TL;DR: A Credit Acceptance repossession can significantly lower your credit score because it is usually preceded by missed payments and followed by a repossession entry, charge-off, collection account, or deficiency balance. Most repossessions remain on a credit report for up to seven years from the original delinquency date. The exact score impact depends on your credit profile before the repossession occurred.

JMJoe Mahlow | Founder and CEO, ASAP Credit Repair USA20+ Years in Credit Repair | CROA Registered | Auto Loan Credit Specialist | 100,000+ Files ReviewedFounded ASAP Credit Repair 20+ Years Experience 100,000+ Files Reviewed CROA Compliant Auto Loan & Repossession Specialist FCRA Dispute ExpertJoe Mahlow | Perspective on Credit Acceptance Repossessions"Credit Acceptance is a subprime lender. Most of their borrowers already have damaged credit before the reposession happens. What people don't understand is that the repo itself isn't the only hit. By the time Credit Acceptance takes the car, there are usually four or five separate negative entries already in the credit report. The 30-day late. The 60-day late. The 90-day late. The default. The charge-off. Then the repo. Then the deficency balance goes to a collection. A repossession and all the missed payments that comes with it can drop your score 50 to 150 points, not from one event but from seven. Most of our clients don't realize that voluntery surrender doesn't protect their credit either. It protects them logistically. The credit report looks almost the same."

