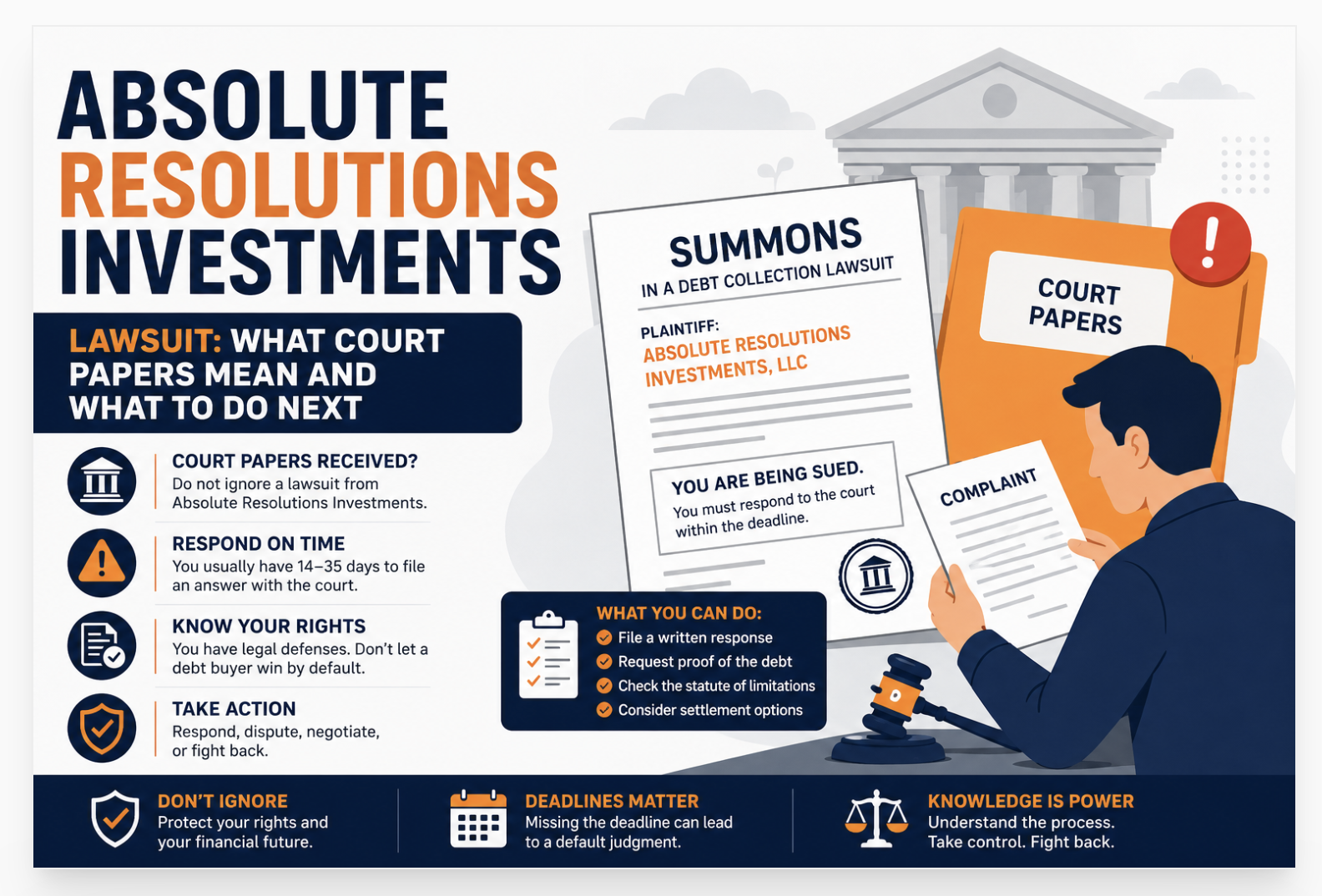

If you received court papers from Absolute Resolutions Investments, do not ignore them.

