Getting denied for a credit limit increase can be frustrating.

Especially if you've been making payments on time and watching your credit score improve.

The first reaction is usually the same.

"How long do I have to wait before I try again?"

The answer depends on why the request was denied.

I've seen people reapply a week later and get denied again because nothing changed.

I've also seen borrowers improve their utilization, increase their income, or reduce debt and get approved just a few months later.

The waiting period matters.

The reason behind the denial matters more.

Before submitting another request, it helps to understand what the lender saw the first time.

How Long Should You Wait After Credit Limit Increase Denial?

Most borrowers should wait at least 3 to 6 months after a credit limit increase denial before reapplying. However, the ideal timeline depends on the reason for the denial and whether meaningful improvements have been made to the credit profile.

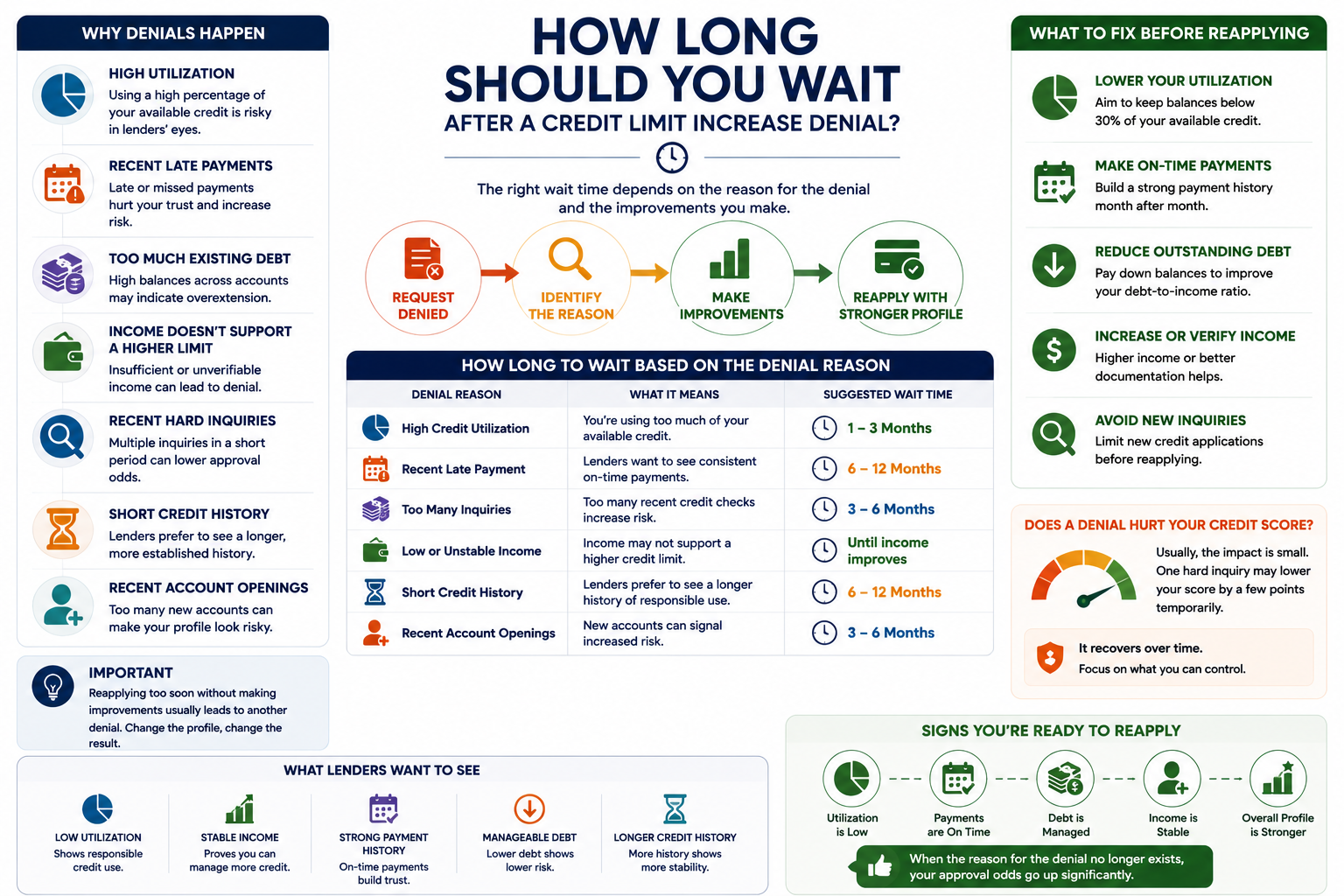

Why Was Your Credit Limit Increase Denied

The denial reason determines the recovery timeline. High utilization on the card is the most common cause , and the fastest to fix. Late payments, high overall debt, insufficient income, recent hard inquiries, short account history, and recent new account openings are the other six most frequent reasons. The adverse action letter the issuer sent within 7 to 10 days of the denial names the specific one. That letter is the starting point for every decision that follows.

