Receiving a call from NCO Financial Systems can send a wave of anxiety through anyone dealing with debt issues.

Despite being a legitimate debt collection agency founded in 1926, NCO Financial has developed what some consider the "nastiest reputation" among collection agencies.

However, it's worth noting that they've helped protect over $1 billion from predatory debt lawsuits.

In this guide, we'll share expert tips to effectively deal with NCO Financial Systems while protecting your rights and financial future.

Understanding NCO Financial Systems Inc.

NCO Financial Systems has a long and complex history in the debt collection industry. First and foremost, understanding who they are and what they do can help you better navigate your interactions with this collection giant.

Who is NCO Financial and what do they do?

Originally established in 1926 in suburban Philadelphia, NCO Financial Systems began as a family-owned business. The company later changed its name from Barrist Corporation to NCO Financial Systems in December 1986. Today, NCO Group operates as a major business process outsourcing company that provides accounts receivable management, customer relationship management, and back office solutions for its clients. With approximately 30,000 employees across over 100 locations in 11 countries, they've grown into what one analyst called the "Wal-Mart of debt collection".

Is NCO Financial legit or a scam?

If you're wondering "is NCO Financial legit?" or searching for ways to handle NCO collections, you're not alone.

In fact, as of October 2018, the Consumer Financial Protection Bureau received over 1,800 complaints related to Expert Global Solutions (NCO's parent company) debt collection practices.

Although NCO Financial Systems reviews are surprisingly mixed online, with some positive feedback about their collection agents, it's essential to understand that all debt collectors, including the NCO collection agency, must follow the Federal Debt Collection Practices Act (FDCPA).

NCO Financial Reviews

NCO Financial is indeed a legitimate debt collection agency, not a scam. As of November 2023, they maintain an A- rating from the Better Business Bureau. Nevertheless, their reputation is far from spotless. The company has faced significant legal challenges, notably paying a $1.5 million penalty in 2004 for violating the Fair Credit Reporting Act - the largest FCRA civil penalty at that time.

Additionally, NCO has been accused of habitually violating the Fair Debt Collection Practices Act through practices like refusing to validate debts, contacting third parties, and harassing people on the phone. The BBB reports 219 complaints closed in the last three years, with customer reviews averaging just 1.11 out of five stars based on 35 reviews. Even Yelp reviews show a “not so favorable” rating:

Industries NCO collects for

NCO Financial primarily collects debts across several key industries:

- Healthcare providers (their apparent focus)

- Credit card companies

- Telecommunications

- Utility providers

- Educational institutions

The company acquires unsettled debts from creditors who have given up on collecting those amounts. Once they purchase your account, they typically contact you through mail or phone seeking payment. Their widespread reach across multiple industries makes them one of the largest players in the debt collection market.

Common Complaints and Red Flags

Dealing with NCO Financial Systems can be stressful, especially when their collection tactics cross the line. Understanding the most common issues reported by consumers can help you recognize potential problems and protect your rights.

NCO Financial Systems harassment reports

Consumer complaints against NCO Financial Systems reveal concerning patterns of aggressive collection practices. Many individuals report receiving as many as seven calls per day on their cell phones. In one documented case, a consumer received automated calls starting in September 2008, and even after explicitly requesting the calls to stop, NCO continued the unwanted contact.

These persistent calls often disrupt sleep and cause significant distress, particularly for those working night shifts. The Better Business Bureau has recorded 460 complaints filed against the company, highlighting the scope of consumer dissatisfaction.

