Here's what nobody tells you about payment arrangements.

They can rescue you from collections. They can also wreck your credit for years.

I've spent almost 2 decades in the finance industry, watching people make the same mistakes. They think any payment plan is better than no plan. That's not always true.

The difference between a helpful arrangement and a harmful one comes down to three things. What you negotiate. What gets reported. What you get in writing.

Let's break down what actually happens to your credit when you set up payment arrangements.

What Is a Payment Arrangement?

A payment arrangement is an agreement between you and a creditor to pay your debt over time instead of all at once.

Think of it as a custom payment schedule. You owe $2,000 but can't pay it today. You work out a deal to pay $200 monthly for ten months.

Sounds simple. It's not.

Payment arrangements come in different forms. Some help your credit. Others destroy it. The type you get depends on who you're dealing with and what you negotiate.

Original creditors offer hardship programs. These keep your account current if you follow the plan. Your credit stays mostly intact.

Collection agencies offer settlement plans. These often report negatively, even when you pay. Your credit takes a hit regardless.

Court-ordered arrangements happen after judgments. These show up as public records and damage credit significantly.

Here's the kicker. Most people don't know which type they're getting until it's too late.

According to the Consumer Financial Protection Bureau, nearly 30% of Americans with credit files have debts in collections. Many of these started as payment arrangements that went sideways.

The arrangement itself isn't listed on credit reports. What shows up is how it's reported by the creditor.

Common Payment Agreement Mistakes You Have to Know:

Most people focus only on the payment amount. That's a mistake.

The reporting terms determine credit impact. The default clauses determine what happens when life gets messy.

- Verbal agreements aren't enough. Creditors can and do change terms if nothing is in writing. I've seen collectors promise one thing on the phone and do another when it comes to credit reporting.

- Get every agreement in writing before making the first payment. Email confirmations work. Letters on company letterhead work better. Recorded calls can help but aren't as strong as written documents.

- Read the fine print on what's NOT included. Some agreements only cover the principal balance. Interest and fees continue accruing. You think you're paying off $2,000 but end up owing $2,800 because interest kept adding up.

- Check if the agreement includes credit reporting protection. Will they report as current? Will they delete upon completion? Will they mark it as settled? These details make or break your credit outcome.

Payment agreements are contracts. They're enforceable. Courts uphold them. Make sure the terms actually help you before signing anything.

The Credit Reporting Reality Most People Miss

Payment arrangements don't have their own category on credit reports.

Instead, creditors choose how to report your account while you're in the arrangement. This is where things get messy.

Scenario one. You set up a hardship plan with your credit card company. They agree to lower your payment to $100 monthly. They report your account as "current" each month you pay. Your credit score stays stable or even improves.

Scenario two. You negotiate with a collection agency. They agree to $50 monthly payments. They report your account as "in collections" every month. Your credit score drops 100+ points and stays there until the debt is paid and deleted.

Same concept. Completely different outcomes.

I've seen clients with identical $3,000 debts. One negotiated with the original creditor and maintained a 680 score. The other went through collections and dropped to 540.

The reporting method matters more than the arrangement itself.

Most creditors won't tell you how they'll report the account. You have to ask explicitly. Get it in writing. Make reporting terms part of your negotiation.

When Payment Arrangements Actually Help Your Credit

Payment arrangements help when they keep you out of default and collections.

With original creditors before you're late. If you're struggling but still current, contact your creditor immediately. Ask about hardship programs. Banks offer temporary payment reductions for medical issues, job loss, or disasters.

These programs report as "current" or "payment plan." Your credit score might dip slightly from high balance utilization. But you avoid the massive hit from late payments and charge-offs.

Credit card hardship programs. Most major issuers offer these. They lower your interest rate and minimum payment. Your account closes, but reports as current. You can't use the card, but your credit stays cleaner than default.

