A good credit score in 2026 is 670 or higher on the FICO scale and 661 or higher on the VantageScore scale. But "good" is not the same as "best." The gap between a good score and a great score can cost you tens of thousands of dollars in interest over a lifetime of borrowing.

Running a credit repair company means we field this question every single week. This is one of my favorite topics to explain, because most people are shocked when they find out what a single-tier jump actually saves them. One of the most common cases we see: a client with a 701 score who believes they are in great shape. Technically, they are in the "good" range. But they are not in the range that gets the best mortgage rate. Moving from 701 to 741 can save over $60,000 on a 30-year mortgage. That is not a rounding error.

Real confusion shows up in online forums, too. A recent thread on r/personalfinance had a user with a 703 FICO score and a 750 VantageScore asking which one was real and which one lenders actually use. The top reply spelled it out clearly: mortgage lenders use FICO, not VantageScore. Most free apps show VantageScore. The two numbers are not interchangeable. (Source: Blind community thread referencing FICO vs. VantageScore)

The data confirms this confusion is widespread. According to Experian, the average U.S. FICO score was 713 as of September 2025, a 2-point drop from 2024. (Source: Experian State of Credit 2025) That marked the first annual decline in over a decade, driven by rising credit card balances and the return of student loan delinquency reporting. Most Americans sit in the "good" range. But most Americans are also not getting the best available rates.

What Is a Good Credit Score on the FICO Scale?

FICO scores range from 300 to 850. FICO breaks that range into five tiers:

800 to 850: Exceptional

740 to 799: Very good

670 to 739: Good

580 to 669: Fair

300 to 579: Poor

A score of 670 qualifies as good. Most lenders approve borrowers at this level for standard loan products. But approval is not the same as the best terms. Lenders reserve the lowest interest rates for borrowers in the "very good" and "exceptional" tiers, typically 740 and above.

The practical threshold most lenders use is 760. At 760, most conventional loan programs offer their best available rates. Pushing above 760 produces diminishing returns. Mortgage experts at Churchill Mortgage confirm that for conventional loans, 780 is the point where rates flatten out. Scores above 780 rarely produce better pricing than 780 itself. (Source: Yahoo Finance / Churchill Mortgage, 2026)

FICO also produces industry-specific scores for auto and mortgage lending. Those scores range from 250 to 900. The "good" tier in those models still starts at 670. Lenders in those industries may pull a different version of your FICO score than the one you see on a monitoring app.

What Is a Good Credit Score on the VantageScore Scale?

VantageScore uses the same 300 to 850 range as FICO, but draws its tier lines differently. VantageScore 3.0 and 4.0 define four categories:

781 to 850: Superprime (Excellent)

661 to 780: Prime (Good)

601 to 660: Near Prime (Fair)

300 to 600: Subprime (Poor)

A score of 661 qualifies as good under VantageScore. That is nine points lower than the FICO "good" floor of 670. This matters because many free apps, Credit Karma, Credit Sesame, and most bank credit score tools show your VantageScore, not your FICO score.

VantageScore's "good" band is also much wider: it runs from 661 all the way to 780. Under FICO, a 750 is "very good." Under VantageScore, a 750 is still just "good." A consumer labeled "good" under VantageScore could be labeled "very good" under FICO at the same score number.

One important 2026 update: VantageScore 4.0 can generate a score with as little as one month of credit history. FICO typically requires six months. This means roughly 37 million more Americans are scoreable under VantageScore than under FICO. (Source: ScoreNerds Credit Score Ranges 2026)

If you are applying for a mortgage or major loan, ask your lender which score model and version they pull. Do not assume your VantageScore matches your mortgage FICO.

By now, you know where the tiers sit and why the two models differ. The next section answers the more important question: what does each tier actually cost you in real money?

What the Average U.S. Credit Score Looks Like in 2026

The average U.S. FICO score was 713 as of late 2025, according to Experian data. The average VantageScore 3.0 sits at 700 for the same period. Both place the typical American consumer in the "good" range, but just barely above the lower threshold.

The generational breakdown tells a more useful story:

Gen Z (ages 18 to 28): 678 average FICO

Millennials (ages 29 to 44): 689 average FICO

Gen X (ages 45 to 60): 709 average FICO

Baby Boomers (ages 61 to 79): 747 average FICO

Silent Generation (ages 80 and up): 760 average FICO

(Source: Experian State of Credit, Q4 2025)

Gen Z saw the sharpest single-year decline of any generation, dropping 3 points to 678. The main driver: 14.4% of consumers aged 18 to 29 experienced a 50-point-or-greater score drop year over year, compared to 10.1% for the overall population. Student loan delinquency reporting resumed after pandemic-era pauses ended, hitting younger borrowers hardest.

Baby Boomers were the only generation to improve, rising one point to 747. Longer credit histories, diversified credit profiles, and lower revolving balances drive that advantage.

