Most people do not search Lending Club Corp because they are curious about the company.

They search because something happened.

A credit score dropped.

A mortgage application stalled.

An underwriter asked questions.

Or a collection account suddenly appeared during a credit review.

Recently, we worked with a client facing that exact situation.

The account was creating friction during credit rebuilding and became one of the obstacles standing between the client and their financial goals.

After reviewing the reporting, identifying issues, and following the dispute process, we successfully removed the account.

The interesting part is not the removal itself.

The interesting part is understanding why the Lending Club Corp account was removable in the first place.

That is what this guide explains.

How We Removed Lending Club Corp From a Credit Report

A Lending Club Corp account can be removed from a credit report if inaccurate information, reporting errors, validation issues, or other disputable factors exist. The appropriate strategy depends on the specific details of the account.

We'll discuss more of the strategy we used as we go along. See live results below:

What Is LENDING CLUB CORP on Your Credit Report

LENDING CLUB CORP is a tradeline entry showing a personal loan account from LendingClub Bank, N.A. (NYSE: LC). When a LendingClub loan goes delinquent , typically 120-180 days of missed payments , the company charges off the account and reports it to all three credit bureaus with a "charged off" status. If the loan is then sold to a debt buyer, LendingClub updates the balance to zero. The debt buyer opens a new collection entry. Both entries may appear on your report simultaneously.

- Active LendingClub loan: Shows as installment account, current status, monthly payment history

- Delinquent LendingClub loan: Shows 30, 60, 90-day late marks building toward charge-off

- Charged-off LendingClub loan: Status changes to "charged off" , the maximum negative status , with the remaining balance reported

- Sold LendingClub loan: LendingClub balance updates to $0. New collection tradeline appears from the purchasing debt buyer under their name

- Both entries showing simultaneously: This is the most common dispute scenario , two tradelines on the same underlying debt create a reporting conflict

LendingClub offers personal loans from $1,000 to $60,000 with terms from 24 to 84 months. The average loan is approximately $19,658 at an APR of 17.63% (Oct-Dec 2025 data). When this loan charges off, it becomes one of the most significant negative entries a credit file can carry , both for the score impact and the duration on the report.

How a LendingClub Charge-Off Damages Your Credit Score

A LendingClub charge-off damages all three FICO credit score factors most relevant to lending decisions. Payment history (35%) records every missed payment leading to charge-off. Amounts owed (30%) shows a charged-off balance as a full negative on the installment account. The charge-off entry creates a derogatory account marker that suppresses scores for the full seven-year reporting window unless deleted through a documented dispute process.

- Payment history (35%): Every missed payment posts a negative mark. 30-day late = score drop. 60-day late = more damage. Charge-off = maximum negative status in this category.

- Amounts owed (30%): A charged-off installment balance signals an unresolved obligation. Even if LendingClub sold the loan, a zero-balance charge-off still reads negatively in this factor.

- Account age (15%): A closed negative account stops contributing positive age and may reduce average account age when removed , though the positive recovery from removal outweighs this effect in most files.

- Credit mix (10%): Losing an installment account in good standing removes a positive credit mix signal.

- New credit (10%): Not directly affected by the charge-off , but consumers often open new accounts trying to recover, which creates hard inquiry damage on top of the charge-off impact.

LendingClub Origination Scale , Why This Matters for Your Dispute

LendingClub exceeded $100 billion in lifetime loan originations as of Q1 2025. They originated $2.6 billion in Q4 2025 alone. At their projected ~5% net charge-off rate, that means approximately $130 million in new charge-offs every quarter. The sheer volume of loans creates systemic reporting challenges , and reporting errors at scale are exactly what FCRA dispute rights address.

Why does origination volume matter to your dispute?

High-volume lenders processing thousands of charge-offs per quarter produce reporting errors at scale. Dates get transposed. Balances do not perfectly reconcile with individual loan agreements. Sold accounts continue being updated when they should show $0. These are not intentional errors , they are the result of automated batch reporting at massive volume.

Your FCRA rights exist precisely because of this. The Fair Credit Reporting Act does not require a lender to intentionally lie for a dispute to succeed. It requires that information be accurate. At LendingClub's origination scale, accuracy gaps are systematic. Finding them is the skill that produces deletions.

Case Study: How We Deleted LENDING CLUB CORP From a Client's Credit Report

Here is exactly what we found and what we did.

