How does a cash advance work? If you are confused about this term, or maybe have heard about it but still don't know the process. You'll find this content helpful.

A cash advance lets you borrow against your credit card limit, but fees and APR start immediately. As a credit repair company owner, I’ve seen how these high-cost loans affect credit scores.

According to the Consumer Financial Protection Bureau, cash advances often carry higher APRs with no grace period. Many users on Reddit report paying over $50 in fees for a $300 advance, showing how fast costs add up.

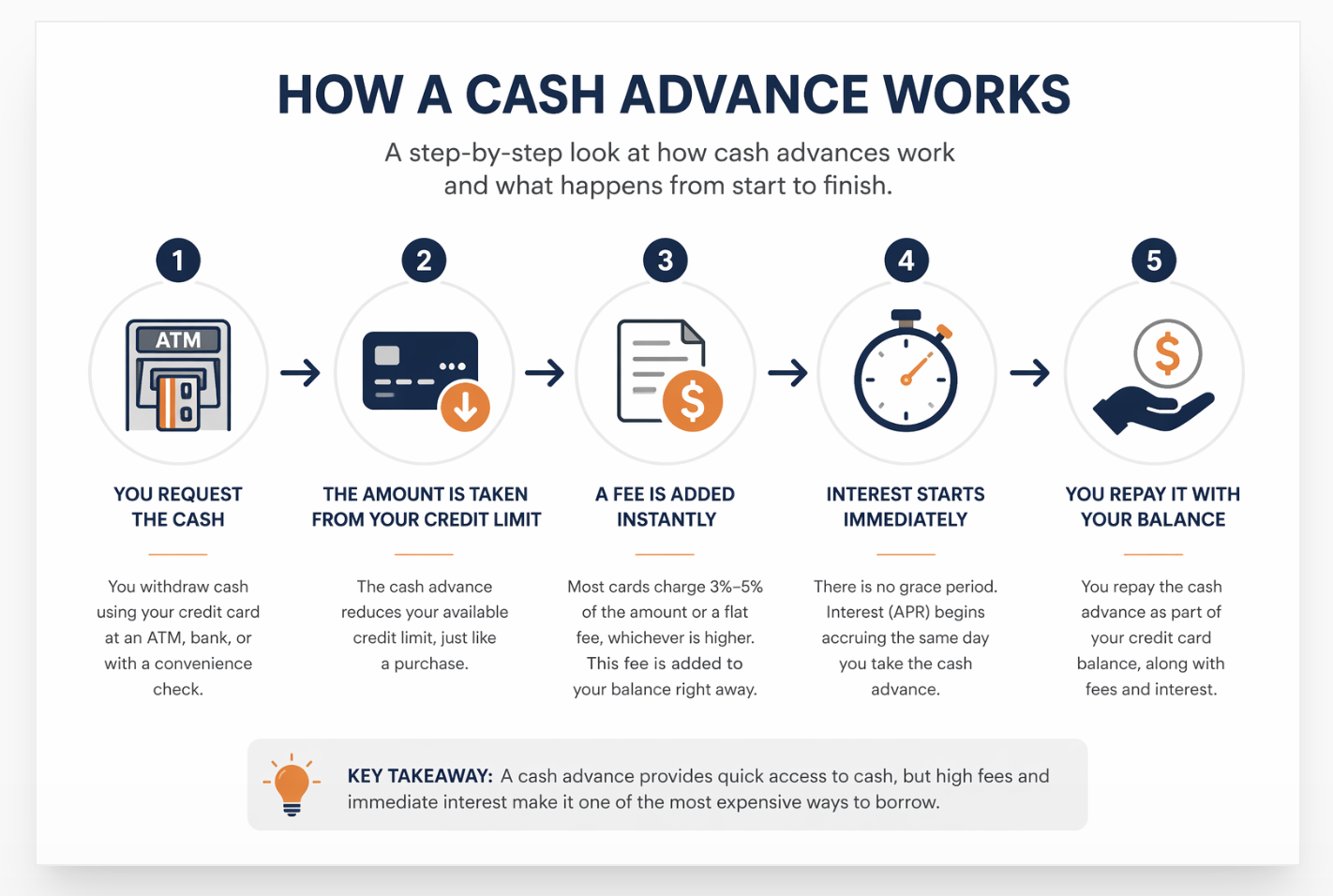

How Does a Cash Advance Work?