Mortgage forbearance done right. Recent forbearance programs let you pause payments without default reporting. Not all forbearance is equal, though. COVID-era programs had protections. Regular forbearance might still report negatively.

Student loan rehabilitation. This is a specific program for defaulted federal student loans. Make nine on-time payments over ten months. The default gets removed from your credit report. Your score can jump 100+ points.

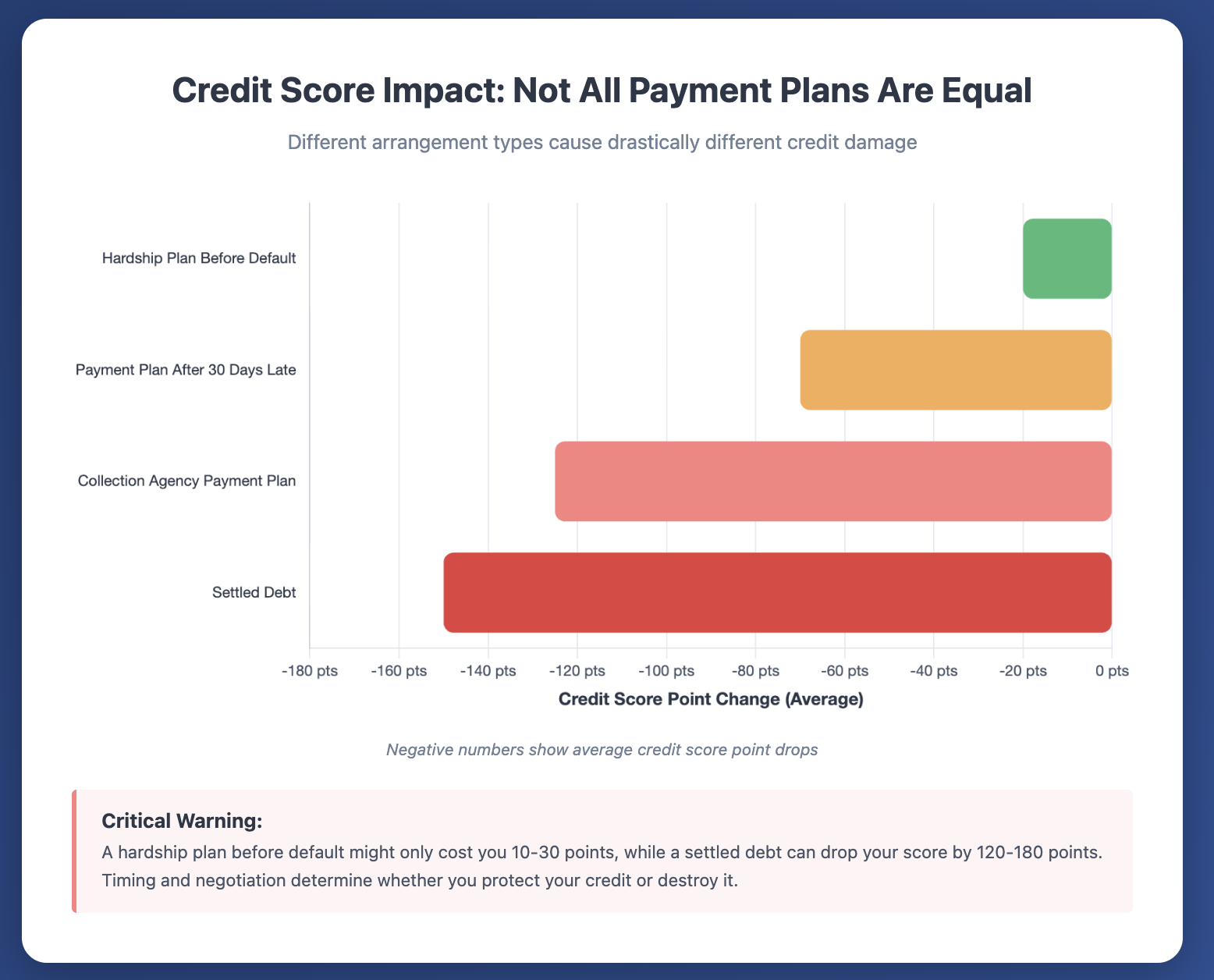

According to Experian, payment plans with original creditors before default typically cause minimal credit damage compared to letting accounts go to collections.

