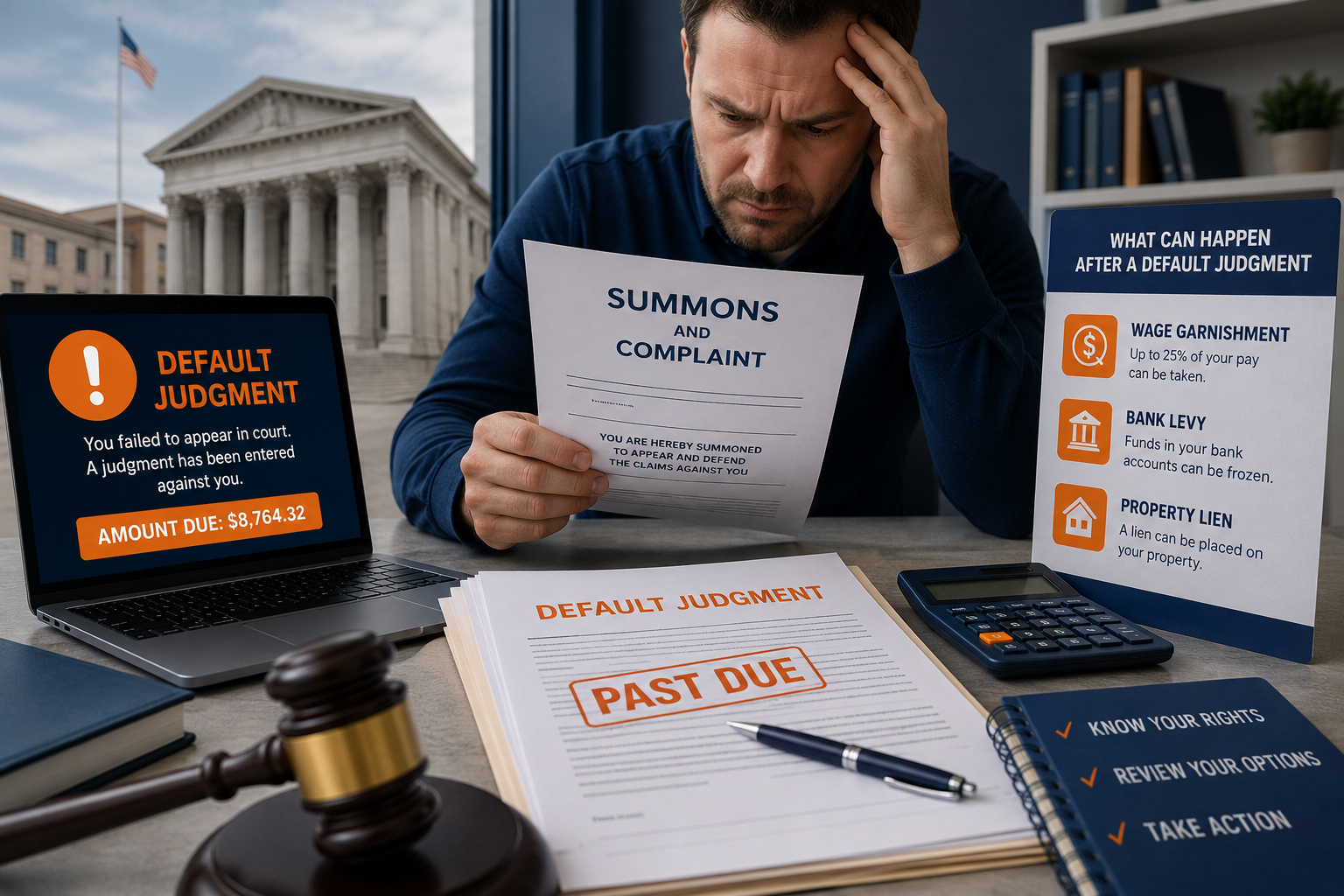

If you missed court for a debt lawsuit, a default judgment has likely already been entered against you, and the creditor can now garnish your wages, freeze your bank account, or put a lien on your property. The clock is running. But you still have options.

At our credit repair company, we see this more than almost any other situation. One case that stands out: a client came to us after finding out about a default judgment, only when her paycheck was suddenly short. She never knew she had been sued. That moment of discovering a garnishment before you even knew there was a case is one of the most jarring things we see, and we see it constantly.

Here is why it matters beyond just one person's story: according to a CFPB-cited report from the Pew Charitable Trusts, 70% of all debt collection judgments are default judgments, meaning the defendant never showed up (source: Pew Charitable Trusts via National Center for State Courts). Only 10% of defendants in these cases have legal representation. Debt collectors count on silence, and they usually get it.