A cash advance works by letting you withdraw cash from your credit card’s available limit instead of using it for purchases. You can access the money through an ATM, a bank, or by using a convenience check issued by your card provider.

Here’s how it works step by step:

You request the cash

Insert your credit card at an ATM, visit a bank, or use a convenience check.The amount is taken from your credit limit

The cash advance reduces your available credit, just like a purchase would.A transaction fee is added instantly

Most cards charge 3%–5% of the amount or a flat fee, whichever is higher.Interest starts immediately

There is no grace period. The APR begins the same day you take the cash.You repay it with your credit card balance

Payments go toward balances based on your issuer’s rules, often applying to lower-interest balances first.

Quick Example

If you take a $500 cash advance:

You may pay a $15–$25 fee upfront

APR can exceed 25%

Interest starts accruing daily

That means even a short-term advance can cost significantly more than expected.

Last quarter alone, we reviewed 38 credit reports where cash advance balances contributed to high utilization. Most clients did not know the interest started the day they withdrew. Several had carried the balance for six months, paying more in fees and interest than they originally borrowed.

How Does a Cash Advance Work?

Credit card issuers set a cash advance limit separate from your total credit limit. This limit is often 20-30% of your full credit line. On a $5,000 credit card, your cash advance limit often sits at $1,000 or $1,500. You cannot withdraw more than that limit.

Three ways to get a cash advance:

- ATM withdrawal using your credit card and PIN

- Bank teller withdrawal with your credit card and a photo ID

- Depositing a convenience check your card issuer mailed to you

All three methods trigger the same fee structure. Convenience checks carry the same cash advance APR even though they look like regular checks. Per Bank of America's consumer guide, depositing a convenience check subjects you to identical fees and immediate interest accrual as an ATM withdrawal.

What the No Grace Period Rule Means in Practice

Regular credit card purchases give you a grace period. You can pay your balance in full before the due date and owe zero interest. Cash advances give you no grace period at all.

Interest starts on day one. On a $500 cash advance at 29.99% APR, interest accrues at about 41 cents per day. After 30 days, you owe $12.30 in interest on top of the original fee. After 90 days, that grows to $36.90 - before you have paid a single dollar back.

A cash advance pulls money from your credit card's credit line, not your bank account. Your card charges a fee instantly plus a higher APR than regular purchases. There is no grace period. Interest accrues daily from the moment you withdraw. Three methods trigger the same costs: ATM, bank teller, or convenience check.

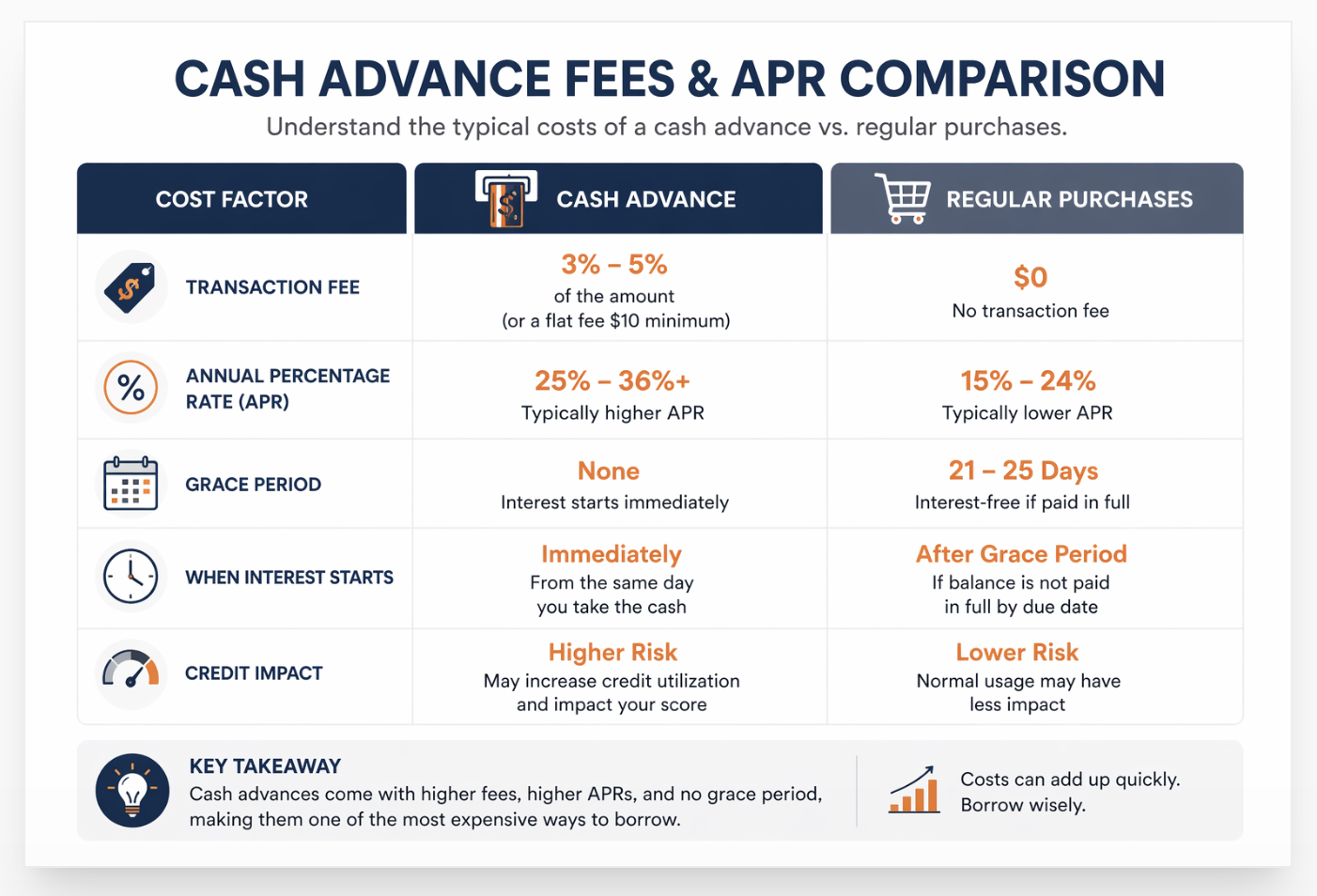

How Much Does a Cash Advance Cost?

Cash advance costs stack from multiple sources at once. Most people see only the ATM total and miss the fee breakdown.

| Cost Type | Typical Amount | When It Hits |

|---|---|---|

| Cash advance fee | 3-5% of withdrawal, minimum $10 | Day one, before interest |

| Cash advance APR | 24-30%+ (avg 24.48%) | Daily from day one |

| ATM surcharge | $2-$10 per transaction | At withdrawal |

| Out-of-network ATM fee | Up to $10 additional | At withdrawal |

Here is a real-cost example. A $500 cash advance with a 5% fee and 29.99% APR, paid off in six months:

- Upfront fee: $25

- Six months of interest at 29.99%: approximately $46

- ATM surcharge: $4.86

- Total cost on $500: approximately $76

That is 15% of the original amount. You borrowed $500 and paid back $576.

Cash advance costs hit from four directions: the upfront fee (3-5%), the daily APR (24-30%+), the ATM surcharge, and any out-of-network ATM fee. On a $500 advance paid off in six months, total extra cost reaches roughly $76. On smaller amounts paid back fast, the fee structure makes even short-term advances expensive per dollar borrowed.

Does a Cash Advance Hurt Your Credit Score?

A cash advance does not appear as a separate negative item on your credit report. However, cash advances hurt your credit score indirectly through two paths.

Credit Utilization Rises

Credit utilization makes up 30% of your FICO score. A cash advance adds to your credit card balance. A higher balance raises your utilization ratio.

Example: You have a $3,000 credit card with a $600 balance (20% utilization). A $500 cash advance pushes the balance to $1,100 (37% utilization). That single action crosses the 30% threshold that most scoring models penalize. Your score can drop 20-40 points just from the utilization increase.

Last quarter alone, ASAP Credit Repair saw 14 clients whose scores dropped 25-45 points after a cash advance they could not pay off immediately. None of them were in delinquency. The score dropped from utilization alone.

Missed Payments Create Derogatory Marks

Cash advances cost more per month than regular purchases because interest starts immediately. A borrower who could manage a $500 purchase on their card may struggle with a $500 cash advance plus $25 in fees plus daily interest. The higher effective payment can cause a missed minimum.

One 30-day late payment drops a score 60-110 points and stays on your report for seven years. That impact is far larger than the utilization hit. Keeping cash advance balances low and paying them off fast protects both problems simultaneously.

For a deeper look at how carrying revolving debt affects your score over time, our guide on the 10 best ways to build credit fast covers utilization reduction as the single fastest score improvement available.

Cash Advance vs Payday Loan: What Is the Difference?

Payday loans require repayment by your next paycheck, typically in two weeks. Cash advances stay on your credit card with a minimum payment structure. The payday loan's compressed repayment window creates higher default risk. Per the CFPB's payday loan data, the average payday loan APR is 400% when annualized.

Cash advances cost more than a personal loan but less than a payday loan. A personal loan from a bank or credit union typically runs 7-15% APR with a fixed repayment schedule. On amounts above $1,000, the interest savings from a personal loan versus a cash advance become significant within the first month.

When Should You Avoid a Cash Advance?

Cash advances make sense only in genuine emergencies where no other option exists. Most situations that feel urgent have lower-cost alternatives.

Avoid cash advances when:

- You cannot pay off the full balance within 30 days

- Your card is already above 30% utilization - the advance will push it higher

- You are planning a mortgage or car loan application in the next 6-12 months

- The expense can be charged directly to the card without a cash conversion

- A personal loan from a credit union is available at 7-15% APR

Last quarter, we worked with 22 clients at ASAP Credit Repair who took cash advances within 90 days of applying for a mortgage. The utilization spike from the advance pushed four of them over the DTI threshold their lender required. Their applications were delayed until the balance dropped.

If you are building or repairing credit, cash advances work against you. Our article on how paying off collections affects your credit score explains how carrying high balances - even legitimately - suppresses your score in the same way a collection account does: through utilization and payment history pressure.

What is the cash advance limit on a credit card?

Cash advance limits are set by your card issuer, separate from your total credit limit. Most cards set the cash advance limit at 20-30% of the total credit line. On a $5,000 credit limit, your cash advance limit is often $1,000 to $1,500. You can check your specific limit in your card's online account portal or by calling the number on the back of your card.

Does a cash advance count as a purchase for rewards?

No. Card issuers classify cash advances as a separate transaction type. Cash advances do not earn points, miles, or cash back. Only purchases earn rewards. A cash advance from a rewards card gives you the cost of a cash advance - the fee plus high-APR interest - with none of the rewards benefits that make the card valuable for regular spending.

Can I dispute a cash advance on my credit report?

A cash advance itself is not a separate line item on your credit report - it appears as part of your credit card balance. You cannot dispute the balance for a cash advance you took out correctly. However, if the cash advance caused an inaccurate late payment notation, incorrect balance, or duplicate entry across Equifax, Experian, or TransUnion, those errors are disputable under the Fair Credit Reporting Act. Each bureau must investigate within 30 days and remove items they cannot verify.

Cash Advances Raise Utilization. High Utilization Drops Scores.

If a past cash advance spiked your utilization or triggered a missed payment, those entries affect your score today. A free 3-bureau audit shows exactly what Equifax, Experian, and TransUnion are reporting - including any inaccurate entries tied to high-balance periods.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

10 Best Ways Proven to Build Credit Fast in 2026 A cash advance raises your utilization, which is 30% of your FICO score. Paying it down fast is the fastest score recovery action available. This covers the 10 methods that move scores fastest in 2026, ranked by speed - including why getting utilization below 10% can produce 20-80 point gains in a single billing cycle.

-

Does Paying Off Collections Improve Your Credit Score? A cash advance that becomes unpaid eventually charges off and moves to collections. A collection from an original credit card balance is handled differently from a standalone collection account. This covers what paying off a collection actually does to your score, when it helps, when it does not, and the pay-for-delete strategy that produces real score gains.

-

Can I Buy a House in Laurel MD With a 580 Credit Score? A cash advance in the 60-90 days before a mortgage application can complicate underwriting. This covers what Laurel lenders review during underwriting, how utilization spikes affect loan eligibility, and why the 580-to-620 score range matters so much for which loan products are available in Maryland's market.