You got a card in the mail from your employer. It looks like a debit card. It says "FSA" on it. And you have no idea what to do with it.

That is more common than you think.

An FSA card is a special payment card your employer gives you. You use it to pay for medical costs. The money on it comes straight from your paycheck before taxes are taken out. That means the government never touches that money before you spend it on health care.

Think of it this way. You earn $100. Normally, taxes come out first, and you spend what is left. With an FSA card, you set aside money before taxes hit. You pay for your doctor visit, your prescriptions, or your glasses all with pre-tax dollars.

That is real savings most people leave on the table.

I run a credit repair company. Medical bills are one of the biggest financial stressors I see with clients. One of the first things I ask is: "Do you have an FSA?" One client came to us last year. She had over $800 sitting in her FSA account. She never used it. It expired. Her employer kept it. No one had ever told her how it worked.

That story is not rare. A thread in r/personalfinance (reddit.com/r/personalfinance) is full of people asking the same questions you probably have right now. And the IRS makes clear: FSA money you do not spend by your plan year-end is gone (irs.gov/publications/p969). It goes back to your employer.

This guide will walk you through everything in plain English so that it never happens to you.

What Is an FSA Card?

An FSA card is a debit card tied to your Flexible Spending Account. It looks and feels like any card in your wallet. But it has one job: pay for approved health expenses using the pre-tax money in your FSA.

Here is the simple version. You sign up for an FSA at work. You pick how much money to set aside for the year. That money gets loaded onto your FSA card. When you go to the doctor or the pharmacy, you swipe it. Done.

You never had to touch that money after taxes. That is the whole point.

The FSA card only works for health-related items that the IRS approves. Try to buy groceries with it, and it will decline. Try to buy cold medicine, and it goes right through.

What Is a Flexible Spending Account (FSA)?

A Flexible Spending Account or FSA is a benefit your employer offers. Not all employers offer one, but many do.

Here is how it works from the start. During open enrollment, your employer asks if you want to put money into an FSA. You pick an amount for the whole year. That amount gets split across your paychecks. A little comes out each pay period before taxes.

