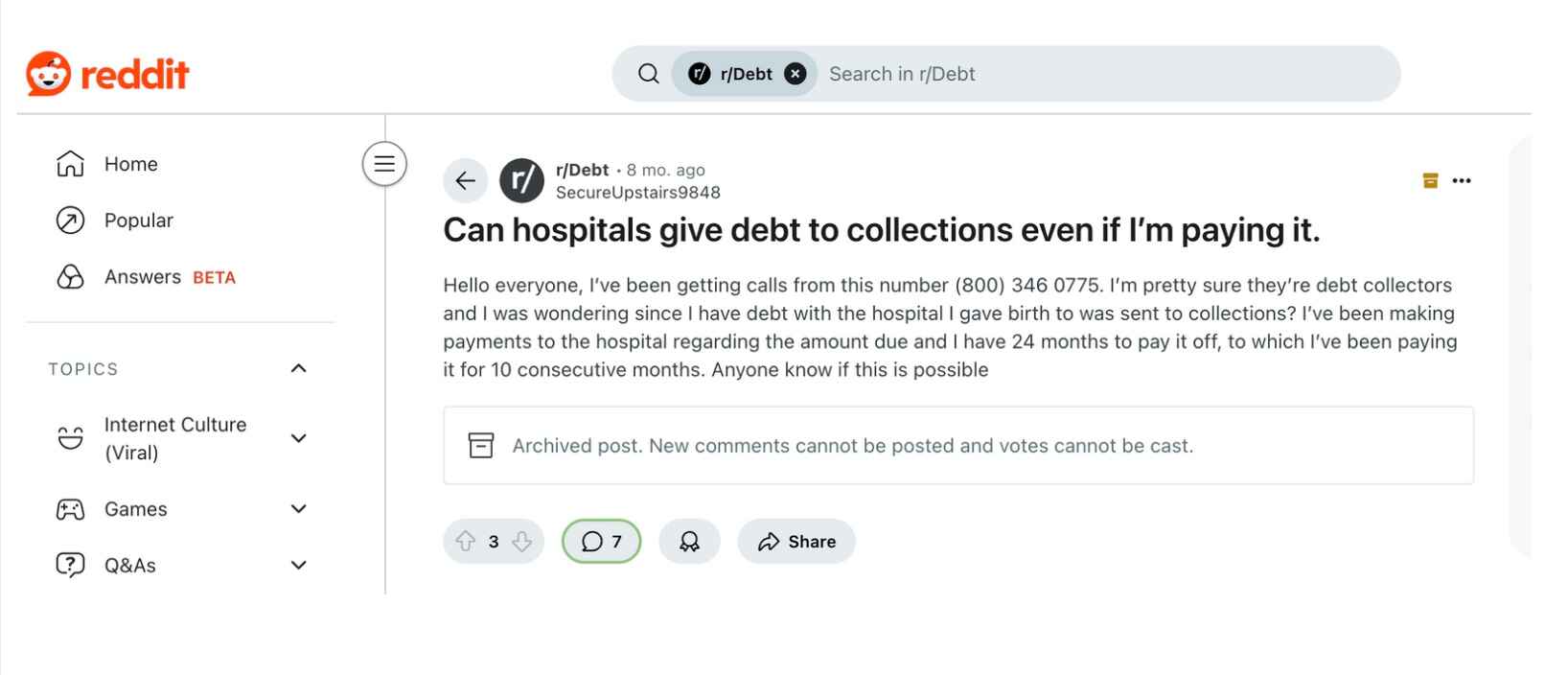

Another User from reddit shared:

"Hello everyone, I’ve been getting calls from this number (800) 346-0775. I’m pretty sure they’re debt collectors. I was wondering — the hospital where I gave birth sent my debt to collections? I’ve been making payments to the hospital and have a 24-month plan. I’ve already paid for 10 consecutive months. Can they still send it to collections?"

This is a very common and frustrating situation. In most cases, if you have a payment agreement in writing with the hospital and you're making payments as agreed, your debt should not be sent to collections.

However, mistakes happen. Sometimes hospitals misapply payments, lose track of accounts, or accidentally transfer debts to collections even if you’re paying.

What you should do:

- Contact the hospital billing department immediately and ask for a detailed account statement.

- Request confirmation in writing that your payment plan is active and in good standing.

