Can debt collectors take money from your bank account? Yes, but only after they take legal action and obtain a court judgment.

Without a judgment, a debt collector cannot withdraw money directly from your account. Once a judgment is entered, the collector can request a bank levy, which allows funds to be frozen or removed under court order.

Under the Fair Debt Collection Practices Act, collectors are restricted in how they pursue debts, but the law does not prevent them from using the court system to enforce payment. In cases we handle, most bank account levies happen after a lawsuit is ignored or unresolved. Many people are unaware that a judgment was entered until their account is frozen.

The process is not automatic. It requires a lawsuit, a judgment, and a court-approved action against the account. This article explains when collectors can access your bank account, what steps lead to that point, and how to protect your funds.

Debt & Bank Accounts · Bank Levy · Wage Garnishment · FDCPA Rights · How to Stop Account Garnishment · Exempt Income Protection

Updated April 2026 · Sources: Bankrate bank levy guide (March 2025), Nolo frozen bank accounts legal guide, FTC consumer debt collection rights, FDCPA 15 U.S.C. § 1692, Federal Reserve Board bank levy regulations

- Private debt collectors cannot take money from your bank account without a court order. They must sue you and win first.

- A bank levy freezes your account. You will likely find out when your debit card stops working - not from a warning letter.

- Federal law protects Social Security, SSI, veterans benefits, and disability income from private debt collectors even after a levy.

- Ignoring a lawsuit summons is the most common way accounts get frozen. A default judgment requires no hearing, no proof, and no court appearance from you.

- You have 10 to 30 days after a levy to file a claim of exemption and recover protected funds. Act immediately.

- Your bank can take money without a court order if you owe debt to the same bank that holds your account. This is called a right of setoff.

