How Fast Can I Increase a 400 Credit Score?

Table of Contents

- Why credit repair timelines exist before you take action

- The 30-60-90 day framework that actually moves scores

- Actions that compound versus actions that expire

- Where this leaves credit repair in 2026

Credit improvement happens before traditional advice takes effect. See which moves create momentum in weeks, not years.

Can I raise my 400 credit score?

How the question form is wrong…

Most people ask, "How fast can I fix my credit score?" only after a credit or loan denial.

A loan rejection. A rental application that goes nowhere. A credit card decline at checkout.

By the time the question feels urgent, the opportunity to build momentum gradually has already passed.

In 2026, credit decisions happen instantly through automated systems that weigh dozens of data points beyond your score. By the time you're searching for quick fixes, the narrative around your creditworthiness has already been written by months or years of reporting history.

This creates a problem for how credit repair is typically approached.

Most advice focuses on what's possible in theory, not what moves scores in practice. Articles promise "boost your score 100 points" without explaining that some accounts take 30 days just to report changes, or that dispute investigations can take 45 days before you see movement.

The result is unrealistic timelines, wasted effort on low-impact actions, and frustration when scores don't jump as promised.

A 400 credit score sits in "poor" territory. It reflects serious delinquencies, collections, or high utilization that won't disappear overnight.

But movement is possible faster than most people expect if you understand which actions create momentum and which just create activity.

This article breaks down realistic timelines for credit improvement and focuses on what actually moves a 400 score in the first 90 days.

Recommended Content: Navigating the Impact of a 400 Credit Score and Strategies for Improvement

Why credit repair timelines exist before you take action

Understanding that a 400 score can improve is only the first step.

The real challenge is not whether improvement is possible. It's knowing which actions move scores quickly and which take months to register.

This is where most credit repair attempts stall.

People dispute everything, hoping something sticks, pay off collections expecting instant score jumps, or open new credit without understanding the utilization impact.

There is a better sequence: understand how credit bureaus process changes and time your actions to create visible momentum within billing cycles.

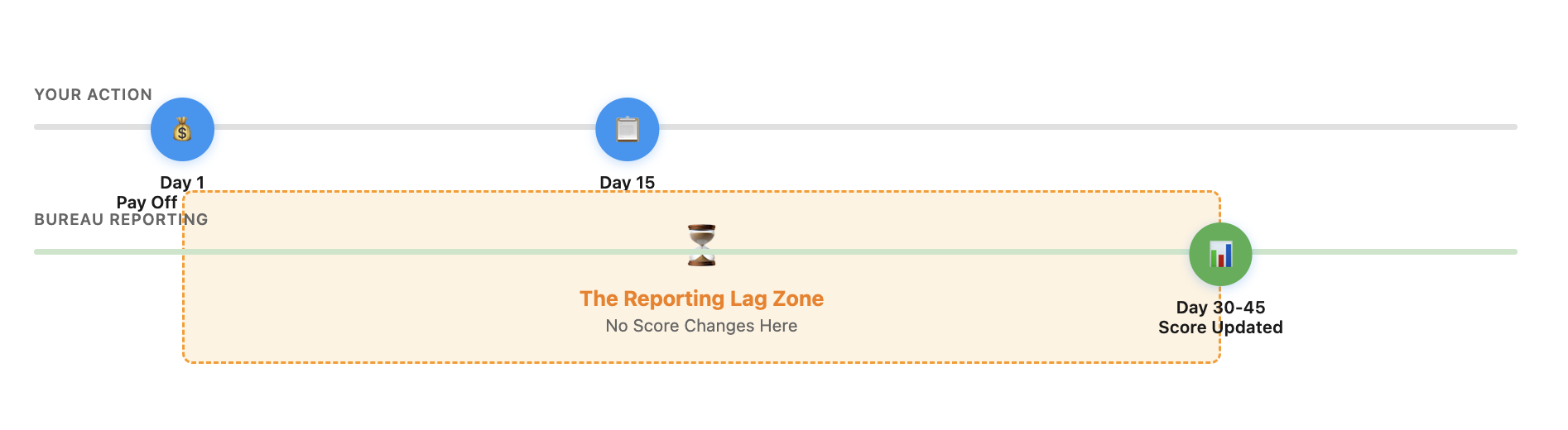

Credit scores update in cycles, not real-time

Once you take action on your credit, nothing happens immediately.

