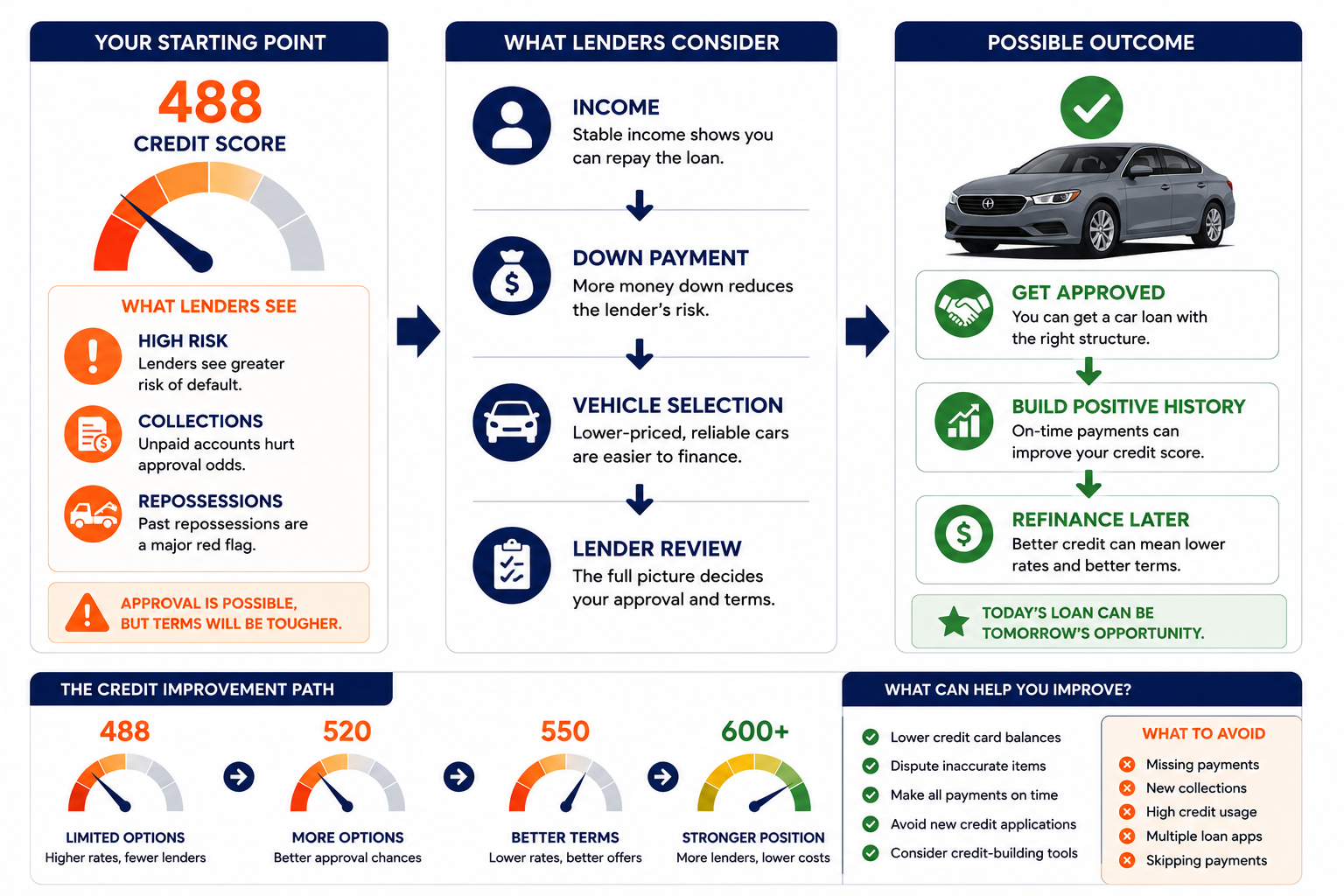

A 488 credit score is not a great place to start when you're shopping for a car.