- Call Central Financial Control directly to verify if they actually have your debt or if it was an error.

- Keep copies of all your payment receipts and any communication.

If it turns out your debt was mistakenly sent to collections, you can dispute it and have it removed from your credit report.

How Does 800-346-0775 Affect Your Credit Score?

This is where it gets complicated. Here's what you need to know:

If It's Already on Your Credit Report:

- The damage is already done

- Collection accounts can lower your score by 50-100 points

- It stays on your credit report for 7 years from the original delinquency date

If It's Not on Your Credit Report Yet:

- The original creditor may have already reported it

- Some collection agencies report to credit bureaus, others don't

- Making a payment can sometimes restart the credit reporting clock

Credit Score Impact Timeline:

- 30-60 days late: Minor impact (10-20 points)

- 90+ days late: Moderate impact (30-50 points)

- Charged off/Collections: Major impact (50-100 points)

Your Rights When 800-346-0775 Calls

The Fair Debt Collection Practices Act (FDCPA) gives you powerful protections:

What They CANNOT Do:

- Call before 8 AM or after 9 PM (your local time)

- Contact you at work after you've told them not to

- Use abusive, threatening, or harassing language

- Discuss your debt with family, friends, or coworkers

- Continue calling after you request they stop in writing

- Threaten legal action they don't intend to take

- Misrepresent the amount you owe

What They MUST Do:

- Identify themselves as debt collectors

- Provide the name of the original creditor

- Tell you the amount of the debt

- Inform you of your right to dispute the debt

- Send written verification if you request it

- Stop collection efforts if you dispute the debt (until they provide proof)

Example of FDCPA Violation:

"They called me at work even after I told them not to. They also called my sister and told her about my debt. I documented everything and filed a complaint with the CFPB. They ended up settling for less than half of what they claimed I owed." - Mike, Texas

What to Do When 800-346-0775 Calls: Step-by-Step Guide

Step 1: Don't Panic (But Don't Ignore)

- Stay calm and take notes

- Don't admit the debt is yours immediately

- Don't make promises you can't keep

Step 2: Gather Information

Ask for:

- The collector's name and company

- The original creditor's name

- The amount of the debt

- The date of the last payment

- Their mailing address

Step 3: Request Debt Validation (Within 30 Days)

This is crucial. Send a debt validation letter requesting:

- Proof the debt is yours

- Verification of the amount

- Proof they have the right to collect it

- Copy of the original signed agreement

Step 4: Check Your Credit Report

- Pull your free annual credit report

- Look for the original creditor and any collection accounts

- Document any inaccuracies

Step 5: Decide Your Strategy

Based on your situation, you can:

- Dispute the debt if it's not yours

- Negotiate a settlement

- Set up a payment plan

- Pay in full if you can afford it

5 Ways to Stop 800-346-0775 from Calling

1. Send a Cease and Desist Letter

Write a letter (send certified mail) requesting they stop contacting you. They must legally stop calling, but the debt doesn't go away.

2. Negotiate a Settlement

Most debt collectors will accept 30-50% of the original debt. Get any agreement in writing before paying.

3. Set Up a Payment Plan

If you can't pay in full, ask about monthly payment arrangements. Make sure you can actually afford the payments.

4. Pay in Full

If you can afford it and the debt is valid, paying in full stops the calls immediately.

5. File for Bankruptcy

As a last resort, bankruptcy can eliminate many types of debt, but it has serious long-term consequences.

Sample Letters and Scripts

Debt Validation Letter Template:

[Your Name]

[Your Address]

[Date]

Central Financial Control

[Their Address]

Re: Account #[if you have it]

Dear Sir/Madam,

I am requesting validation of the above-referenced debt. Under the Fair Debt Collection Practices Act, I have the right to request verification of this debt.

Please provide:

1. Verification of the debt amount

2. Name of the original creditor

3. Proof that you are licensed to collect debts in my state

4. Proof that the statute of limitations has not expired

I dispute this debt and request that you cease all collection activities until you provide proper validation.

Sincerely,

[Your signature]

[Your printed name]

Phone Script for When They Call:

"I need to verify this debt. Please send me written documentation showing that this debt is mine and that you have the right to collect it. I'm not making any payments until I receive proper verification."