Most borrowers focus on the question of when to reapply.

The more important question is: what did the lender see that produced the denial?

Without that answer, the wait period is meaningless. Six months of unchanged behavior produces a second denial. One month of targeted improvement sometimes produces an approval.

The full breakdown of each denial reason and what card issuers evaluate in a limit increase request , including how internal account behavioral data plays into the decision beyond the credit score , is in the companion guide on why credit limit increases get denied. Read the adverse action letter. Then read that guide. Then come back to this timeline framework.

Can You Reapply Immediately After a Denial

No , and not just because of the 6-month waiting period most issuers enforce. Reapplying before fixing the denial reason produces the same denial. The issuer's risk model sees the same risk signals as before. Immediate reapplication with a hard-pull issuer also costs an additional 5 to 10 score points without producing any benefit. Wait. Fix the named cause. Then reapply with a stronger file.

Two things happen when a borrower reapplies too quickly.

First: the same evaluation system sees the same risk signals and produces the same outcome.

Second: if the issuer runs a hard inquiry, the score drops again. Now the file shows two recent hard inquiries from limit increase requests , which itself becomes a new risk signal in the next evaluation.

Immediate reapplication does not demonstrate persistence. It demonstrates that the borrower did not understand the reason for the denial.

How Long Should You Wait Based on the Denial Reason

The wait time after a credit limit increase denial depends on the specific denial reason. High utilization denials resolve fastest , 1 to 3 months after paying the balance down. Late payment denials take longest , 6 to 12 months of clean payment history. The table below gives the specific wait time for each denial reason.

| Denial Reason | Suggested Wait Time | Required Action |

|---|---|---|

| High credit utilization | 1 to 3 months | Pay card to under 10% before reapplying. Let the lower balance report at statement close. |

| Recent late payments | 6 to 12 months | Build a clean payment streak with zero misses. Set every account to autopay minimum. |

| Too many recent inquiries | 3 to 6 months | Wait for inquiry impact to fade. Open no new accounts during this period. |

| Low or outdated income | Immediate after update | Update income on file through the account portal before reapplying. |

| Short account history | 6 to 12 months | Use the card regularly with low balances and pay in full each month. Build behavioral data. |

| Too much existing debt | 3 to 6 months | Pay down highest-balance accounts to reduce total revolving debt exposure. |

| Recent new account openings | 3 to 6 months | Keep the credit profile stable. No new applications or new accounts during the wait. |

What Should You Fix Before Reapplying

Fix the specific thing named in the adverse action letter. Not the most common issue. Not what this guide names as "most likely." The thing named in the letter. After that specific fix, confirm these five conditions before reapplying: utilization on this card is under 30% (under 10% for the strongest signal), at least 6 months of consecutive on-time payments, income on file is current, no new accounts or hard inquiries in the last 3 months, and the 6-month issuer minimum has passed.

- Step 1: Address the specific denial cause first. The adverse action letter names one primary reason. If it says high utilization, that is the first and highest-priority fix. Everything else is secondary until that cause resolves.

- Step 2: Update income on file if income has changed. Log into the account portal. Update the annual income figure before submitting any new request. This takes two minutes and sometimes changes the outcome immediately for income-related denials.

- Step 3: Confirm payment history on this account. No missed payments on any account in the past 6 months. The issuer evaluates recent payment behavior more heavily than older history in limit increase decisions.

- Step 4: Check the account activity pattern. Issuers prefer to see regular card usage with low balances. A card with no activity for 4 months followed by a limit increase request shows no behavioral signal. Use the card for small purchases and pay in full each month during the waiting period.

- Step 5: Confirm no new accounts or inquiries in the last 3 months. A clean, stable credit profile going into the reapplication strengthens the case. New accounts and new inquiries add risk signals that work against the evaluation regardless of the primary denial reason.

Does a Credit Limit Increase Denial Hurt Your Credit Score

Only if the issuer ran a hard inquiry. Soft-pull issuers , like Capital One for limit increase requests , produce zero score impact from either the request or the denial. Hard-pull issuers create a temporary 5 to 10 point dip that stays on the report for two years but fades after 3 to 6 months. Asking the issuer directly , "Do you use a soft or hard inquiry for limit increase evaluations?" , before reapplying prevents an unnecessary score penalty on a likely-denied application.