But it does not automatically mean you're out of options.

The bigger challenge is not getting approved.

It's getting approved without accepting a loan that becomes a financial burden later.

We just had a situation like this in our Houston office. I've seen borrowers focus so much on hearing "yes" from a dealership that they never ask a second question:

What is this loan actually going to cost me?

That matters.

At a 488 credit score, lenders usually see elevated risk. That often leads to higher interest rates, larger down payment requirements, and stricter approval conditions.

What I want to tell you (that's why I created this content) is that approval is still possible in many cases.

The better news is that some borrowers can improve their financing options faster than they think.

Can You Get a Car Loan With a 488 Credit Score in Houston?

Yes, it is possible to get a car loan in Houston with a 488 credit score. However, borrowers in this range typically receive subprime financing offers and may face higher interest rates, larger down payments, and more lender requirements.

Can You Realistically Get Approved With a 488 Credit Score

Yes , but not through most standard lenders. A 488 score sits in Experian's deep subprime tier (300-500). That tier closes the door at most banks, credit unions, and traditional dealership financing. The doors that remain open include subprime specialty auto lenders, Buy Here Pay Here dealers, and some dealerships with relationships with Credit Acceptance Corporation or Westlake Financial. Approval at 488 is real. The terms at 488 are expensive.

As NerdWallet's 2026 auto loan rate analysis confirms, scores below 501 face the highest auto loan rates in the market and the most limited options. Houston has a large and active subprime auto market. That matters.

Larger cities mean more dealer inventory, more subprime finance options, and more competition among BHPH operators. A 488-score buyer in Houston has more choices than the same buyer in a small Texas town. That does not mean those choices are all good. It means there are more of them , and comparing terms before signing matters even more.

- Subprime specialty lenders. Companies like Credit Acceptance Corporation, Westlake Financial, and DriveTime partner with dealerships specifically to fund deep subprime buyers. They charge high rates but have legitimate reporting to all three bureaus. Consistent payments build credit history.

- Buy Here Pay Here dealers (BHPH). Houston has many BHPH operators. They hold the loan themselves rather than selling it to a lender. Approval is typically based on income and down payment, not credit score. Trade-off: some do not report to credit bureaus. Confirm before signing that the dealer reports to Equifax, Experian, and TransUnion.

- Credit unions. A few Texas-based credit unions work with members who have challenged credit. BHPH rates may still be lower through a credit union auto loan program. Check with any existing credit union membership before visiting a dealer.

What Auto Lenders See When They Review a 488 Credit Score

Lenders do not just see the number 488. They see the file behind it. A 488 from one missed payment two years ago looks different from a 488 with three collections, an unpaid repossession, and 90% credit card utilization. The score starts the review. The file finishes it. At 488, lenders are specifically evaluating whether the borrower has stable income that supports the payment , because that is now the primary approval criterion.

- Payment history. Recent lates are more damaging than old ones. A 30-day late from six months ago matters more than a charge-off from four years ago. Subprime lenders look at the pattern: is this person currently managing their obligations?

- Repossessions. An auto repossession in the last 24 months is the hardest single item to overcome. It tells an auto lender that this borrower already defaulted on a car loan. Most subprime lenders require at least 12-24 months post-repossession before approving another car loan. BHPH dealers are more flexible but charge accordingly.

- Collections. Multiple open collections signal ongoing financial difficulty. One or two old paid or disputed collections are less concerning than three or four active collection accounts from the last year.

- Debt-to-income ratio. Subprime lenders often place more weight on DTI than on the credit score itself. The payment on the car loan plus all existing monthly obligations must fit within an acceptable percentage of gross monthly income , typically 40-50%.

- Income stability. Consistent income from the same source for 6-12 months is a major positive. Lenders want W-2 employment or documented consistent self-employment income. Gig economy income, recent job changes, or inconsistent deposits create friction.

