Few things are more frustrating than seeing your credit score improve, making on-time payments, and still getting denied for a credit limit increase.

Most people immediately assume the problem is their credit score.

Often it isn't.

Credit card issuers evaluate risk differently than credit scoring models.

A borrower can have a decent score and still appear risky for a limit increase.

That is why understanding the reason behind the denial matters.

The denial itself is often a clue.

It reveals which part of your credit profile lenders believe needs improvement.

Once you understand that, approval becomes much easier to plan for.

Why Was My Credit Limit Increase Denied?

Credit limit increase requests are commonly denied because of high credit utilization, insufficient income, recent late payments, excessive debt, recent inquiries, short account history, or lender-specific risk concerns.

Common Reasons Credit Limit Increases Get Denied

What Happens When You Request a Credit Limit Increase

When a credit limit increase request comes in, the card issuer runs an automated risk evaluation. It reviews the credit profile, the account's internal behavioral data, and sometimes income. The issuer may run a soft inquiry (no score impact) or a hard inquiry (5 to 10 point temporary dip), depending on the issuer's policy. The result: approved, denied, or approved for a lower amount than requested.

Two things happen in this evaluation. The external credit file check. And the internal account data review.

The external check uses bureau-reported information: credit score, payment history across all accounts, total debt, and recent inquiries.

The internal review uses data no credit score captures: how often the borrower pays this card in full versus carries a revolving balance, how spending velocity changed over the past 12 months, and whether the card activity signals a borrower who manages credit or depends on it.

These two reviews happen simultaneously. A borrower with a strong external credit profile but concerning internal account behavior can still receive a denial. That combination is exactly why many borrowers with "good scores" get surprised by denials.

Why Credit Card Companies Increase Limits

Card issuers increase credit limits when they believe extending more credit creates low risk and future business value. Low risk means the borrower is unlikely to max out the new limit and fail to repay. Business value means the borrower spends on the card and generates interchange fee income. Both conditions need to point in the same direction for an approval to follow.

Understanding the issuer's goal helps explain what they look for.

Card issuers profit from interchange fees on purchases and interest on carried balances. A borrower who uses the card actively, pays reliably, and stays below the credit limit is a profitable customer. A borrower who maxes out the card and stops paying is a loss.

A credit limit increase request signals that the borrower wants more capacity. The issuer asks: will that capacity produce more responsible activity, or more risk? The answer shapes the decision far more than the credit score alone.