Typical FDCPA violations by NCO

NCO Financial Systems has faced serious consequences for violating consumer protection laws. Most significantly, they paid a $1.5 million civil penalty, the largest FCRA penalty at that time, for reporting inaccurate information about consumer accounts to credit bureaus. Their violations typically include:

- Reporting later-than-actual delinquency dates, causing negative information to remain on credit files beyond the seven-year reporting period

- Continuing collection calls after being told the person they seek doesn't live at that number

- Revealing personal financial information through window envelopes

- Contacting third parties about consumer debts

How to verify if the debt is yours

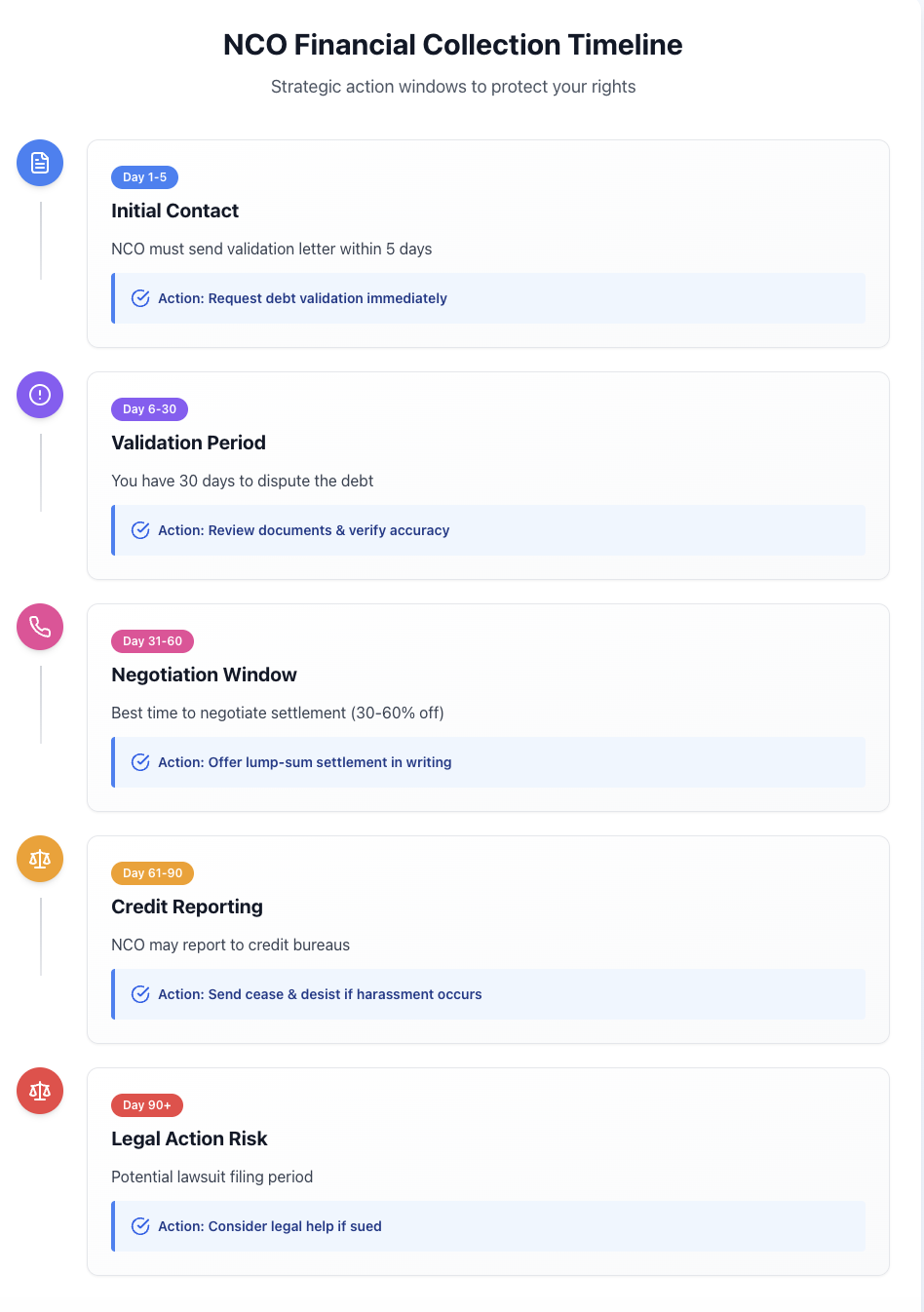

Before making any payments, always verify that the debt legitimately belongs to you. Request debt validation in writing from NCO Financial Systems, they must respond within 30 days. Once you receive their verification, you have another 30 days to dispute the debt if necessary. This verification process gives you time to review your records alongside their information.