Why Some 488 Borrowers Get Approved and Others Don't

Two borrowers can both score 488. One gets approved. The other does not. The score is not the deciding factor. Income, down payment, vehicle selection, and credit file details determine the outcome. Lenders at this credit tier have approved borrowers with scores below 500 who had strong income and 20% down , and declined borrowers at 510 who had a recent repossession and no verifiable income.

The 488 score is a threshold marker. It tells the lender which financing category to use. It does not tell the lender whether to approve the file.

The approval or denial comes from what is behind the score , and from what the borrower brings to the table in terms of income, down payment, and vehicle choice.

What Interest Rates Should You Expect

According to Experian Q4 2025 automotive data, deep subprime borrowers average 21.58% APR on used cars. Do not expect an exact rate before applying. Rates change daily. What the Experian data shows is positioning: 488 sits in the tier that averages 21.58% APR for used cars and 16.01% for new. You will not qualify for new car financing at most dealerships. Used cars are the realistic market. Compare offers from at least two or three lenders before signing. A one or two point APR difference on $15,000 over 60 months is $1,000 to $2,000.

| Credit Tier | Score Range | Avg New Car APR | Avg Used Car APR |

|---|---|---|---|

| Super Prime | 781-850 | 4.66-5.18% | 6.82-7.13% |

| Prime | 661-780 | ~7-9% | ~9-11% |

| Nonprime | 601-660 | ~10-13% | ~12-15% |

| Subprime | 501-600 | 13.18-13.34% | 18.86-19.00% |

| Deep Subprime | 300-500 (488 is here) | 15.81-16.01% | 21.58-21.60% |

How Much Down Payment Helps With a 488 Credit Score

Down payment is one of the most powerful approval variables at 488. A larger down payment reduces the loan-to-value ratio , the percentage of the car's value the lender is financing. Lower LTV means less lender risk. At 488, where the credit score already signals risk, a meaningful down payment is often what moves a file from declined to approved. Most subprime lenders want 10-20% down. BHPH dealers may require 20-25%.

Down payment also reduces the total amount financed. At a 21% APR, every $1,000 less borrowed saves approximately $630 in interest over 60 months. Saving an additional $1,500 in down payment before applying produces better approval odds AND lower monthly cost simultaneously.

One more thing: trade-ins count. If a current vehicle has equity , worth more than the payoff balance , that equity functions as down payment. Know the trade-in value before visiting a dealer. Check Carmax, CarGurus, or Carvana online offers to establish a realistic baseline.

Can Collections or Repossessions Affect Approval

Yes , and at 488, they often matter more than the score itself. A recent repossession is the single hardest barrier to auto loan approval in this credit tier. Most subprime lenders require 12 to 24 months of payment history after a repossession before approving a new auto loan. Collections are less immediately blocking , but multiple open collections in the last 12 months signal ongoing financial difficulty that compounds the score concern.

- Repossession within the last 12 months. Most specialized subprime lenders will decline. BHPH is often the only path. Some BHPH dealers accept recent repossessions with a larger down payment (25-30%). The rate runs at or near the maximum.

- Repossession with an unsatisfied deficiency balance. After repossession, the lender typically sells the car at auction and pursues the remaining balance. If this balance remains unpaid and is still in collections, it is doubly damaging. Some subprime lenders require the deficiency paid off before approving a new auto loan.

- Medical collections. Treated more leniently by most auto lenders than consumer debt collections. Medical debt does not carry the same behavioral signal as unpaid credit cards or personal loans.

- Auto-specific collections. An unpaid balance to a prior auto lender , not repossession, but charged-off auto account , sends a very specific signal to the next auto lender. It says this borrower defaulted on a car loan before. This collection may need to be resolved before approval at most lenders.

Should You Buy Now or Improve Your Credit First

Buy now if transportation is urgent , work, family, medical. The cost of not having a car often exceeds the cost of a high-rate loan. Consider waiting 60 to 90 days if credit card utilization is high (a fast fix) or if one reporting error can be corrected quickly. Getting from 488 to 520 or 540 does not dramatically change the terms. Getting from 488 to 600+ does. The 600 threshold moves a borrower from deep subprime to subprime , and the rate difference is meaningful.

