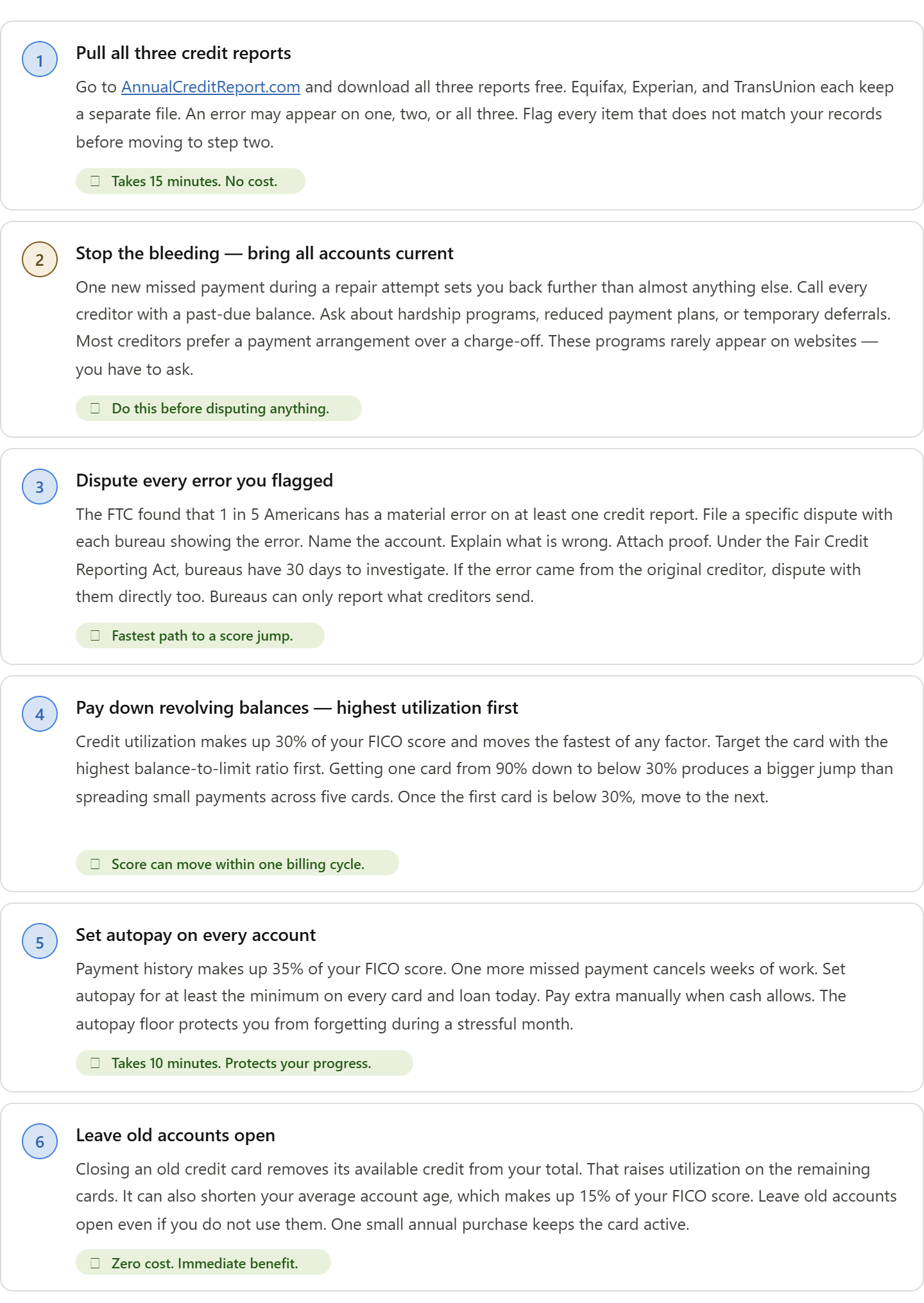

How to Save a Failing Credit Score and Rebuild Fast: pull all three credit reports first, bring every past-due account current, dispute any errors, then pay down revolving balances. Do not open new credit or close old cards during this process. The fastest gains, up to 40 to 60 points, come from fixing utilization and removing errors within the first 30 to 60 days.

A failing credit score does not fix itself. But it does respond fast to the right actions in the right order. Most people try to save a failing credit score by doing things that feel productive but actually slow recovery down. They open new cards, close old ones, or pay off the wrong debts first. This guide covers what works and what the data shows about how long each step takes.