This matters most for timing a reapplication.

If the issuer uses a hard pull and the file still shows the same denial reason, reapplying scores another hard inquiry with no approval to offset it. The net result: lower score, same denial, worse file for the next attempt.

As Experian's guide on credit limit increase timing confirms, whether the issuer runs a hard or soft inquiry should factor into the timing of any limit increase request , and this is especially important during the post-denial recovery period when the file is already in a weaker state.

Should You Call and Ask for Reconsideration

Yes , and this is the first action to take after receiving the adverse action letter, before any waiting period begins. Calling the card issuer's credit department for reconsideration is different from submitting a new request. Some issuers route reconsideration calls to human reviewers who can evaluate context the automated system cannot. This costs nothing, takes one phone call, and sometimes reverses the denial entirely.

- Income recently increased but the on-file figure still reflects the old amount

- The high utilization was temporary , the card now shows a lower balance

- A single late payment resulted from a specific circumstance and the full pattern is otherwise clean

- The issuer's automated model missed data the human reviewer can see

- High utilization is still present with no paydown completed

- Multiple late payments in the past 12 months , pattern, not one incident

- Recent hard inquiry cluster across multiple credit applications

- Income genuinely cannot support the requested higher limit

When calling for reconsideration, lead with the specific context that changes the picture. "I recently got a salary increase to $X that isn't yet on file" is a specific, actionable reason for reconsideration. "I've been a good customer for two years" is not , it does not address the specific risk signal that triggered the denial.

What If Your Credit Score Improved After the Denial

Score improvement alone may not change the outcome. Card issuers evaluate internal account behavioral data alongside the credit score , data that does not appear in FICO calculations. A 30-point score increase from paying down a different card does not automatically change the utilization signal on this specific card, the payment history pattern on this account, or the internal account risk model the issuer uses. Score improvement is necessary but not sufficient for many denials.

This is the most common post-denial misconception.

A borrower sees their score rise 28 points. They assume the issuer's concern is resolved. They reapply at the 6-month mark. Same denial.

Why? Because the score went up from paying down a different card. But the card with the limit increase request still shows 76% utilization. The score improvement did not change the specific signal the issuer flagged.

Score improvement matters. It matters most when the score improvement comes from fixing the exact factor named in the adverse action letter. A score jump from reduced utilization on this specific card changes the evaluation. A score jump from other factors may not.

Can High Utilization Cause Multiple Denials

Yes. High utilization on the card being reviewed is the single most common repeating denial cause. Each application with the same high utilization produces the same evaluation and the same outcome. Multiple denials from the same cause also compound the damage if the issuer runs hard inquiries , each denial leaves an inquiry on the report while doing nothing to address the utilization signal.

The pattern looks like this.

Borrower has a card at 83% utilization. Gets denied. Waits four months. Score goes up slightly from other improvements. Reapplies. Same 83% utilization. Same denial. Score drops another 7 points from the second hard inquiry.

Now the file shows two hard inquiries from limit increase requests and the same high utilization. That file looks more concerning to the issuer's risk model , not less.

One targeted paydown breaks this cycle. Get the specific card to under 10% utilization before any reapplication. As NerdWallet confirms, credit utilization is one of the most impactful factors in credit scoring , and on a limit increase request, it receives even more direct evaluation since the issuer focuses specifically on this account's balance-to-limit ratio.

What Do Credit Card Companies Want to See Before Approving a Higher Limit

Card issuers want to see five things in the reapplication file: utilization on this card below 30% (under 10% for the strongest signal), consistent on-time payments for at least 6 months, updated income that supports the requested limit, reduced total debt across all accounts, and at least 12 months of account history with this issuer. Meeting these five conditions produces the strongest reapplication file regardless of which reason caused the original denial.

| Factor | Strong Signal | Why It Matters |

|---|---|---|

| Card utilization | Under 10% on this card | Directly signals responsible use of the existing limit. The primary evaluation trigger for limit increase requests. |

| Payment history | Zero lates in past 6-12 months | Confirms the existing limit is manageable. Recency carries more weight than older history. |

| Income documentation | Current income on file | Supports repayment of the new limit if fully charged. Outdated figures underrepresent actual repayment capacity. |

| Total debt exposure | Declining across all accounts | Signals overall credit management, not just this card's pattern. |

| Account history length | 12 to 24 months with this issuer | Provides enough behavioral data for the issuer's model to evaluate risk accurately. |

Should You Request a Credit Limit Increase Before Applying for a Mortgage

Timing matters significantly when a mortgage is in the near-term plan. A soft-pull limit increase 6 to 12 months before the mortgage application lowers utilization and raises the credit score , strengthening the mortgage file. A hard-pull limit increase within 90 days of mortgage application may trigger underwriter questions. Know the issuer's inquiry type before deciding when to make a post-denial reapplication request.