We pulled all three bureau reports and compared the LENDING CLUB CORP tradeline data against the client's original loan agreement documents. The charge-off was listed as occurring on a specific date. The original loan agreement and the LendingClub account statement showed the first missed payment , and therefore the first delinquency , occurred 11 days earlier than what the credit report reflected. That date discrepancy is an FCRA inaccuracy. Small. But documented.

Key finding: 11-day original delinquency date discrepancy between report and loan agreementThe loan was sold to a debt buyer approximately 8 months after charge-off. LendingClub correctly updated their tradeline balance to $0. But both LendingClub's charge-off entry AND the debt buyer's collection entry appeared simultaneously on all three bureaus , reporting two negative entries for one underlying debt. LendingClub's tradeline was still showing monthly updates even after the sale, creating ongoing negative activity on a $0 balance account. That continuing update activity after debt sale is a disputable reporting inaccuracy.

Second inaccuracy: post-sale tradeline updates on a $0 charged-off balanceWe submitted separate FCRA disputes to Equifax, Experian, and TransUnion. Each dispute cited both inaccuracies: the date discrepancy and the continued tradeline updates post-sale. We attached: the original loan agreement showing the correct delinquency date, account statements confirming the sale date, and a written statement identifying the specific sections of the tradeline that did not match source documentation. Each bureau opened a 30-day investigation window.