How to Remove 800-346-0775 from Your Credit Report

If the Debt is Accurate:

- Pay for Delete: Negotiate with Central Financial Control to remove it from your credit report in exchange for payment

- Wait It Out: Collection accounts automatically fall off after 7 years

- Dispute After Payment: Sometimes paid collections can be disputed as "not mine"

If the Debt is Inaccurate:

- Dispute with Credit Bureaus: File disputes with Experian, Equifax, and TransUnion

- Send Dispute Letter to Central Financial Control: Request they remove inaccurate information

- Use a Credit Repair Service: They can help navigate the dispute process

Success Story:

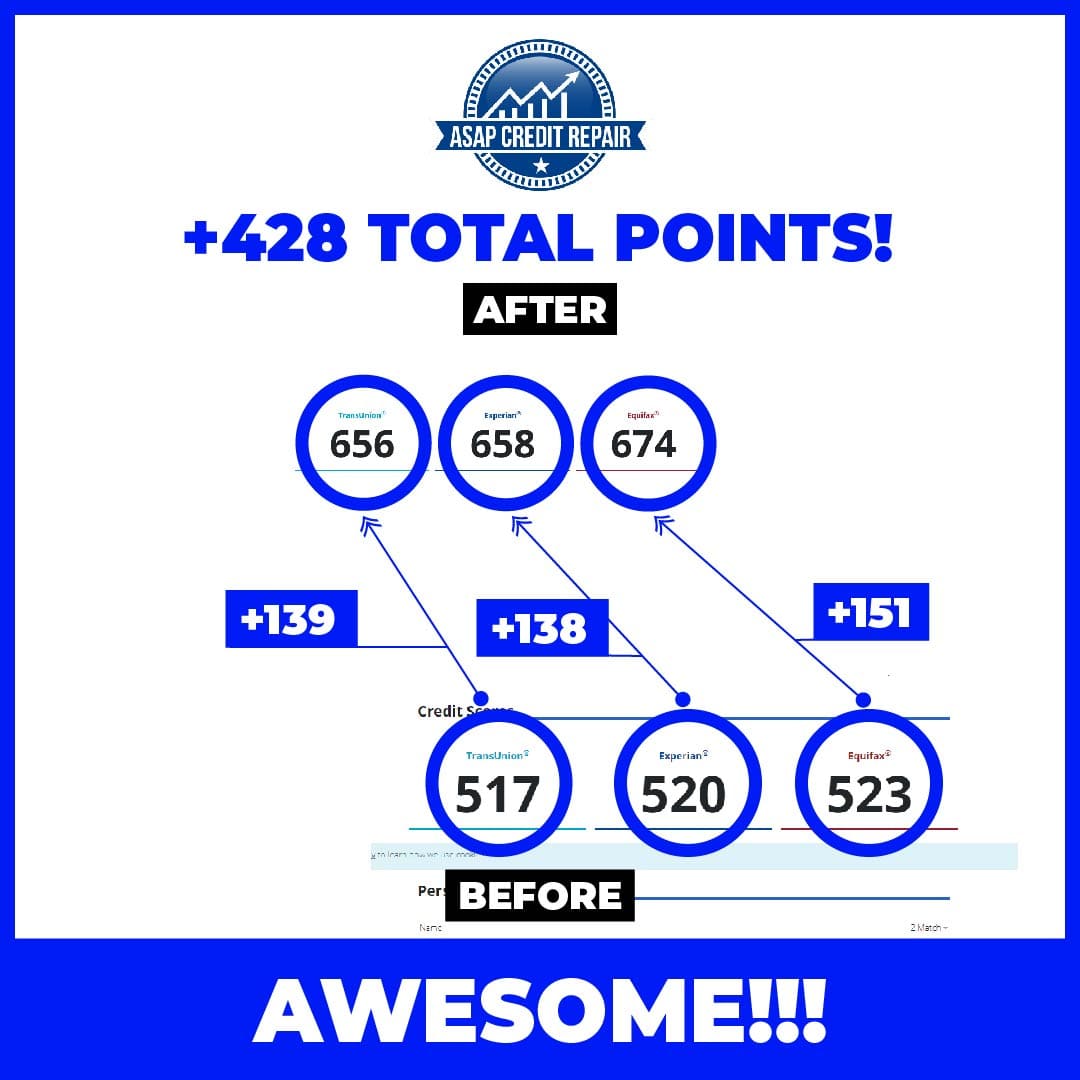

"I disputed a collection from Central Financial Control with the help of ASAP Credit Repair, because the amount was wrong. It took 3 months, but they removed it from my credit report completely. My credit score went up 130+ points!" - Jennifer, Florida

Common Mistakes to Avoid

1. Ignoring the Calls

This makes everything worse. The debt won't disappear, and you lose leverage.