A lawsuit from a debt buyer can quickly turn into a default judgment, wage garnishment, or frozen bank account if you fail to respond on time.

In my company, we regularly speak with consumers being sued by debt buyers like Absolute Resolutions Investments.

This happens frequently than what you expect.

Most people panic when they see a summons. The first question they ask is whether the lawsuit is real. In many cases, it is.

Debt buyers purchase charged-off accounts for pennies on the dollar. Then they attempt to collect the full balance through calls, letters, settlements, or lawsuits. According to consumer lawsuit trends and debt collection litigation data, debt buyer lawsuits have continued rising after pandemic slowdowns. Large debt buyers and collection law firms file thousands of collection lawsuits every year.

What's important to know is that getting sued does not automatically mean the collector wins.

Many lawsuits contain weak documentation, inaccurate balances, or statute of limitations issues. What you need to do is responding before the court deadline expires.

Absolute Resolutions Investments Lawsuit: Meaning and Next Move

What Are Absolute Resolutions Investments

Absolute Resolutions Investments LLC is a junk debt buyer headquartered at 8000 Norman Center Drive, Suite 350, Bloomington, MN 55437. The company purchases portfolios of charged-off consumer debts , credit card accounts, medical bills, auto loans, cell phone accounts , from original creditors for 2 to 5 cents per dollar of face value. They then file lawsuits to collect the full balance plus interest and fees. The company also operates under the name Absolute Resolutions Corporation. Both names are the same entity.

Absolute Resolutions Investments is not a credit card company, a bank, or the original lender. They are a third-party debt purchaser.

Here is how the model works. Your original creditor , a credit card company, hospital, or bank , charges off a delinquent account after 180 days of non-payment. They sell that charged-off account to a debt buyer like ARI for a small fraction of the balance. ARI then owns the debt legally and attempts to collect the full amount.

The problem for consumers is that by the time ARI files a lawsuit, the original account has changed hands multiple times. Documentation gets lost. The chain of ownership breaks down. ARI often cannot produce a clear line of title proving they legally own the specific debt they are suing over. This documentation gap is the most common defense in ARI lawsuits.

| Company Detail | Information |

|---|---|

| Legal Name | Absolute Resolutions Investments, LLC |

| Also Known As | Absolute Resolutions Corporation, ARI-RES |

| Headquarters | 8000 Norman Center Dr., Suite 350, Bloomington, MN 55437 |

| Company Type | Junk debt buyer / third-party debt collector |

| What They Buy | Credit card debt, medical debt, auto deficiency, cell phone accounts |

| Common Law Firms Used | Stenger & Stenger, P.C. (MI); Pressler, Felt & Warshaw (NJ); Abrahamsen Gindin, LLC (NJ) |

| States They Sue In | New York, Michigan, New Jersey, Florida, Texas, Minnesota, and others |

| FDCPA Status | Accused of multiple FDCPA violations; sued by consumers regularly |

| BBB Profile | Has profiles under both Absolute Resolutions Investments and Absolute Resolutions Corporation |

Companies like ARI operate under the same model as National Enterprise Systems and other major debt buyers , purchase large portfolios at steep discounts, file hundreds of lawsuits monthly, and collect judgments from the fraction of defendants who never respond. The strategy works because most consumers do not know they have the right to fight back, and many effective defenses exist even against valid debts.

Why Is Absolute Resolutions Investments Suing Me

Absolute Resolutions Investments is suing you because they purchased a charged-off debt that allegedly belongs to you, their standard collection attempts did not produce payment, and filing a lawsuit is their primary collection strategy. ARI files high volumes of lawsuits expecting most defendants to ignore the court papers and default , which gives ARI an automatic win without needing to prove anything.

There are four main reasons ARI files against a specific person.

You have a charged-off debt they purchased. This is the most common situation. You had a credit card, medical bill, or auto loan that went unpaid. The original creditor charged it off and sold the portfolio to ARI. ARI now claims legal ownership of the balance.

Their other collection methods failed. Before suing, ARI typically sends letters and makes calls. If those do not produce payment or a payment arrangement, they escalate to filing a lawsuit. The lawsuit is not a bluff , they file and pursue it.