Creditors report to bureaus monthly, usually around your statement closing date. Changes made mid-cycle won't show up until the next report. Disputes take 30-45 days to investigate. Paid collections may not improve scores at all if you're using older FICO models.

You're looking for actions that trigger updates quickly:

- Paying down credit card balances below 30% utilization before your statement closes.

- Becoming an authorized user on an account with a perfect payment history and low utilization.

- Disputing inaccurate negative items that bureaus can't verify within 30 days.

- Removing recent late payments through goodwill letters if the account is otherwise current.

These moves work because they either change what's reported next cycle or remove items that bureaus can't validate.

The 30-60-90 day reality

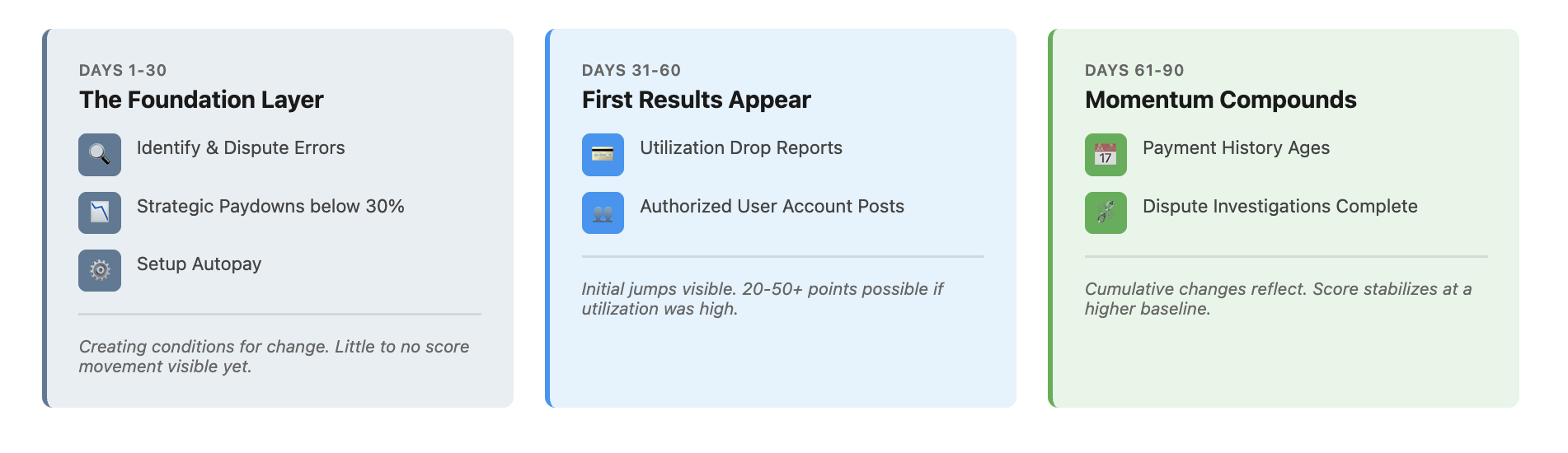

After starting credit repair from 400, visible movement follows a predictable pattern.

Days 1-30: You're setting up the foundation.

Request credit reports from all three bureaus. Identify what's actually hurting your score, collections, charge-offs, high utilization, recent late payments, or a mix. Dispute obvious errors. Pay down credit card balances strategically.

Nothing shows up on your score yet. You're creating the conditions for change.

Days 31-60: First updates start appearing.

If you paid down high utilization, that reports and your score jumps, sometimes 20-50 points if utilization was severely high. Authorized user accounts may post. Some disputes complete and inaccurate items disappear.

