How to dispute apartment collections starts with one question most renters never ask:

“Why am I being charged this much?”

Not many know about this. But, apartment collections are some of the most frustrating accounts we deal with. Not because the balances are always huge. Because many people never even knew the charges existed until they got denied for another apartment or saw their credit score drop.

A lot of these accounts come from move-out charges. Carpet replacement. Paint. Cleaning fees. Early lease termination. Sometimes the apartment sends the balance straight to collections without explaining the charges clearly first.

I’ve seen people charged $2,000 for carpet in a unit they lived in for years. I’ve seen duplicate utility balances. I’ve seen collections show up after tenants already paid the apartment directly.

That is why you should never rush to pay apartment collections before reviewing the details carefully.

The collector needs to prove the charges are real, accurate, and legally collectible. Let's expand this discussion.

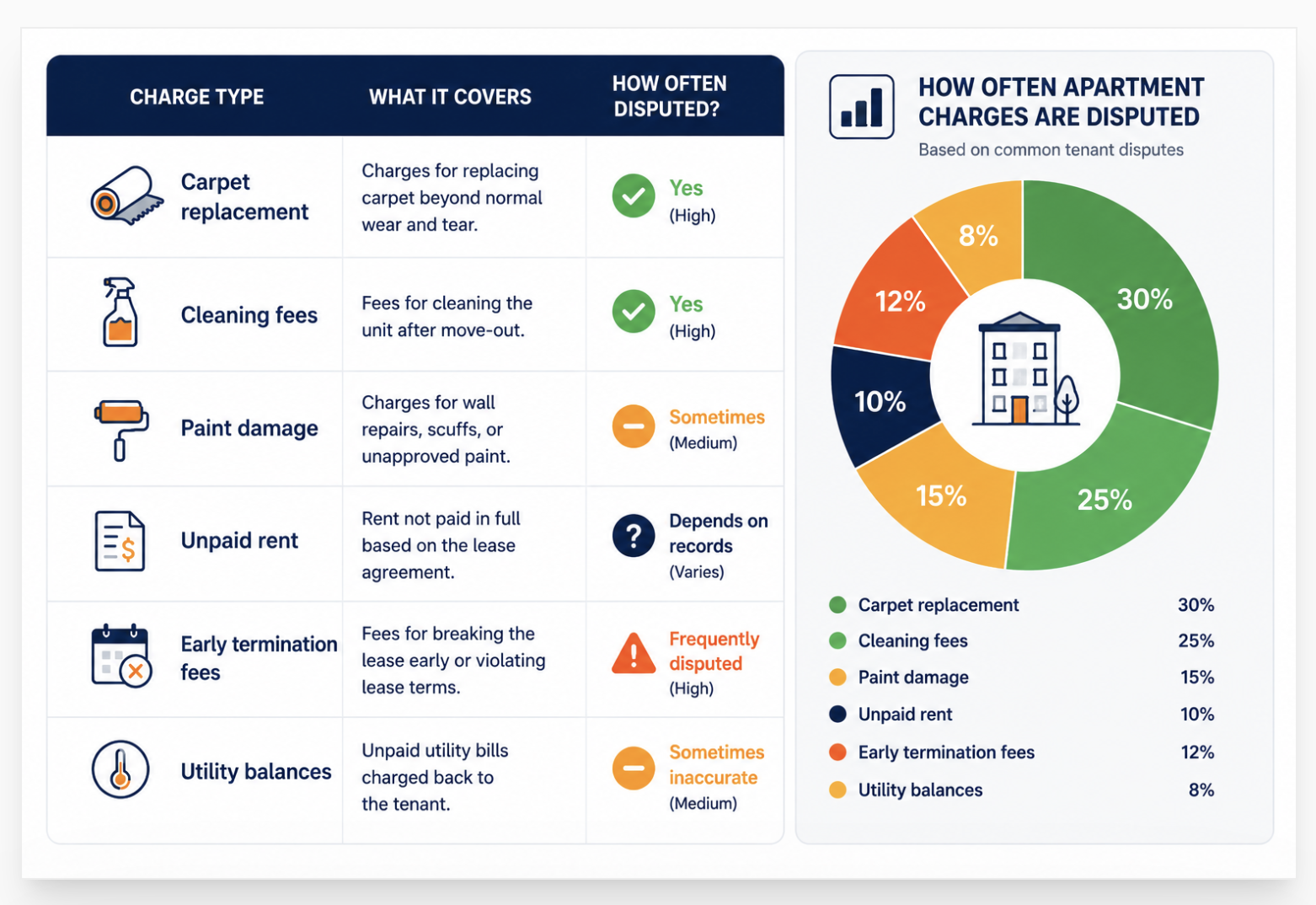

Common Apartment Collection Charges

Most apartment collections do not come from unpaid rent alone. A large number come from move-out charges tenants never expected or never agreed with in the first place.

I’ve seen apartment complexes send people to collections over carpet replacement, paint touch-ups, cleaning fees, and utility balances months after moving out. Some charges are valid. Some are inflated. Some fall under normal wear and tear and should not have been billed that aggressively.

Carpet replacement and cleaning fees are some of the most disputed charges because many landlords try charging tenants for full replacement costs instead of prorated wear. Early termination fees also create problems, especially when lease terms are unclear or the apartment rerents the unit quickly after move-out.

Before paying apartment collections, ask for:

itemized charges

photos of damages

invoices or receipts

lease agreements

payment records

move-out inspection reports

If the apartment or collector cannot clearly prove the balance, you may have grounds to dispute the account with the collector and the credit bureaus.

What Are Apartment Collections

An apartment collection is a debt collection account that appears on your credit report for money a landlord or property management company claims you owe after move-out. The landlord could not collect through normal billing and sent the balance to a third-party collection agency. That agency now reports the account to the credit bureaus and contacts you for payment.

Most people do not see an apartment collection coming.

They move out. They think everything is squared away. Three to six months later, they check their credit or apply for a new apartment and find out a collection account appeared. The balance is often higher than expected.