The high-volume strategy requires lawsuits to work. ARI paid pennies on the dollar for the debt. Even collecting a fraction of the face value produces profit. They file many lawsuits simultaneously knowing most defendants will not respond, producing default judgments they can then use for garnishment.

Identity theft or wrong person situations. Some ARI lawsuits target the wrong person entirely , a name match on an old database, mixed files, or identity theft. If you do not recognize the debt in the lawsuit, dispute it immediately. Do not assume they are correct just because they filed.

Similar patterns appear across other high-volume debt collectors. The Stafford Group and Associates operates under the same model , purchasing old debt portfolios and filing lawsuits expecting default judgments from non-responding defendants.

What Happens If You Ignore an Absolute Resolutions Investments Lawsuit

Ignoring an ARI lawsuit produces a default judgment. A default judgment means ARI wins automatically because no defense was filed. With a judgment, ARI can garnish wages, freeze and seize bank accounts, and place property liens. Judgments remain valid for 10 or more years in most states and can be renewed. The balance also grows as interest and legal fees add to the original amount.

This is the sequence that happens when someone ignores the court papers:

- ARI files a lawsuit and you receive a summons

- You do not respond within the deadline (14-30 days depending on state)

- ARI applies for a default judgment from the court

- The court grants the default judgment , ARI wins automatically

- ARI begins judgment enforcement: wage garnishment, bank account levy, or property lien

- Your employer receives a garnishment order deducting money from each paycheck

- Or your bank receives a freeze notice, making your account inaccessible

The critical point: once a default judgment exists, you lose most of your defenses. The time to fight back is before the default , during the answer period.

What Are the 11 Words to Stop a Debt Collector

The 11 words reference a real federal right. Section 1692c(c) of the FDCPA gives every consumer the right to demand a debt collector stop all communication by sending a written request.

Here is what the 11 words actually does and what it does not do.

What it does:

- Legally requires the debt collector to stop calling, texting, emailing, and mailing you

- Requires all further contact to be in writing and only for specific reasons

- Creates a paper trail that protects you if the collector continues anyway (which is an FDCPA violation)

- Can be used at any stage of collection , before or after a lawsuit is filed

What it does not do:

- Does not eliminate the debt

- Does not stop a lawsuit already filed in court

- Does not prevent ARI from obtaining a judgment if you do not respond to a summons

- Does not start the dispute or validation process (that requires a separate debt validation letter)

The 11 words stop calls. They do not stop the legal process if a lawsuit is already filed. If you received a summons, the 11 words alone are not enough. You must also file a written answer with the court within your state's deadline.

As the FTC's debt collection consumer guide confirms, debt collectors who violate your right to cease communication face civil liability. Keeping records of every contact after a written cease and desist request creates the documentation for an FDCPA claim.

How to Respond to an Absolute Resolutions Investments Lawsuit

The summons lists how many days you have to respond. Most states give 20-30 days from the date of service. Texas gives 14 days. Do not count from the date on the papers , count from the date you were actually served. Mark the deadline on your calendar the same day you receive the summons. Missing this date ends your ability to defend the case.

Do not call ARI to explain the situation, confirm the account, or propose a payment. Any admission that you recognize the debt or owe the balance can be used against you in court. Do not sign any documents ARI sends without legal review. The burden of proof is on ARI to prove they own the debt and that you owe the amount they claim. Do not hand them that proof through an admission.

Every state has a statute of limitations on how long a debt collector can sue. If the original delinquency date is older than your state's limit (typically 3-6 years for credit card debt), the lawsuit may be time-barred. Pull your credit report to confirm the original delinquency date. If the debt is past the statute, asserting the SOL as a defense in your answer is the strongest response available.

The answer is your formal response to the lawsuit. It goes to the court , not to ARI. In the answer, you deny the claims and assert your defenses: statute of limitations, lack of standing (ARI cannot prove they own the debt), insufficient documentation, or any factual inaccuracies in the complaint. Most courts charge a small filing fee ($30-$75). This one document prevents the default judgment. Attorneys specializing in debt defense can file a stronger answer with counterclaims if FDCPA violations exist.

Under the FDCPA, you can demand ARI provide written verification of the debt , proof that they own it, the original creditor's name, the original account number, and the amount owed. Send this via certified mail. If ARI cannot validate the debt with proper documentation, they must cease collection activity until they do. ARI's documented history of filing without complete ownership paperwork makes validation requests particularly effective.

Debt defense attorneys who handle ARI cases often provide free initial consultations. Many work on flat-fee arrangements ($300-$800 for a straightforward answer and defense) or on contingency if FDCPA violations exist. The cost of an attorney is almost always less than a default judgment plus interest. Similar law firm structures work against law firms like Mandarich Law Group that file on behalf of debt buyers , the defense strategies overlap significantly across all major debt buyer lawsuits.

Common Defenses Against Absolute Resolutions Investments

ARI must prove they legally own the specific debt they are suing over. Debt portfolios change hands multiple times and original account records are frequently incomplete or missing. If ARI cannot produce a complete chain of assignment from the original creditor to themselves, they have no standing to sue. This is the most common ARI lawsuit defense and the one attorneys pursue first.

Each state sets a time limit on debt collection lawsuits. In most states, the clock starts from the date of the first missed payment (original delinquency). If ARI sues after that window closes, the lawsuit is time-barred regardless of whether the debt is valid. Credit card statutes range from 3 years (some states) to 6 years (others). Check your state's specific limit against the original delinquency date on your credit report.

ARI often claims a balance that includes fees, interest, and charges that may not be legally enforceable. If the amount in the lawsuit does not match the original contract terms or applicable state law, this is a valid defense. Junk debt buyers frequently inflate balances when original account documentation is incomplete.

ARI sues based on database records that are not always accurate. If you do not recognize the account, the creditor, or the time period in the lawsuit, this may be a case of mistaken identity or identity theft. Request full debt validation immediately and dispute the debt with all three credit bureaus.

If ARI or their attorneys violated the FDCPA during collection , false statements, harassment, contacting you after a cease and desist request, or failing to validate the debt , you can file a counterclaim. A successful FDCPA counterclaim entitles you to actual damages, up to $1,000 in statutory damages, and attorney fees. This sometimes results in ARI dismissing their own lawsuit to avoid a judgment against them.

If the debt was previously paid, settled, or discharged through bankruptcy, ARI cannot legally collect on it. Debt buyers sometimes purchase portfolios that include accounts already resolved. If you have documentation of payment or a bankruptcy discharge, present it immediately with your answer.

Does Absolute Resolutions Investments Violate the FDCPA

Yes. Absolute Resolutions Investments is regularly sued by consumers for FDCPA violations. Multiple debt defense attorneys publicly identify ARI as a company that violates federal debt collection law.

The Fair Debt Collection Practices Act prohibits debt collectors from using false, deceptive, or misleading representations. It prohibits harassment. It requires proper debt validation when requested. And it prohibits continuing collection activity after a consumer's dispute.

Common ARI FDCPA violations reported by consumers and attorneys include filing lawsuits without adequate proof of ownership, collecting on debts past the statute of limitations without disclosing that the debt is time-barred, and continuing collection attempts after cease and desist requests.

As Nolo's debt collection lawsuit defense guide explains, FDCPA violations by a debt collector suing you can form the basis of a counterclaim that shifts the legal dynamic entirely. Instead of defending against ARI's lawsuit, you become the plaintiff in an FDCPA action against them , which is often enough to prompt ARI to dismiss their own case.

How an ARI Lawsuit Affects Your Credit

The debt underlying an ARI lawsuit likely already appears on your credit report as a collection account or charged-off account from the original creditor. ARI may also have added their own collection tradeline.