This is when you see whether your actions are working.

Days 61-90: Momentum either compounds or stalls.

Additional disputes resolve. Payment history starts improving if you're staying current. New positive accounts begin aging. Your score reflects cumulative changes, not just individual fixes.

That is realistic progress.

Rethinking what "fast" actually means

This is where expectations shift.

Instead of asking "can I jump from 400 to 650 in 30 days?" the better question is "what score can I reach in 90 days with strategic action?"

If disputes remove multiple collections or charge-offs:

- You might see 60-100 point gains as negative items disappear.

If high utilization was your main problem:

- Dropping from 90% to 10% utilization can add 40-80 points within one reporting cycle.

If your report is accurate but severely damaged:

- Expect slower progress. Adding positive payment history takes time to outweigh serious negatives.

In this model, "fast" means 60-90 days for meaningful movement, not overnight miracles.

Credit repair is the compounding layer, not the instant fix.

Good Read: How Fast Can I Increase a 450 Credit Score?

Actions that compound versus actions that expire

Most traditional credit repair advice still works, but not exactly as you expect it to be.

Below are some scenarios:

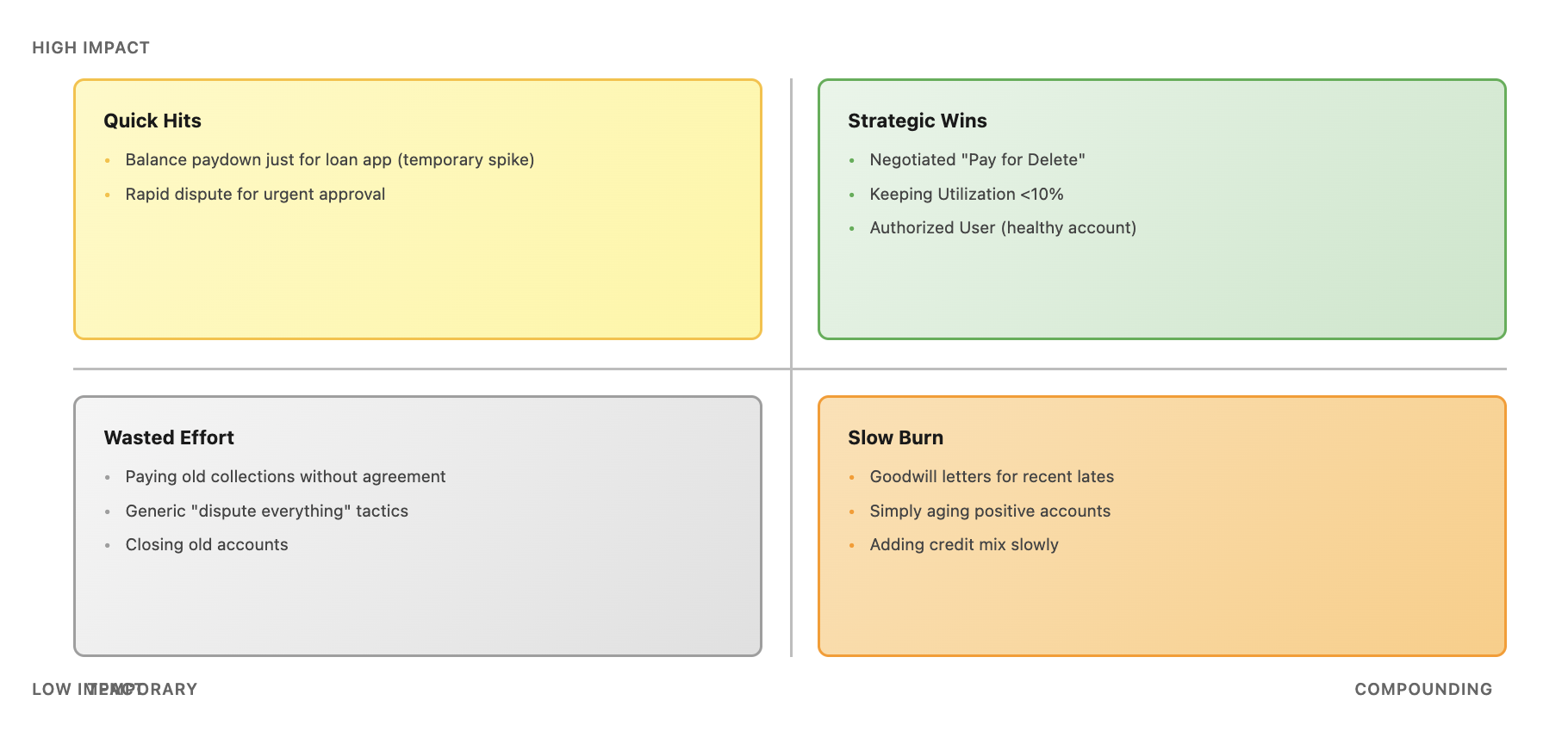

Someone reads that paying collections helps. They pay everything immediately. Their score barely moves or actually drops. Why? Because they acknowledge the debt and it’s a negative item that sticks on their record for years.

They dispute negative items randomly. Some get removed temporarily, then reappear 60 days later when the creditor provides verification.

They open new credit hoping to dilute their bad credit history. Instead, hard inquiries ding their score, and low credit limits barely help utilization math.

The result is wasted money, minimal score improvement, and confusion about what actually works.

Strategic credit repair makes it possible to reverse that dynamic by focusing on actions that create lasting momentum, not temporary activity.

Why compounding actions outperform quick fixes

When a credit action creates one-time movement, it helps once. When it creates compounding improvement, it helps every month going forward.

Focus on actions where:

- The benefit increases over time rather than disappearing.

- One improvement enables another.

- Your score improves even if you take no additional action.

This is the point where credit repair shifts from chasing points to building creditworthiness.

The difference is mechanical

Instead of "pay off all collections immediately," the strategic approach considers:

Paying collections might not raise your score at all. This is especially true if you're using FICO 8 or earlier models, which still count paid collections as negative. Newer models ignore them, but most lenders still use older scoring.

Better move: Negotiate "pay for delete" agreements in writing before paying. If the collector won't agree, paying does nothing for your score with most lenders.

Instead of "dispute everything and see what sticks," you focus on:

Inaccurate information that can't be verified. Wrong account details, incorrect dates, or outdated information. These disputes often succeed because creditors can't validate bad data.

Better move: Dispute strategically with specific documentation showing why the item is wrong. Generic disputes get generic responses.

Instead of "open new credit cards to improve your mix," consider:

Opening new credit when you have a 400 score usually means high-fee cards with low limits that barely help and can tempt overspending.

Better move: Become an authorized user on someone else's established account with perfect history. You get the benefit without the hard inquiry or temptation.

This approach compounds because each action either removes lasting damage or adds reporting that improves monthly.

Credit score Improvement is not the end

Improving your score to 550 or 600 is not the finish line.

You need a clear plan to maintain momentum and avoid falling back into behaviors that tanked your score originally.

For ongoing improvement, that means:

- Setting up autopay so you never miss payments going forward.

- Keeping utilization below 10% on revolving accounts.

- Letting positive history age rather than opening unnecessary new accounts.

- Monitoring your reports quarterly to catch errors before they compound.

With a strategic approach, credit repair stops being a one-time project and starts acting as a lasting financial foundation, one that opens access to better loans, lower insurance rates, and housing opportunities.

Where this leaves credit repair in 2026

A 400 credit score does not improve in days.

It develops across weeks and months as changes report, disputes resolve, and positive behaviors accumulate.

Realistic timelines help set expectations. Strategic action determines how much movement happens within those timelines. Understanding what compounds versus what expires keeps you from wasting time on moves that don't matter.

In this model, credit repair is the layer that turns damaged credit into rebuilding momentum across 90 days, six months, and beyond.

Credit scores no longer need to feel permanent. The people who act on that reality will see meaningful improvement faster than those still chasing overnight miracles.