Many people do not discover Resurgent Capital Services while monitoring their credit.

They discover it when something important is about to happen.

A mortgage application.

An auto loan.

A refinancing review.

A lender pulls the report and suddenly an old collection account becomes the center of attention.

That changes the conversation.

The question is no longer:

"What is Resurgent Capital Services?"

The question becomes:

"Can this account stop my approval?"

And more importantly:

"Can it be removed?"

I've seen borrowers spend months improving their scores only to find that a single collection account creates more underwriting friction than expected.

In my close to 20 years of experience doing credit repair, I am confident to say that Resurgent accounts can be challenged.

What's important to say is not every collection should be handled the same way.

You should first know what you're dealing with before making a payment or settlement decision.

How to Remove Resurgent Capital Services From Your Credit Report

Resurgent Capital Services accounts can be deleted from a credit report through disputes, validation requests, reporting corrections, or other credit reporting challenges. The best strategy depends on the account's accuracy, age, ownership, and supporting documentation.

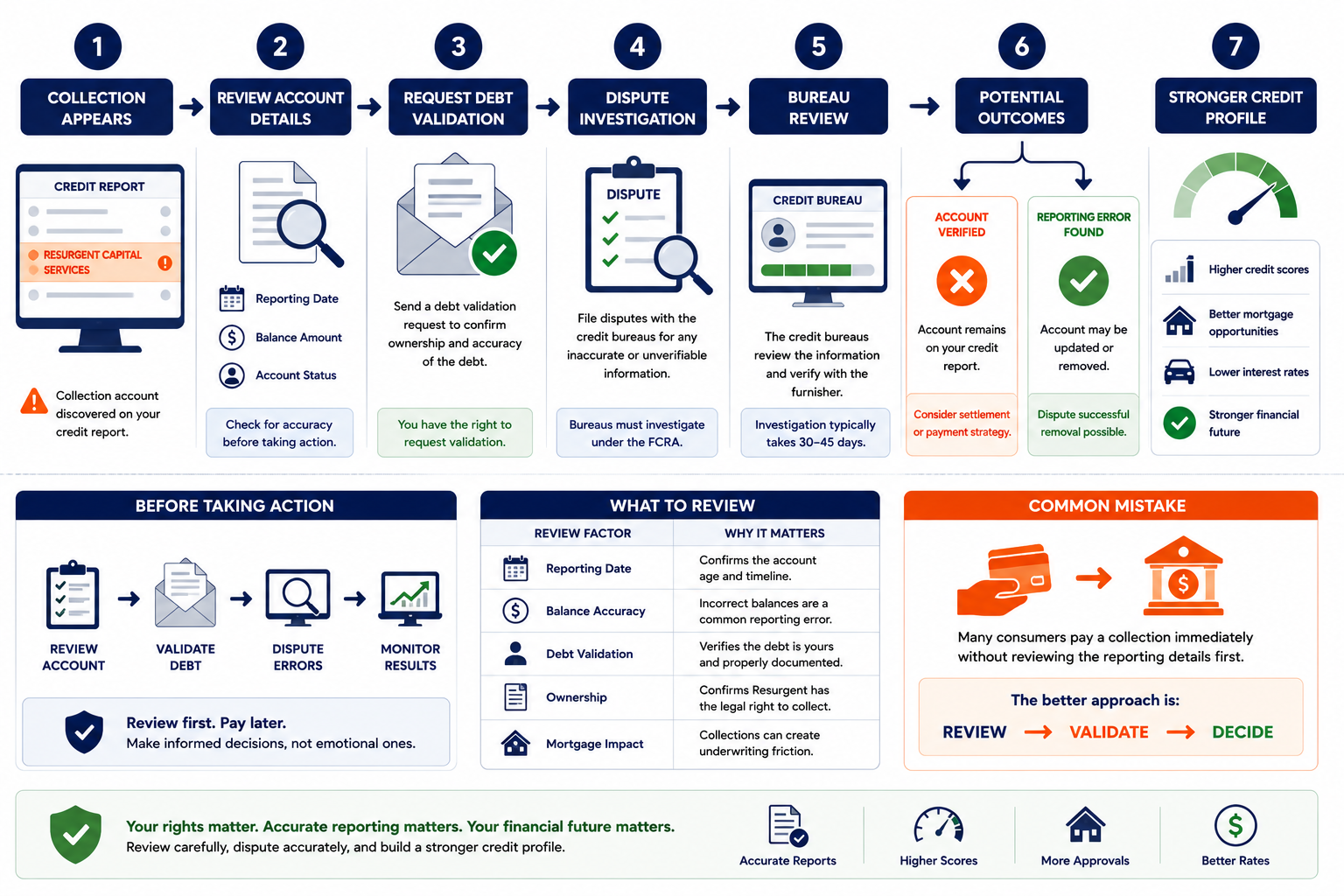

So before of thinking about paying or disputing a Resurgent Capital Services account, it helps to understand the review process.

The visual below shows how collection accounts are evaluated, validated, disputed, and sometimes removed when reporting issues are identified.

What Is Resurgent Capital Services on Your Credit Report

Resurgent Capital Services is a debt collection company. It is the operational arm of LVNV Funding LLC. Both are owned by Sherman Financial Group and headquartered in Greenville, South Carolina. LVNV buys the debt. Resurgent collects it. Your credit report may show LVNV Funding as the account creditor. Your calls and letters come from Resurgent. They are the same operation under two names.

This two-name system confuses a lot of people. It is not an accident.

LVNV is the legal debt holder. It does not contact consumers. It does not send letters. It simply owns the paper on your account.

Resurgent is the face of the operation. They call. They write letters. They file lawsuits. They handle all credit reporting. They report under their name and under LVNV's name simultaneously.

Sherman Financial Group also owns other related entities in this web. Ascension Capital Group originates the purchases. Lighthouse Management Services handles additional collections. Pinnacle Credit Services is another name that sometimes appears. Some consumers get calls from all three names for a single debt.

Understanding who you are actually dealing with is the first step. They are all the same organization.

The Sherman Financial Group Web , One Debt, Multiple Names

When both LVNV and Resurgent appear on your credit report for the same debt, that is a dual-entry conflict.

One underlying debt. Two negative tradelines. That is a disputable reporting inaccuracy under the FCRA.

Dispute both. Cite the conflict. Neither entity can accurately represent 100% of a single debt balance simultaneously.

How Resurgent Capital Services Gets on Your Credit Report

Resurgent and LVNV appear on credit reports after purchasing charged-off consumer debt from original creditors , credit card companies, banks, retailers. They pay 3-7 cents per dollar of face value. They then attempt to collect the full stated balance. The average account ASAP reviewed in Q3 2025 was 3.8 years old at the time of collection. Old debt means fewer records. Fewer records means weaker validation responses.

The type of debt varies. But the pattern is consistent.

- Charged-off credit cards from Capital One, Chase, Citibank, Bank of America, and Credit One

- Retail store accounts from Best Buy, Sears, and similar retailers

- Charged-off personal loans

- Medical debt portfolios in some cases

Many consumers first discover Resurgent on their credit report during a loan application.

They did not get a letter. They did not receive a call. The account just appeared. This is debt parking , reporting a debt to bureaus before contacting the consumer. It violates CFPB Regulation F, effective November 2021. Document when the account appeared versus when you first received communication. If the report date came first, file a CFPB complaint immediately alongside your dispute.

Resurgent Capital Services Enforcement Record , Why This Matters

Resurgent Capital Services and LVNV Funding have a documented history of regulatory problems. The 2023 CFPB action. The Maryland licensing settlement. The active 2025 Oregon lawsuit. Over 26,000 total CFPB complaints. These are not isolated incidents. They show a pattern. That pattern is what makes disputes against Resurgent more likely to succeed than disputes against collectors with cleaner records.

- 2023 CFPB enforcement action against Resurgent Capital Services for illegal collection practices. CFPB described the conduct as violating consumer protection law. Settlement terms required changes to collection operations.

- Maryland licensing settlement , LVNV Funding filed collection lawsuits in Maryland while not licensed to do business in the state. Consumers who were sued had grounds to challenge the lawsuits on procedural standing. The settlement confirmed that Resurgent's legal filings do not always follow proper licensing requirements.

- Active 2025 Oregon lawsuit alleging Resurgent attempted to collect a 15-year-old time-barred debt without disclosing the SOL status. Under the FDCPA, this disclosure is required. Failure to provide it is a federal violation.

- 26,000+ combined CFPB complaints (Resurgent and LVNV as of April 2025). Top complaint pattern: collecting debts consumers say are not theirs. Second pattern: inaccurate credit reporting. Third: failure to validate when requested.

- 1.4-star BBB rating with 1,581 complaints filed in the last three years. Most complaints cite billing disputes, collection errors, and failure to remove after payment.

This record has a practical application. It means two things.

First, CFPB complaints carry real weight with this collector. They are already under scrutiny. Another complaint adds regulatory pressure they do not want.

Second, their validation responses are often inadequate. Bulk purchased debt plus documented validation failures equals a high success rate when you push for specific documentation.

As the FTC's debt collection rights guide explains, you have the right to request written validation before making any payment decision. For collectors with documented validation failures like Resurgent, this request is not just a legal right , it is your most effective tool.

Can Resurgent Capital Services Be Removed From Your Credit Report

Yes. Multiple paths exist. The strongest paths for most Resurgent accounts are debt validation (their documentation is frequently incomplete), dual-entry dispute (LVNV and Resurgent both appearing for one debt), and obsolete debt challenge (original delinquency past seven years). CFPB complaints accelerate outcomes that bureau disputes alone miss. Pay-for-delete is possible , they paid 3-7 cents per dollar, so settling at 25-30 cents is still profit for them.

- Debt validation request. LVNV and Resurgent buy in bulk. Original documentation degrades at each sale. Many validation responses return generic summaries without chain-of-title documentation, original account agreements, or account-specific assignment records.

- Dual-entry FCRA dispute. When both LVNV and Resurgent appear for the same underlying debt, dispute both. Two entities cannot simultaneously and accurately report 100% of the same balance.

- Obsolete debt challenge. Average account age in ASAP's Q3 2025 review: 3.8 years. Some accounts are older. If original delinquency is more than seven years ago, the account must be removed regardless of anything else.

- Re-aging dispute. If the reported date looks newer than the actual original delinquency, dispute it as re-aging. Resurgent cannot reset the 7-year FCRA clock.

- CFPB complaint + bureau dispute combined. Filing both simultaneously produces faster outcomes. CFPB complaints create mandatory 15-day response requirements and federal regulatory pressure on top of the bureau's 30-day investigation window.

- Pay-for-delete (if debt is valid). Negotiate a written agreement before paying anything. They paid 3-7 cents per dollar. Settling at 25-30 cents is still profitable for them. Get bureau removal confirmed in writing as part of the agreement.

How to Remove Resurgent Capital Services , Step by Step

Get reports at AnnualCreditReport.com. Look for entries under "LVNV Funding," "Resurgent Capital Services," "Pinnacle Credit Services," and "Lighthouse Management Services." All are Sherman entities. The same underlying debt may appear under multiple names. Note the original delinquency date, the reported balance, and the account status on each entry. Compare each entry against the others for conflicts.

Free | Required first stepFind the original delinquency date , when you first missed payment on the original account. Not when the account was charged off. Not when LVNV purchased it. Count from that date. Past seven years: dispute as obsolete immediately. Approaching seven years: do not pay , let it age off. 2-6 years: proceed with validation and dispute. The date is the single most important number on the entire report entry.

This date controls everythingWithin 30 days of first contact, send a written validation request by certified mail. Address it to Resurgent Capital Services , they are the servicer and handle all collection correspondence. Request: original creditor name, original account number, complete chain of assignment from original creditor to LVNV, itemized balance accounting, and evidence the debt is within the FCRA reporting window. Keep the return receipt. Resurgent must cease collection activity until they respond.

Certified mail | 30-day FDCPA windowResurgent typically sends a response. Look at what it actually contains. Did they produce the original account agreement? The complete chain of ownership from the original creditor through to LVNV? A specific account number tied to the assignment? Account-specific ledger entries versus a generic balance summary? Gaps in any of these areas are grounds for the next step. The 2025 ASAP review showed average debt age of 3.8 years , records that old frequently do not survive the transfer process intact.

Gaps = bureau dispute groundsSubmit separate disputes to Equifax, Experian, and TransUnion. Attach the validation request you sent, Resurgent's incomplete response, and any specific inaccuracies , wrong dates, dual entries, balance discrepancies. Each bureau investigates independently within 30 days. If Resurgent cannot verify the specific account information during that window, the bureau must remove or correct the entry.

File all three bureaus separately | 30-day window per bureauDo not wait for bureau results before filing the CFPB complaint. File both simultaneously. The CFPB complaint creates a federal regulatory record. Resurgent must respond within 15 days. This pressure often produces faster resolution than the bureau investigation alone. Include the specific violation if known , debt parking (no prior notice), failure to validate, inaccurate reporting dates, time-barred debt without disclosure. The more specific, the more weight the complaint carries.

File at consumerfinance.gov | Mandatory 15-day Resurgent responseIf Resurgent violated the FDCPA , failed to disclose time-barred debt status, continued collecting after a validation request, reported before notifying you, or added unauthorized fees , document every violation with dates. Consumer protection attorneys handle Resurgent and LVNV cases frequently. Many work on contingency. A successful FDCPA claim against Resurgent entitles you to up to $1,000 in statutory damages plus attorney fees. Their enforcement history makes these cases attractive to consumer attorneys.

FDCPA: 1-year statute of limitations | FCRA: 2 yearsThe guide on what debt collectors must prove when you request validation covers the exact documentation standards Resurgent must meet , and what incomplete responses look like in practice.

What Resurgent Must Prove

Resurgent must produce: the name and address of the original creditor, the original account number, proof that LVNV legally owns the debt through a complete chain of assignment, an itemized accounting of the balance, and disclosure that the debt is time-barred if the statute of limitations has passed. A generic letter asserting the debt is valid is not validation. A balance summary without account-specific assignment documentation is not validation.

- Chain of title. From original creditor, through every intermediary, to LVNV. Each sale in the chain needs documentation that specifically identifies your account number.

- Original account agreement. The terms of the original account you allegedly owed. Without this, the balance itself cannot be verified as authorized.

- Itemized balance breakdown. Principal, interest, and fees , separately stated. Fees that were not authorized by the original agreement are disputable even if the underlying balance is valid.

- SOL disclosure. If the debt is past your state's statute of limitations, Resurgent must disclose this. The 2025 Oregon lawsuit against them specifically alleges they failed to do this on a 15-year-old debt. If they contacted you about old debt without that disclosure, that may be an FDCPA violation.

As NerdWallet's debt collection rights guide explains, consumers have the right to request debt validation in writing , and collectors must cease all collection activity until they provide adequate documentation. For Resurgent and LVNV, who purchase debt in bulk with limited original records, this requirement is where many disputes succeed.

Resurgent Capital Services and Lawsuits

Resurgent files collection lawsuits on behalf of LVNV Funding. They have over 254 documented federal court cases. They will sue , especially on debts within the statute of limitations. If you receive a court summons from Resurgent, a law firm they use, or Midland Funding (a related entity), respond in writing before the deadline. A default judgment from not responding gives them the ability to garnish wages and freeze bank accounts , even on debts they may not have standing to collect.

- If you receive a summons: respond within the deadline stated (14-30 days depending on state)

- Your response should assert: lack of standing to sue, SOL defense if applicable, and request for documentation proving ownership

- Resurgent has settled after filing lawsuits when consumers challenge their standing to sue in court

- The Maryland settlement confirms they have filed lawsuits without proper licensing in at least one state , challenging standing is a legitimate defense

- A consumer protection attorney who handles FDCPA and FCRA cases can respond to a Resurgent lawsuit for you , often at no upfront cost on contingency

Should You Settle or Dispute Resurgent Capital Services

| Your Situation | Best First Step | Why |

|---|---|---|

| Original delinquency past 7 years | Obsolete dispute immediately | Account must come off regardless of balance accuracy. Dispute as obsolete , no payment needed. |

| Both LVNV and Resurgent on report for same debt | Dual-entry FCRA dispute | Two entries for one debt is a reporting conflict. Dispute both simultaneously. |

| Debt is not yours | Dispute + CFPB complaint | Top CFPB complaint pattern. Dispute immediately. File CFPB complaint at the same time. |

| Reported without prior notice to you | Regulation F violation complaint | Debt parking is illegal. File CFPB complaint citing specific violation before anything else. |

| Debt is past statute of limitations | Validate + challenge SOL | Resurgent cannot sue on time-barred debt. Do not pay , may restart the clock in some states. |

| Debt is valid and within SOL and reporting window | Pay-for-delete in writing first | Get written agreement they remove all three bureau entries before sending a dollar. They paid 3-7 cents , they can accept 25-30 cents and still profit. |

Does Paying Resurgent Capital Services Help Your Score

Paying updates the account status from unpaid to paid. It does not remove the entry. The derogatory mark stays for seven years from the original delinquency. Score improvement from payment alone is minimal. What payment can do is satisfy a mortgage lender's requirement for resolution , but only if you know exactly what the underwriter needs before paying. Paying without a deletion agreement is the most common mistake. Do not do it.

Resurgent pays 3-7 cents per dollar for the debt. They profit enormously even on settlements.

That math is your negotiating position.

Before paying, try the dispute route. If dispute produces removal, you pay nothing and the entry disappears. If dispute does not produce removal and the debt is valid, negotiate a pay-for-delete. Get it in writing. Confirm Resurgent will remove both the LVNV entry and the Resurgent entry from all three bureaus upon payment.

Without that written agreement, payment resolves the balance , not the credit damage.

As Experian confirms in their charge-off guide, a paid collection still appears on your credit report and still signals a delinquency , the only difference is the account status label. For lenders reviewing the full tradeline, the derogatory nature of the account does not disappear with payment alone.

Understanding the full LVNV picture alongside this article , including how they handle collection lawsuits and bureau reporting , gives you the complete strategy. The ASAP guide to LVNV Funding specifically covers the collection arm in more detail since LVNV is the entity that appears on most credit reports even when Resurgent is the servicer you interact with.

What is the difference between LVNV Funding and Resurgent Capital Services?

LVNV Funding LLC is the legal owner of the debt. It appears on your credit report as the account creditor. It does not contact consumers directly. Resurgent Capital Services is the servicer , they make all calls, send letters, handle credit reporting, and file lawsuits on LVNV's behalf. Both are owned by Sherman Financial Group and based in Greenville, South Carolina. Your credit report may show LVNV Funding as the creditor while Resurgent Capital Services appears as the collection servicer , or both may appear as separate tradeline entries for the same underlying debt.

Can I dispute both LVNV Funding and Resurgent Capital Services at the same time?

Yes , and you should. If both appear for the same underlying debt, file separate FCRA disputes for each tradeline with each bureau showing them. The dispute for LVNV cites the dual-entry conflict and any reporting inaccuracies on that entry. The dispute for Resurgent cites the same conflict plus any additional reporting errors on their entry. Both disputes run independently. A CFPB complaint naming both entities creates regulatory pressure simultaneously.

Can Resurgent Capital Services sue me?

Yes, if the debt is within the statute of limitations in your state. Resurgent files lawsuits regularly on behalf of LVNV Funding. If you receive a summons, respond before the deadline. Assert lack of standing (they must prove LVNV legally owns the debt), statute of limitations defense if applicable, and request documentation proving ownership. A consumer protection attorney can respond on your behalf , often at no upfront cost. Never ignore a summons from Resurgent, their law firm, or any entity identifying itself as acting on LVNV's behalf.

Why did Resurgent appear on my credit report without notice?

Debt parking , reporting to credit bureaus before contacting the consumer , is prohibited under CFPB Regulation F, effective November 2021. Multiple 2024-2025 BBB and CFPB complaints describe exactly this experience with Resurgent and LVNV. If the account appeared on your credit report before you received any letter, call, or email from them, document the timeline. File a CFPB complaint citing the Regulation F violation. Include the date the entry appeared on your report and the date you received your first communication. This creates a federal regulatory record alongside your dispute.

-

Can RJM Acquisitions Be Removed From Your Credit Report? RJM Acquisitions is a zombie debt specialist , they specifically purchase time-barred accounts. The FTC investigated them in 2012. After that, RJM must disclose in writing that debt is past the SOL and they cannot sue. The removal strategy differs from Resurgent because RJM's reach is limited to credit reporting only. No lawsuits. No calls. Just the bureau entry , which makes the dispute path even more straightforward than Resurgent accounts.

-

How to Remove Portfolio Recovery Associates From Your Credit Report PRA is the largest debt buyer in the US with over $51M in CFPB fines. Like Resurgent, they buy debt in bulk and often cannot produce complete chain-of-title documentation. This covers the full dispute process for PRA including their settlement vs dispute comparison, FDCPA counterclaims, and why their documentation history makes validation requests effective. The strategy applies directly alongside your Resurgent dispute.

-

How to Remove Midland Credit Management From Your Credit Report Midland Credit Management (Encore Capital Group) files 500 lawsuits per week in some states. They also paid $15M for robo-calling violations. Like Resurgent, they are an aggressive litigator with documented enforcement problems. This covers the TCPA claim angle most consumers miss, the lawsuit response framework, and why Midland's documentation gaps create the same validation dispute opportunities as Resurgent accounts.