Last year alone, our office saw 91 clients in the 680 to 710 range who believed their score was "basically the same" as 760. The real-world lending difference told a different story every single time.

Does a Good Credit Score Get You the Best Rates?

No. A good score — 670 to 739 on FICO — gets you approved. It does not get you the best pricing.

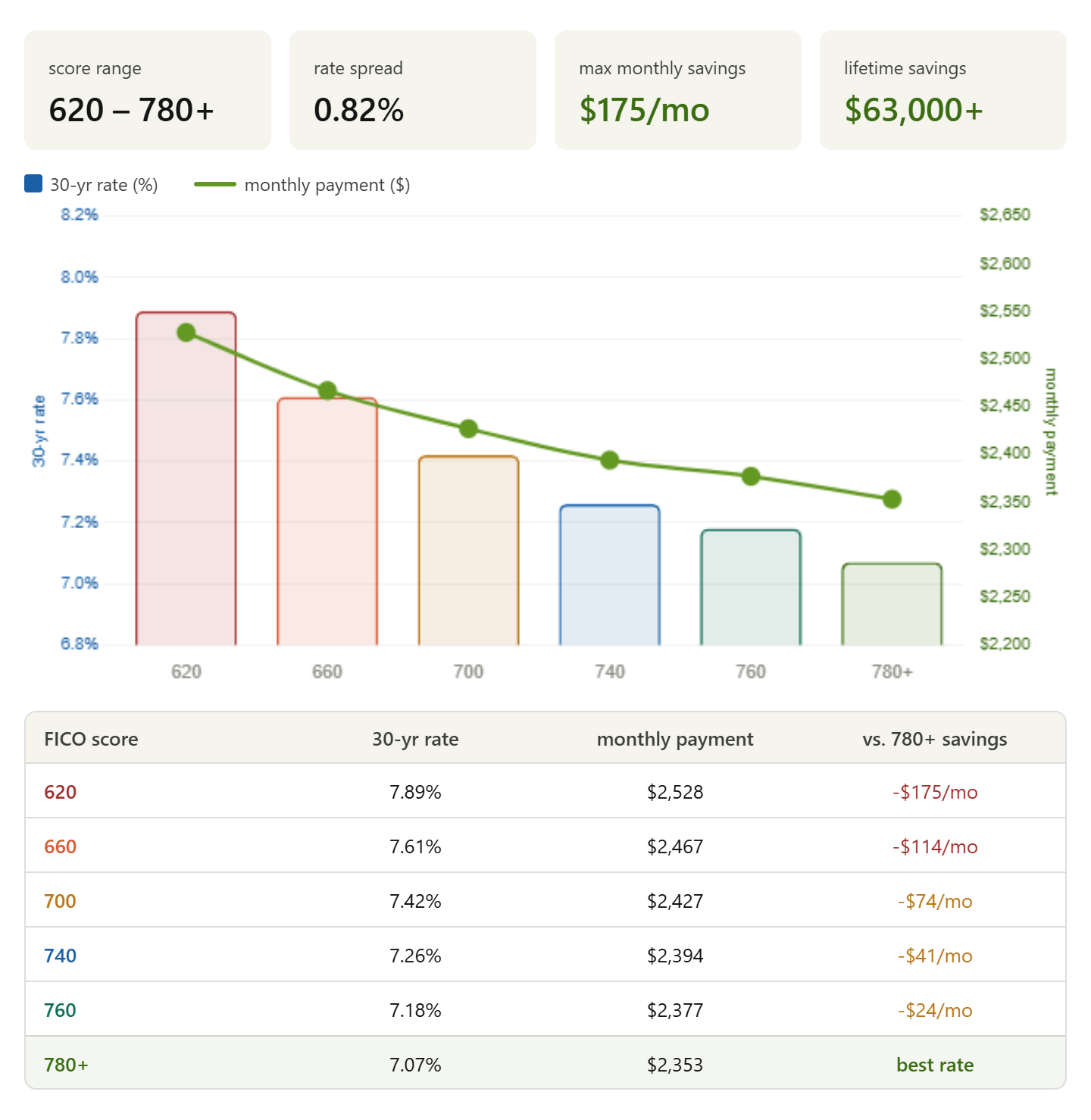

Here is what the difference looks like on a 30-year conventional mortgage, based on Experian 2025 data and early 2026 Freddie Mac averages:

(Source: The Mortgage Reports, citing Experian data, 2026)

Borrowers at the top tier save roughly $168 per month and $60,447 in total interest over the loan term compared to borrowers at the bottom tier. That gap exists even within the "good" range. A 700 score costs about $74 more per month than a 780 score on the same loan.