Apartment collections cover a range of charges. Some are valid , unpaid last month's rent, broken lease fees, actual damages. Others get disputed because they include things the landlord should never have charged for, like carpet replacement on an old carpet or cleaning fees that exceed what the lease allows.

What types of charges lead to apartment collections

Landlords frequently charge the full cost of new carpet. In most states, normal wear and tear on carpet is the landlord's expense. A carpet with remaining useful life cannot be billed entirely to the tenant.

Vague "cleaning fees" without documentation are hard to justify. If you left the apartment in the same condition as you received it (or better), a cleaning charge may not hold up to a validation challenge.

These depend heavily on lease language. If the fee structure was not clearly stated in the lease, the charge may be unenforceable. Collectors often inflate these without being able to provide the lease provision that authorizes them.

This is more often valid but also frequently wrong. Miscalculations, payments applied incorrectly, and disputes over the move-out date all produce inaccurate unpaid rent balances that are worth verifying.

Sometimes accurate. Often contain billing errors, final-month estimates, or charges that should have come from the security deposit first. Always request the breakdown before accepting the balance.

Holes in walls, broken fixtures, appliance damage beyond normal use , these are generally valid charges. The challenge is that landlords often bundle these with normal wear and tear without separating them.

Why Apartments Send Tenants to Collections

Landlords send tenants to collections because billing through normal channels did not produce payment. They send the balance to a third-party agency that reports to credit bureaus and contacts the tenant directly. The goal is payment. The side effect is a derogatory mark on the tenant's credit report that affects future rental applications, loan approvals, and credit scores for seven years.

The timeline usually goes like this.

You move out. The landlord processes the security deposit and calculates what they claim is owed. They send a final itemized statement , usually within 14-30 days depending on the state. If the balance is not paid, they may first try to collect directly. When that fails, the account goes to a collection agency. Some landlords skip direct billing entirely and go straight to collections.

The collection agency then reports the account to Equifax, Experian, and TransUnion. Some also report to specialty tenant screening databases used specifically by landlords and property managers. Those tenant screening reports can follow you independently of your standard credit report.