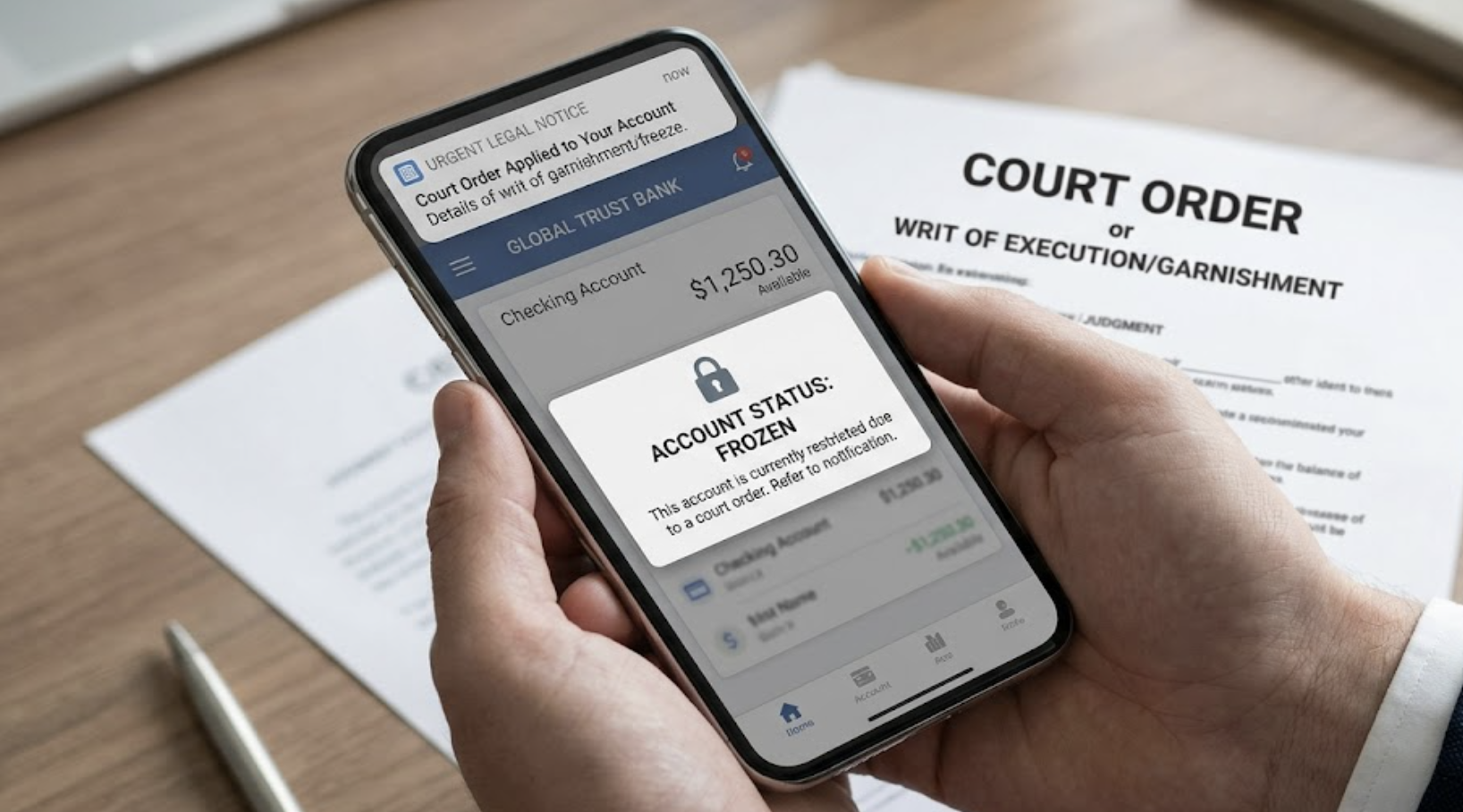

Most people who find out their bank account is frozen discover it the same way. They try to pay for groceries, gas, or rent, and the card declines. They call the bank. The bank says their funds are frozen under a court order. They have no idea how this happened.

Here is how it actually works, step by step, so you know exactly what a collector can and cannot do.

Can a Debt Collector Withdraw Money from My Bank Account?

The process always starts with a lawsuit. There are no shortcuts for private collectors. The Fair Debt Collection Practices Act (FDCPA) requires them to give you notice of the suit and a chance to respond. As the FTC's debt collection guide explains, you have the right to dispute the debt in writing within 30 days of first contact, request proof of the debt, and sue any collector who violates your FDCPA rights for statutory damages. If you do not respond, the court enters a default judgment against you, which is exactly the same as losing the case. Most frozen bank accounts happen because of default judgments. The debtor got served, did not respond thinking it would go away, and woke up one day with no access to their money.

As Bankrate's bank levy guide explains, a bank levy is a legal action that allows a creditor to take money directly from your bank account to satisfy an unpaid debt. The bank is required to freeze the account and surrender funds once it receives the court's levy order. This is not a payment you agreed to. It is a legal command the bank must follow.

That story repeats itself constantly in debt forums. The judgment is real, even if you never received the papers. Creditors are allowed to serve you at your last known address. If you moved and did not update your address with the court or the creditor, service may still be considered valid. The judgment stands. The levy follows.

One situation many people miss: if you bank at the same institution where you have a loan or credit card, the bank may take your money without any court order at all. This is called a right of setoff, and it is buried in the fine print of most bank account agreements. If your Chase credit card goes delinquent and you also have a Chase checking account, Chase may offset the balance directly from your checking. No lawsuit required.

What Happens Right Before Your Account Gets Frozen?

The debt collection process follows a predictable path. Most collectors spend 90 to 180 days on phone calls and letters before escalating to a lawsuit. When the calls stop, many people assume the debt went away. It did not. It went to a law firm.

If you are dealing with repeated collector contact and want to understand the rules around those calls, our guide on what to do when debt collectors keep calling after you told them to stop covers your FDCPA rights to demand collectors cease contact, what that demand must include to be legally binding, and what collectors can still legally do even after a cease-and-desist letter - including filing a lawsuit.

One thing many people do not know: a judgment does not expire quickly. In most states, a creditor can collect on a judgment for 10 to 20 years. They can renew it. That means a $500 credit card debt from 2018 can result in a frozen bank account in 2026. The original debt is the same debt. The judgment just waited.

If you are not sure whether a debt collector can even sue you for the amount they are claiming, our breakdown of whether a debt collector can sue you for $500 covers the real-world threshold where lawsuits become financially viable for collectors, how small claims courts change that math, and what your defenses are when a lawsuit is filed over a small balance.

What's the Worst a Debt Collector Can Do?

| Action | Requires Court Judgment? | Impact | Protected Income? |

|---|---|---|---|

| Bank Levy | Yes (private) | Entire account frozen; funds released to creditor after ~21 days | Social Security, SSI, veterans benefits protected |

| Wage Garnishment | Yes (private) | Up to 25% of disposable income taken per paycheck | Federal minimum wage protects some; varies by state |

| Property Lien | Yes | Cannot sell or refi home until debt paid; affects title | Homestead exemptions vary by state |

| Writ of Execution | Yes | Sheriff can seize personal property and sell at auction | Household goods, tools of trade often exempt |

| IRS Tax Levy | No (30-day notice required) | Bank holds funds 21 days before release to IRS | IRS can access Social Security up to 15% |

| Child Support / Alimony | No (court order via family court) | Automatic income withholding; can also levy bank accounts | Very limited exemptions; enforcement is aggressive |

| Bank Right of Setoff | No | Same bank takes from your deposit to cover their loan | Very limited; depends on state and account agreement |

Wage garnishment is often more damaging over time than a bank levy. A levy hits once per account per order. Wage garnishment happens every paycheck, every payday, until the full debt plus interest and court fees is paid. On a $3,000 judgment, at 25% of a $2,000 monthly take-home, that is $500 per month for six months, assuming no interest is still accruing on the judgment balance.