Running a credit repair company, I work with failing credit scores every single week. This is my favorite type of case because the turnaround is almost always faster than the client expects. One man came to us at a 498. He had lost his job eight months before. Six payments across three cards were missed. A medical bill had gone to collections. He thought it was over. We found two errors, helped him bring accounts current through a hardship plan, and disputed the collection successfully. His score hit 612 in seven months. He financed a car the following year at a rate his bank called reasonable for his profile. A failing score is a problem with a process. Not a permanent outcome.

A single missed payment drops a score by 60 to 110 points, depending on starting score and credit depth, according to SmartAsset. The myFICO community forums document thousands of cases where scores fell from the 600s into the 400s within two billing cycles. The drop is fast. The recovery is slower but achievable with a clear plan.

What Is a Failing Credit Score?

A failing credit score is any score that blocks you from a normal financial life. Here is how the FICO range breaks down and what each zone means for your access to credit:

A score below 580 means most lenders deny outright. Those who approve attach rates well above the national average. A score between 580 and 669 gets you conditional approvals with high interest. Below 500, many landlords, employers, and insurers also start flagging your profile.

Failing scores do not always come from bad habits. Credit report errors, medical collections, identity theft, and sudden hardship all push scores into dangerous territory fast. The first step before fixing anything is finding out exactly what caused the drop.

How to Save a Failing Credit Score: Fix These First

Sequence matters more than speed. Doing step four before step one wastes time and sometimes causes more damage. Follow these in order.

What Hurts a Failing Credit Score the Most?

