Learning how to start from bad credit is not about one big move. It is about doing several small things right, in the right order, every month.

Running a credit repair company, I have seen this situation hundreds of times. One case I always come back to is a woman who walked in with a 498 score, three collections, and two maxed-out cards. She thought her credit was beyond saving. Fourteen months later, her score crossed 680. She did not do anything dramatic. She just followed the right steps.

A thread on r/personalfinance sums it up well. A user posted with a 520 score and no idea where to start. The top reply had over 4,000 upvotes. The advice: pull your free credit report first, dispute any errors, then get a secured card. Simple. Actionable. It works.

The data backs this up. Experian reported that 15% of U.S. consumers now fall in the poor credit range as of 2025. That is roughly 1 in 7 American adults. If that is you, this guide is your starting point.

What "Bad Credit" Actually Means

Bad credit means a FICO score below 580. Scores between 580 and 669 fall in the "fair" range. The FICO scoring range runs from 300 to 850. A score in the mid to high 600s or above is generally considered good.

A low score tells lenders one thing: lending to you carries risk. That leads to higher interest rates, lower credit limits, and more denials.

Here is what a bad score costs you in real terms:

A mortgage with a 580 score can carry an interest rate 1.5% to 3% higher than one with a 740 score.

Auto lenders charge average APRs above 15% for scores under 600.

Some landlords reject rental applications below 620 outright.

Insurance premiums in many states rise when your credit score drops.

The good news is that bad credit is not permanent. Every factor that hurts your score is something you can influence over time.

How to Start From Bad Credit: Your First 3 Moves

1. Pull Your Free Credit Reports

Start here. Do not skip this step.

Go to AnnualCreditReport.com, the only site authorized by the federal government for free credit reports. Pull reports from all three bureaus: Equifax, Experian, and TransUnion.

Look for four things:

Accounts that do not belong to you

Late payments are marked incorrectly

Debts listed more than once

Accounts showing the wrong balance

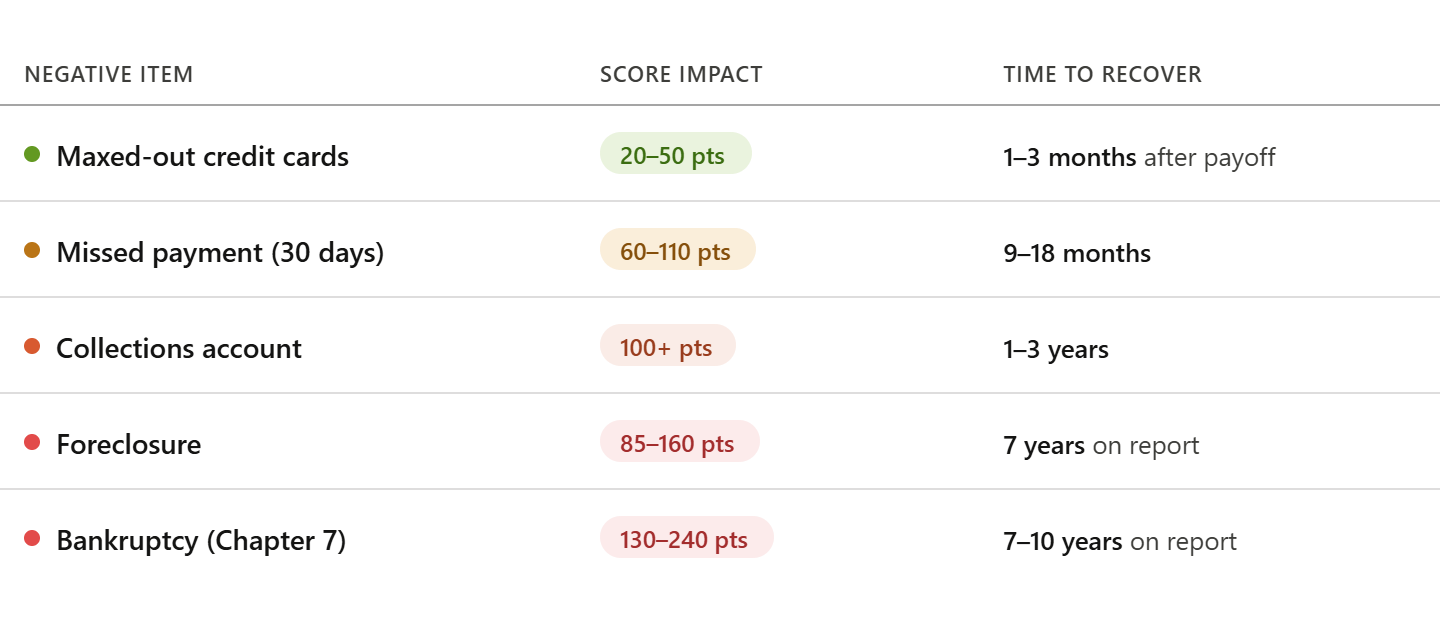

Errors are more common than most people think. Last year alone, our office helped 61 clients remove inaccurate negative items from their reports. Every single removal raised their score. In some cases by 40 to 80 points.

2. Dispute Errors in Writing

The Fair Credit Reporting Act gives you the right to dispute any item on your report. Send disputes directly to the credit bureau that listed the error.

Write a short, clear letter. State the account name, the error, and what you want corrected. Include a copy of the report with the item circled. Send it by certified mail.