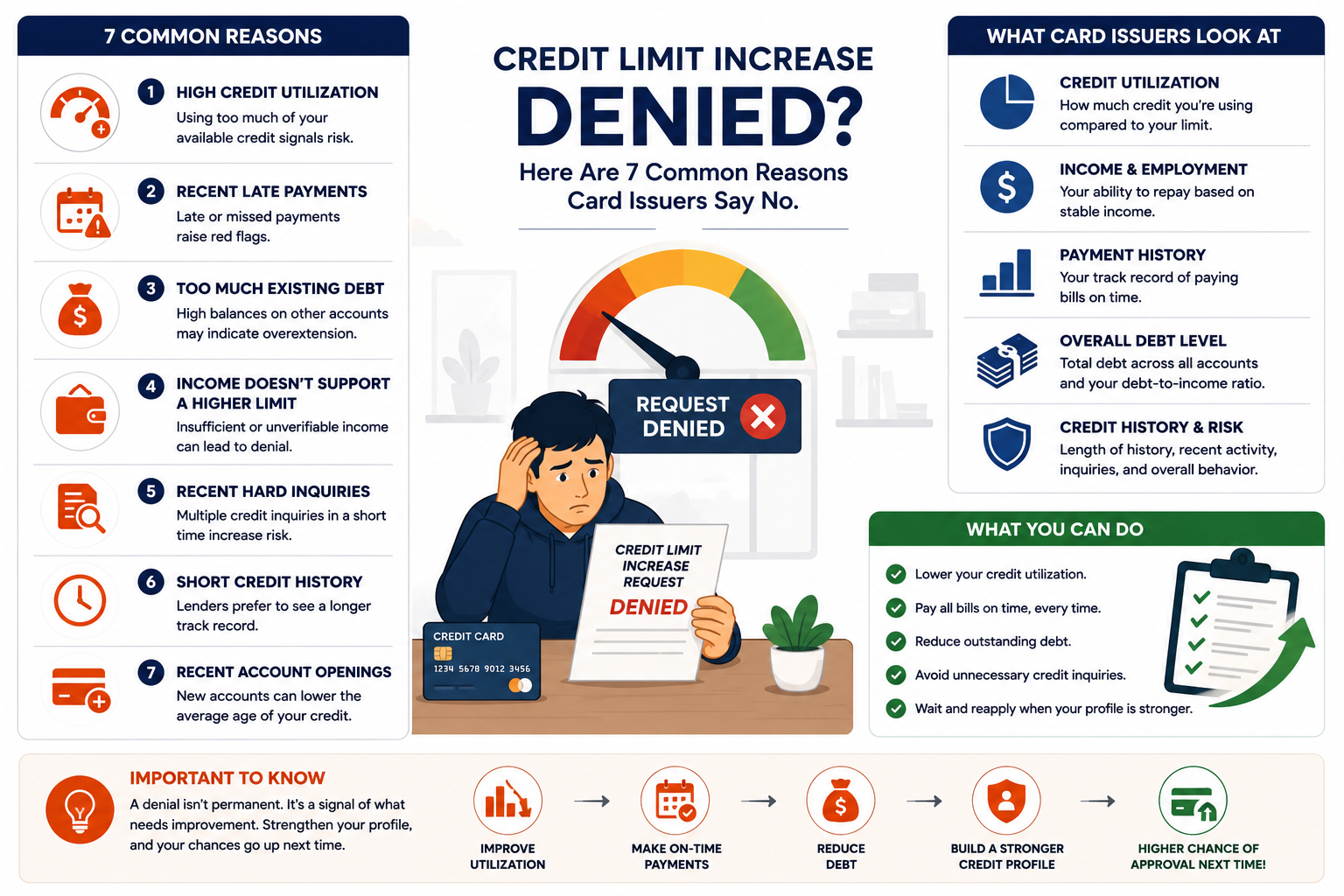

7 Common Reasons Credit Limit Increases Get Denied

1. High Credit Utilization

Borrowers often request more credit precisely because a card is nearly maxed out. That high utilization is exactly what triggers the denial. A card at 85% signals to the issuer that existing credit gets consumed rather than managed. Extending more limit creates more exposure to the same behavior pattern the issuer is already observing.

The irony: the moment most people feel they need a higher limit is the worst moment to request one. The right time to request is when the balance is low.

Fix: Pay the card to under 10% utilization before reapplying. The lower balance changes the risk signal entirely.2. Recent Late Payments

A missed payment on any account tells the issuer that credit obligations already strain the budget. A late payment on this specific card carries extra weight , it directly shows that the current limit creates repayment difficulty. Raising it amplifies the risk the late payment already demonstrated.

Recency matters most. A late payment from six months ago is more damaging than one from three years ago in a limit increase evaluation.

Fix: 6 to 12 months of perfect on-time payments before reapplying. Set every bill to autopay minimum to prevent further damage.3. Too Much Existing Debt

Card issuers evaluate total exposure across all accounts, not just this card. A borrower with four credit cards, two personal loans, and an auto loan may receive a denial even with strong payment history, because the total debt load signals overextension risk. The issuer is not just evaluating this account , it is evaluating the full picture of how much credit is already in use.

Fix: Pay down highest-balance accounts before reapplying to reduce the total revolving debt picture visible across the credit file.4. Income Does Not Support Higher Limits

Card issuers evaluate whether income supports full repayment of the requested limit if it were charged up entirely. If income on file hasn't updated since the card opened , and income has since increased , the issuer may be evaluating a stale income figure. Many borrowers forget that income information on file gets outdated and never update it.

Fix: Log into the account portal and update income before requesting. Higher documented income reduces the risk the issuer assigns to the same limit amount. Check the income on file with the issuer first. An outdated lower figure may be the only reason for the denial.5. Recent Hard Inquiries

Multiple recent hard inquiries from credit card applications, personal loan requests, or auto financing create a pattern that reads as active credit seeking. Issuers interpret this as a potential sign of financial pressure. Each individual inquiry is minor. A cluster of inquiries in a short window raises a flag about why the borrower needs new credit from multiple sources simultaneously.

Fix: Wait 3 to 6 months after the last hard inquiry before reapplying. Avoid opening any new accounts during the waiting period.6. Short Account History

An account open for 8 to 10 months provides limited behavioral data. The issuer does not yet know how spending patterns evolve, whether the borrower carries balances through difficult months, or how the account gets managed across different financial circumstances. Insufficient history produces insufficient confidence for a limit expansion.