- Transportation is required for work, childcare, or medical appointments , absence of a car is costing income or creating safety risk

- Income is stable and the monthly payment at deep subprime rates fits within the budget

- A BHPH or subprime lender reports to all three credit bureaus , so payments improve the score simultaneously

- The plan is: get approved now, pay consistently, refinance in 12-18 months when score improves

- Credit card utilization is above 60% , paying down cards could add 20-40 points in one billing cycle

- A reporting error exists , a wrong collection date or account not yours , that can be disputed in 30-45 days

- Score can realistically reach 520+ within 60 days, which opens more lender options

- Current transportation is workable , rideshare, carpooling, or existing vehicle , making a 60-day delay manageable

The Fastest Ways to Improve a 488 Credit Score Before Applying

The fastest improvements at 488 come from reducing credit card utilization, disputing reporting errors, and adding a secured credit card or credit builder loan for positive payment history. All three can produce visible results in 30 to 90 days. Getting from 488 to 550 in 60 to 90 days is realistic when utilization is the primary cause. Getting from 488 to 600+ typically takes 6 to 12 months of consistent action.

- Pay credit card balances to under 10% of each card's limit. This is the fastest action available. The average person in the deep subprime range carries very high utilization. Getting from 90% to under 10% can add 30 to 50 points in one billing cycle. Pay before the statement closes.

- Dispute any reporting errors on all three bureaus. Pull reports at AnnualCreditReport.com. Wrong dates, wrong balances, accounts that are not yours, and collections with inaccurate information are all disputable. One removed inaccuracy can add 15 to 50 points in 30 to 45 days.

- Open a secured credit card. A $200-$500 deposit-backed card reports as a revolving account to all three bureaus. Use it for small purchases. Pay it in full before the statement closes every month. After 6 months of perfect history, the positive payment record begins contributing meaningfully to the score.

- Add a credit builder loan. Kikoff ($5/month) or Kovo ($10/month) add installment tradelines without a hard inquiry. Combined with a secured card, both account types contribute to credit mix , improving the score in the 10% credit mix category alongside the payment history improvement.

- Become an authorized user on a low-utilization account. A family member with a long credit history, low utilization, and perfect payment record can add you as an authorized user. Their account history posts to your file within 30 to 60 days. Impact: typically 20 to 40 points depending on the account age and utilization.

The full action-by-action timeline , including exactly how many points each move produces and how quickly , is covered in the realistic credit score improvement guide. The same mechanics apply at 488. Utilization and authorized user moves are always the fastest because they update every billing cycle.

How Long Does It Take to Move From 488 to 550

| Credit Issue | Typical Fix Timeline | Estimated Score Gain |

|---|---|---|

| High credit card utilization | 30-60 days | +20 to +50 points |

| Reporting errors / inaccuracies | 30-90 days | +10 to +50 points per item |

| Secured card + on-time payments | 6-12 months | +15 to +40 points over time |

| Collection account deleted | 3-12 months | +20 to +70 points |

| Charge-off deleted | 6-24 months | +30 to +90 points |

What Vehicle Price Range Makes Approval Easier

According to U.S. News auto loan data, the average used car buyer score in Q4 2025 was 690. At 488, the vehicle price range that produces the most reliable approvals is $8,000 to $15,000. Lower prices mean smaller loans, which means lower lender risk. The monthly payment on a $10,000 loan at 21% APR is $270. On a $20,000 loan at the same rate, it is $540. Lenders evaluate whether the income supports the payment , and larger loans require stronger income verification to justify at a deep subprime score.

- Older vehicles (2015-2019) with under 100,000 miles. These price into the $8,000-$14,000 range for reliable options. At a deep subprime rate, this range keeps monthly payments manageable while giving the vehicle enough useful life to outlast the loan term.