The sequence that works best when a mortgage is 12 to 18 months out:

- Address the denial cause (typically 1 to 3 months for utilization, up to 12 months for late payments).

- Reapply for the limit increase when the file meets the five criteria above , at least 6 to 12 months before the mortgage application.

- If approved: score improvement from lower utilization improves the mortgage rate tier. If denied again: reassess whether the credit file needs broader work before the mortgage application.

A limit increase denial that keeps repeating often signals a credit profile issue broader than this one card. That broader picture , every account balance, every collection, every scoring factor across all three bureaus , is exactly what a full credit review through credit repair Houston addresses before a borrower approaches a mortgage application.

The full framework for pre-mortgage debt strategy is also covered in the guide on paying off debt before applying for a mortgage , which includes when limit increase requests help versus when they create inquiry risk in the wrong window.

Signs You Are Ready to Reapply

As Bankrate's credit limit guidance confirms, timing a limit increase request to align with a stronger credit profile , lower balances, clean payment history, updated income documentation , produces better results than simply waiting out the minimum period and reapplying with the same file.

The Best Time to Request Another Credit Limit Increase

The best time is not based on the calendar. It is based on whether the denial reason no longer exists. A borrower who pays a card from 85% to 8% utilization in 45 days and updates their income is a stronger reapplication at month 2 than a borrower who waited 12 months without changing anything. The clock matters for the issuer's 6-month minimum. The credit profile condition matters for the actual approval outcome.

The distinction is simple and worth remembering.

Waiting produces eligibility to ask again. Improving produces a reason to say yes.

Both are required. Waiting alone produces a repeated denial. Improving without waiting past the 6-month minimum produces a rejection on procedural grounds.

When both conditions are met , the minimum time has passed AND the specific denial reason no longer exists , reapply with confidence. That is the best time.

How many times can you request a credit limit increase on the same card?

Most card issuers allow multiple lifetime requests but enforce a 6-month minimum between each. There is no universal cap on the total number of requests. However, repeated denials from the same cause , especially when they trigger hard inquiries each time , create a pattern of credit-seeking behavior that works against future approvals. Focus on addressing the denial cause rather than frequency of applications.

What credit score helps most for a credit limit increase reapplication?

There is no universal minimum score for a successful limit increase. Most issuers view scores above 670 favorably for this purpose, but as shown in this article, the score alone often does not determine the outcome. The utilization on this specific card, income on file, and payment pattern on this account typically carry as much weight as the overall FICO score. A borrower with a 650 score and 5% utilization on this card may receive an approval while a 700-score borrower at 80% utilization on the same card gets denied.

Does waiting 6 months guarantee a credit limit increase approval?

No. Waiting 6 months sets the minimum eligibility window. It does not change the credit profile signals that triggered the original denial. A borrower who waits exactly 6 months with the same high utilization, unchanged income documentation, and the same behavioral pattern on the account receives the same denial. The approval comes from addressing the cause, not from the passage of time alone.

-

Why Was My Credit Limit Increase Denied? 7 Common Reasons This article covers what to do after a denial. The companion guide covers why the denial happened in the first place , the seven specific causes, how card issuers use internal behavioral data beyond the credit score, what the adverse action letter is legally required to tell you, and what each denial reason means for the approval profile. Start there before building the reapplication strategy covered here.

-

How Available Credit Can Raise Your Credit Score Faster Than You Think High utilization is the most common credit limit increase denial cause , and the fastest to fix. This covers the exact mechanics of how available credit drives the FICO utilization calculation, why paying before the statement closes produces the fastest score improvement, and why the improvement is non-linear so that getting to under 10% produces the largest score gain. Understanding this article makes the utilization paydown before a reapplication more purposeful and measurable.

-

Should You Pay Off Debt Before Applying for a Mortgage? For borrowers managing a post-denial timeline alongside a mortgage application window, this covers the pre-mortgage credit strategy: which debt to pay first, when to time a limit increase request versus when to avoid any new inquiries, and the 90-day plan that produces the strongest file before the mortgage goes in. The interaction between limit increase timing and mortgage underwriting is specific and actionable here.