2. Admitting the Debt is Yours Immediately

Always verify first. Sometimes they have the wrong person or wrong amount.

3. Making Partial Payments Without an Agreement

This can restart the statute of limitations and hurt your negotiating position.

4. Giving Banking Information Over the Phone

Never give out account numbers or routing numbers during the first call.

5. Not Getting Agreements in Writing

Verbal agreements are worthless. Always get settlement agreements in writing.

State-Specific Information

Statute of Limitations by State:

- California: 4 years

- Texas: 4 years

- Florida: 5 years

- New York: 6 years

- Illinois: 5 years

Note: This varies by state and type of debt. Check your state's specific laws.

States Where Central Financial Control is Licensed:

Central Financial Control is licensed to collect debts in all 50 states, but they must follow each state's specific rules.

Frequently Asked Questions about 800-346-0775(FAQ)

Q: Is 800-346-0775 a scam?

A: No, it's a legitimate debt collection agency, but scammers sometimes spoof this number. Always verify before giving any information.

Q: Can 800-346-0775 hurt my credit score?

A: If Central Financial Control reports to credit bureaus, yes. However, the original creditor may have already damaged your credit before the debt was sold.

Q: What if I don't recognize the debt?

A: Request debt validation within 30 days. They must prove the debt is yours and that they have the right to collect it.

Q: Can I negotiate with 800-346-0775?

A: Yes, most collection agencies will accept 30-50% of the original debt to settle the account.

Q: How long can 800-346-0775 try to collect?

A: It depends on your state's statute of limitations, typically 3-6 years from the last payment or activity.

Q: What if I can't afford to pay?

A: You can request a payment plan, negotiate a settlement, or seek help from a credit counselor.

Q: Can 800-346-0775 garnish my wages?

A: Not without a court judgment. They would need to sue you first and win.

Q: Should I pay old debts in collections?

A: It depends on your situation. Consider the statute of limitations, your credit goals, and whether you can negotiate a pay-for-delete agreement.

When to Get Professional Help

Consider hiring a consumer law attorney if:

- Central Financial Control violates the FDCPA

- You're being sued by a creditor

- The debt is very large (over $10,000)

- You're considering bankruptcy

Consider credit counseling if:

- You have multiple debts in collections

- You're struggling to create a budget

- You need help negotiating with creditors

Alternative Ways to Handle Debt

1. Debt Consolidation

Combine multiple debts into one payment with a potentially lower interest rate.

2. Debt Management Plan

Work with a credit counseling agency to create a structured payment plan.

3. Debt Settlement

Either do it yourself or hire a company to negotiate with creditors.

4. Bankruptcy

Chapter 7 or Chapter 13 can eliminate or restructure debts.

Resources and Support

Free Resources:

- National Foundation for Credit Counseling: 1-800-388-2227

- Consumer Financial Protection Bureau: consumerfinance.gov

- Federal Trade Commission: consumer.ftc.gov

Legal Help:

- National Association of Consumer Advocates: consumeradvocates.org

- Legal Aid Society: (search for your local office)

Credit Monitoring:

- Annual Credit Report: annualcreditreport.com

- ASAP Credit Repair: asapcreditrepairusa.com (free credit analysis)

Final Thoughts

Dealing with 800-346-0775 and Central Financial Control doesn't have to be overwhelming. Remember:

- You have rights under the FDCPA

- They want to collect more than they want to sue you

- Most debts can be negotiated for less than the full amount

- Documentation is key - keep records of everything

- Don't ignore it - the problem won't go away

The most important thing is to take action. Whether that's validating the debt, negotiating a settlement, or simply getting the calls to stop, you have options. Don't let debt collectors control your life - take back the power by knowing your rights and using them.

Related Articles:

Who Is 866-258-1104? Parallon Medical Collections Explained (And What to Do)

Elan Financial Services on Credit Report? Complete Identification Guide 2025

SynCom Collections: How to Deal with Synergetic Communication Debt Collectors

This guide is for educational purposes only and is not legal advice. If you need specific guidance, consult with a professional in your state.