- Avoid vehicles with over 120,000 miles. Many subprime lenders impose mileage limits. A car over the lender's mileage cap gets declined regardless of the score. Confirm mileage limits with the lender before selecting a vehicle.

- New cars are not a realistic option at 488. Deep subprime buyers account for less than 2% of new car sales (Cox Automotive, 2025). The price points are too high, the depreciation too fast, and most dealership new car financing is arranged through lenders who require 580+ minimum.

- Stick to reliable brands with lower maintenance costs. At deep subprime rates, the monthly payment on the loan is already high. A car that breaks down and requires major repairs on top of a 21% APR payment creates a compounding financial problem. Toyota, Honda, Mazda, and Hyundai used models in the $10,000-$14,000 range consistently offer the best reliability-to-price ratio.

488 Credit Score Car Loan Checklist

Most subprime lenders require $1,500-$2,000/month minimum verifiable income. Provide two to three months of recent pay stubs, bank statements, or documented self-employment income. Inconsistent income is the most common reason for denial at this score tier beyond the score itself.

10-20% minimum for subprime lenders. 20-25% for many BHPH dealers. Cash, trade equity, or a combination. The larger the down payment relative to the vehicle price, the lower the loan-to-value ratio and the more likely the approval. Start saving before visiting any dealer.

The single most damaging item for auto loan approval. A repossession in the last 12 months blocks most subprime lenders and raises the barrier at BHPH significantly. An older repossession (2-4 years) with a larger down payment can be worked around with patience and the right dealer.

Auto-specific collections and large unpaid balances are most damaging. Medical collections are treated more leniently. Multiple recent collections signal ongoing financial difficulty that compounds the 488 score concern. Dispute inaccurate ones before applying.

Older, lower-mileage, moderately priced vehicles in the $8,000-$15,000 range produce the most approvals at 488. Vehicles over 120,000 miles may hit lender mileage caps. New cars are effectively unavailable at deep subprime. Used cars from 2015-2019 are the realistic market.

Two forms of proof: utility bill, lease agreement, or government mail with current Houston address. Many subprime lenders require 6-12 months at the same address. Frequent moves create additional friction at this score level.

What Houston Auto Lenders Typically Look For

Houston is one of the largest auto markets in Texas. That creates more subprime financing options , more BHPH operators, more dealerships with Credit Acceptance and Westlake relationships, more independent used car lots that specialize in 488-score buyers. Houston lenders at this tier focus heavily on income, residency stability, and down payment. The score confirms the tier. Everything else determines the terms.

Most subprime and BHPH operators in Houston require:

- Verified employment or income. Last 30 days of pay stubs or bank statements. Self-employed buyers need 3-6 months of bank statements showing consistent deposits.

- Proof of Houston residency. Two documents , utility bill, lease, or government mail with address. Lenders want to confirm where the vehicle is located for insurance and repossession purposes.

- Valid Texas driver's license. Required for all auto loan approvals. An out-of-state license delays processing. Bring the current valid license.

- Active auto insurance. Most lenders require full coverage (comp and collision) confirmed before finalizing the loan. Get insurance quotes before visiting , prices vary significantly and the monthly insurance cost needs to fit within the total transportation budget.

- References. Some BHPH dealers and subprime lenders ask for three to five personal references with names and phone numbers. These are not required for approval but are collected for contact purposes if the borrower becomes unreachable.

Can You Refinance Later

Yes , and this is the most important long-term strategy for 488-score borrowers. Get approved for transportation now at whatever rate is available. Make every payment on time without exception. Use that payment history to build the credit score. Refinance when the score reaches 580-600 (12 to 18 months of consistent payments typically gets there from 488). The refinance drops the APR from 21% to something manageable , and saves thousands in interest on the remaining loan balance.

The math makes the strategy compelling.