That four-month garnishment cost them nearly $2,000. The original balance that led to the judgment was $1,800. Court costs and judgment interest pushed it past $2,000 total. They paid more than they originally owed because they did not respond to the lawsuit when it was filed.

Many people also do not realize that a debt can land in collections without them getting a formal advance notice. Our guide on whether a company can send you to collections without notice explains the FDCPA rules around notification requirements, what constitutes proper notice, and what your rights are when a debt appears in collections without warning - including on your credit report.

What Income Is Protected from a Bank Levy?

The automatic protection only covers two months of deposits. If you have more than two months of Social Security sitting in one account, the amount above that threshold is not automatically protected. You have to file a claim of exemption with the court to get those extra funds excluded from the levy. That is why many attorneys advise people who receive exempt income to keep only small rolling balances in their checking accounts and transfer excess to a savings account.

State laws add additional protections in some states. Pennsylvania requires collectors to leave at least $300 in a levied account regardless of the source. Several other states protect minimum wage amounts or specified household income thresholds. The FTC's consumer debt rights resources confirm that certain types of income are legally protected from private debt collectors even after a judgment. As Nolo's bank levy legal guide notes, federal law protects Social Security, veterans benefits, and similar funds from private creditor bank levies, but government agencies like the IRS can access Social Security up to 15% for tax debts.

One protection most people overlook: if your only income is Social Security or another fully exempt source, a private debt collector has no legal right to freeze your account at all. A judgment creditor can obtain a levy order, but if all funds in the account are protected, they cannot actually take anything. You still have to file the exemption claim paperwork to prove this, but the funds are shielded.

How Can I Stop a Debt Collector from Garnishing My Bank Account?

- Respond to every lawsuit summons, every time, before the deadline. Most state courts give you 14 to 30 days from the date you were served to file an answer. Even a simple denial, filed without an attorney, prevents a default judgment. A default judgment is the fastest and most common path to a frozen bank account. You do not have to win the case to prevent immediate harm. You just have to show up.

- File a claim of exemption immediately if your account is already frozen. You typically have 10 to 30 days from when the levy is served to file this claim, depending on your state. Contact the court clerk the same day you find out your account is frozen. Ask for the claim of exemption form. List every protected source of income in your account. Submit it to the court. This form triggers a review of which funds are legally off-limits.

- Call the creditor's attorney and propose a payment plan before the levy releases funds. The 21-day waiting period before the bank releases funds to the creditor is a negotiation window. Call the attorney listed on the garnishment paperwork. Offer to set up a payment plan. If they agree, they can lift the levy. Get every agreement in writing before anything is signed or paid.

- Challenge the levy if proper procedures were not followed. You have the right to challenge a levy if you were not properly served with the original lawsuit, if the debt is past your state's statute of limitations, if the amount claimed is wrong, or if the debt is not yours. Each of these is a legal defense. A consumer law attorney can file a motion to vacate the judgment in some cases, which would dissolve the levy entirely.

- Move exempt income to a dedicated single-purpose account going forward. If you receive Social Security, SSI, veterans benefits, or disability income, consider a separate account that receives only those deposits. This makes it much easier for your bank to identify and protect those funds automatically in the event of a future levy. A mixed account, where protected deposits sit alongside wages, is harder to fully exempt and creates gray areas that courts resolve differently by state.

One thing to understand about the bankruptcy option: filing for Chapter 7 or Chapter 13 bankruptcy triggers an automatic stay under 11 U.S.C. Section 362. That stay immediately stops all collection activity, including wage garnishment, bank levies, and creditor calls. It does not permanently discharge the debt in all cases, and bankruptcy has its own long-term credit consequences. But if you are facing multiple levies or garnishments at once, it is a legal tool worth understanding. A bankruptcy attorney can tell you within one consultation whether it makes financial sense for your situation.