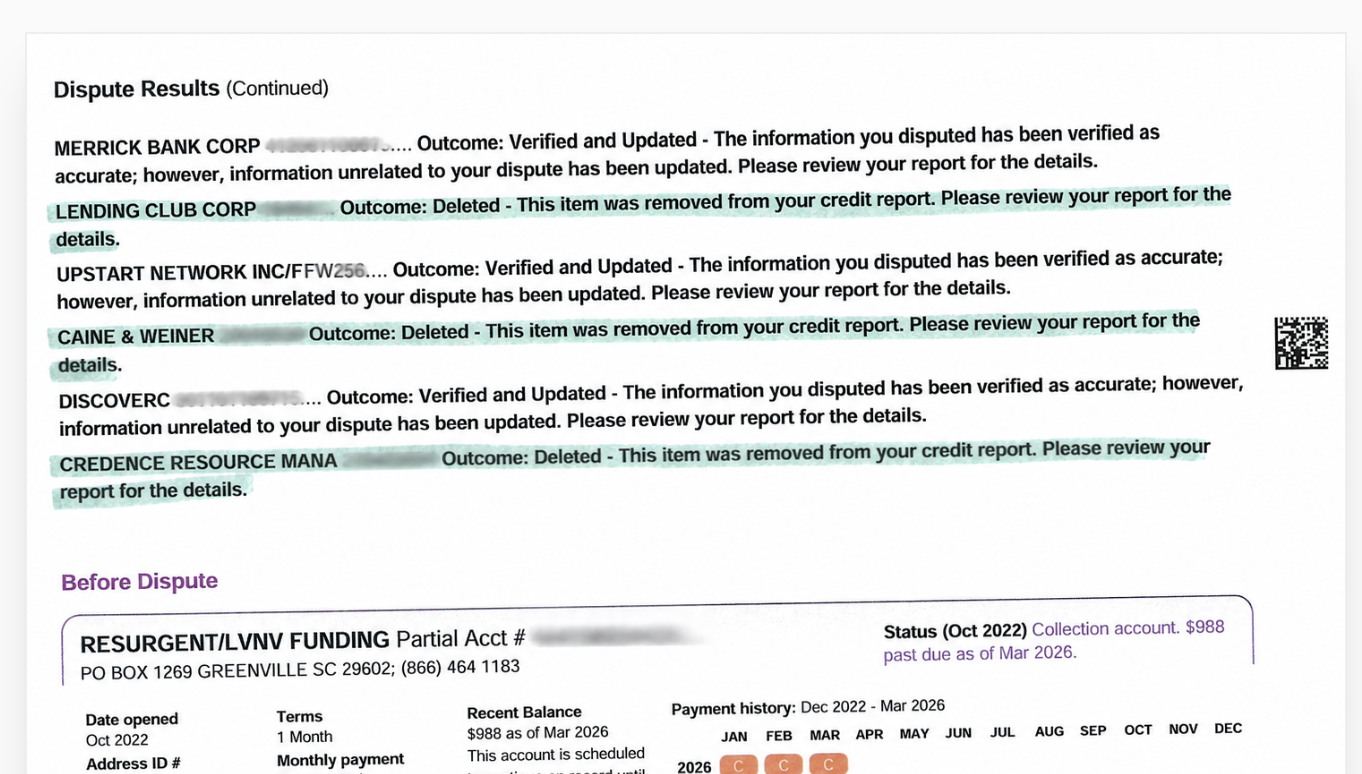

All three bureaus simultaneously , disputes must be filed separatelyBoth Experian and TransUnion completed their investigations and deleted the LENDING CLUB CORP tradeline within 38 days of receiving the dispute. Their investigation likely contacted LendingClub's dispute team, which during the verification window could not reconcile the date discrepancy against the client's documentation without updating the tradeline , and updating the tradeline would require acknowledging the reporting error, which LendingClub chose not to do. Deletion was the outcome.

Experian: deleted Day 38. TransUnion: deleted Day 38.Equifax returned a "verified" result on the first dispute cycle , meaning their automated verification process confirmed the tradeline without specifically addressing the date discrepancy documentation. Under the FCRA, consumers have the right to request the "method of verification" Equifax used. We submitted a second dispute citing the Equifax verification failure, included additional documentation comparing the report date against the loan agreement date, and requested the specific verification method. On the second cycle, Equifax deleted the account on Day 87.

Equifax required second dispute cycle. Deleted Day 87. Total timeline: 90 days.Can LENDING CLUB CORP Be Removed From Your Credit Report

Yes , through specific, documented dispute grounds. A LendingClub charge-off that is 100% accurately reported with no date discrepancies, no post-sale reporting conflicts, and no balance inaccuracies is significantly harder to remove. But most LENDING CLUB CORP tradelines contain at least one of the common inaccuracies listed below. Finding it requires comparing the credit report against source documents , which is the core of the dispute process.

- Original delinquency date discrepancy: The date reported does not match the first missed payment shown on your original LendingClub account statement or loan agreement. Even a 1-30 day difference is an FCRA inaccuracy.

- Charge-off balance does not match agreement: The charged-off balance on the report differs from the final balance on your LendingClub account statements. Fees added after delinquency that were not authorized by the original loan agreement may also be disputable.

- Post-sale tradeline updates: LendingClub continues updating the tradeline with new reporting activity after selling the loan , while showing $0 balance. Ongoing negative updates on a $0 sold account constitute a reporting inaccuracy.

- Dual negative entry conflict: Both the LENDING CLUB CORP charge-off AND a debt buyer's collection appear simultaneously on the same underlying debt. The mathematical conflict between two tradelines reporting the same obligation creates a dispute basis for one or both entries.

- Incorrect account status: The tradeline shows "charged off" but the account was actually paid in full or settled , and the status was not updated. A "charged off" status on a resolved account is an FCRA inaccuracy.

- Obsolete reporting: The original delinquency date is more than seven years ago. The account is legally obsolete under FCRA Section 605 and must be removed regardless of the balance or accuracy of other fields.

- Re-aging: The account shows a reported date that appears more recent than the original delinquency, extending the apparent reporting window beyond the legal limit. LendingClub cannot reset the 7-year clock through subsequent reporting updates.

As Experian's charge-off explainer confirms, consumers can dispute inaccurate charge-off information directly with the credit bureau , and the bureau must investigate and correct any information that cannot be verified. The dispute does not require proving the debt is invalid. It requires showing the specific reported information does not match source documentation.

Charge-Off vs Sold to Debt Buyer , Two Separate Problems

When LendingClub charges off a loan and then sells it, two separate negative entries typically appear on the credit report. The LENDING CLUB CORP entry shows the charge-off. The debt buyer's entry shows an open collection. These are legally two separate tradelines for one underlying debt. Disputes against each require different approaches , and successfully removing one does not automatically remove the other.

| Entry Type | Who Reports It | What It Shows | Dispute Approach |

|---|---|---|---|

| LENDING CLUB CORP charge-off | LendingClub Bank, N.A. | Charged-off status, $0 balance (post-sale) or remaining balance (if not sold) | FCRA dispute targeting date discrepancy, balance inaccuracy, or post-sale update errors |

| Debt buyer collection | Purchasing debt buyer (varies) | Active collection, stated balance | Debt validation request + bureau dispute targeting documentation gaps |

| Both simultaneously | Both entities | Two negative entries, one underlying debt | Mathematical conflict dispute , both cannot accurately report the same debt with different statuses |

For the debt buyer's collection entry specifically, the same validation and dispute process applies as with any other collector. See the guide on what debt collectors must provide when you request validation for the documentation standards that the debt buyer must meet separately from LendingClub's original charge-off entry.