On a $12,000 loan at 21% APR over 60 months, total interest is approximately $7,100. At 12 months in, the remaining balance is approximately $10,200. Refinancing that balance at 13% APR over 48 months costs approximately $2,700 in remaining interest , versus $5,800 at the original 21% rate. The refinance saves approximately $3,100 on the remaining loan.

The refinance only works if payments are made on time consistently. One missed payment in the first 12 months resets the recovery timeline and may block the refinance option.

At 488 today, the goal for the next 12 months is simple: make every payment on time, address utilization, dispute any inaccuracies, and watch the score improve from deep subprime to subprime to nonprime. That progression opens conventional lenders, lower auto refinance rates, and eventually the full range of financing products.

The path does not stop at the car loan. Getting from 488 to 649 over 18-24 months opens mortgage pre-approval conversations. The 649 credit score mortgage guide covers what borrowers at that score can realistically expect from FHA and conventional lenders , including the apply-now-or-wait decision and the rate tiers that open with further improvement.

Can I get a car loan with a 488 credit score in Houston?

Yes. Options include Buy Here Pay Here dealerships across Houston, subprime specialty lenders (Credit Acceptance Corporation, Westlake Financial, DriveTime), and some credit union programs. Expect deep subprime rates averaging 21.58% APR on used car loans (Experian, Q4 2025). Approval depends more on income, down payment, and vehicle selection than on the credit score alone. A recent repossession or multiple active collections may require a larger down payment or limit choices to BHPH only.

Does income matter more than the credit score at 488?

At this score level, yes , often significantly more. The 488 score has already categorized the borrower as deep subprime. The lender then turns to income, down payment, and file details to determine whether the specific borrower within that tier gets approved. A borrower with $3,500/month in stable income and 20% down may get approved at 488 while someone with the same score, $1,400/month income, and 5% down gets declined. The score determines the rate tier. Income and down payment determine the approval outcome.

What lenders work with 488 credit scores in Houston?

Dealerships that use Credit Acceptance Corporation or Westlake Financial for financing often work with scores as low as 488. DriveTime has Houston locations and specializes in deep subprime financing. Buy Here Pay Here operators throughout Houston approve based primarily on income and down payment with no minimum credit score requirement. A few Texas-based credit unions also have programs for members with challenged credit. Always confirm that the lender reports payments to all three credit bureaus before signing.

Can I refinance my car loan after improving my credit score?

Yes. After 12 to 18 months of on-time payments, most borrowers who started at 488 reach 580-620. At that point, credit unions, online lenders like LightStream or PenFed, and many banks will offer refinance rates significantly below the original deep subprime rate. The refinance does not require going back to the original dealer , any lender who offers auto refinancing can refinance the existing loan. The key is 12 consecutive months of on-time payments and a score above 580.

-

649 Credit Score Mortgage , Should You Apply Now or Wait? The 12 to 24-month path from 488 to 649 is where mortgage conversations begin. This covers what FHA and conventional lenders offer at 649 , the rate tiers, the apply-now vs wait decision framework, the underwriting friction at that score level, and the $22,000+ lifetime savings from crossing the 680 LLPA threshold. The car loan built the payment history that made the mortgage conversation possible. This is the next destination.

-

How Long Does It Take to Raise a Credit Score? Realistic Timelines The gap between 488 and 550 often closes in 60 to 90 days when utilization is the cause. This covers the exact action-by-action improvement timeline with point estimates , utilization reduction in 30-60 days, error disputes in 30-90 days, collection deletions in 3-12 months. The visual chart showing points gained per action is the planning tool every 488-score buyer needs before deciding whether to apply immediately or build for 60-90 days first.

-

How Available Credit Can Raise Your Credit Score Faster Than You Think Credit card utilization is the fastest-moving factor in credit scoring and one of the most common suppressors at 488. This covers exactly how available credit on a credit card drives the FICO utilization calculation, why the score updates in 30 days when utilization drops, and what the non-linear improvement looks like at each utilization tier. If credit card balances are part of what is holding the score at 488, this is the first action to take before visiting any Houston dealership.