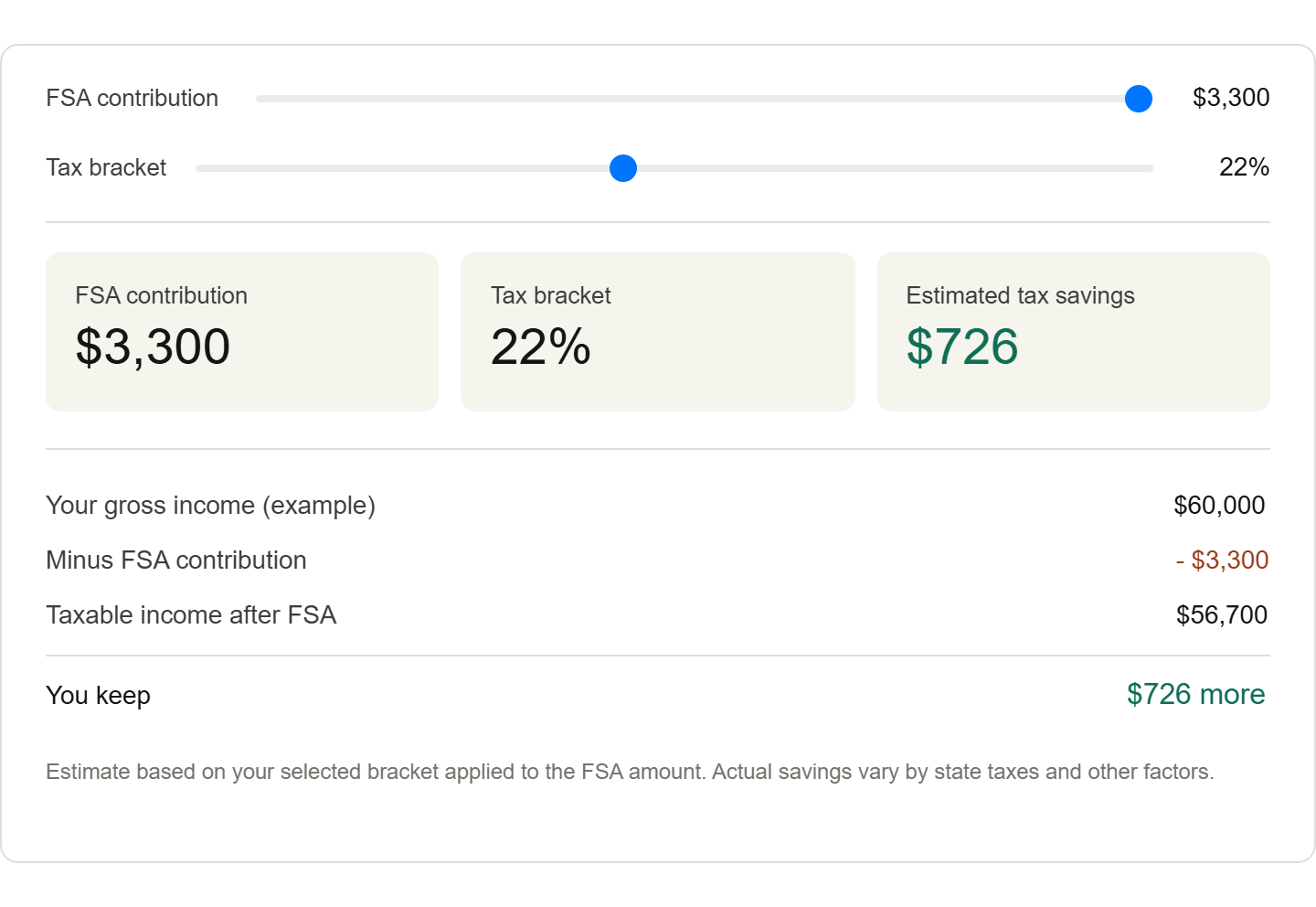

The IRS caps how much you can put in. For 2025, the limit is $3,300 (IRS Revenue Procedure 2024-40). That is up from $3,200 in 2024. Your employer may allow less than that. Check your benefits documents.

There are three types of FSAs. Most people get the first one:

Healthcare FSA — pays for medical, dental, vision, and prescription costs. This is the most common type.

Dependent Care FSA — pays for childcare or adult daycare so you can work. The limit here is $5,000 per household.

Limited Purpose FSA — covers only dental and vision. Usually used alongside an HSA.

When someone asks what an FSA card is, they almost always mean the healthcare FSA card.

How Do FSA Cards Work?

Using your FSA card is simple. Swipe it like a regular debit card. The money comes out of your FSA balance right away.

But here is what happens behind the scenes. Every time you swipe, the card checks if the purchase is on the IRS-approved list. If it is, the transaction goes through. If it is not, the card says no.

Here is the full process from start to finish:

You pick your annual amount during open enrollment.

Your employer takes a small amount from each paycheck throughout the year.

Your full elected amount is loaded onto your FSA card on day one of your plan year.

You swipe the FSA card at the pharmacy, doctor's office, or eligible retailer.

The money leaves your balance right away.

Sometimes, your FSA administrator asks for a receipt to confirm the purchase was eligible.

If you forgot to use the card and paid out of pocket, you can file a claim to get reimbursed.

One big perk: your full balance is available on January 1. You do not have to wait for your paychecks to build it up first.

So if you elected $1,200 for the year, all $1,200 is ready to use on day one. That is something an HSA cannot do.

What Is the Difference Between an FSA Card and an HSA Card?

Both cards help you pay for health costs with tax-free money. A lot of people mix them up. Here is the easy breakdown.

An FSA belongs to your employer. If you leave your job, you usually lose what is left. An HSA belongs to you. It goes with you when you leave.

An FSA gives you all your money on day one. An HSA only has what you have already put in.

An FSA has a use-it-or-lose-it rule. Leftover money at year-end goes back to your employer. An HSA rolls over forever with no deadline.

An HSA requires a High Deductible Health Plan. An FSA does not. But you need a job with benefits to get an FSA. Self-employed people cannot open one.

For 2025, the HSA limit is $4,300 for one person and $8,550 for a family. The FSA card limit is $3,300.

If you already have an HSA, you cannot open a regular healthcare FSA at the same time. You can pair an HSA with a Limited Purpose FSA for dental and vision only.

So now you know the basics. An FSA card gives you money upfront, but has a deadline. HSA builds over time, but it is yours forever.

Is Your FSA Tax-Free?

Yes. 100%.

The money you put into an FSA never gets taxed. It skips federal income tax, Social Security tax, and Medicare tax. When you spend it on eligible items, that spending is tax-free too.

