I remember the first time I got a CCS notice—my heart raced.

Seeing that Credit Collection Services (CCS) was reaching out to collect a debt from me, I instantly felt overwhelmed.

What was this all about?

Did I really owe money?

Is CCS collections real or fake?

The panic I felt was real, but what I learned through the process was that handling a CCS notice doesn’t have to be as scary as it seems.

If you’ve received a CCS notice text message, I’ve been in your shoes.

Disclaimer: The information below is for general knowledge and informational purposes only and does not constitute legal or financial advice. If you have received a CCS notice, it's essential to verify the legitimacy of the debt and understand your rights. Consulting with a legal or financial professional is highly recommended. While we strive to offer accurate and up-to-date content, the topics discussed are subject to change and may not be applicable to your specific situation.

Here’s how I handled the situation, along with tips I wish I’d known from the beginning.

My hope is that sharing my experience and the steps I took will not only ease your stress but also help you take control of your debt situation.

What Is a CCS Notice?

Let’s start with the basics—what is a CCS notice?

When I got mine, I had no idea what Credit Collection Services was or why they were contacting me.

CCS is a third-party debt collection agency.

When companies, like credit card issuers, utility providers, or medical offices, have trouble getting customers to pay their bills, they might sell the debt to a company like CCS.

Who Is CCS: Credit Collection Services?

CCS, or Credit Collection Services, is one of the largest third-party debt collection agencies in the United States.

They specialize in collecting overdue accounts on behalf of various businesses, including credit card companies, utility providers, auto lenders, and healthcare facilities.

Essentially, when an original creditor—like a credit card company or a medical office—has difficulty getting a customer to pay their bill, they may sell or transfer the debt to CCS.

CCS then takes on the responsibility of collecting the amount owed.

CCS operates out of Norwood, Massachusetts, and has been in the business of debt collection for decades. They are known for managing both consumer and commercial debts, meaning they collect not only from individual consumers but also from businesses that owe money.

What Types of Debts Does CCS Collect?

When you receive a CCS notice letter, it could be tied to several types of debt, including:

- Credit card debt

- Medical bills

- Utility bills (such as electricity, gas, or water)

- Auto loans

- Telecommunication bills (like unpaid phone or internet services)

- Retail or personal loans

Because CCS handles a wide range of accounts, it’s not unusual to receive a notice from them even if you’ve never heard of the company before.

That was the case for me—I had never interacted with CCS directly until they reached out regarding a debt I owed to a different company.

Why Did CCS Contact Me?

Simple. You get those collection calls from them because of debt.

They are legally allowed to contact you about this debt and attempt to collect it.

What you should do when you receive a notice from CCS is to first verify that the debt is legitimate (which I talked about earlier) and then decide how to respond based on your financial situation.

We’ll be expanding this topic on the next section.

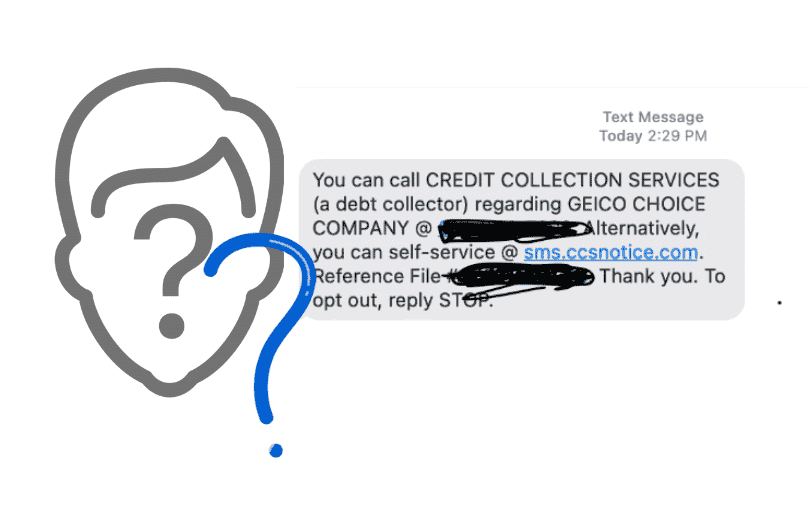

What To Do When You Get a CCS Notice

I figured out that upon receiving a notification from CCS, I have to act fast.

So the CCS notice listed the debt amount, the original creditor, and how to contact CCS.

I get to note all of those information.

This is important information because understanding the basics of the debt is your first step toward resolving it.

Let me share with you guys how I take a CCS Notice.

1. Stay Calm and Don’t Ignore It

I’ll admit—my initial reaction was to shove the letter into a drawer and forget about it.

But after doing some research, I quickly realized that ignoring a CCS notice is the worst thing you can do.