Fix: Request after 12 to 24 months of account history. Use the card regularly with low balances and pay in full every month during this period.7. Recent New Account Openings

Opening multiple new credit accounts in a short window raises the same concern as multiple inquiries. Rapid credit expansion signals that a borrower is actively building new credit capacity , which may indicate anticipation of financial need. Requesting a limit increase on an existing card while also opening new accounts compounds this signal.

Fix: Wait at least 6 months after the last new account opening. Keep the credit profile stable during the reapplication period.Can High Utilization Cause a Credit Limit Increase Denial

Yes , and it is the most common single reason for denial. The timing problem is built into the pattern: borrowers most often request more credit when the card is near its limit. That near-limit balance is the first thing the issuer's risk model flags. The request itself confirms the card runs at near-full consumption. Extending more limit in this situation creates more exposure to the same consumption pattern.

The issuer's risk logic runs this way.

A card at 88% utilization means $8,800 of a $10,000 limit is in use. If the limit moves to $15,000, the issuer expects the balance to stay at or near $8,800 , not the utilization to drop. The behavioral history says: this card gets used heavily.

Low utilization before the request tells the opposite story. A card at 7% , $700 of a $10,000 limit , says this borrower has capacity and uses it selectively. More limit creates negligible additional risk. That file gets approved.

The fix is straightforward. Pay the card to under 10% before requesting. Wait for the lower balance to report to the bureaus at statement close. Then submit the request. The same borrower, the same issuer, the same account , but a dramatically different utilization signal.

Understanding how available credit affects credit scores explains exactly why the utilization signal matters not just for limit increases but for every lending decision tied to the credit profile.

Why Your Credit Score May Not Be the Problem

A 700 score can produce a denial. A 650 score can produce an approval. The credit score determines a general risk tier , it does not make the limit increase decision. Card issuers supplement the score with internal account data that no bureau captures: payoff behavior on this specific card over the past 12 months, spending velocity changes, and balance carry patterns. Two borrowers with identical scores look completely different inside the issuer's internal model.

This pattern is also why focusing exclusively on the credit score after a denial often misses the actual fix. The score is a summary. The issuer's internal model is the detail. When the adverse action letter names a specific reason, that reason is the detail worth addressing.

What Do Credit Card Issuers Actually Look At

| Factor | Why It Matters to the Issuer | Impact on Decision |

|---|---|---|

| Utilization (this card) | How much of the current limit gets consumed. Signals credit dependence vs credit management. | Very High |

| Payment history (this card) | Whether the current limit creates repayment difficulty. Recent lates are most damaging. | Very High |

| Income on file | Whether income supports full repayment if the new limit gets charged up entirely. | Very High |

| Total existing debt | Overall credit exposure across all accounts. Overextension risk at the portfolio level. | High |

| Recent hard inquiries | Pattern of new credit seeking. Multiple recent inquiries signal financial pressure. | High |

| Account history length | Sufficient data for the issuer to evaluate behavioral patterns over time. | Moderate-High |

| Credit score (overall) | General creditworthiness tier. Sets the starting evaluation point, not the final one. | Moderate |

| Payoff behavior (internal) | Whether the borrower pays in full or carries revolving balances. Invisible to borrower, visible to issuer. | Very High |

Does a Credit Limit Increase Denial Hurt Your Credit Score

Only when the issuer runs a hard inquiry. Soft inquiries , used by issuers like Capital One for limit increase evaluations , produce zero score impact and leave no trace on the credit report. Hard inquiries cost approximately 5 to 10 points and remain on the report for two years, though scoring impact fades significantly within 3 to 6 months. Before requesting, ask the issuer: "Do you run a hard inquiry for limit increase evaluations?" If they use a hard pull and the file has known risk factors, improving the file before applying saves the score cost of a likely denial.

- Soft pull issuers. Many issuers evaluate limit increase requests without a hard inquiry. Denial after a soft pull costs nothing in score terms. The credit profile improves as the borrower addresses the denial reason, and the reapplication carries no inquiry penalty.

- Hard pull issuers. Other issuers run a full hard inquiry regardless of outcome. Denial after a hard inquiry means the score drops 5 to 10 points without the utilization improvement that an approval would have provided. Net effect: worse off than before applying.

- The strategic implication. Ask before applying. The question is simple and the answer changes the approach entirely. For hard-pull issuers, address the denial-likely risk factors before submitting the request.