If you're struggling with persistent debt collection issues or need help validating suspicious claims, contact our credit repair company for professional assistance in resolving these matters properly.

Remember: Ignoring collection letters, even for debts you don't recognize, often leads to lawsuits. Always respond promptly to avoid escalation.

7 Expert Tips to Beat NCO Financial Systems

Taking control when facing NCO Financial Systems requires strategic action rather than panicking. Here are seven expert-backed strategies to effectively handle their collection attempts:

1. Review your financial situation first

Before engaging with NCO, carefully analyze your income, recurring expenses, and savings to determine how much you can realistically afford to pay. This assessment gives you a clear picture of your negotiating position and prevents you from making promises you can't keep.

2. Request debt validation in writing

Under the Fair Debt Collection Practices Act, NCO Financial must provide a debt validation letter within five days of initial contact. This letter should include the creditor's name, account number, and itemization of the current debt amount. Always request this documentation to confirm the debt is legitimate.

3. Send a cease and desist letter if needed

If NCO's calls become excessive, send a formal cease and desist letter via certified mail with return receipt. Once received, they must stop contacting you except to confirm receipt or notify you of specific actions they intend to take.

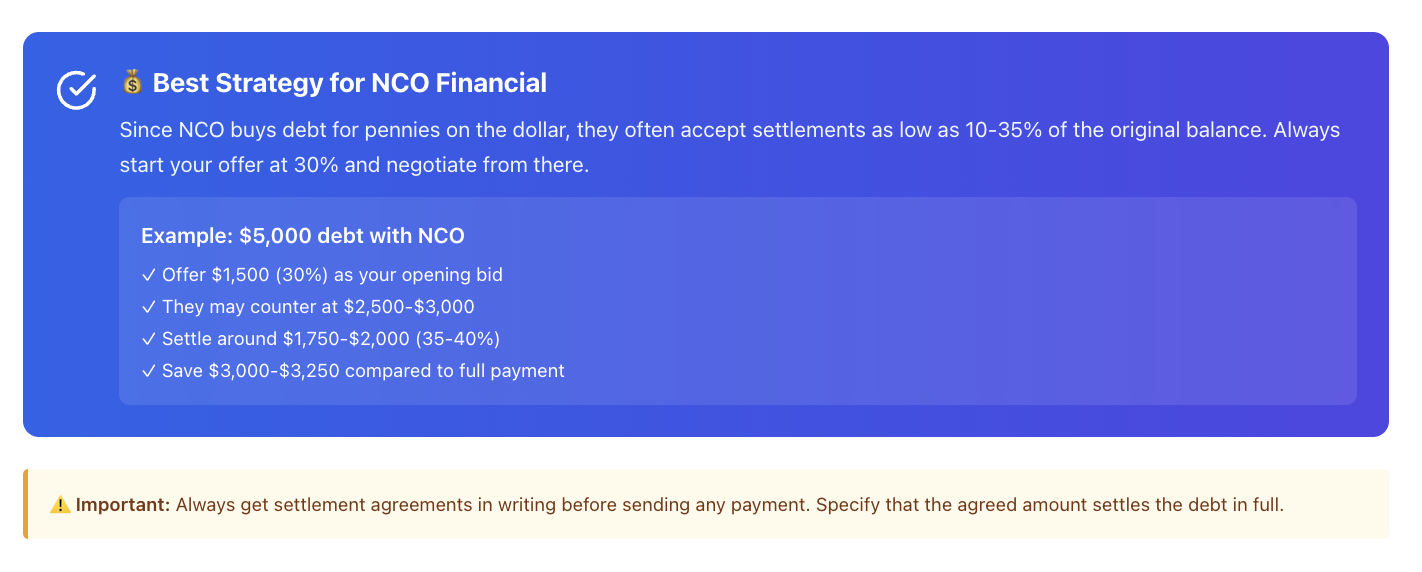

4. Negotiate a lump-sum settlement

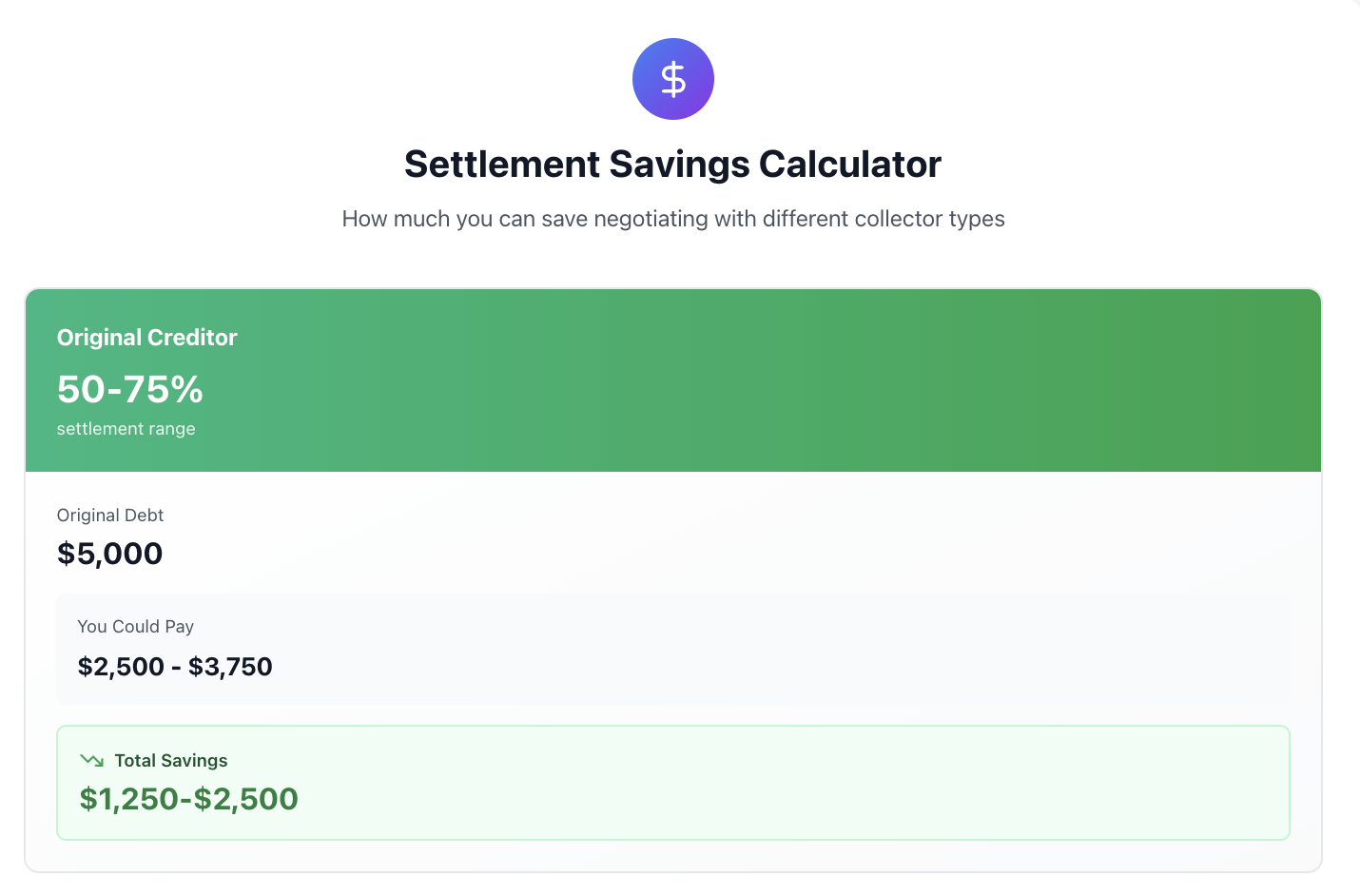

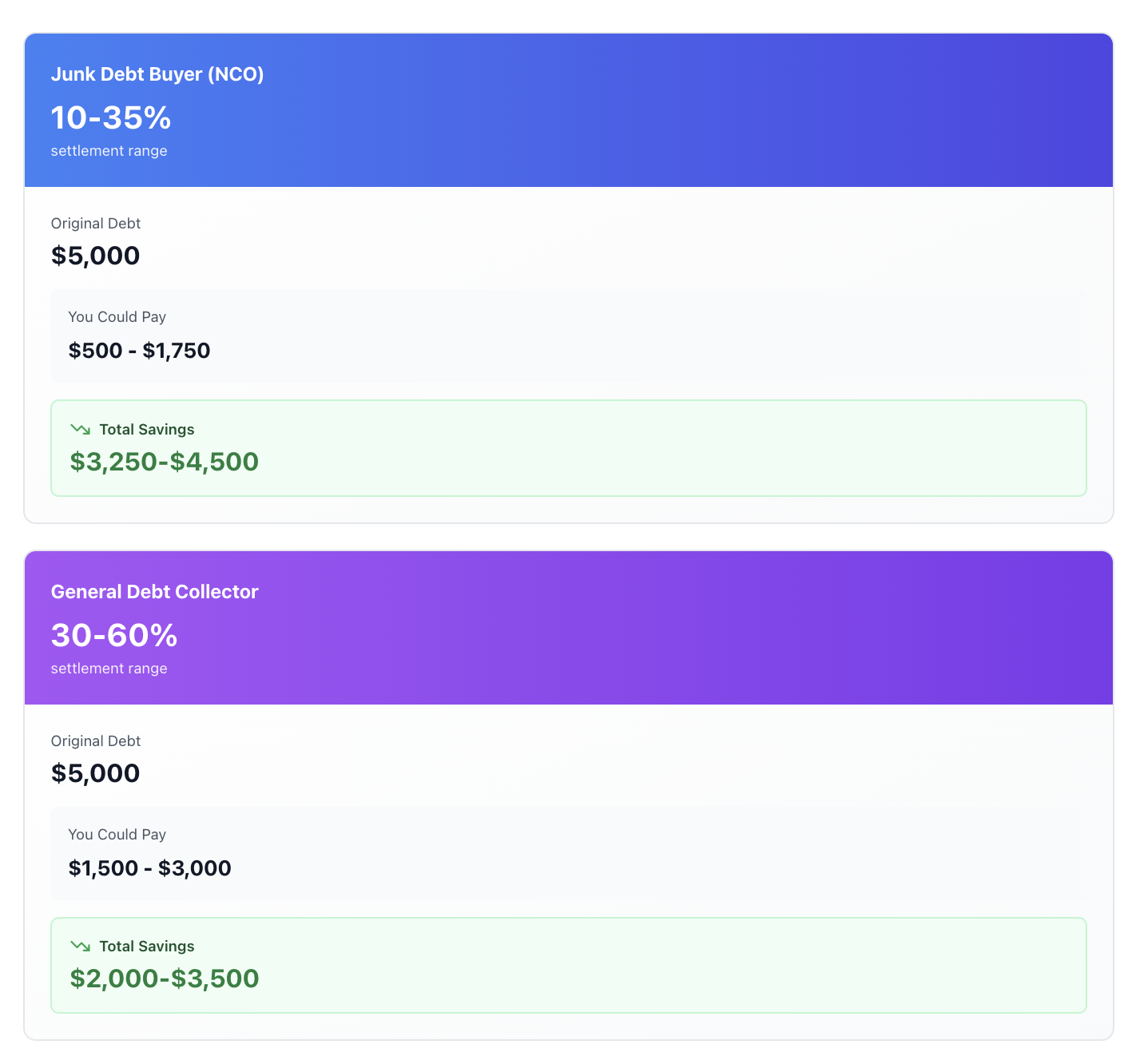

Most debt collectors, including NCO, will accept less than the full amount owed. Start by offering around 30-60% of the original balance. For junk debt buyers, settlements of 10-35% are typical, whereas original creditors may accept 50-75%.