How Apartment Collections Hurt Your Credit

An apartment collection account drops a credit score by 50-100 points depending on the starting score and the rest of the file. The impact is strongest in the first year. It also triggers denials on future rental applications because landlords specifically screen for rental collection history using databases like CoreLogic SafeRent and TransUnion SmartMove.

Two separate systems track apartment collections. The first is the standard credit report at Equifax, Experian, and TransUnion , the one you already know about. The second is a set of specialized tenant screening databases that landlords use specifically when evaluating rental applications.

A collection that appears in both systems creates a double problem. The credit score drops affect your ability to get loans, cards, and better rates. The tenant screening database entry affects your ability to rent , even if you later improve your credit score significantly.

Understanding what credit score landlords require matters because apartment collections often pull a score below the threshold many landlords set. Most landlords look for 620-650 at minimum. A collection that drops a 700 score to 625 moves a qualified applicant into the "requires co-signer or increased deposit" category at most properties.

How to Dispute Apartment Collections

Send a debt validation request first. Do not pay or acknowledge the debt before seeing written proof of what the charges are and whether they are accurate. If the documentation is incomplete or the charges are wrong, dispute the account with the credit bureaus. Each step has a specific deadline and process under the FDCPA and FCRA.

Go to AnnualCreditReport.com and request Equifax, Experian, and TransUnion separately. Find the apartment collection. Note the original delinquency date, the balance, the collection agency name, and whether the same debt appears more than once. Duplicate entries on the same account from the original landlord and a debt buyer are common , and disputable.

Free | Takes 15 minutes | Do this before any other stepUnder the FDCPA, you have 30 days from the collector's first contact to request full written validation of the debt. Send the letter by certified mail with return receipt. Ask for the itemized charge list, a copy of your lease, damage documentation with photos and dates, proof that the security deposit was applied first, and documentation showing they legally own the account. As Nolo's FDCPA debt validation guide confirms, collectors must provide this documentation before continuing collection activity.

Certified mail only | 30-day deadline from first contact | Keep the receiptWhen the collector responds, go line by line. Flag carpet charges on old carpet. Flag cleaning fees without receipts or photos. Flag charges the lease does not authorize. Flag anything already covered by the security deposit. Identify charges that qualify as normal wear and tear under your state's landlord-tenant law. Most states prohibit billing tenants for general deterioration from normal use.

Document every discrepancy in writing before proceedingIf the collection contains inaccurate details , wrong balance, wrong date, charges that are not supported by the lease or documentation , file a dispute with each bureau showing the account. Include your documentation: the lease, the collector's response, move-out photos, and any written communication with the landlord. The bureau has 30 days to investigate. Under the Fair Credit Reporting Act, accounts that cannot be verified must be removed.

Dispute all three bureaus separately | 30-day investigation window eachIf specific charges are inaccurate , normal wear and tear billed as damage, fees not in the lease, duplicate charges , write to the collector disputing those specific line items. Provide your documentation. This puts the burden on the collector to substantiate or remove those charges. Collectors that continue reporting inaccurate information after a dispute may violate the FCRA and face civil liability.

Written disputes create a paper trail | Fax or mail with confirmationIf the agency failed to provide validation, contacted you after a cease and desist, reported inaccurate information, or used false or threatening language, file a complaint at consumerfinance.gov. According to the CFPB's tenant and debt collection rights page, renters have federal protections under both the FDCPA and FCRA. Complaints create a public record and trigger investigation. Documented FDCPA violations allow you to sue for up to $1,000 in statutory damages plus attorney fees.

File at consumerfinance.gov and reportfraud.ftc.gov | One year from the violation dateWhat Proof Should a Debt Collector Provide

If the collector provides a vague summary without supporting documentation, that is insufficient validation. You can note this in writing and dispute the account with the bureaus based on unverifiable information.

Can You Remove Apartment Collections From Your Credit Report

Yes, but the path depends on whether the account is accurate.

If the account is inaccurate , wrong balance, charges for normal wear and tear, fees not in the lease, wrong dates, or the account does not belong to you , dispute it. The bureau investigates. If the collector cannot verify the accuracy, the account comes off.

If the account is accurate, removal is harder but not impossible. Three options exist.