As Experian confirms, while a single hard inquiry has minimal long-term impact, multiple inquiries from various limit increase requests and new applications within a short period create a cumulative concern for issuers reviewing the file.

How Long Should You Wait Before Reapplying

Fix utilization before counting days. Pay the card to under 10% of the limit before the next statement closes. Wait for the lower balance to report to the bureaus. Then reapply , even if only 60 to 90 days have passed. The 6-month minimum still applies at most issuers, but the utilization fix is what actually changes the outcome. Waiting 6 months at the same high balance produces the same denial.

Wait 6 to 12 months and make every payment on time during that period. Set every account to autopay minimum. Issuers want a clean, recent payment streak , not just an old one. One more missed payment during the waiting period restarts the timeline.

Update income on file before reapplying. Log into the account portal and update the annual income figure. Many issuers let borrowers update income without submitting a new limit increase request. Once income is updated, reapply immediately , no additional wait required if that was the sole denial reason.

Wait 3 to 6 months after the last hard inquiry. Do not open any new accounts during the waiting period. Each new application adds another inquiry and another new account flag to the file. The goal is a quiet, stable profile going into the reapplication.

Wait until the account reaches 12 to 24 months of consistent activity. Use the card regularly for small purchases and pay in full each month. This builds the internal behavioral data the issuer's model needs to see before extending additional exposure.

Can a Credit Limit Increase Help Your Credit Score

Yes. An approved credit limit increase reduces utilization without requiring any debt paydown. The same balance on a higher limit represents a smaller percentage of available credit. Utilization makes up 30% of a FICO score. A meaningful utilization drop from a limit increase can add 20 to 40 points , sometimes more , within a single billing cycle. That score improvement then carries into future lending decisions including mortgage rate pricing.

The chain: higher limit, same balance, lower utilization percentage, stronger scoring signal, potential score improvement. As Bankrate's credit limit guide confirms, a limit increase that reduces utilization without increasing the balance is one of the most efficient score improvement strategies for borrowers already managing their accounts responsibly.

A card carrying $2,500 on a $5,000 limit is at 50% utilization. After a limit increase to $12,000, the same $2,500 balance drops to 20.8%. That single change can move the score from a 40-50% suppression band into the 20-30% range , a meaningful improvement in the amounts owed category that accounts for nearly one third of the FICO calculation.

This is why a credit limit increase at the right moment is a deliberate score improvement strategy, not just a convenience request.

Should You Request a Credit Limit Increase Before Applying for a Mortgage

Timing matters significantly here. A soft-pull limit increase 6 to 12 months before mortgage application lowers utilization, improves the score, and strengthens the mortgage file , with zero inquiry risk. A hard-pull limit increase within 90 days of a mortgage application may trigger underwriter questions about the new inquiry and whether new credit accumulates before closing. Know the inquiry type before making any request near a mortgage timeline.

- 6 to 12 months before application. Best window for soft-pull issuers. Score improvement from lower utilization compounds over several months before the mortgage credit pull. No inquiry risk. No underwriting complication.

- 30 to 90 days before application. Avoid hard-inquiry limit requests. Mortgage underwriters review recent inquiries and may ask about new credit being sought while a mortgage is pending. A new inquiry in this window can trigger conditions or documentation requests.

- After mortgage approval. The safest window for hard-pull issuers. No impact on an approved mortgage, and the improved utilization from an approval helps with future credit decisions.

How to Improve Approval Odds Before Reapplying

The five highest-impact actions before reapplying, in order: pay this card to under 10% utilization, update income documentation on file with the issuer, achieve 6 or more months of perfect payments across all accounts, avoid opening new accounts or new inquiries during the waiting period, and confirm whether the issuer uses a soft or hard pull before submitting. These five actions address all seven common denial reasons.

- Pay this card to under 10% utilization. Highest single impact. Changes the primary risk signal the issuer's model evaluates for this account. Do it before the statement closes so the lower balance reports to the bureaus before the request goes in.

- Update income on file. Log into the account portal and submit current income. An increase in income since the original card opening is one of the most common easily fixable denial reasons , and the most commonly overlooked.

- 6 months of zero missed payments across all accounts. Set every bill to autopay for the minimum. This creates a clean recent payment streak visible to the issuer's model even if older late payments exist in the history.

- No new accounts, no new hard inquiries. Keep the credit profile stable during the waiting period. Every new inquiry and every new account opening adds risk signals to the file that work against the limit increase evaluation.