A Judgment on Your Credit Report Compounds the Damage

A court judgment that leads to a bank levy also appears on your Experian, TransUnion, and Equifax reports. It can stay there for 7 years. A free 3-bureau audit shows every judgment entry, whether it is still being reported accurately, and whether any entries are disputable under the FCRA.

Get My Free Credit Audit → Secure · 2 minutes · No credit card requiredFrequently Asked Questions

Can debt take money from my bank account?

Not directly. A private debt collector must first sue you in civil court, win a judgment, and then get the court to issue a bank levy order. Once the levy hits your bank, the bank freezes your funds. After a state-mandated waiting period (usually 21 days), the money is released to the creditor. Government agencies like the IRS can skip the lawsuit step but must still give advance written notice. If you bank at the same institution where you have a loan in default, that bank may also take funds directly under a right of setoff without a court order.

Can a debt collector withdraw money from my bank account?

No. A private debt collector cannot withdraw money from your bank account without a court order. Threatening to do so without a judgment is likely a violation of the Fair Debt Collection Practices Act. You can report such a threat to the FTC and can sue the collector for up to $1,000 in statutory damages plus attorney fees. To legally access your account, the collector must sue you, win or obtain a default judgment, then get a writ of garnishment from the court that is served on your bank.

What's the worst a debt collector can do?

After winning a court judgment, the worst a private collector can legally do is: freeze your entire bank account through a levy; garnish up to 25% of your paycheck every pay period until the debt is paid; place a lien on your home that prevents sale or refinancing; or seize personal property through a writ of execution. All four require a judgment first. The judgment itself also appears on your credit report for 7 years and remains collectible for 10 to 20 years depending on your state.

How can I stop a debt collector from garnishing my bank account?

The best way to stop a bank levy is to respond to the lawsuit before a default judgment is entered. If a levy is already in place, file a claim of exemption with the court within your state's deadline (typically 10 to 30 days) to protect any exempt income like Social Security or veterans benefits. You can also negotiate a payment plan with the creditor's attorney during the 21-day bank hold period before funds are transferred. If the debt is past your state's statute of limitations or you were not properly served, those are legal defenses you can raise in court.

What income is safe from debt collectors even after a levy?

Federal law protects Social Security, Supplemental Security Income, veterans benefits, federal student aid, railroad retirement benefits, and federal employee retirement income from private debt collector bank levies. If these funds are direct-deposited into your account, federal law requires your bank to automatically protect up to two months of those deposits. You may need to file a claim of exemption to protect amounts above two months or if your account has a mix of protected and non-protected income. State laws may protect additional funds beyond these federal minimums.

Will I get a warning before my bank account is frozen?

Probably not. Most people find out their account is frozen when their debit card declines. Your bank must notify you that your account has been frozen, but that notice typically comes after the freeze is already in place, not before. The only advance warnings are the court summons (if you received and read it) and any prior collection letters. If the creditor used an old address to serve the lawsuit and you never appeared in court, you may have no idea a judgment exists until your account is frozen.

-

Does Conn's Collections Sue for a $300 Debt? If you have an outstanding Conn's balance now owned by Jefferson Capital, this covers the real lawsuit likelihood by debt amount, how Texas justice of the peace courts make small-debt suits cheaper, and what your rights are if Jefferson Capital contacts you.

-

Can Credit Card Companies Sue If Social Security Is Your Only Income? If your only income is Social Security or disability, this answers whether credit card companies can still sue you, whether your monthly benefit is truly protected from a bank levy, and what collectors can and cannot do when your only assets are federally exempt.

-

Wage Garnishment in Phoenix, AZ: What You Need to Know Arizona-specific breakdown of how wage garnishment works after a judgment, the state's garnishment limits, how creditors find your employer, and the timeline from judgment to first garnished paycheck.

People Also Ask

Can a debt collector take money from your bank account without permission?

No. A collector must first obtain a court judgment before accessing your bank account.

Can creditors freeze your bank account?

Yes. After a judgment, a creditor can request a bank levy, which may freeze funds in your account.

What happens after a debt judgment is entered?

The creditor can pursue collection methods allowed by law, including bank levies, wage garnishment, or liens.

How can you stop a bank account levy?

You may be able to challenge the levy, claim exemptions, or resolve the debt before funds are removed.

Closing

Debt collectors cannot take money from your bank account without going through the court process. The key event is the judgment. Once it is entered, your account may be at risk if further action is taken.

Most account levies occur because the legal process was not addressed early. Responding to a lawsuit, verifying the debt, or resolving the balance can prevent the situation from reaching that stage.

The risk is not the collection call. It is what happens after a judgment is entered.