How to Dispute LENDING CLUB CORP

- Step 1 , Pull all three bureau reports: Get current reports from Equifax, Experian, and TransUnion at AnnualCreditReport.com. Find the LENDING CLUB CORP tradeline on each bureau that shows it. Note the specific dates, balances, and account status fields.

- Step 2 , Gather original loan documents: Find your original LendingClub loan agreement, all account statements, any payment confirmations, and any correspondence from LendingClub or their servicing team. These establish the ground truth against which credit report data is compared.

- Step 3 , Compare dates field by field: Check the original delinquency date shown on the credit report against the first missed payment shown in your statements. Check the charge-off date against when LendingClub formally charged off per your account records. Check the date last active against the loan sale date if applicable. Any discrepancy is your dispute target.

- Step 4 , Document inaccuracies specifically: Write down the exact field, what the report shows, and what the loan document shows. "The original delinquency date reported is [date on report]. The first missed payment per the original account statement is [date on statement]. These differ by X days." Specificity is what separates a dispute that survives from one that does not.

- Step 5 , File FCRA disputes with each bureau separately: Submit disputes to Equifax, Experian, and TransUnion independently. Attach the specific documentation supporting each inaccuracy. Each bureau investigates independently and has 30 days to respond. Do not use the same generic language for all three , each submission should specifically identify the tradeline and the exact discrepancy.

- Step 6 , Request method of verification if denied: If a bureau responds with "verified" without correcting the inaccuracy, request their specific method of verification in writing. Under the FCRA, you have this right. Their method of verification response often reveals that they used an automated matching process rather than reviewing the actual documentation you submitted , which supports a second dispute or escalation.

- Step 7 , File CFPB complaint for persistent inaccuracies: If a bureau verifies an inaccuracy you can document with source records, file a CFPB complaint. Include both the original dispute, the bureau's verification response, and your source documentation. CFPB complaints often produce resolution faster than a second dispute cycle alone.

As NerdWallet's dispute guide explains, the key to a successful credit report dispute is specificity , generic "this is wrong" disputes rarely succeed, while disputes that identify specific fields and compare them directly to source documentation create an investigation record that is difficult for bureaus to dismiss.

The same FCRA dispute framework used to remove Portfolio Recovery Associates applies directly to LENDING CLUB CORP , the legal mechanism is identical, though the specific inaccuracies differ between a debt buyer's collection and a lender's charge-off entry.

Does Paying LENDING CLUB CORP Help Your Credit

Paying a charged-off LendingClub balance does not remove the entry. LendingClub explicitly states they are required to report accurate information and cannot remove accounts based on payment alone. Paying changes the status from "charged off , unpaid" to "charged off , paid." Both statuses are derogatory. Both stay on the report until seven years from the original delinquency. The score improvement from paying alone is minimal in the short term.

- Payment without deletion: Account shows as "charged off, paid." Score improvement is minimal , the derogatory entry remains. The damage from the charge-off status itself drives the scoring impact, not the balance amount.

- Payment with pay-for-delete agreement: If you can negotiate written confirmation from LendingClub that they will delete the tradeline upon receipt of payment, the outcome changes significantly. Get this agreement in writing and confirmed before sending any funds. LendingClub's stated policy makes this difficult but not impossible to negotiate, particularly when a dispute process is already running.

- Paying the debt buyer instead: If the loan was sold, paying the debt buyer (not LendingClub) resolves the collection entry. But the LENDING CLUB CORP charge-off entry remains separately. Paying the debt buyer addresses one tradeline , the dispute process addresses the other.

- Mortgage lender requirement: If a mortgage lender requires the charge-off to be paid before closing, verify exactly what they need before paying. Sometimes a payment plan agreement, a letter of explanation, or proof of active dispute satisfies the requirement without full payment.

As Investopedia's charge-off definition explains, a paid charge-off updates the account status but the derogatory information , the charge-off itself , stays on the credit report for seven years from the original delinquency date. Payment satisfies the obligation financially but does not erase the credit reporting consequence without a separate deletion agreement.