The key is timing. Arrange payment plans before you're 30 days late. Once you hit 30, 60, or 90 days past due, that reporting sticks for seven years even if you later set up payments.

Here's a sample bar graph comparing the credit score impact of each payment plan:

When Payment Arrangements Absolutely Destroy Your Credit

Some payment arrangements guarantee credit damage.

Collection agency payment plans. Once your debt is sold to collections, payment arrangements rarely help your score. The collection account reports monthly. Each month adds another negative mark.

You might think paying through a plan shows responsibility. Credit scoring models don't see it that way. They see an active collection account. Your score stays suppressed until the account is deleted.

Debt settlement programs. These third-party companies negotiate reduced payoffs. Sounds good. Here's the problem. They tell you to stop paying creditors while they negotiate. Your accounts default. Late payments pile up. By the time they settle, your credit is demolished.

The settlement itself reports as "settled for less than owed." This is almost as damaging as a charge-off. It stays on your report for seven years.

Payment plans after charge-off. If your creditor already charged off the debt, payment plans don't remove the charge-off. The account still reports as charged-off every month. You're paying on a debt that continues to hurt your credit.

I've watched clients pay thousands on charged-off accounts, thinking it would help their scores. It didn't. They just gave money to collectors while the negative mark remained.

Partial payment settlements without deletion agreements. You negotiate to pay 50% of the balance. You pay it. The account updates to "settled" but stays on your report. Your score barely improves because the negative account is still there.

Here's what makes this worse. Some creditors use payment arrangements as a tactic to restart the statute of limitations. Making even one payment on old debt can reset the clock on how long they can sue you.