When debt collectors don't hear from you, they might take further action, which can include reporting the debt to credit bureaus, negatively impacting your credit score, or even pursuing legal action.

Instead of panicking, take a deep breath, read the letter carefully, and make note of key information like the amount owed, the due date, and the original creditor.

This is the foundation for how you’ll respond.

What Happens If You Ignore CCS?

So if you ever wondered what would happen if you just ignored CCS?

Trust me, that turns out that's not the best idea. Here's why:

- Credit damage: Ignoring CCS doesn’t make the debt go away. It stays on your credit report and can really lower your credit score, which makes it harder to get loans or even a credit card in the future.

- More collection efforts: If you ignore them, CCS might keep trying to contact you, and they can report the debt to credit bureaus, which only makes things worse.

- Legal action: In some cases, if you don’t respond, they could take legal action to collect the debt. That means they might sue you, and if they win, they could garnish your wages.

It's always better to handle the situation before it gets out of control. I learned that dealing with it upfront saved me a lot of stress later.

2. Verify That the Debt Is Legitimate

One of the first things I did was ask myself, “Is this CCS notice legit?, “Do I really owe this debt?”

Just because you receive a notice doesn’t automatically mean you’re responsible for paying it. Debt collectors sometimes make mistakes. They could be trying to collect on an old debt or even one that’s not yours.

In my case, I wasn’t entirely sure the debt was accurate.

So, I sent a debt validation letter to CCS.

This is a formal way of asking them to prove that the debt is legitimate and that you owe the amount they’re asking for. They’re legally required to respond and provide details like who the original creditor is, when the debt was incurred, and how much is owed.

About two weeks later, CCS responded with the necessary documents, which allowed me to confirm that the debt was indeed mine.

This step is crucial because, if you find discrepancies, you can dispute the debt and potentially remove the debt from your record.

The Legitimacy of CCS Collections

While I was dealing with my own debt collection, I realized that there’s a fine line between legitimate collection efforts and scams.

It’s so important to be able to identify the authenticity of CCS communications and ensure that you aren’t being targeted by fraudulent activity.

Evaluating the Authenticity of CCS Payments

The first thing I did when I received a payment request from CCS was verify its legitimacy.

You should make sure that CCS sends you a Notice of Debt within five days of their first contact. I took this as my chance to request documentation that verified the debt.

You’ll want to carefully review this for any inconsistencies. If you have doubts, sending a debt validation letter within 30 days is your best bet to request proof that the debt belongs to you.

I found out that while most CCS collections are legitimate, it’s always a good idea to verify any payment request before moving forward.

Scammers sometimes try to pose as collection agencies, and you definitely don’t want to fall victim to fraud.

One thing I did was contact the original creditor directly to confirm that they had transferred my account to CCS.

Distinguishing Real from Fake CCS Communications

One of the scariest parts of my experience with CCS was worrying whether I was being scammed. With so much fraud out there, it can be hard to know who to trust. Here’s what I learned that helped me feel more confident:

- Look for detailed information: Legitimate CCS communications will always provide clear details about the debt, including the original creditor, the amount owed, and your options to dispute it. If any of this information is missing or seems vague, that’s a red flag.

- Watch out for scammers: Some fraudsters use similar logos or names to trick people into paying fake debts. It’s crucial to double-check any communication you get, especially if something seems off. Scammers rely on people acting too quickly without verifying.

- Never give personal info: One thing I made sure of was to never provide personal information or make any payments before verifying the legitimacy of the communication. Scammers love to prey on people who panic and give up their info without asking questions first.

- Visit their official website: If you’re still unsure, you can always go to their official website, www.ccspayment.com online, to check your account and confirm the debt. This gives you an extra layer of security, ensuring you're on the real Credit Collection Services website.

3. Know Your Rights Under the FDCPA

As I faced my CCS notice, I learned something valuable: you have rights when dealing with debt collectors.

Under the Fair Debt Collection Practices Act (FDCPA), there are limits to what CCS (or any collection agency) can do.

They can’t harass you, threaten you, or call you at odd hours of the day. They also can’t lie about the amount you owe or misrepresent the legal status of your debt.

Here are a few key rights I learned about:

- No Harassment: Debt collectors cannot use abusive language or make repeated phone calls to annoy you.

- Transparency: They must tell you the exact amount you owe, who you owe it to, and how you can dispute the debt.

- Privacy: They can’t talk about your debt with anyone else, except your spouse or attorney.

Arming myself with these rights gave me the confidence to move forward without feeling intimidated.

If you’re dealing with CCS, knowing what they can and cannot do will empower you to take control of the situation.

4. Evaluate Your Options for Handling the Debt

Once I verified that the debt was legitimate, I had to decide how to handle it. And here’s the thing—there’s no one-size-fits-all solution. It all depends on your financial situation.