The pattern repeats with auto loans. In Q1 2026, Experian reported average new-car loan rates of 4.66% for super-prime borrowers (781 and above) versus 16.01% for deep-subprime borrowers (500 and below). On a $20,000 five-year loan, that rate difference adds up to over $7,500 in extra interest. (Source: U.S. News, citing Experian Automotive Finance Market Q1 2026)

The takeaway is simple: "good" is a passing grade. "Very good" is where the real savings begin.

What Credit Score Do You Need for the Best Mortgage Rate?

The target for the best conventional mortgage rate is 760 to 780. At 760, most lenders offer their best available pricing. Pushing past 780 produces minimal additional savings.

For government-backed loans, FHA, VA, and USDA score tiers matter less. These programs treat all scores above a certain threshold more similarly. But for conventional loans, every 20 points you gain between 620 and 760 improves your rate in a meaningful way.

The minimum to qualify for any conventional mortgage is 620. But a 620 score gets you the worst conventional rate. The jump from 620 to 740 is where most of the savings are concentrated.

If you are 6 to 12 months away from a home purchase, targeting 760 before applying is worth the effort. Each tier jump produces measurable monthly savings that compound over 30 years.

What Credit Score Do You Need for the Best Car Loan Rate?

The best new-car loan rates go to borrowers with scores of 781 and above. Experian calls this the "super prime" tier. In Q4 2025, super-prime borrowers averaged 4.66% on new-car loans.

Here is the breakdown by VantageScore tier for auto loans, based on Q1 2026 Experian data:

Super prime (781 to 850): ~4.66% new car

Prime (661 to 780): ~6.07% new car

Near prime (601 to 660): ~9.29% new car

Subprime (501 to 600): ~11.86% new car

Deep subprime (300 to 500): ~16.01% new car

Auto lenders use VantageScore more frequently than mortgage lenders do. Knowing your VantageScore before car shopping helps you negotiate from a position of knowledge. A score of 750 puts you in the prime tier. Crossing 780 moves you into the super-prime tier and unlocks the lowest available rates.

How Does a Good Credit Score Affect Insurance Premiums?

Most states allow auto and homeowners insurance companies to use your credit score when setting premiums. Insurers use credit-based insurance scores, a separate model from FICO but the same underlying credit data drives both.

A lower credit score typically means higher insurance premiums. In most states, moving from a poor credit tier to a good credit tier can reduce auto insurance premiums by 20% to 50%. The exact impact varies by state. California, Hawaii, and Massachusetts prohibit insurers from using credit scores for auto insurance.

If your score is improving, contact your insurer annually to request a re-rating. Many policyholders do not know they can ask. Insurers do not automatically lower premiums as your score improves.

Is Your Credit Score Costing You Money?

A good credit score may get you approved, but a better score can help you qualify for lower interest rates, better loan terms, and bigger long-term savings.

Check Your Credit Report TodayTake the first step toward improving your credit score.

How to Move From Good to Very Good in 2026

The jump from "good" (670 to 739) to "very good" (740 to 799) is the most valuable move most consumers can make. Here is what drives it fastest:

Pay Every Bill on Time

Payment history is 35% of your FICO score. One 30-day late payment can drop a 720 score by 60 to 80 points. Consistent on-time payments for 12 months erase the damage from a single missed payment and push scores upward.

Lower Your Credit Utilization Below 10%

Credit utilization is 30% of your FICO score. Most advice targets 30% or below. But scoring data shows that consumers in the "very good" tier typically carry utilization below 10%. On a $10,000 total credit limit, that means balances stay below $1,000.

Pay your balance before the statement closing date, not just before the due date. The statement balance is what gets reported to the bureaus.

Dispute Errors on Your Credit Report

One in five credit reports contains an error significant enough to affect a lending decision, according to FTC research. Pull all three reports at AnnualCreditReport.com. Dispute inaccuracies directly with the bureau. Correcting a reporting error can add 20 to 50 points within 30 to 60 days.

Avoid New Credit Applications Before Major Loans

Each hard inquiry drops your score by 3 to 5 points. Applying for a store card, a new auto loan, or a credit line increase in the 90 days before a mortgage application can push you out of a better rate tier. Space out applications and consolidate loan shopping within a 14 to 45-day window, where FICO treats multiple inquiries of the same loan type as a single inquiry.

Keep Old Accounts Open

Credit history length is 15% of your FICO score. Closing a paid-off credit card shortens your average account age and reduces your available credit. Both hurt your score. Keep old accounts open and make a small purchase on them quarterly to keep them active.

A good credit score gets you in the door. A very good score — 740 and above — is where the financial benefits become concrete. Borrowers at 760 and above save $60,000 more on a mortgage, pay half the auto loan interest rate of a subprime borrower, and qualify for better insurance premiums and credit card terms. The average American at 713 is close. The gap between 713 and 760 is achievable in 6 to 12 months with consistent payment habits and lower utilization. The math on closing that gap is some of the best personal finance math you will ever run.