Pay-for-delete. Offer to pay the balance in exchange for written agreement that the agency removes the tradeline. Some smaller collection agencies agree. Larger national agencies rarely do. Get any agreement in writing before paying a single dollar. A verbal promise is not enforceable.

Goodwill deletion. After paying in full, write to the collection agency explaining your situation and asking them to remove the account as a goodwill gesture. This works more often with original creditors than debt buyers. It is worth trying, especially if the balance was relatively small or the account is recent.

Wait it out. The account ages off automatically after seven years from the original delinquency date. As it ages, the score impact decreases. By years five through seven, most collection accounts have minimal scoring impact on borrowers who have otherwise rebuilt their credit profiles.

What If the Charges Are Wrong

If the charges are wrong, dispute them in writing to the collector and to the credit bureaus. Provide documentation supporting your position. The collector must investigate and correct or remove inaccurate information. Continuing to report information you have disputed and they cannot verify is an FCRA violation.

The most common errors in apartment collections fall into four categories.

Normal wear and tear billed as damage. Scuffs on walls, small carpet indentations, minor fading , these are the landlord's cost in most states. If the collector bills you for them, pull your state's landlord-tenant statute and cite the specific provision in your dispute letter.

Security deposit not applied before sending to collections. The landlord must apply the security deposit to valid charges first. Whatever remains after that is what could legitimately go to collections. If the collection balance reflects the full charges without subtracting the deposit, the number is wrong.

Charges for items pre-existing at move-in. If your move-in walkthrough documented damage already present , stained carpet, marked walls, broken blinds , the landlord cannot charge you for those items on the way out. Move-in inspection reports are powerful dispute documents.

Lease does not authorize the fee. Landlords sometimes charge fees that are not in the lease , administrative fees, reletting fees, or miscellaneous charges. If the lease does not mention it, the collector has difficulty justifying it.

Some apartment collection agencies specialize in rental debt and use aggressive reporting tactics. National Credit Systems is one of the most frequently searched collection agencies handling apartment and rental debt. The same validation rights and dispute process applies regardless of which agency the landlord used.

Can Apartment Collections Stop You From Renting Again

Yes. Apartment collections appear in tenant screening databases that landlords use specifically for rental history. These are separate from standard credit reports. Even if your credit score recovers, the rental collection may still appear in TransUnion SmartMove, CoreLogic SafeRent, or RentBureau and cause denials at properties that run specialized tenant screening.

This is the part most people do not realize until they are denied again.

You dispute the collection. Your credit score improves. You think you are clear. Then a new landlord runs a tenant-specific background check through CoreLogic or TransUnion's rental screening service. The apartment collection shows up there even though your credit report looks better.

Disputing with the credit bureaus may not fix the tenant screening database. You may need to dispute separately with the specific screening company. The CFPB's tenant screening dispute guide explains that you have 60 days from a denial to request a free copy of the report used against you. Review it, dispute inaccuracies, and the screening company has 30 days to investigate.

Having an eviction or collection on your rental record makes the application process harder at large corporate properties. Smaller private landlords tend to be more flexible. Many private landlords consider context , the age of the collection, whether it was paid, the circumstances , rather than applying a hard cutoff rule.

Should You Pay Apartment Collections

Do not pay automatically. Run through these checks first.

- Is the debt accurate? If charges are wrong, inflated, or include normal wear and tear, dispute before paying. Paying validates the account and removes your ability to dispute the balance after the fact.

- Is the debt within the statute of limitations? Each state limits how long a collector can sue. If the delinquency date is older than your state's limit, the debt is time-barred. They can still call. They cannot win a lawsuit.

- Does the account appear on your credit report? If it does not, paying puts it on the radar and may restart reporting. Verify the credit report status first.

- How old is the account? An apartment collection from six and a half years ago ages off in six months. Paying it may reset it to "paid collection" without improving the score meaningfully and does not accelerate removal.

If the debt is valid, recent, and accurate, paying it helps. A paid collection looks better to some lenders than an unpaid one. And a pay-for-delete agreement , where the collector agrees in writing to remove the tradeline upon payment , produces the best possible outcome.