Let’s explore the main options.

- Pay the Debt in Full: This is the quickest way to resolve the situation and stop any collection efforts. If you’re financially able, paying the full amount is the most straightforward option. This can also protect your credit score from further damage. However, not everyone has the cash on hand to pay off a large debt immediately.

- Set Up a Payment Plan: This is what I ultimately chose. I wasn’t in a position to pay the full amount, so I reached out to CCS and negotiated a payment plan that fit my budget.

- Negotiate a Settlement: If you can’t pay the full amount but have some funds available, you might consider negotiating a settlement. This means offering to pay a portion of the debt in exchange for CCS considering it fully paid. Sometimes, collection agencies will accept less than what’s owed to close the account. However, this could still negatively affect your credit score, so keep that in mind.

- Dispute the Debt: If you believe the debt is inaccurate, outdated, or doesn’t belong to you, you can dispute it with CCS and the credit bureaus.

How Do I Remove CCS from My Credit Report?

Did you know that you can easily remove ccs from your credit report?

Here's how I went about it:

- Check the debt: First, I made sure the debt was real by asking CCS for a debt validation letter. You have the right to ask them to prove the debt is yours.

- Dispute errors: If there’s any mistake, you can dispute it with the credit bureaus. I wrote a letter to explain why the debt was wrong and included proof. The credit bureau has 30 days to investigate.

- Pay off the debt: If the debt is real, paying it off might help. Sometimes, you can ask CCS to remove it from your report if you pay. This is called "pay for delete," but remember, not all agencies agree to it.

- Wait for it to drop off: If you can't pay or settle the debt, it will eventually drop off your credit report after seven years. However, during that time, it can hurt your credit score, so it's best to deal with it sooner.

5. Get Everything in Writing

One thing I can’t stress enough: always get everything in writing.

Whether you’re setting up a payment plan, negotiating a settlement, or disputing a debt, having documentation is crucial.

This protects you if there are any issues later on.

When I set up my payment plan, I made sure to get written confirmation from CCS detailing the terms. I also saved all my communication with them, including emails and notes from phone calls.

Keeping thorough records ensured that I had proof of every step I took in case any problems arose.

6. Monitor Your Credit Report

As I share my situation, you already know by now that the way I handled my CCS notice was to pay them.

Once I completed my payment plan, I didn’t just assume everything was fine—I monitored my credit report to make sure CCS had accurately reported the debt as paid.

You’re entitled to one free credit report from each of the major bureaus—Experian, Equifax, and TransUnion—every year, and it’s a good idea to take advantage of this.

In some cases, mistakes can happen, and a paid debt might still show up as unpaid on your credit report. If that happens, you can file a dispute with the credit bureau to have the error corrected.

How CCS Collections Affects Your Credit Score

One of my biggest concerns was how this whole situation would affect my credit score.

Having CCS collections show up on your credit report can be damaging. Even if you plan to resolve the debt, just having the account in collections can drop your score significantly. That’s why acting quickly is key.

I learned that CCS collections can remain on your credit report for up to seven years if left unresolved, which can make it much harder to qualify for loans, credit cards, or even a mortgage.

To minimize the impact on your score, you’ll want to remove CCS collections from your credit report as soon as possible.

Here’s what worked for me:

- Respond Quickly: The sooner you resolve the debt, the less damage it can do to your credit.

- Negotiate “Pay-for-Delete”: This is an agreement where the collection agency removes the negative item from your credit report in exchange for payment. While not all agencies will agree to this, it’s worth asking.

- Monitor Your Credit: After resolving the debt, keep a close eye on your credit report to ensure that CCS accurately reports the account as “paid” or “settled.”

By staying proactive, I was able to reduce the negative impact on my credit score and prevent further damage.

Final Thoughts: Take Control of Your CCS Notice

Receiving a CCS notice is stressful, but it’s not something you have to face alone or ignore. By verifying the debt, knowing your rights, and acting quickly, you can take control of the situation and resolve the debt in a way that works for you.

Looking back, I’m glad I took the time to understand the process and explore my options.

By doing so, I avoided further damage to my credit and gained peace of mind. If you’ve received a CCS notice, I hope my experience gives you the confidence to tackle it head-on.

You have more control than you think, and with the right approach, you can turn a challenging situation into a manageable one.

Need Help? Contact ASAP Credit Repair Today!

If you're feeling overwhelmed by CCS or any other debt collections, ASAP Credit Repair is here to help.

Our team specializes in handling credit repair and guiding you through the process, step by step. We’ll work with you to improve your credit score and put you on the path to financial freedom.

Don’t let debt collections bring you down—reach out today and take the first step toward a better credit future!