The lawsuit itself does not appear on your credit report while active. However, the outcome matters significantly:

- Default judgment , a judgment from a debt collection case can appear in public records sections of credit reports in some states and stays for 7 years

- Wage garnishment , does not appear directly on credit reports but significantly affects financial stability

- Settlement or dismissal , existing collection tradelines may remain but the active lawsuit closes without creating new derogatory marks

- FDCPA counterclaim victory , ARI may agree to remove any tradelines they added as part of a settlement

The existing collection accounts from ARI and the original creditor suppress scores heavily regardless of the lawsuit outcome. Addressing inaccurate entries, wrong dates, or duplicate accounts through the dispute process under the FCRA is a parallel action that improves the credit profile while the lawsuit is handled separately.

What are Absolute Resolutions Investments?

Absolute Resolutions Investments LLC is a junk debt buyer headquartered in Bloomington, MN. The company purchases portfolios of charged-off consumer debts from original creditors for 2-5 cents on the dollar, then files lawsuits to collect the full balance. They also operate under the name Absolute Resolutions Corporation. They are one of the largest debt buyers in the country and file high volumes of lawsuits expecting most defendants to default without responding.

Why is Absolute Resolutions Investments suing me?

ARI is suing you because they purchased a charged-off account with your name on it , typically a credit card, medical bill, or auto loan , and their standard collection attempts did not produce payment. Filing lawsuits is their primary collection strategy. They rely on the majority of defendants ignoring court papers and defaulting, which gives them an automatic judgment for wage garnishment and bank account freezes. Responding to the summons with a written answer filed to the court within your state's deadline is essential.

What are the 11 words to stop a debt collector?

"Please cease and desist all calls and contact with me, immediately." Sent in writing via certified mail, this phrase triggers Section 1692c(c) of the FDCPA, requiring the debt collector to stop all communication. The 11 words stop phone calls and letters. They do not eliminate the debt and do not stop a lawsuit already filed in court. If ARI has already filed a lawsuit, you must also file a written answer with the court within your state's deadline.

Can Absolute Resolutions Investments garnish my wages?

Yes, but only after obtaining a court judgment. ARI cannot garnish wages or freeze bank accounts without a valid judgment from a court. The judgment requires either a default (you did not respond to the lawsuit) or a court victory after litigation. Filing a timely written answer with the court prevents a default judgment. Without a judgment, ARI has no legal mechanism to access your paycheck or bank accounts.

What is the statute of limitations on an ARI lawsuit?

The statute of limitations on debt lawsuits varies by state and debt type. Most states give creditors and debt buyers 3 to 6 years from the original delinquency date to file a lawsuit on credit card debt. If ARI is suing on a debt that became delinquent more than 3-6 years ago (depending on your state), the statute of limitations is a complete defense , the court must dismiss the lawsuit. Check your state's specific limit and compare it to the original delinquency date shown on your credit report or in the lawsuit complaint.

ARI Lawsuit on Your Credit File? Start Here.

An ARI lawsuit often comes with collection tradelines on your credit report that contain inaccurate dates, wrong balances, or duplicate entries. A free 3-bureau audit shows exactly what each bureau reports so you can identify disputable entries alongside your legal defense strategy.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

What Is Insolvency , Definition and What It Means for Your Debt When an ARI lawsuit results in a judgment, understanding insolvency matters. This covers what insolvency means legally and financially, how it affects your ability to respond to a debt judgment, and whether insolvency status protects any of your assets or income from garnishment under state exemption laws.

-

501 Credit Score , What It Means and How to Improve It ARI collection accounts and charge-offs often contribute to scores in the Very Poor range. This covers what a 501 score means for loan access and lending decisions, the specific dispute and improvement steps that move a debt-damaged score fastest, and the realistic timelines from 501 to the score thresholds that open FHA mortgages, auto financing, and credit cards.

-

Guarantor Definition , What It Means to Co-Sign a Debt Some ARI lawsuits name guarantors or co-signers on the original account alongside the primary borrower. This covers what guarantor liability means, whether a guarantor can be sued separately from the primary debtor, and how being named as a guarantor in a debt collection lawsuit affects both your legal exposure and your credit profile.