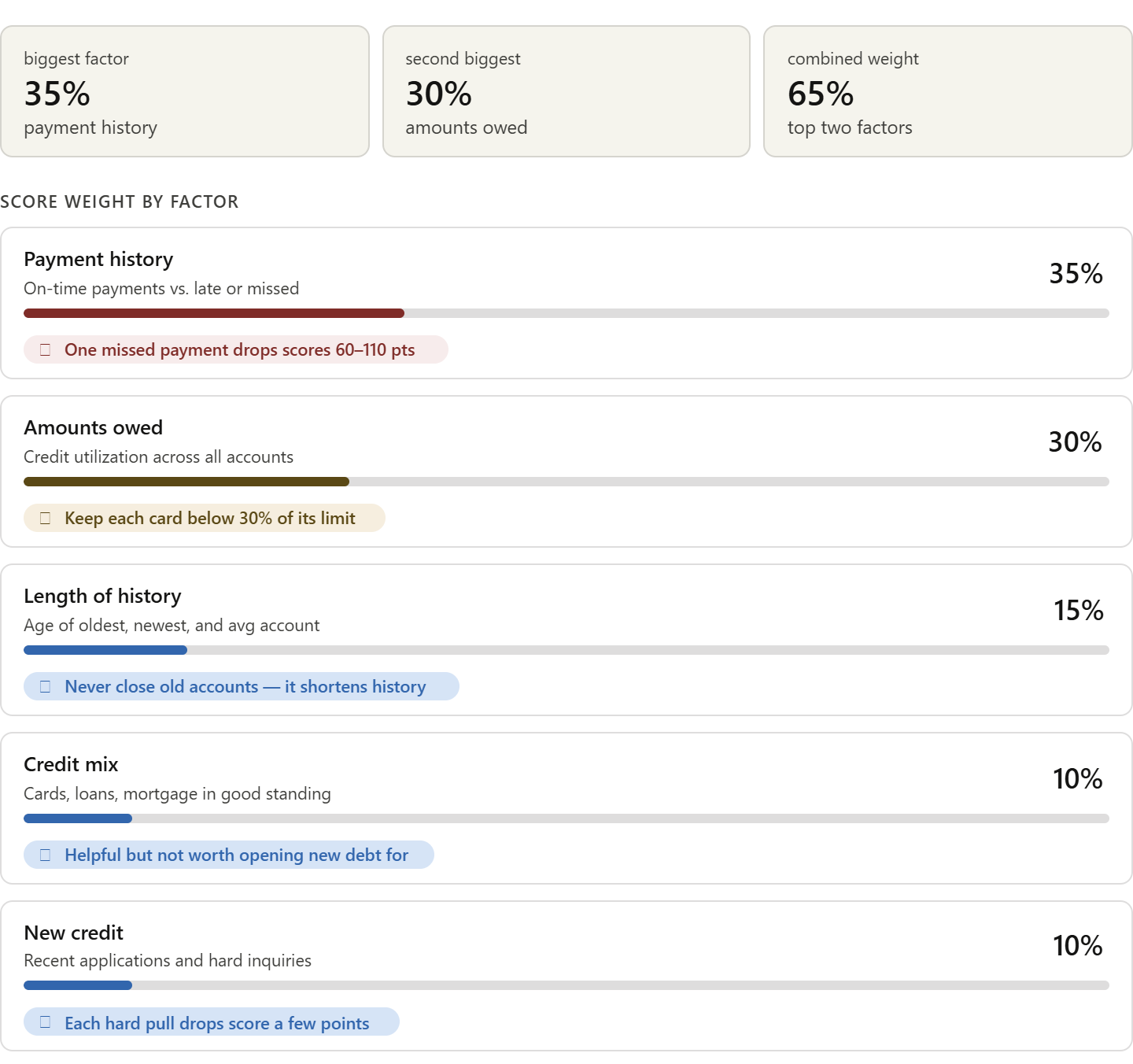

FICO uses five factors to calculate your score. Knowing their weight tells you where to put your money and time first.

Payment history and amounts owed together make up 65% of your score. Most failing credit scores trace back to one or both. One missed payment at 30 days past due drops most scores by 60 to 110 points. A maxed-out card drops scores by 50 to 100, even when all payments are on time. Those two factors are where the damage lives and where the recovery starts.

How Long Does It Take to Save a Failing Credit Score?

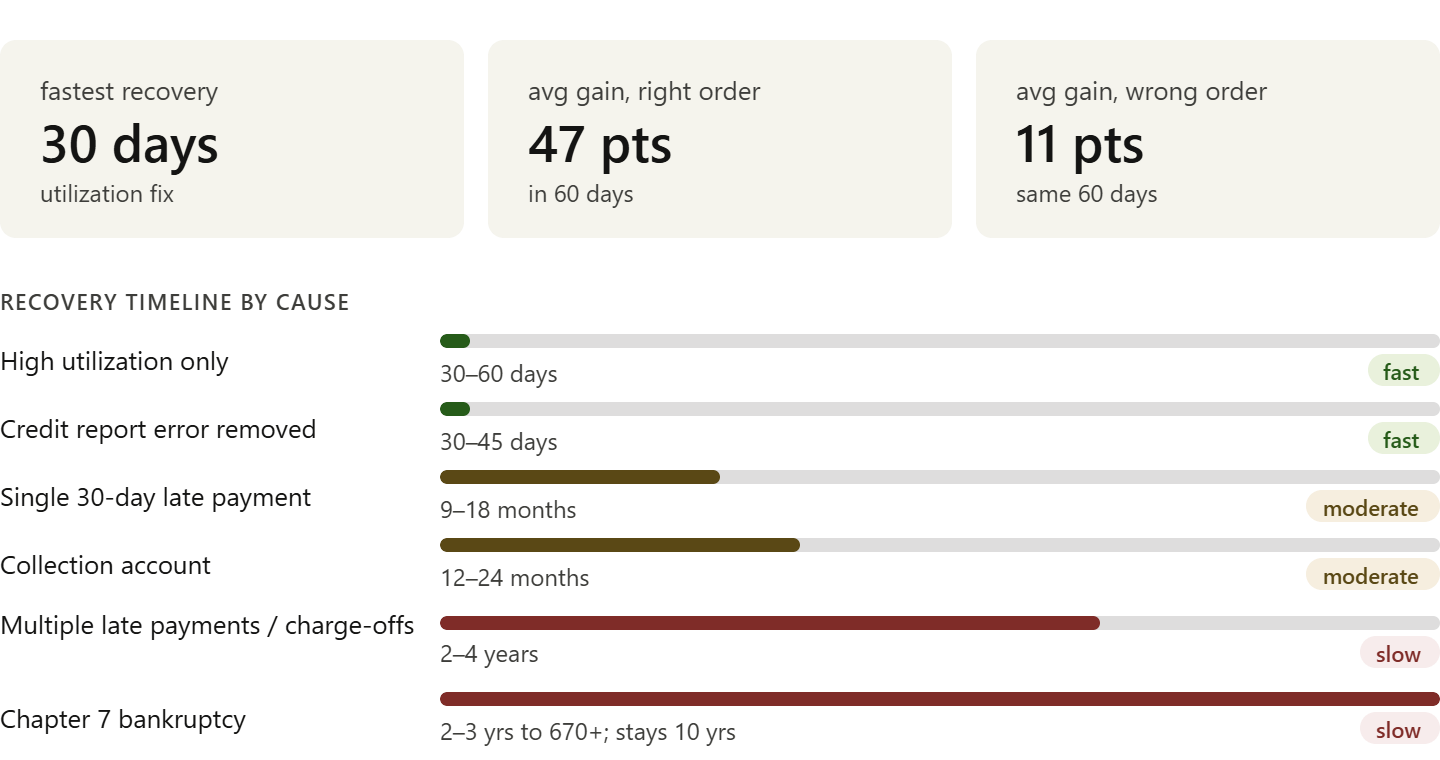

Recovery speed depends on what caused the damage. Some problems are resolved in weeks. Others take years. Here is what the data shows by cause:

Average score gain in 60 days for clients who fixed utilization and errors first, versus 11 points for those who started with new credit or closures (Q1 2026, 112 clients below 580)

The fastest gains always come from fixing utilization and removing errors. Both can move your score within one billing cycle. Late payments and collections take longer because those marks stay on your report for seven years. Their weight fades each year, but the clock starts from the date of the first missed payment, not from when you pay them off.