What Happens If You Miss a Court Date for a Debt Collection Lawsuit?

When you miss your court date for a debt collection lawsuit, the court enters a default judgment against you. The creditor wins automatically. They do not have to prove the debt is valid. They do not have to prove the amount is correct. You lose every defense you had, including the statute of limitations, because you were not there to raise them.

Most states give you 20 to 30 days from the date you are served to file a written response. If you miss that window and skip the court date, the creditor files for default. The court grants it. From that point, the full amount claimed plus interest, court costs, and attorney fees becomes a court-ordered debt.

Post-judgment interest starts running immediately. Rates vary by state but commonly fall between 4% and 12% per year. A $10,000 judgment at 8% interest adds $800 every year until you pay it off.

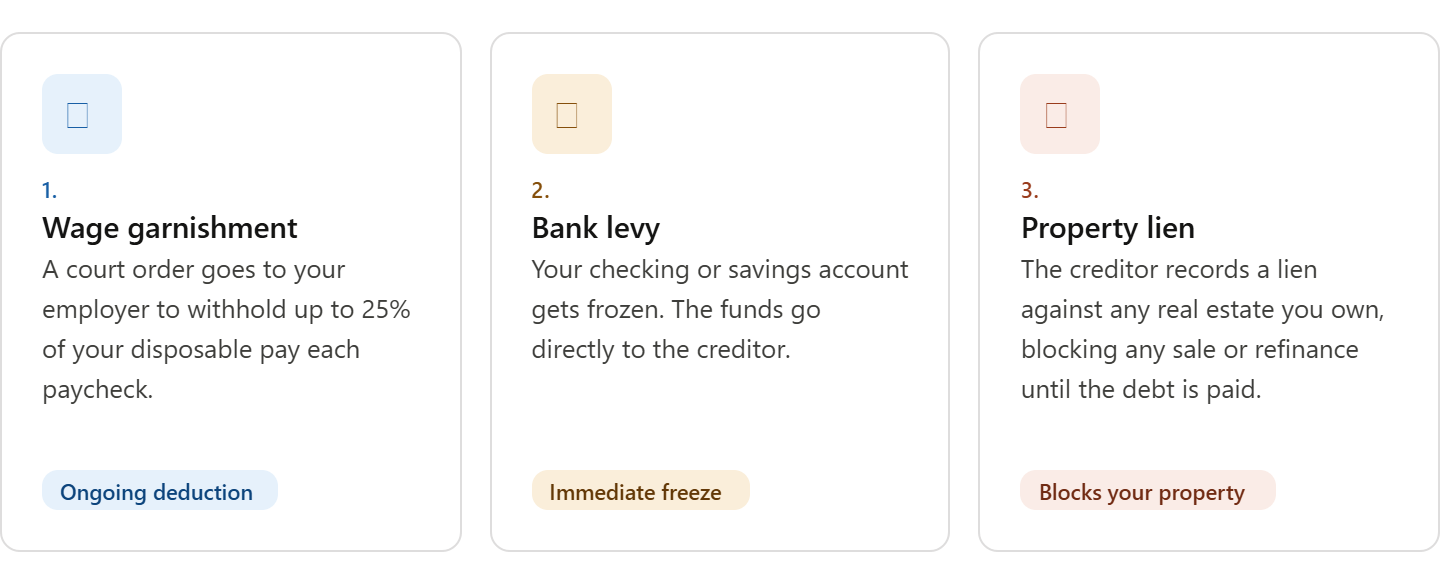

The three most immediate consequences you face:

[=fg1jh

What Happens If You Fail to Respond to a Lawsuit?

Failing to respond and missing the court date produces the same result: a default judgment. The court does not chase you down. It accepts the creditor's version of events as fact.

Many people assume ignoring a lawsuit makes it go away. It does the opposite. Once the creditor has a default judgment, they gain access to every legal collection tool available in your state. According to the FTC, debt collectors filed over 70 million collection attempts in a recent year, and the vast majority of the lawsuits they file end exactly this way, with no response from the consumer.

One defense that disappears fast: the statute of limitations. Every state limits how long a creditor can sue you, usually 3 to 6 years, for consumer debt (CFPB). If a debt buyer sued you on a 7-year-old debt, that case may have been illegal. But courts do not check the clock on their own. You had to show up and say so. If you did not, the judgment stands.

At our firm, we have seen cases where a $500 original debt ballooned past $4,000 by the time a client found out about the judgment, purely from post-judgment interest and added fees. Ignoring the lawsuit did not make the debt smaller. It made it much larger.

What Happens If You Go to Court for a Debt?

Showing up to court for a debt collection case puts the burden back on the creditor. They must prove:

You owe the debt.

The amount is accurate.

They have legal standing to sue you.

Debt buyer companies that purchase old debts for pennies on the dollar often lack the paperwork to prove any of these things. The original signed contract, accurate account statements, and proof of debt ownership must all be presented. Many cannot do it.

When you show up, you can raise defenses like:

The debt is past the statute of limitations.

The amount is wrong.

The debt was already paid.

The debt was discharged in bankruptcy.

The account belongs to someone else (identity theft).

The creditor does not actually own the debt.

Even without a lawyer, showing up forces the other side to prove their case. Many collectors settle or dismiss when challenged. The FTC confirms this directly: showing up often results in better outcomes, including lower settlements or outright dismissal (FTC).

What Happens If You Miss a Court Date? (The Arrest Question)

Debt collectors sometimes imply that you can be arrested for missing a court date in a civil debt case. That claim is false, and it may violate the Fair Debt Collection Practices Act (FDCPA).

You cannot be arrested for owing money. Period. The CFPB is clear on this (CFPB source).

However, there is one scenario that catches people off guard. After a judgment, the creditor can ask the court to require you to appear for a debtor's examination, a formal hearing where you answer questions under oath about your income, assets, and bank accounts.

If you ignore that court order, the judge can hold you in contempt and issue a bench warrant for your arrest. The warrant is not for the debt. It is for defying a court order. That is a real distinction with real consequences.

The safest move: never ignore any court order, even after a default judgment is already entered.

Can You Reverse a Default Judgment?

Yes. A default judgment is not necessarily permanent. Courts can vacate (undo) one if you file a motion to vacate and show valid grounds. This is your most important next step.

The strongest grounds courts accept:

Improper service — You were never properly served with the lawsuit papers. If the process server went to the wrong address or falsely claimed personal delivery, the court may lack jurisdiction over you. Most states impose no time limit for this defense.

Excusable neglect — A legitimate emergency kept you from responding, such as a serious illness, hospitalization, military deployment, or documented family crisis. Most states require you to file within one year of the judgment.

Fraud by the creditor — The creditor misrepresented the debt amount, your identity, or other material facts to the court.

Void judgment — The court lacked jurisdiction entirely, such as suing you in the wrong state.

Courts generally require two things: a good reason for missing court, and a legitimate defense to the underlying debt. Filing fees for a motion to vacate are usually modest, often $35 to $60, and many courts offer waivers for those who cannot afford them.

Under federal court rules, motions based on excusable neglect or fraud must be filed within one year of the judgment (Cornell Law, Rule 60). State court rules follow a similar structure. Do not wait.

Missed Court for a Debt Lawsuit?

A default judgment can lead to wage garnishment, frozen bank accounts, and property liens. Don't wait until collection actions start. Get a professional review of your credit and debt situation today.

✓ Free Credit Analysis

Discover collection accounts, judgments, and potential credit reporting errors that may be hurting your financial future.

No obligation. Learn your options before creditors take further action.

What If You Are "Judgment Proof"?

Even with a default judgment against you, creditors can only collect from income and assets that are not legally protected. If everything you own or earn falls under an exemption, you are judgment proof, meaning the creditor wins on paper but cannot collect in practice.

You may be judgment-proof if:

Your only income comes from Social Security, disability, veterans' benefits, or other exempt federal benefits.

You own no significant property with equity.

You have no wages to garnish or non-exempt bank funds to levy.

Being judgment-proof does not erase the judgment. The creditor can try again if your financial situation improves. But active collection stops when there is nothing to take.

One important note from our work at the company: clients sometimes think commingling exempt funds with regular income protects them. It does the opposite. When you mix Social Security deposits with other money in the same account, it becomes much harder to trace which dollars are protected, and you may lose the exemption entirely.

Your Next Three Moves Right Now

If you just realized you missed court for a debt lawsuit, here is what to do:

Find out if a judgment has been entered. Search your name on your county court's public records portal. Many courts have free online case lookups.

Contact a consumer rights attorney immediately. Many offer free consultations. If you qualify for legal aid, use it. The National Legal Aid and Defender Association (nlada.org) can connect you with free help.

File a motion to vacate if you have grounds. Do not call the creditor first. Get legal guidance, then act through the court.

The worst outcome is not losing in court. It is never showing up at all. Courts, unlike debt collectors, are neutral. Once you engage the process, you have a chance. Before that, you have none.