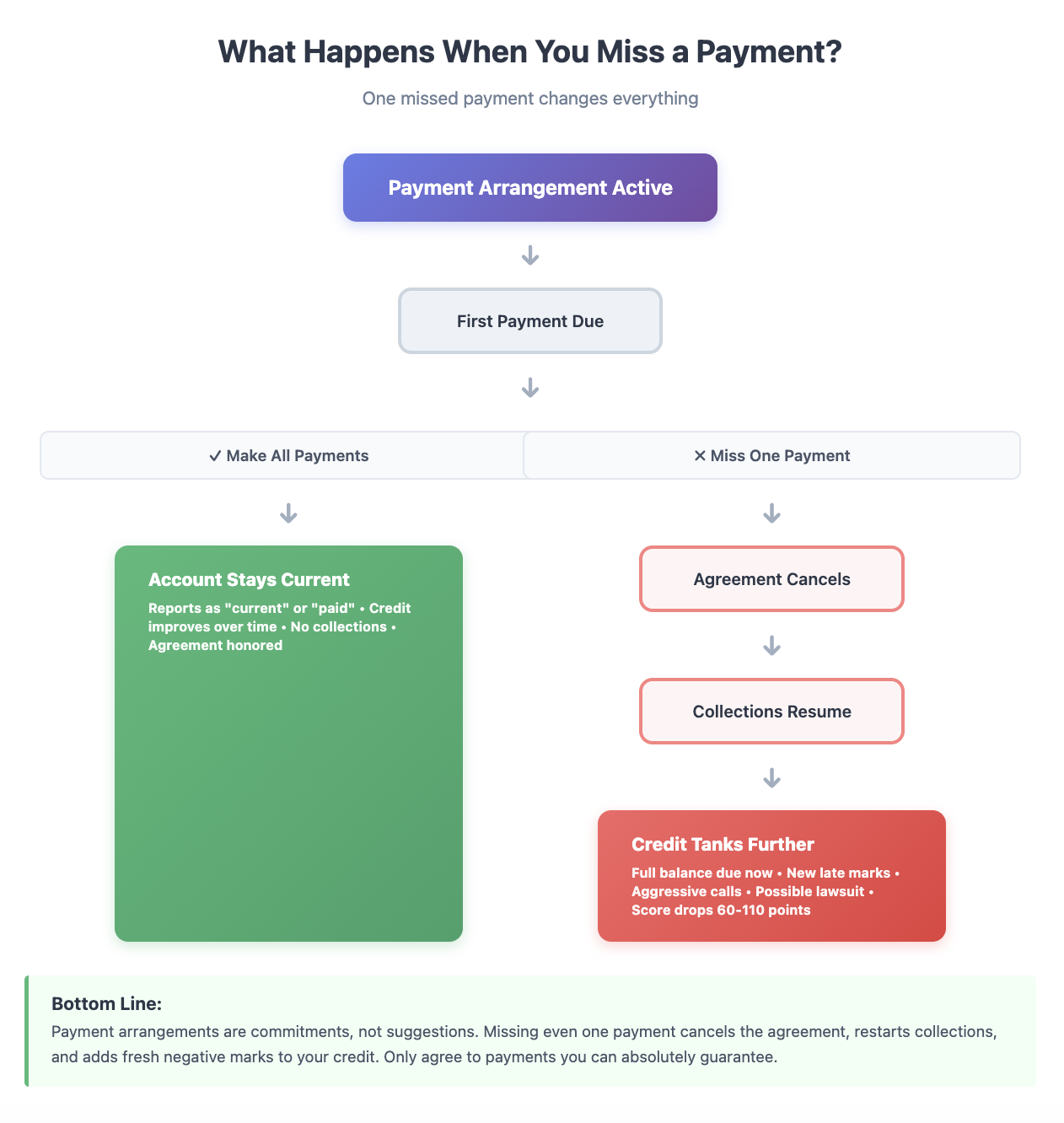

What Happens If You Miss Your Payment Arrangement?

Missing a payment in your arrangement triggers immediate consequences.

The protection ends. The creditor cancels the agreement. Everything gets worse fast.

Your remaining balance becomes due immediately. That $5,000 you were paying over 12 months? All due now.

Late payment reporting resumes. If the arrangement was keeping your account current, missing a payment means a new 30-day late mark. This drops your score another 60 to 110 points depending on your starting score.

Collection activity restarts. Phone calls increase. Letters come more frequently. The creditor may pursue legal action.

You lose negotiating power. Creditors rarely offer the same terms twice. Your next arrangement will likely have worse terms or higher payments.

The debt may sell. Original creditors often sell debts after failed payment arrangements. Once sold, you're dealing with collection agencies. They're harder to negotiate with and report more aggressively.

Some creditors report to credit bureaus when you default on payment arrangements. This creates a fresh negative entry even if previous late payments already existed.

I tell clients that payment arrangements are commitments, not suggestions. If you can't absolutely guarantee the payments, don't make the arrangement. One missed payment can undo months of progress.

The Four Types of Payment Structures You Need to Know

Not all payment arrangements work the same way. Understanding the structure protects you from surprises.

Installment agreements. You pay fixed amounts on a schedule. Think car loans or personal loans. These report monthly. On-time payments help credit. Late payments hurt it.

With debt payment arrangements, installment plans work best when dealing with original creditors. They report the account as current if you pay on time.

Lump-sum settlements. You pay one large payment for less than you owe. This closes the account immediately. The downside? It reports as "settled for less than owed" which damages credit nearly as much as default.

Only use lump-sum settlements when you can negotiate deletion. Get "pay-for-delete" in writing before paying.

Graduated payment plans. Payments start small and increase over time. These work for people expecting income growth. The risk is overestimating future income. If you can't make the higher payments later, you default partway through.

Percentage-based payments. Some creditors tie payments to your income. This is common with student loans and IRS payment plans. As your income changes, so do your payments.

These can help if your income is unstable. But if your income increases significantly, your payments might become unaffordable relative to other expenses.

According to the National Foundation for Credit Counseling, consumers who understand their payment structure before agreeing have a 40% higher success rate in completing arrangements without default.

Choose the structure that matches your realistic financial situation. Don't agree to increasing payments unless you're certain income will increase. Don't commit to fixed high payments if your income is unstable.

The Pay-for-Delete Strategy That Actually Works

Here's the arrangement that helps credit most. Pay-for-delete.

You agree to pay the debt. The creditor agrees to delete the negative item from your credit report entirely.

This is the gold standard. It removes the damage instead of just stopping it from getting worse.

Collection agencies are most likely to agree to pay-for-delete. Original creditors rarely do it. Government debts like student loans and taxes never do it.

How to negotiate pay-for-delete. Start by offering to pay in full in exchange for deletion. If they won't agree to full deletion, try "goodwill deletion" after payment. Some creditors delete as a courtesy after accounts are paid.

Get it in writing before paying. This is non-negotiable. Without written confirmation, they can keep your money and leave the negative mark.

Use specific language. Say "I will pay $X in exchange for complete deletion of this account from all three credit bureaus within 30 days of payment." Get them to confirm these exact terms.

Verify deletion after payment. Wait 45 days then pull your credit reports. If the item isn't deleted, you have written proof to dispute it.

The Consumer Financial Protection Bureau doesn't prohibit pay-for-delete. It's legal. It works. It's just not guaranteed unless you negotiate it upfront.

I've helped hundreds of clients remove collection accounts through pay-for-delete. It can raise credit scores 50 to 100 points instantly when the deletion processes.

But it only works if you get the agreement in writing first. Collectors who promise deletion verbally often "forget" after receiving payment.

The Income-Based Arrangements That Keep You Safer

If your income fluctuates, standard payment arrangements set you up for failure.

Income-based arrangements adjust to what you can actually afford.

Federal student loan income-driven repayment plans. These cap payments at 10% to 20% of discretionary income. If income drops, payments drop. You won't default just because income changed.

These plans report as current to credit bureaus when you make required payments. They protect credit even when payments are as low as $0 monthly.

IRS payment plans. The IRS offers installment agreements based on your ability to pay. They analyze your income and expenses. They set payments you can realistically make.

Tax payment plans don't report to credit bureaus at all. The IRS doesn't report to Equifax, Experian, or TransUnion. Only tax liens show up, and those must be filed separately.

Nonprofit credit counseling debt management plans. These consolidate unsecured debts into one monthly payment. The payment amount is based on your budget.

Creditors agree to lower interest rates and stop collection calls. The plan reports to credit bureaus but typically shows as current when you make payments.

According to the National Foundation for Credit Counseling, consumers in debt management plans pay off debt 3 to 5 years faster than those making minimum payments.

The credit impact is mixed. Some scoring models see debt management plans negatively. Others don't penalize them. Overall, the impact is far less than default and collections.

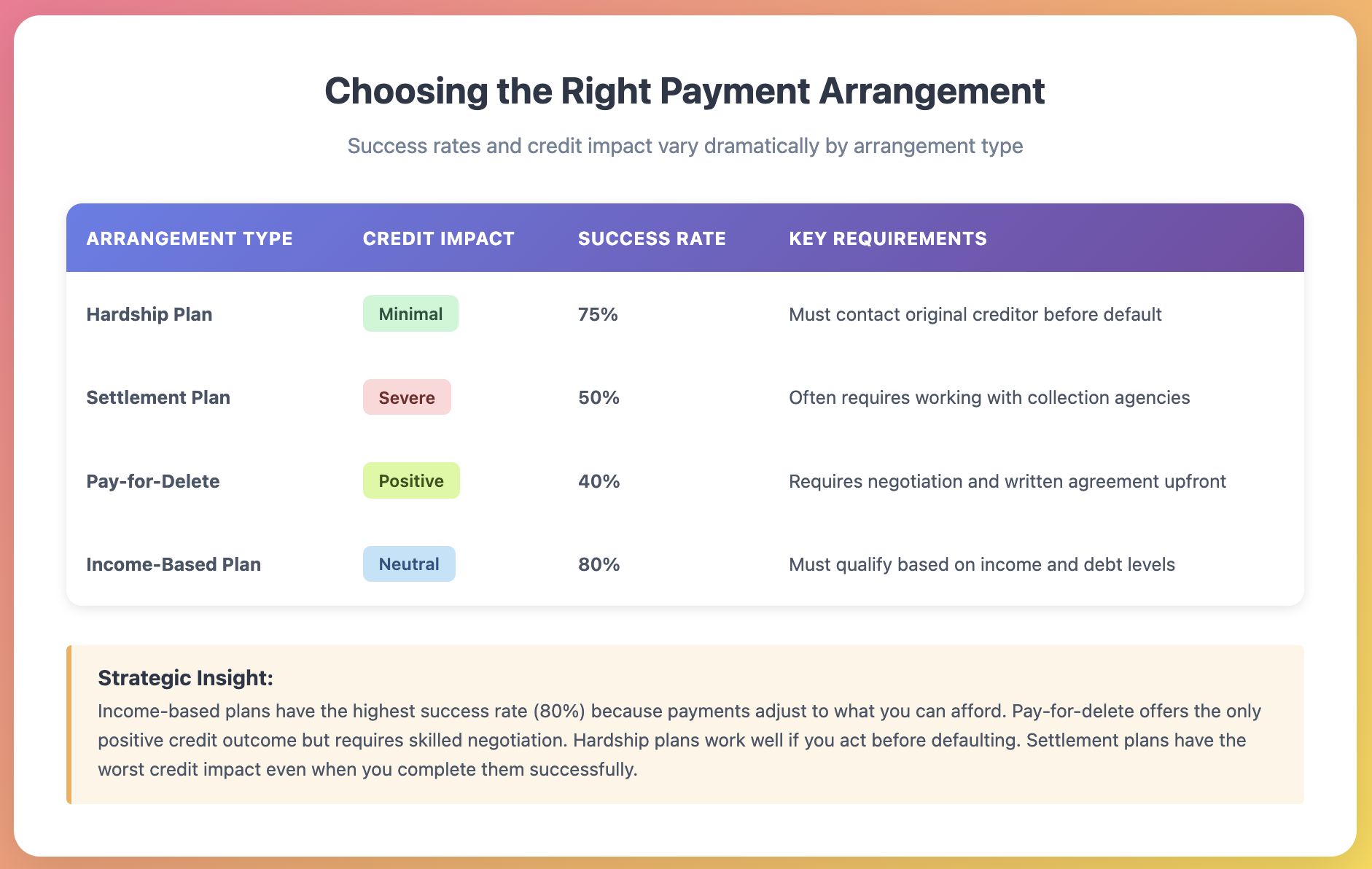

Below is a comparison table showing payment arrangement types:

The Documentation That Protects You

Payment arrangements fall apart when documentation is missing.

Protect yourself with these documents before making any payment.

- Written payment agreement. Email or letter confirming the total amount, payment schedule, and any special terms. Both parties should have copies.

- Credit reporting terms. Separate confirmation of how the account will report while you're making payments and after it's paid off.

- Proof of payment for every transaction. Bank statements, canceled checks, money order receipts, or confirmation numbers from phone payments. Keep everything until the debt is completely resolved and verified removed from credit reports.

- Deletion agreement if applicable. Separate written confirmation that the creditor will delete the account from credit reports after final payment.