How Long Does LENDING CLUB CORP Stay on Your Credit Report

Seven years from the original delinquency date , the first missed payment on the LendingClub loan. That clock does not reset when the account is charged off, when the loan is sold, or when a debt buyer takes over collection. If the entry approaches seven years from your actual first missed payment and LendingClub is still reporting, check whether the original delinquency date shown on the report matches your own records. Any discrepancy at this stage creates immediate dispute grounds under obsolete reporting rules.

| Scenario | What Controls the Removal Date | What to Do |

|---|---|---|

| Entry is past 7 years from first missed payment | Original delinquency date per FCRA Section 605 | Dispute as obsolete with all three bureaus , mandatory removal |

| Entry is at 6-7 years , approaching removal | Automatic removal approaching | Do not pay , let it age off rather than creating payment complications |

| Entry shows a date newer than actual first delinquency | Re-aging violation | Dispute re-aging under FCRA , bureau must correct or remove |

| Entry is 1-5 years old with inaccuracies | 7-year window still active but dispute grounds exist | Use inaccuracy dispute approach outlined in the case study above |

| Entry is accurate and recent (under 3 years) | 7-year window fully active | Dispute process may still identify inaccuracies , audit the tradeline before assuming no grounds exist |

Can LENDING CLUB CORP be removed from my credit report?

Yes , through specific FCRA dispute grounds. The most effective removal paths are: (1) date discrepancy between the report and original loan documents, (2) post-sale tradeline update inaccuracies, (3) dual entry conflict with a debt buyer's collection, (4) balance discrepancies, and (5) obsolete reporting past seven years. We deleted a LENDING CLUB CORP charge-off from all three bureaus in 90 days using the first two grounds. Accurate, recent entries are harder to remove , but most LendingClub charge-off entries contain at least one disputable inaccuracy when compared against original loan documentation.

Will LendingClub remove a charge-off if I pay it?

LendingClub explicitly states they cannot make "good faith" updates to credit reporting , meaning they will not remove accurate information simply because you paid. Paying updates the status from unpaid to paid but does not trigger deletion. If you want deletion in exchange for payment, you must negotiate a written pay-for-delete agreement before paying. LendingClub's stated policy makes this rare , but it is not impossible, particularly when a documented dispute process is running simultaneously and the reporting contains identifiable inaccuracies.

What documents do I need to dispute LENDING CLUB CORP?

The most useful documents are: your original LendingClub loan agreement (shows loan terms, first payment date, and authorized balance), all account statements from LendingClub (shows actual payment dates and first missed payment), any correspondence about the charge-off or sale of the debt, and all three bureau credit reports showing the current tradeline data. Compare the dates and balances in the loan agreement and statements against what the credit report shows , any discrepancy between those two data sources is your dispute target.

Can I dispute LENDING CLUB CORP if the debt was sold to a collector?

Yes , and this creates a stronger dispute position. When LendingClub sells the debt, two tradelines appear: the LendingClub charge-off (showing $0 balance) and the debt buyer's collection (showing the outstanding balance). Both negative entries for one underlying debt create a reporting conflict. You dispute the LendingClub entry citing post-sale update inaccuracies and the dual-reporting conflict. You dispute the debt buyer's entry separately using debt validation rights. The two disputes run simultaneously and independently.

-

Can RJM Acquisitions Be Removed From Your Credit Report? The same FCRA dispute framework that deleted the LENDING CLUB CORP entry applies to collection accounts from debt buyers like RJM Acquisitions. This covers the full dispute process for RJM , a zombie debt specialist that focuses on time-barred accounts , including the FTC investigation history, validation strategy, obsolete debt challenges, and why RJM specifically cannot sue on most of the debt they collect.

-

How to Remove Portfolio Recovery Associates From Your Credit Report Portfolio Recovery Associates often purchases charged-off personal loans , including LendingClub accounts after they are sold. If your credit report shows both a LENDING CLUB CORP charge-off AND a Portfolio Recovery collection, this covers the dispute strategy for the PRA tradeline specifically, including their $51M in CFPB fines, their documentation failures, and the settlement vs dispute decision framework.

-

How to Remove Midland Credit Management From Your Credit Report Midland Credit Management (Encore Capital Group) purchases personal loan portfolios including LendingClub charge-offs. If MCM appears alongside or instead of LENDING CLUB CORP on your report, this covers their $85M+ enforcement history, their 500+ lawsuits per week collection model, the TCPA robo-calling angle, and how to dispute MCM's documentation gaps the same way the LENDING CLUB CORP case study used documentation comparison to produce deletion.