In our office last year, we went over the finances of three separate clients who had never enrolled in an FSA. All three had out-of-pocket medical costs every year. All three were paying taxes on money they did not have to. That is money they could have kept.

One rule to know: do not use your FSA card for non-eligible purchases. If you do, that amount becomes taxable income. You may also face a penalty. Always keep your receipts. The IRS can ask for proof.

What Can You Buy with an FSA Card?

More than most people expect.

The IRS sets the list of eligible items. It is a long list. Here are the most common things you can buy with your FSA card:

Doctor visit copays

Prescription drugs

Over-the-counter medications — no prescription needed since the 2020 CARES Act

Dental cleanings, fillings, and braces

Eye exams, prescription glasses, and contact lenses

LASIK eye surgery

Physical therapy

Mental health counseling

Hearing aids and batteries

Blood pressure monitors and glucose meters

Menstrual care products

Sunscreen (SPF 15 or higher, broad-spectrum)

Pregnancy tests

First aid kits and supplies

Things that do NOT qualify: gym memberships, general vitamins, cosmetics, teeth whitening, and non-prescription sunglasses.

Not sure if something qualifies? The FSA Store (fsastore.com) has a free search tool. Type in any item and it tells you right away.

What Happens to Unused FSA Card Funds?

Here is the part most people do not know until it is too late.

If you do not spend your FSA balance by the end of your plan year, you lose it. It does not roll over into a savings account. It does not come back to you as cash. Your employer keeps it. That is the use-it-or-lose-it rule.

Your employer can offer one of two options to soften this rule — but not both at the same time:

A 2.5-month grace period. You get extra time until mid-March to spend what is left.

A rollover of up to $660 into next year's plan (the 2025 limit, per fsafeds.gov).

Not every employer does either one. Ask HR before you assume.

If you leave your job in the middle of the year, your FSA funds are usually gone unless you keep your health coverage through COBRA.

The fix is simple. Set a phone reminder in October. Check your FSA card balance. Use what is left before the deadline. Book that dentist visit. Order a backup pair of glasses. Stock up on FSA-eligible items you already buy.

Can You Use a FSA Card Online?

Yes. Shopping online with your FSA card works just like using a regular debit card.

Major retailers accept it. Amazon has a whole FSA/HSA section where every listed item is eligible. Walmart accepts FSA cards for health items, too. The FSA Store (fsastore.com) sells only eligible products, so you never have to guess.

At checkout, enter your FSA card number like you would any payment card. Always save the receipt or order confirmation. Your FSA administrator may ask for proof that the purchase was eligible.

Does a FSA Card Affect Your Credit Score?

No. Not at all.

An FSA card is a debit card. It does not show up on your credit report. It does not affect your credit score. You are spending money you already set aside. No lender is involved. No debt is created. Nothing gets reported to the credit bureaus.

That said, unpaid medical bills are a different story. If a medical bill goes unpaid and gets sent to collections, it can hurt your credit. Using your FSA card to pay eligible costs on time helps you avoid that problem entirely.

Medical Bills Can Turn Into Credit Problems Fast

An FSA card can help you pay eligible health costs before they become unpaid bills. But if medical debt is already affecting your credit, ASAP Credit Repair can help you understand what is hurting your score and what steps may help.

Check Your Credit Report NowReview your report today and find out what may be holding your credit back.

How to Get the Most Out of Your FSA Card

The number one mistake people make with an FSA card: putting in more money than they actually spend.

Because of the use-it-or-lose-it rule, guessing too high means losing money at year-end. The goal is to contribute just enough to cover your real health costs for the year.

Before you enroll, think through what you actually spend on health care each year. Ask yourself:

How often do I go to the doctor? What are my copays?

Do I take regular prescriptions? What do those cost per month?

Do I have any dental or vision appointments coming up?

What over-the-counter items do I buy every year anyway?

Add those up. That is your starting number.

Set a calendar reminder for three months before your plan year ends. Check your FSA card balance. If money is left, use it. Book a checkup. Buy a new pair of glasses. Grab a year's worth of contact solution.

The IRS publishes Publication 969 if you want the full rulebook. It covers FSA cards, limits, and every eligible expense. Reading it once can save you hundreds of dollars.

Your FSA card is one of the easiest ways to save money on health costs. The hard part is just knowing it exists, and now you do.