Bureaus have 30 days to investigate and respond. If they cannot verify the item, they must remove it.

Do not use third-party dispute mills that promise fast results. Many charge high fees and use template letters that bureaus often ignore.

3. Open a Secured Credit Card

A secured credit card is the most direct tool for rebuilding credit from bad credit.

Here is how it works. You put down a cash deposit, usually $200 to $500. That deposit becomes your credit limit. You use the card for small purchases. You pay the full balance every month. The issuer reports your payments to all three bureaus.

Payment history is the most critical factor, and you may start to see improvements within 60 days if you use the secured credit card responsibly and make payments on time.

Top secured cards for bad credit rebuilding:

Discover it Secured reports to all three bureaus and earns 2% cash back at gas stations and restaurants.

Capital One Platinum Secured offers a path to upgrade to an unsecured card after six months of on-time payments.

OpenSky Secured Visa does not require a credit check at all, making it accessible at any score level.

Those first three moves set the foundation. Once they are in place, the next focus is your ongoing habits.

The Five Habits That Rebuild a Bad Credit Score

Pay On Time, Every Time

Payment history makes up 35% of your FICO score. It is the single largest factor.

One missed payment can drop your score by 60 to 110 points, depending on where you start. Set up autopay for the minimum on every account. Then manually pay the rest before the due date.

Keep Credit Utilization Below 30%

Credit utilization is the percentage of your available credit that you are using. If your limit is $1,000 and your balance is $400, your utilization is 40%. That hurts your score.

Keep balances below 30% of each card's limit. Below 10% is even better. This factor makes up 30% of your FICO score.

Experian data from 2025 shows that credit card utilization held steady at 29.1% for the average U.S. consumer. That 30% level is the exact point at which utilization begins to have a greater negative effect on scores.

In practice, our office sees the biggest score jumps when clients pay balances down from above 50% to below 20%. The change can show up in the next billing cycle.

Do Not Apply for Multiple Cards at Once

Every credit application triggers a hard inquiry. Hard inquiries stay on your report for two years. Each one can cost you five to ten points.

Space out applications by at least six months. Apply only when you are confident you will be approved.

Do Not Close Old Accounts

Credit history length makes up 15% of your FICO score. Closing an old account shortens your average history and reduces your total available credit. Both actions lower your score.

Keep old accounts open, even if you rarely use them. Make one small purchase every few months to keep them active.

Add an Installment Loan to Your Mix

Credit mix accounts for 10% of your FICO score. Bureaus reward borrowers who manage both revolving credit (cards) and installment loans (personal loans, auto loans, credit-builder loans).

A credit-builder loan is the lowest-risk way to add an installment account. Self Financial and many credit unions offer them. You make monthly payments and receive the loan amount at the end of the term. The payment history reports to all three bureaus.

How Long Does It Take to Rebuild Bad Credit?

The timeline depends on what caused the damage.

Most clients in our office who follow all five habits see their first 50-point gain within three to six months. Getting from a 580 to a 680 typically takes 12 to 18 months of consistent work.

Should You Hire a Credit Repair Company?

A credit repair company can help, but only with specific tasks.

Legitimate services dispute inaccurate or unverifiable items on your behalf. They understand credit law and know how to communicate with bureaus. They can also help you track progress across all three reports.

What no company can do: remove accurate, verified negative information. Any company promising to wipe your report clean is misleading you.

Under the Credit Repair Organizations Act (CROA), credit repair companies must give you a written contract, cannot charge you before services are delivered, and must tell you about your right to dispute items yourself for free.

If a company asks you to pay up front before doing any work, walk away.

What Not to Do When Starting From Bad Credit

Rebuilding credit from bad credit takes patience. These mistakes slow the process down or reverse progress.

Do not pay a collection just to pay it. Ask for a pay-for-delete agreement first. Get it in writing.

Do not apply for every secured card you see. Many come with high annual fees and low limits.

Do not sign up for credit repair services that charge monthly fees for things you can do yourself.

Do not ignore accounts in collections. Unpaid collections keep hurting you until they age off or are removed.

Do not use a debit card to build credit. Debit activity never reports to the bureaus.

Ready to Start Rebuilding Your Credit?

Bad credit does not have to control your next approval. Get a clear credit review, find the negative items holding you back, and start building a better score step by step.

Get Your Free Credit Report ReviewStart with your report. Then build your plan.

How to Start From Bad Credit After a Major Financial Event

After Bankruptcy

Bankruptcy stays on your credit report for seven years (Chapter 13) or ten years (Chapter 7). But you can start rebuilding the day your case is discharged.

Open a secured card immediately. Your score will start to recover faster than most people expect. Many clients reach 620 within 18 to 24 months post-discharge by staying consistent.

After Collections

Pay or settle the collection account. Then send a pay-for-delete letter asking the collector to remove the item from your report in exchange for payment. Not all collectors agree, but many do.

After Identity Theft

Place a fraud alert or credit freeze at all three bureaus right away. Then dispute every fraudulent account in writing. Under the FCRA, bureaus must block fraudulent information once you provide an identity theft report from IdentityTheft.gov, a federal resource run by the FTC.

Starting with bad credit feels overwhelming at the beginning. But the path is clear. Pull your reports. Fix the errors. Open a secured card. Pay on time. Keep balances low. Repeat every month.

Experian data confirms that 70% of U.S. consumers now hold a good or better score of 670 or higher. Most of them were not born there. They built it, one on-time payment at a time.