- Use the card regularly with low balances. Small monthly charges paid in full each billing cycle build the internal behavioral data the issuer values: active use, responsible balances, consistent payoff. This pattern directly addresses the internal account risk model that affects the decision alongside the credit file.

Borrowers working on overall credit profile improvement alongside a limit increase strategy can get a full picture of what the file shows across all three bureaus through credit repair in Houston , identifying not just the limit increase factors but every item affecting lending decisions across the complete credit file.

What a Credit Limit Denial Really Tells You

A denial is data. It identifies which specific risk signal the issuer reacted to. The adverse action letter names it. Fix that signal. The outcome changes. Most denial reasons on this list resolve within 60 to 180 days when the specific factor gets addressed. The denial is not a judgment of creditworthiness for all time. It is a snapshot of one risk variable that the issuer's model flagged at the time of the request.

Borrowers who reapply successfully after a denial are not the ones with the highest scores.

They are the ones who read the adverse action letter, fixed the specific issue it named, waited the appropriate period, and reapplied with that signal resolved.

The letter is an instruction. Follow it.

| Risk Signal | Approval Impact | Typical Fix Timeline |

|---|---|---|

| High utilization | Negative | 30 to 90 days to pay down below 10% |

| Late payments | Negative | 6 to 12 months clean payment history |

| High total existing debt | Negative | 3 to 12 months of systematic paydown |

| Low or outdated income | Negative | Immediate , update on file before reapplying |

| Recent hard inquiries | Negative | 3 to 6 months for impact to reduce |

| Short account history | Negative | 12 to 24 months of consistent account use |

| Low utilization | Positive | Immediate after paydown |

| Strong updated income | Positive | Immediate after income update |

| Long clean payment streak | Positive | Compounds each month |

As NerdWallet's credit limit increase guide confirms, timing matters as much as credit profile , requesting at the right moment in the account lifecycle, with the right utilization and income documentation, changes the outcome for the same borrower at the same issuer more than chasing a higher overall score number.

Why was I denied a credit limit increase with a good credit score?

Credit scores summarize credit file data. Card issuers also use internal behavioral data that credit scores do not include: spending patterns on this specific account, whether balances get paid in full or carried month to month, and spending velocity changes over the past year. A borrower with a 715 score carrying 82% utilization on this card for six months looks riskier inside the issuer's model than the score suggests. Always read the adverse action letter , it names the specific reason, which is often behavioral, not score-related.

What credit score is typically needed for a credit limit increase?

There is no universal minimum score for credit limit increases. Each issuer sets its own criteria. Scores above 670 are generally competitive for limit requests, but the score is often not the deciding factor. Utilization, income, and payment history on this specific account carry as much weight as the overall score in most issuers' models. A 650-score borrower with low utilization, updated income, and a 12-month clean payment streak on this card may receive approval while a 710-score borrower with high utilization and recent inquiries gets denied.

Can I request reconsideration after a credit limit increase denial?

Yes. Call the issuer's credit department and ask for reconsideration. Explain any context the automated system missed: a recent income increase not yet on file, a temporarily high balance now paid down, or a specific hardship that caused a past late payment. Some issuers have human review processes for reconsidering automated decisions. This is worth one phone call before waiting six months and reapplying from scratch.

-

Does Debt Consolidation Hurt Your Credit Score? High total existing debt is one of the seven reasons credit limit increases get denied, and consolidation is often the strategy borrowers consider to reduce it. This covers the actual FICO score impact of consolidating debt: what creates a temporary score drop (hard inquiry, new account), what produces longer-term improvement (lower utilization, simplified payment structure), and when consolidation helps versus when it adds new negative signals to the credit file before a limit increase request.

-

How Available Credit Can Raise Your Credit Score Faster Than You Think The fastest path from a denied limit increase to an approved one runs through utilization reduction , and this covers exactly how it works. Why the score updates within 30 days when utilization drops, why paying before the statement closes matters, and how the improvement is non-linear so that crossing below 10% produces the largest single score gain. The mechanics explained here are the same ones that determine whether a reapplication succeeds or fails.

-

Should You Pay Off Debt Before Applying for a Mortgage? A credit limit increase before a mortgage application can lower utilization and improve the score , but only at the right timing and with the right inquiry type. This covers the full pre-mortgage credit strategy: which debt to pay first, when to request limit increases versus when to avoid them, and the 90-day plan that produces the strongest file before the application goes in. The connection between limit increase timing and mortgage outcome is made specific and actionable here.