How Long Do Apartment Collections Stay on Your Credit

Seven years from the original delinquency date. The clock starts when you first fell behind on rent or when the charges became overdue , not when the landlord sent the account to collections, not when a debt buyer purchased it, and not when the collection agency first reported it. Any collection showing a more recent start date may be re-aged, which violates the FCRA.

Re-aging is when a debt buyer or collection agency reports the account with a newer date to extend how long it appears on your report. This is illegal.

Compare the date of first delinquency on the collection to the date the original account went bad. If the collection shows a date that is months or years later than the original delinquency, dispute it. Include documentation of the actual original delinquency date in your dispute. The bureau must correct or remove accounts with inaccurate dates.

The score impact of a collection also decreases over time. A four-year-old collection hurts much less than a one-year-old collection, assuming the rest of the credit file looks clean. Borrowers who rebuild credit aggressively while waiting for an old collection to age off often reach 680-720 scores before the account drops off.

Can apartment collections be removed from my credit?

Yes. If the account contains inaccurate information , wrong balance, wrong dates, charges for normal wear and tear, or fees not authorized by the lease , dispute it with the credit bureaus. Unverifiable information must be removed under the FCRA. Valid collections can also be removed through a written pay-for-delete agreement before payment, though not every collector offers this. All collections age off automatically after seven years from the original delinquency date regardless of payment status.

Can apartments charge for normal wear and tear?

No. In most states, landlords cannot legally charge tenants for normal wear and tear. This includes minor wall scuffs, small carpet compression from furniture, and general fading from regular use. Landlords can charge for damage beyond normal use , large holes, major stains, intentional damage. The specific definition of normal wear and tear varies by state. If a charge is based on standard property deterioration from regular use, it may not be legally enforceable and can be disputed.

What if I never received the final bill?

This is common. Many landlords send the final bill to the old address , the apartment you just vacated , rather than a forwarding address. The bill goes undelivered. The account moves to collections and the first time you hear about it is from the collection agency or on your credit report. Not receiving the bill does not eliminate the obligation, but it does strengthen your case for negotiating the balance, requesting removal, or demonstrating that the landlord failed to follow proper notice procedures under your state's law.

Can landlords send you to collections without notice?

Most states require landlords to send an itemized statement of charges within 14-30 days of move-out, along with the security deposit accounting. Sending an account to collections without first providing this notice may violate state landlord-tenant law. Check your state's specific notice requirement. If the landlord skipped the required notice and sent you directly to collections, document that fact and include it in any dispute with the collector or the credit bureaus.

Do apartment collections hurt your credit score?

Yes. A collection account drops most credit scores by 50-100 points depending on the starting score and how recent the account is. Higher starting scores typically see larger drops because lenders consider a collection more unexpected from a previously clean borrower. The impact is strongest in the first two years. By years five and six, most collections have significantly less score impact on borrowers who have rebuilt their files with positive payment history and low utilization.

Apartment Collection Pulling Down Your Score?

An apartment collection may contain charges that are inaccurate, unsupported by documentation, or based on normal wear and tear. A free 3-bureau audit shows exactly what each bureau currently reports so you can identify what is disputable before paying or responding to anything.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

701 Credit Score , What It Means and What You Can Qualify For An apartment collection often drops a score into the 620-660 range. This covers what you can and cannot get approved for at each tier, the specific rate differences between 670 and 740, and the fastest path from a collection-damaged score back to the 700s where most rental applications and loan products open up again.

-

RJM Acquisitions , What to Do When a Debt Buyer Contacts You About Old Debt Some apartment collections get sold to third-party debt buyers years after the original delinquency. This covers how zombie debt buyers purchase old rental accounts for pennies, how to verify whether the statute of limitations has expired, and the validation rights and dispute steps that apply whenever a debt buyer contacts you about a past-due rental balance.

-

Credit Score Landlords Use , FICO vs VantageScore Not all landlords use the same credit score model. Understanding which score a landlord pulls , and how apartment collections appear differently across FICO and VantageScore models , helps you target your dispute and rebuild strategy toward the specific score that matters most in the rental market where you are applying.