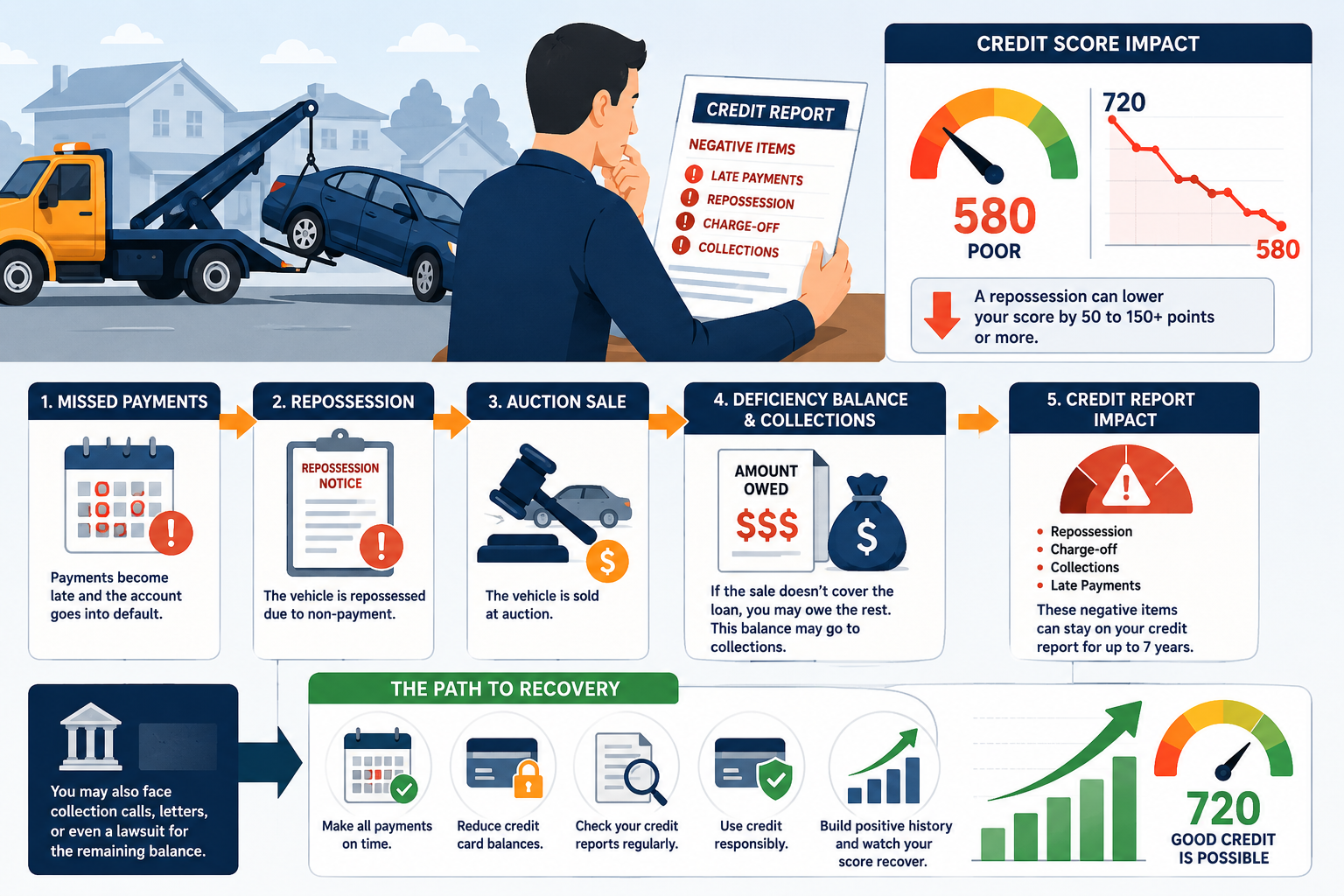

Direct Answer | Credit Acceptance Repossession and Credit Score ImpactA Credit Acceptance repossession can drop your credit score by 50 to 150 points or more. The damage doesn't come from one event. It comes from a chain: missed payments, loan default, charge-off, the repo itself, and then a collection if the deficiency balance goes unpaid. Each step is a separate negative entry on your credit report. All of them stay for up to seven years from your first missed payment. Voluntery surrender does not reduce the credit damage.Score drop range from a repossession , Experian data50-150+Points dropped. Higher scores fall further because they have more room to fall. A borrower at 720 loses more than one already at 580. The actual number depends on the full credit profile and how many negative entries stacked up before and after the repo.How long a repossession stays on a credit report , FCRA requirement7 yearsFrom the date of the FIRST missed payment , not the repo date. If the first missed payment was January 2024 and the repo happened in June 2024, the repo entry stays until January 2031. Each related entry runs its own 7-year clock from the same start date.Average new car price in 2025 , Equifax via NerdWallet, April 2026$49,814Up 39% since 2017. Credit Acceptance borrowers typically buy used vehicles at lower prices. But the combination of high interest rates and subprime APRs means many still owe far more than the car is worth at auction , creating large deficiency balances.

Who Is Credit Acceptance and Why This Matters

Direct AnswerCredit Acceptance Corporation (CAC) is one of the largest subprime auto lenders in the United States. They work with dealerships to finance vehicle purchases for borrowers who cannot get approved elsewhere. Their loans typically carry high interest rates. Their borrowers often already have damaged credit. When a Credit Acceptance loan goes into default, the repossession follows a pattern that adds multiple new negative entries to a credit report that may already have problems.

This matters for two reasons.

First, Credit Acceptance reports to all three credit bureaus. So every late payment, every default notice, and the repossession itself shows up on Equifax, Experian, and TransUnion.

Second, their borrowers are often in the subprime credit range already. A repo on top of an existing damaged file can push a 580 score to 530. That puts auto loan approval, apartment rentals, and any financing out of reach for years.

How Does a Credit Acceptance Repossession Affect Your Credit Score

Direct AnswerThe score drops in stages. Each stage is a separate hit. A 30-day late payment is one hit. A 60-day late is another. A 90-day late is another. The loan default is another. The charge-off is another. The repo itself is another. If the deficiency balance goes to a collection, that is one more. A borrower who starts with a 650 score and goes through this full chain can end up in the 520 to 560 range , all from one loan that went bad.

Credit Score Damage Stages , Credit Acceptance Repossession ChainStage 130-Day Late PaymentFirst missed payment reported to all three bureaus. This is the starting event. The 7-year removal clock starts here, not at the repo date.

Score drop: 15-30 pointsStage 260-Day Late PaymentSecond missed payment. A separate negative entry. Compounds the first hit. Score suppression increases at each level.