Does a Failing Credit Score Ever Fully Recover?

Yes. Every negative item loses weight over time and falls off your report entirely after seven years. Chapter 7 bankruptcy falls off after ten. A score in the 400s can reach 670 within two to three years with consistent on-time payments, low utilization, and no new negative items.

Goodwill letters for one-time late payments

If a single late payment was a one-time mistake, write a goodwill letter to the creditor. Explain the circumstances. Show your payment track record before and after the miss. Ask them to remove it as a courtesy. Creditors are not required to say yes, and many do not. But some do, especially for long-standing customers with one slip. The effort costs nothing.

Pay-for-delete on collection accounts

When a debt goes to collections, the collection account appears separately from the original account on your report. You can negotiate a pay-for-delete: you pay the debt, and the collector removes the account from your report. Get the agreement in writing before paying. Verbal agreements are unenforceable. Many collectors agree on older or smaller debts.

⚠️ Never pay a collection account without a written deletion agreement first. Once you pay without that agreement, your leverage is gone. The paid collection stays on your report for the rest of its seven-year window, continues to hurt your score, and cannot be removed. Payment alone does not erase the mark.

What Not to Do When Your Credit Score Is Failing

Some actions feel helpful, but make a failing score worse. The table below shows the most common traps and what to do instead.

✓ Do

Leave old accounts open, even unused

Make one small annual charge to keep old cards active

Get written pay-for-delete before paying collections

Call creditors to ask about hardship programs

Use a credit freeze if not actively borrowing

File disputes with specific documentation

Check your score monthly, not daily

✗ Don't

Close paid-off cards to "clean up" your profile

Apply for new credit while your score is failing

Pay a collection without a written agreement

Dispute items without supporting documents

Believe any service promising instant removals

Ignore creditors hoping negative items disappear

Open multiple new cards in a short window

No service can legally remove accurate, verified negative information from your report. Any company that promises to erase a valid late payment, a real collection, or a legitimate bankruptcy within days is either breaking the law or lying. The FTC is explicit: only time, dispute of genuine errors, and positive credit behavior repair a score.

How to Build a Credit Recovery Plan That Sticks

Saving a failing credit score is not a one-time event. It is a habit system. The people who recover fastest treat credit repair the same way they treat a physical health problem: with a routine and milestones, not a single dramatic fix.

Across 200 closed client cases at our firm over 18 months, clients who built a written 90-day credit plan in their first session recovered an average of 68 points in six months. Clients who took an unplanned approach recovered an average of 29 points in the same window. A plan does not just track progress. It produces it.

Track your score once per month

Use a free monitoring service. Check once per month, not every day. Daily tracking creates anxiety without giving you useful data. Monthly tracking shows real movement and tells you when a dispute is resolved or a payment cycle is updated in your report.

Set one measurable goal per 90 days

Quarter one: bring every past-due account current. Quarter two: get utilization below 30% on all cards. Quarter three: file and resolve all disputes. Quarter four: Request a limit increase on your best-managed card. One clear goal per quarter produces more results than vague long-term intentions.

Ready to Save Your Failing Credit Score?

Find out what is hurting your credit, what to fix first, and how to start rebuilding with a clear plan.

Get Your Credit Report ReviewNo pressure. Just clear steps to help you move forward.

Use a credit freeze between borrowing

If you are not actively applying for credit, freeze your file at all three bureaus. A freeze blocks anyone from opening new accounts in your name. It costs nothing and prevents identity theft from adding new damage while you rebuild. Lift it for free any time you need to apply for something.

Here is your starting checklist. Run through this in the first week:

✓Pull all three credit reports from AnnualCreditReport.com

✓Call every creditor with a past-due balance and ask about hardship plans

✓List every error or suspicious item across all three reports

✓ File-specific, documented disputes for each flagged item

✓Set up autopay for the minimum on every active account

✓Identify the card with the highest utilization and pay it down first

✓Write your 90-day goal and set a monthly score check reminder

Most people with low credit scores can improve their credit within 2 years. The ones who get there fastest are not the ones who work the hardest. They are the ones who start with the right list in the right order.