How lenders read your credit report determines whether you get approved, denied, or offered a higher rate. Most borrowers think lenders only check a score. They do not. They read payment history, utilization, account age, credit mix, and recent inquiries to decide how risky you look on paper.

I have sat across from lenders, underwriters, and finance managers. I know what they see when they pull a report and I know what makes them hesitate. Most people walk into a loan application thinking the score is the decision. It is not. The score gets you in the room. The report decides whether you walk out with approval or a denial. I have seen clients with a 700 score get denied because of one open collection the report showed. And I have seen a 640 get approved because the file told a clean story with no derogatory marks in the last 24 months. The report is the story. The score is the headline.

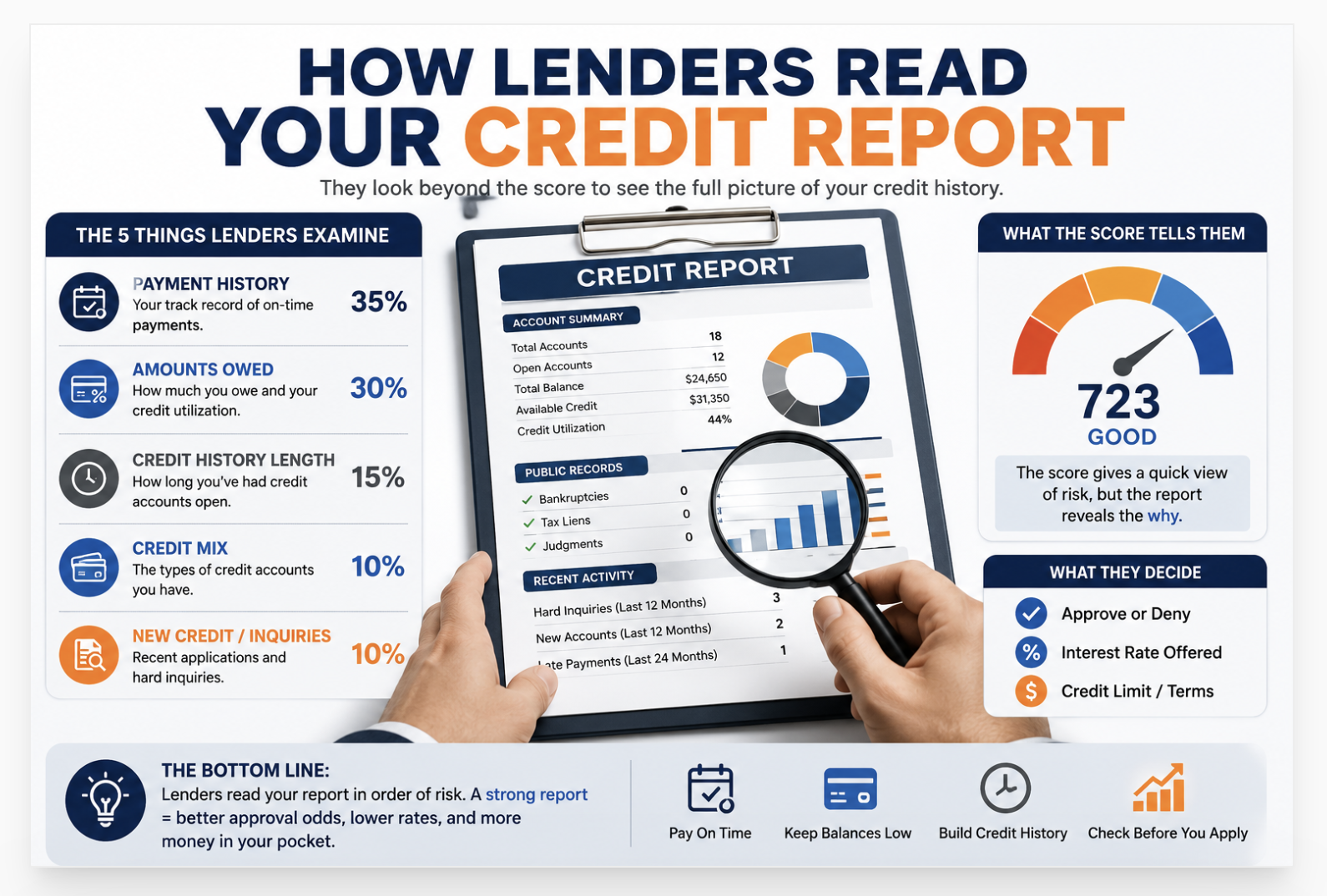

How Lenders Read Your Credit Report

Lenders read your credit report by pulling a tri-merge report from all three bureaus simultaneously. They look at payment history first, then utilization, then account age, then credit mix, then recent inquiries. Each section tells them something specific about risk. The report and score together determine whether you qualify and at what rate.