Score drop: additional 10-20 pointsStage 390-Day Late Payment + Loan DefaultThird missed payment. Most lenders classify the loan as in default at this stage. Default is its own negative event. Credit Acceptance typically begins repossession process here.

Score drop: additional 15-30 pointsStage 4Vehicle RepossessionThe repossession itself is noted on the credit report. This is a derogatory entry showing loan termination by force or voluntery surrender.

Score drop: significant , additional 20-50 pointsStage 5Charge-Off and Deficiency CollectionIf the deficiency balance isn't paid, Credit Acceptance or a debt buyer reports a collection account. This is a sixth or seventh negative entry from one original loan.

Score drop: additional 30-60 points per entryAs Experian's repossession credit guide confirms, a repossession is rarely a single event , it typically brings late payments, loan default, a charge-off, collection activity, and potentially a court judgment, each of which appears on the credit report and hurts the score.

"CAC repossessed my car in March. My score was already 591 before it happened. Now it's 544. But that's not even the worst part. They sold the car for $4,200 at auction. I owed $12,800. Now they say I still owe $9,800. How is that legal? I gave them the car back. I lost the transportation AND I still have a massive debt AND my credit is destroyed." r/personalfinance · Credit Acceptance repossession thread, 2025 Score went from 591 to 544. Deficiency balance: $9,800 remaining after $4,200 auction sale. Car gone, debt still exists, credit damage already accumulated from every missed payment before the repo.

How Long Does a Credit Acceptance Repossession Stay on Your Credit Report

Direct AnswerSeven years , from the date of your first missed payment, not the repo date. This is important. If your first missed payment was February 2024 and the repo happened in July 2024, the repossession entry stays until February 2031. All the related entries , late payments, charge-off, collection , also run from that same February 2024 start date. So everything cleans up at the same time.

As Experian's repossession timeline guide confirms, the 7-year removal clock starts at the original delinquency date , the date of the first missed payment after which the account was never brought current , not the date the vehicle was taken.

Here is the practical example from Experian's guide:

- First missed payment: September 2025

- Repossession: November 2025

- Repossession removed from credit report: September 2032

That is 7 years from September 2025 , when payments stopped , not from November 2025 when the car was taken.

What Happens After Credit Acceptance Repossesses the Vehicle

Direct AnswerAfter repossession, Credit Acceptance sells the car , usually at auction. Whatever the car sells for gets applied to what you owe. If the car sells for less than the loan balance plus fees, you still owe the difference. That remaining amount is called a deficiency balance. Credit Acceptance can collect this balance directly, send it to a collection agency, sell it to a debt buyer, or file a lawsuit depending on state law and the balance size.

Item Amount Remaining loan balance at time of repo $14,000 Vehicle auction sale price -$6,500 Repossession fees +$500 Storage and auction costs +$400 Deficency balance you still owe $8,400 This is a representative example, not actual Credit Acceptance data. Actual amounts vary by loan, auction result, and state law. You have the right to receive a post-sale notice from Credit Acceptance showing the exact sale price, costs deducted, and the remaining balance. Request this in writing if you don't receive it.The deficency balance is what most people miss. They think giving the car back ends the story. It doesn't. The car is gone but the debt may still exist.

Does Voluntery Repossession Hurt Your Credit Less

Direct AnswerNo. Voluntery repossession and involuntary repossession cause nearly identical credit damage. Both show a derogatory account with loan default and vehicle surrender. Both come after the same chain of late payments. The credit report still shows every missed payment, the default, and the vehicle return. The practical benefits of voluntary surrender are logistical , less stress, no surprise tow, potentially lower fees. The credit impact is almost the same either way.

The voluntary surrender myth is one of the most common misconceptions we see at ASAP Credit Repair. Borrowers call and say "I gave it back voluntarily so my credit won't be as bad." Both outcomes have the same credit impact. The account shows a default. The vehicle is gone. All the preceding late payments remain on the report. