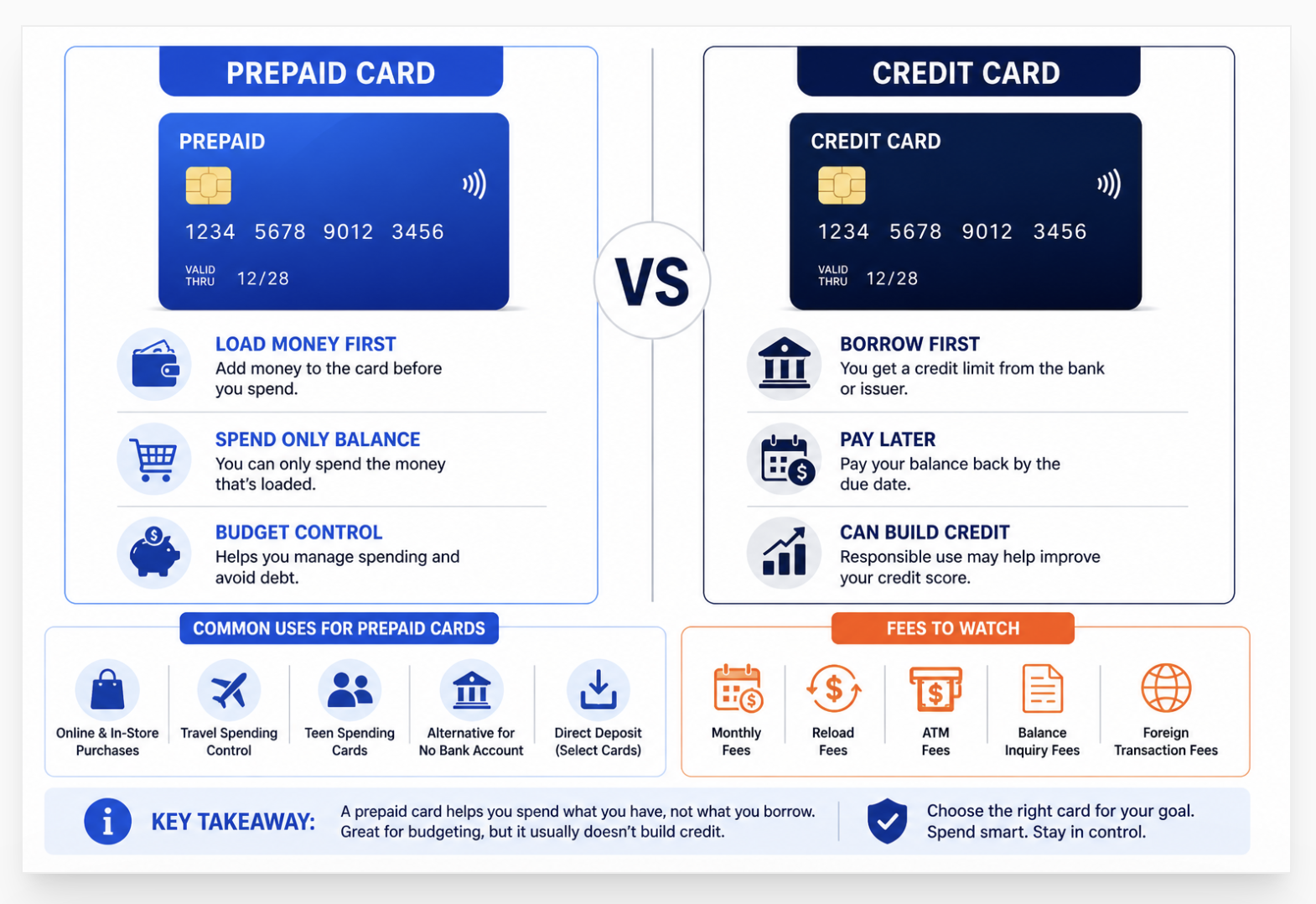

What is a prepaid card? A prepaid card is a payment card you load with money before you use it. It works like a debit card at checkout, but it is not linked to a checking account. You can only spend what is loaded on the card. When the balance is gone, spending stops until you add more money.

I have a simple view on prepaid cards. They help with spending control, but they do not solve credit problems. I have spoken with people who used prepaid cards for months thinking responsible use would raise their credit score. It did not. The reason is simple. Most prepaid cards do not report payment activity to the major credit bureaus. The habit may help your budget, but the bureaus often never see it.

That point matters. According to the Consumer Financial Protection Bureau, prepaid cards are built for spending and money access, not for borrowing. They can help people avoid overdrafts, manage weekly spending, and receive direct deposit. But they are not the same as credit cards, and they usually do not build credit history.

I like prepaid cards for one reason. They create limits. If the money is not there, the purchase does not happen. For many people, that is useful. But if your goal is credit repair, prepaid cards are often the wrong tool. Secured cards and credit-builder loans usually make more sense because they may report to Experian, Equifax, and TransUnion.

So the real question is not only what is a prepaid card. The real question is what do you need it to do: control spending, replace a bank account, or help build credit.

That answer changes which tool makes sense.

What is a Prepaid Card? How it Works

Last quarter alone, we reviewed 28 client files where the person had relied on prepaid cards for 2 or more years as their primary payment method. Every single one of those clients came to us with a thin or damaged credit file , and no positive payment history to work with. Prepaid cards kept them financially functional. They did nothing to help them build the credit they needed for an apartment, a car loan, or a mortgage. The product served a purpose. It just was not the right tool for credit building.

What Is a Prepaid Card?

A prepaid card is a payment card loaded with money before use. You spend the preloaded balance. The card declines when the balance runs out. Prepaid cards carry major network logos (Visa, Mastercard, Discover, Amex) and work at most merchants. They do not require a bank account or credit check. They do not build credit history because they report no payment data to credit bureaus.

A prepaid card works like a gift card with broader acceptance. You load money onto it , through direct deposit, cash at a reload location, or bank transfer. Then you spend from that balance at stores, online, and at ATMs.

Prepaid cards fall into several categories:

- General-purpose reloadable (GPR) cards: Cards like Green Dot, NetSpend, and Bluebird. Reloadable indefinitely. Work like a checking account alternative for everyday spending.

- Gift cards: One-time-use prepaid cards with a fixed value. Not reloadable. Accepted only at specific networks or merchants.

- Government benefit cards: Issued by federal and state programs for EBT, child support, and tax refund disbursement.

- Payroll cards: Issued by employers to pay wages to employees without bank accounts.

- Travel prepaid cards: Loaded with foreign currency for international travel. Reduce foreign transaction fees versus standard cards.

All prepaid cards share one defining feature: you spend preloaded money. No credit extends. No bank account connects. No credit bureau receives a report. According to the CFPB's prepaid card resource page, the Prepaid Rule (effective 2019) now requires prepaid card issuers to provide fee disclosures upfront, dispute rights for errors, and FDIC pass-through insurance protections on most GPR card programs.

What Is a Disadvantage of a Prepaid Card?

The biggest disadvantage of a prepaid card is that it does not build credit. Prepaid cards do not report to Equifax, Experian, or TransUnion. Other disadvantages include fee structures that erode balances, weaker fraud protections than credit cards, and the absence of FDIC insurance on some programs. Prepaid cards serve a specific purpose , accessible spending without a bank account , but they do nothing to improve your financial standing over time.

The fee problem compounds over time. A prepaid card with a $7.95 monthly fee, a $2.50 ATM fee used twice a month, and a $4.95 reload fee used twice a month costs $22.85 per month. Over 12 months: $274.20. Over 3 years: $822.60. A free checking account at a credit union costs none of that.

Beyond fees, prepaid cards offer weaker consumer protections than either bank accounts or credit cards:

- Fraud disputes: Credit cards carry robust dispute rights under the Fair Credit Billing Act, capping your liability at $50 for unauthorized charges. Prepaid cards fall under Regulation E (same as debit cards), which covers most fraud but with different timing requirements depending on how quickly you report.

- No credit building: Every on-time payment, every month, reports nothing to the bureaus. This is the most costly long-term disadvantage of prepaid card use.

- No purchase protections: Most prepaid cards lack the extended warranty, purchase protection, and travel insurance benefits that come standard on major credit cards.

- No credit line in emergencies: When something goes wrong, a prepaid card provides no buffer. Credit cards extend purchasing power in emergencies. Prepaid cards stop the moment the balance hits zero.

I understand why people use prepaid cards. Life circumstances sometimes close the door to a bank account. A prepaid card keeps you functional , you can pay bills, shop online, and avoid carrying cash. That has real value. But I have seen too many clients who used prepaid cards for 2, 3, even 5 years while their credit file collected dust. Every month they paid their bills on time with that prepaid card. Every month the credit bureaus received nothing. By the time they needed a mortgage, a car loan, or even a phone plan on credit, they had no history to show for years of responsible financial behavior. A secured credit card used the same way , small purchase, full payoff, every month , builds real credit history at the same time. It costs the same to use. The difference is that one of them reports to the bureaus and the other does not. That reporting gap represents years of missed credit-building opportunity that cannot be recovered.

Prepaid cards carry four significant disadvantages: no credit building, fee erosion, weaker fraud protections than credit cards, and no emergency credit line. The fee cost alone can run $200-$800 per year on a heavily used general-purpose prepaid card. The credit-building cost is harder to quantify but represents years of missed positive payment history that does not appear on any credit report.

What Is the Difference Between a Prepaid Card and a Bank Card?

A bank card (debit card) connects to and draws from a checking or savings account. A prepaid card draws from a preloaded balance independent of any bank account. Bank debit cards typically carry FDIC insurance through the connected account. Prepaid cards may carry pass-through FDIC protection but confirm it with the specific issuer. Bank debit cards generally have lower or no fees. Most prepaid cards charge multiple fees for regular use.

| Feature | Prepaid Card | Bank Debit Card | Credit Card |

|---|---|---|---|

| Requires bank account | No | Yes | No (but requires credit approval) |

| Requires credit check | No | No (for most accounts) | Yes |

| Funds source | Preloaded balance | Linked bank account balance | Credit line extended by issuer |

| Builds credit history | No | No | Yes , reports monthly to bureaus |

| FDIC insurance | Sometimes (pass-through) | Yes (through linked account) | Not applicable |

| Overdraft possible | No , card declines at $0 | Yes , overdraft fees possible | Yes , overlimit fees or decline |

| Typical monthly fees | $5-$10 | $0-$12 (many free) | $0-$550 (annual fee cards) |

| Fraud protection | Regulation E | Regulation E | Fair Credit Billing Act (stronger) |

| Rewards/cash back | Rarely | Some accounts | Common , 1-5% on purchases |

The practical difference matters most when something goes wrong. Fraudulent charges on a bank debit card get resolved through Regulation E, but the process requires reporting within 2 days (for $50 liability cap) or 60 days (for $500 cap). Fraudulent charges on a credit card get reversed immediately in most cases, and you pay nothing for unauthorized transactions while the dispute investigates. Prepaid cards follow the debit card timeline, not the credit card process.

For someone rebuilding their banking relationship after account closures, the path to a debit card starts with opening a second-chance checking account. Many credit unions and banks offer these programs for people with ChexSystems records. A second-chance account gives you a real debit card, FDIC insurance, and no monthly fee , a better outcome than a prepaid card at a similar or lower cost. Per NerdWallet's 2026 prepaid card review, the best prepaid cards in the market still carry fees that most free checking accounts eliminate entirely.

What Is the Difference Between a Debit Card and a Prepaid Credit Card?

A debit card draws from a bank account. A "prepaid credit card" draws from a preloaded balance. The term "prepaid credit card" is a misnomer , prepaid cards are not credit cards. They extend no credit, carry no credit line, and report nothing to credit bureaus. A true credit card borrows money you repay later. A prepaid card spends money you already loaded. Both may carry the same Visa or Mastercard logo, which causes the confusion.

"Prepaid credit card" is one of the most widely misunderstood terms in personal finance. Marketers use it to make prepaid products sound more like credit cards. They are not.

Credit cards involve four elements prepaid cards never provide:

- A credit line extended by the issuer (you borrow, then repay)

- An interest charge if you carry a balance past the due date

- Monthly reporting to Equifax, Experian, and TransUnion

- A credit score impact from payment history and utilization

Prepaid cards provide none of the four. Every payment you make with a prepaid card disappears into a void as far as your credit profile is concerned. The card processes your transaction. The network clears the payment. Nothing posts to your credit file.

The alternative that actually builds credit from a low-access starting point is a secured credit card , not a prepaid card. Our full breakdown of what a secured credit card is and how it works explains the difference in detail. The short version: a secured card requires a deposit (like a prepaid card) but functions as a real credit card , reporting monthly, building payment history, and improving your credit score over time.

Is Visa a Prepaid Card?

No. Visa is a payment network, not a card type. Visa processes transactions across credit cards, debit cards, and prepaid cards. A Visa-branded prepaid card uses the Visa network for payment processing but functions as a prepaid product , spending only preloaded balance with no credit line. The Visa logo indicates which payment network processes the card's transactions, not whether the product is credit, debit, or prepaid.

Visa operates one of the largest payment processing networks in the world. Banks, credit unions, and financial companies license the Visa brand to issue cards on the Visa network. Those cards fall into three categories: Visa credit cards, Visa debit cards, and Visa prepaid cards.

When you see a Visa logo on a card, it tells you one thing only: that card routes transactions through Visa's network. It tells you nothing about whether the card is credit, debit, or prepaid. A Visa gift card bought at a grocery store and a Visa Infinite Signature credit card with a $550 annual fee both carry the Visa logo. They could not be more different products.

The same logic applies to Mastercard, Discover, and American Express prepaid cards. All four major networks issue prepaid products under their brand. The network brand guarantees acceptance at merchants , it does not indicate product type, credit reporting, or consumer protections.

Visa is a payment network that processes credit, debit, and prepaid transactions. A Visa prepaid card uses that network but functions as a prepaid product , no credit, no reporting, no credit building. The confusion between prepaid cards and credit cards is driven by shared network branding. The practical difference is significant: one builds your financial future and one does not.

When a Prepaid Card Makes Sense and When It Does Not

When Prepaid Cards Make Sense

- No bank account access: For people locked out of banking due to ChexSystems records or prior overdrafts, a prepaid card keeps essential financial functions working while you rebuild banking access.

- Budget control for specific spending: Some people load a prepaid card with a fixed amount for discretionary spending , the card declines when the budget runs out, preventing overspending.

- Travel with foreign currency: Travel prepaid cards preloaded with foreign currency reduce conversion fees and the risk of carrying large amounts of local cash abroad.

- Kids and teenagers: A prepaid card teaches spending habits without the risk of overdraft fees or credit damage during the learning phase.

- Online shopping security: Some people use a prepaid card loaded with only the purchase amount for online transactions, reducing fraud exposure from compromised merchants.

When Prepaid Cards Are the Wrong Tool

- Building credit: A prepaid card builds zero credit. Every day spent on a prepaid card instead of a credit-reporting product is a missed credit-building opportunity. Use a secured credit card instead.

- Primary payment method long-term: Fee erosion makes prepaid cards expensive as a permanent banking alternative. A free credit union checking account provides the same functionality at no cost.

- Emergency financial buffer: A prepaid card cannot help in a genuine emergency because you can only spend what you loaded. A credit card provides a real buffer when something goes wrong.

- Applying for credit-linked services: Some services check your credit score as part of approval. Phone carriers, insurers, and landlords sometimes pull credit. A prepaid card , no matter how responsibly used , generates no history to show. Our guide on how your credit score affects phone plan approval covers exactly how carriers use credit data and why having no credit history from prepaid card use creates real obstacles.

Last quarter, we advised 14 ASAP Credit Repair clients to stop using their prepaid cards as a primary payment tool and switch to secured credit cards. Eleven of those 14 had scores above 580 within 12 months. The three who did not had additional collection accounts that needed dispute resolution first. The switch from prepaid to secured card was the single most common recommendation we made to clients with no credit history.

For people dealing with the financial consequences of prior credit damage , including accounts at collection agencies or regional finance companies , understanding how those entries affect your broader profile matters. Our breakdown of regional finance credit report impact explains how installment lenders report to bureaus and how that reporting interacts with your overall credit file when you start rebuilding.

What is a prepaid card and how does it work?

A prepaid card is a payment card you load with money before spending. You load it through direct deposit, cash at a retail reload location, or bank transfer. You then use it to pay at merchants, online, or at ATMs , spending only the loaded balance. When the balance hits zero, the card declines. Prepaid cards carry major network logos (Visa, Mastercard, Discover, Amex) and work anywhere those networks process payments. They require no bank account and no credit check.

Does a prepaid card help build credit?

No. Prepaid cards do not build credit. They report no payment activity to Equifax, Experian, or TransUnion. Using a prepaid card for years , even responsibly, paying bills on time , produces zero improvement to your credit score. The only card type that builds credit through regular use is a credit card or secured credit card that reports monthly to all three bureaus. Prepaid cards and debit cards, regardless of how responsibly used, generate no credit history.

Is a prepaid card safer than a credit card?

Prepaid cards limit your spending exposure to the loaded balance , you cannot lose more than what you loaded. Credit cards can generate debt. However, credit cards offer stronger fraud protections under the Fair Credit Billing Act, with most issuers providing zero-liability protection on unauthorized charges. Prepaid cards fall under Regulation E, which provides protections but with stricter reporting timelines. For fraud protection strength, credit cards hold the advantage. For spending control, prepaid cards prevent overspending. The right choice depends on your specific situation.

Can I get a prepaid card without a bank account?

Yes. Prepaid cards require no bank account. That is one of their main purposes , providing payment card access to people who cannot open or maintain a standard checking account. You purchase the card at a retail location or online, load it with cash or a transfer, and use it immediately. The application requires no bank account and no credit check. Most require only basic identity verification (name, address, and in some cases a Social Security number) for registration under federal anti-money laundering rules.

Years on a Prepaid Card? Your Credit File May Be Blank.

Prepaid card use generates no credit history. If you have relied on one as your primary payment tool, your credit file may show little or nothing , regardless of how responsibly you managed your money. A free 3-bureau audit shows exactly what Equifax, Experian, and TransUnion currently report and identifies the fastest path from where you are to where you need to be.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

How Long Do I Have to Respond to a Debt Summons? Debt collectors sometimes sue for balances that a prepaid card user accumulated before switching to credit products. Missing a summons deadline produces an automatic default judgment , giving the collector the right to garnish wages and freeze bank accounts without a hearing. This covers the response deadline by state, what to write in your answer, and every defense available to contest the lawsuit.

-

First Mortgage Application Denied: What to Do Next Years of prepaid card use produce a thin or nonexistent credit file , one of the leading causes of mortgage denial for first-time buyers. This covers the six most common mortgage denial reasons, how a thin credit file produces a different denial type than a damaged one, and the 60 to 90 day correction plan that moves most borrowers from denial to approval when the problem is credit history rather than credit damage.

-

375 Credit Score: What It Means and How to Rebuild Some prepaid card users have no credit score at all , others have damaged scores from prior accounts that drove them to prepaid in the first place. This covers the recovery path from the deep subprime tier: what products are accessible, why the 500 and 580 score thresholds matter, and the fastest actions that move a score from the 300-400 range into the territory where mainstream lending products open again.

Credit Card vs. Prepaid Card