When you apply for credit, the lender does not just see a number. They pull a full report , often a tri-merge that combines data from Equifax, Experian, and TransUnion into a single document. Each bureau maintains its own file. The lender sees all three.

The tri-merge report shows every account you have ever opened, every payment you have made or missed, every collection that posted, and every inquiry from a lender or credit application. The lender's underwriter goes through this document in a specific order, and that order matters.

As Bankrate explains in their lender risk analysis guide, payment history is the first and most weighted factor , it represents 35% of a FICO score calculation. Lenders check it first because it answers the most important question: does this person pay their bills?

Lenders read the report in order of risk weight. Payment history is their first stop. Then utilization. Then how long you have had credit. A clean payment record with high utilization reads differently than a messy payment record with low utilization. Both matter. Both get read.

The Five Sections Lenders Examine

1. Payment History , The One That Matters Most

Payment history runs 35% of your FICO score. Lenders look at this section and count late payments, missed payments, charge-offs, and collections. They notice the date of each negative event. A collection from six years ago reads differently than one from six months ago.

One thing people do not always know: a 30-day late payment hurts a 780-score borrower more than a 580-score borrower in terms of point loss. The higher you sit, the more a single late mark costs you. I have seen clients lose 90 points from one missed payment after years of clean history. That mark sits on the report for seven years.

If you have a late payment on your file and it occured by mistake or a billing error, there is a process for that. A goodwill letter to remove a late payment sometimes works with creditors who have a history with you. It does not always succeed. But lenders respect a file where the borrower followed up and resolved what they could.

2. Amounts Owed , Utilization Is the Lever

Utilization is the ratio of your credit card balance to your credit limit. Lenders want to see this below 30%. Below 10% is better. A borrower using 80% of every credit card looks maxed out , and to a lender, maxed out means risk.

This section also shows total debt balances across all accounts: auto loans, mortgages, student loans, personal loans. Lenders use this to calculate your debt-to-income ratio, which sits outside the credit score but inside the underwriting decision. High balances on revolving accounts trigger concern even at a good score.

I tell every client: before any major loan application, pay down your cards. Not to zero , that can actually reduce your score slightly by removing revolving activity , but to below 10% on each card. Do it before the statement close date so the low balance reports to the bureaus. I have watched clients gain 40 points from a single paydown cycle, done at the right time.

3. Length of Credit History

This section covers the age of your oldest account, the age of your newest account, and the average age across all accounts. Lenders use this to gauge stability. A borrower with a 12-year-old credit card has demonstrated longer-term financial behavior than someone whose oldest account is 18 months old.

Closing an old card to simplify your wallet damages this section. The account's age still counts while it remains on the report , but eventually it ages off, and your average account age drops. Keep old accounts open. A zero-balance card with no annual fee costs nothing and protects your credit age.

4. Credit Mix

Lenders look at whether you have managed different types of accounts , credit cards (revolving), auto loans, mortgages, student loans (installment). A mix of both types signals experience across product categories. A file with only credit cards looks narrower to a lender than one with cards plus an installment loan in good standing.

This factor carries 10% of the FICO weight. It is not the most important section but it matters in manual underwriting. An underwriter reviewing a borderline file will note whether the borrower has ever managed an installment product successfully.

5. New Credit and Inquiries

Every hard inquiry from a credit application stays on your report for two years and counts toward your score for twelve months. Lenders see a cluster of inquiries as a flag. Five credit applications in a 60-day window looks different from one. It signals that someone is seeking credit across multiple sources at once, which lenders associate with financial stress.

The exception: rate-shopping protection. Multiple mortgage or auto inquiries within a 45-day window count as one under FICO 8 and newer models. Shop multiple lenders during the same 45-day period. The score impact stays the same as a single pull.

Here is something I have seen the industry understate: lenders do not just read the score. They read the pattern. A 680 with 24 months of on-time payments and no new derogatory marks tells a different story than a 680 built from a thin file with one secured card and nothing else. The underwriter reading the first file sees recovery and stability. The underwriter reading the second sees a borrower who has not been tested yet. Same number. Different decision. The score, it doesn't tell the whole story. The report does.

What Lenders Do Not See on Your Credit Report

Not everything follows you into a credit decision. Lenders do not see your income, employment history, savings balance, or net worth on a credit report. Those come through separate documentation , pay stubs, tax returns, bank statements , and the lender asks for them seperately during underwriting.

Lenders also do not see your race, religion, national origin, gender, marital status, or age in the credit report itself. The Equal Credit Opportunity Act prohibits using any of these in a lending decision. The credit report does not include them at all.

Soft inquiries from checking your own credit or from pre-qualification checks do not appear on the version of the report a lender sees. They appear on your personal copy but not on the lender's pull. Checking your own credit never penalizes you with a lender.

According to Experian's guide on mortgage credit scores, mortgage lenders pull a tri-merge report that contains data from all three bureaus plus three separate FICO scores. They use the middle score, not the highest. If your scores are 640, 660, and 720, the lender uses 660. A weak bureau report pulls your effective qualifying score below what your best bureau shows.

This is why checking all three reports matters , not just the one where your score looks strongest. Our guide on how often to check your credit report covers the monitoring schedule that catches errors before a lender pulls it.

What Lenders Look for Beyond the Score

Manual underwriting happens when the automated system cannot clear the file. The underwriter reads the report as a narrative, not a number. They look for patterns.

Patterns that create concern: multiple late payments within the same 12 months, a cluster of new accounts opened in a short period, a charge-off followed by a new credit application within 90 days, collections that the borrower has not addressed, or a rapid increase in balances over the past 6 to 12 months.

Patterns that build confidence: 24 consecutive months of on-time payments after a derogatory event, decreasing balances over time, long-standing accounts with no missed payments, and a mix of account types all reporting positively.

An insight from 20 years in this field: lenders respond to evidence of change. A borrower who had a rough 2020-2021 and then built 3 years of clean history has a more compelling story than a borrower with a thin file and nothing to show either direction. The report is a timeline. Present it as one.

As NerdWallet's FICO Score explainer notes, lenders use scores to predict the likelihood you will fall 90 days past due within the next 24 months. Every element of your report feeds that prediction. The goal is not a high number for its own sake. The goal is a file that signals you will pay as agreed.

When your report contains errors that distort that signal, the lender reads an inaccurate story. Incorrect late payment notations, wrong balances, and accounts that belong to someone else all drag the score and the narrative in the wrong direction. Disputing those errors is the most direct action you can take. Our guide on how to clean your credit report walks through the dispute process and the specific documentation that produces results.

Pull all three reports before any lender does. Do it yourself, at no cost, at AnnualCreditReport.com. Read every line with the question: what does this tell a lender about me? A collection account you forgot about still tells a story. An incorrect late payment tells a story that is not yours. Fix what you can fix before a lender reads it. You have the right to dispute. You have the right to submit a consumer statement. Use every tool available before the lender sees the file. Most people do not know they can do this. Now you do.

Do lenders see the same credit report I see?

No. Lenders see a different version. Your personal credit report includes soft inquiries, marketing records, and all bureau data. The lender's version excludes soft inquiries and is formatted for underwriting review. Lenders also pull FICO scores that you may not see on free monitoring apps , those apps typically show VantageScore, not the FICO model the lender uses. The data behind both comes from the same bureaus, but the score calculated from that data can differ by 20 to 50 points between models.

How far back do lenders look on a credit report?

Derogatory items stay on a credit report for seven years from the original date of first delinquency. Bankruptcies stay for ten years. Lenders see all of it within that window. However, the recency of negative events carries more weight than the age. A collection from six years ago during a hardship period carries less weight in manual underwriting than a collection from six months ago. Lenders are reading patterns and trajectory, not just a list of events.

Can I control what lenders see on my credit report?

Yes, within limits. You cannot remove accurate information that falls within the reporting window. But you can dispute inaccurate entries , wrong dates, wrong balances, accounts that are not yours , and have those removed under the FCRA. You can add a consumer statement to your report explaining a specific circumstance. You can pay down balances to reduce utilization before a lender pulls the report. And you can time your application to follow a statement close date where your updated balances reflect recent payoffs. Each action shapes what the lender reads.

Know What the Lender Sees Before They See It

A free 3-bureau audit shows every entry across Equifax, Experian, and TransUnion right now. Inaccurate entries, duplicate accounts, and wrong dates all change the story your report tells. Find them before the lender does.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

580 Credit Score: What It Means for Your Next Application 580 is the FHA threshold. Lenders read a 580 score alongside the full report , payment history recency, utilization, and derogatory account age all determine whether the 580 produces an approval or a denial with conditions.

-

Paying a Collection Agency: What It Does to Your Credit Report Lenders see collection accounts as a risk signal. Paying without deletion leaves the mark on the report. This covers when payment helps the lender's read of your file and when it does not change the underwriting outcome.

-

Medical Bills on Your Credit Report Medical collections appear in the same section as any other collection when a lender reads your report. The 2022 bureau policy changes and the July 2025 federal rule reversal both affect what medical debt a lender currently sees.