5. Get all agreements in writing

Never make any payment without a signed settlement agreement from NCO. This document should clearly state that the amount paid settles the account in full and specify whether the trade line will be deleted from your credit bureaus.

6. Track all communication with NCO

Document everything, phone calls, letters, and payments. Use certified mail for all written correspondence and keep copies of everything you send. This documentation protects you if disputes arise later.

7. Consider legal help if sued

If NCO files a lawsuit, respond promptly by the deadline specified in the court papers. Even when sued, you can still negotiate a settlement, accordingly putting yourself in a stronger position. Contact our credit repair company if you need professional guidance navigating this process.

Remember that debt collectors must follow federal laws, knowing your rights gives you leverage in any negotiation with NCO Financial Systems.

How to Prevent Future Debt Collection Issues

Preventing debt collection problems with companies like NCO Financial Systems is far simpler than resolving them after they start. By taking proactive steps now, you can avoid stressful interactions with collectors in the future.

Monitor your credit report regularly

Credit monitoring services allow you to track activity on your credit report and receive alerts about changes that might indicate problems. Consequently, checking your credit reports at least once a quarter (once a month is ideal) helps you spot potential issues early. Furthermore, regularly monitoring your credit ensures your report remains accurate and allows you to take immediate action if something suspicious appears.

Communicate with original creditors early

One in three people get contacted by creditors or collectors seeking payment within a year. Initially, reaching out to your original creditors when you first experience financial difficulty can prevent your account from being sent to NCO Financial Systems or other collection agencies.

Most creditors prefer working directly with customers to arrange payment plans rather than selling debts to third-party collectors. Above all, helping customers early builds trust and prevents small financial issues from becoming major problems.

Understand your rights under FDCPA

The Fair Debt Collection Practices Act (FDCPA) prohibits collection companies from using abusive, unfair, or deceptive practices. Under this federal law, debt collectors:

- Cannot contact you before 8 a.m. or after 9 p.m.

- Must stop calling if you request it in writing

- Cannot harass you or use obscene language

- Must provide debt validation within five days of initial contact

Simply put, knowing these rights empowers you to confidently address collectors and request they follow the law.

Conclusion

Dealing with NCO Financial Systems certainly presents challenges, but armed with the right knowledge, you can effectively manage their collection attempts. Throughout this guide, we've examined their history, practices, and the legal boundaries they must respect. While NCO operates as a legitimate collection agency, their track record shows numerous consumer complaints and regulatory penalties that demand caution when interacting with them.

Remember You Have Rights Against NCO Financial

First and foremost, remember your rights under the Fair Debt Collection Practices Act. These protections exist specifically to shield consumers from unfair collection tactics. Therefore, always verify any debt before making payments and document all communications meticulously. A written record provides essential protection should disputes arise later.

Many people find success negotiating settlements for less than the full amount owed. Additionally, requesting proper debt validation often reveals inaccuracies or time-barred debts that collectors legally cannot pursue. If you feel overwhelmed by the process or face particularly aggressive collection attempts, contact our credit repair company for professional guidance through these complex situations.

After all, preventing collection issues proves far easier than resolving them after escalation. Regular credit monitoring, early communication with original creditors, and understanding consumer protection laws form your strongest defense against future collection problems. Though NCO Financial Systems may seem intimidating, their power diminishes significantly when confronted with informed consumers who understand their rights and options.