- Correspondence logs. Record every phone call. Note the date, time, representative name, and what was discussed. Follow up calls with emails summarizing what was agreed.

I keep client files for seven years after debts are resolved. Why seven years? That's how long negative items stay on credit reports. If something resurfaces, you have proof of the arrangement and payment.

Creditors lose paperwork. Representatives quit or forget conversations. Computer systems glitch. Your documentation is the only protection when things go wrong.

Without proof, it's your word against theirs. Courts and credit bureaus side with creditors when consumers can't provide documentation.

What Happens After You Complete the Arrangement

Completing a payment arrangement doesn't automatically fix your credit.

What happens next depends on what you negotiated upfront.

If you negotiated deletion. The account should disappear from your credit reports within 30 to 45 days of final payment. Check all three bureaus. Dispute if it doesn't delete as agreed.

If you negotiated "paid in full" status. The account updates to show a zero balance and "paid" status. It still reports for seven years from the date of first delinquency. Your score improves but the negative history remains.

If you settled for less. The account updates to "settled" status. This is still negative but slightly less damaging than "charged off." It stays seven years from first delinquency.

If you just made payments without specific agreements. The account reports however the creditor chooses. Collection accounts might update to "paid collection" which barely helps your score.

The age of negative items matters. Older negatives hurt less than recent ones. As your payment arrangement account ages, its impact on your score decreases even if it stays on your report.

New positive credit history helps too. As you add on-time payments to other accounts, the negative arrangement item becomes a smaller part of your credit profile.

Some people ask if they should pay old debts in collections. The answer depends on your goals. If you're applying for a mortgage soon, paid collections look better than unpaid ones even if the score impact is similar. If you're years away from needing credit, paying without deletion might not be worth it.

The Mistakes That Turn Good Arrangements Bad

Smart people make these mistakes constantly.

Agreeing to payments you can't truly afford. You want to resolve the debt quickly. You commit to $300 monthly when your realistic budget allows $150. You miss payments. The arrangement fails.

Not getting reporting terms in writing. The collector says they'll report as current. You believe them. They report as collection anyway. Your credit tanks while you're paying them.

Paying old debts without checking statute of limitations. Some debts are too old to sue over. Making a payment restarts this clock. You give collectors new legal power they didn't have before.

Focusing only on monthly payment amount. You negotiate down to $50 monthly. Great. But the total payoff increased because interest keeps adding. You end up paying more than the original debt.

Making payments to the wrong party. Debts sell between collection agencies. You keep paying the original collector. The new owner reports late payments. You're paying someone who doesn't even own the debt anymore.

Trusting verbal promises. "Just make this payment and we'll work something out." You pay. They don't work anything out. You're out the money with nothing to show for it.

Not verifying deletion after payment. You got pay-for-delete in writing. You completed payments. You assume it's handled. Six months later you check your report and the item is still there. The 30-day deletion window has passed. Now it's harder to get removed.

I've seen every one of these mistakes cost people thousands of dollars and years of credit damage.

Final Thoughts About Payment Arrangements

Payment arrangements can rescue your credit or ruin it.

The difference comes down to what you negotiate and what you document.

Before agreeing to any payment arrangement, ask yourself three questions. Will this keep me out of collections or am I already there? What exactly will this do to my credit reporting? Do I have this agreement in writing?

If you can't answer all three confidently, don't agree yet.

The best payment arrangements happen early. Before you're late. Before you default. Before collections.

The worst happens when you're desperate and agree to anything just to stop the calls.

Take your time. Negotiate hard. Get everything in writing. Verify what actually gets reported.

And remember this. The person calling you isn't your friend. They're doing a job. That job is collecting money, not protecting your credit.

Your job is to protect your credit while resolving debts. These goals can align with the right arrangement. They can also directly conflict with the wrong one.

Choose wisely. Document everything. Follow through completely.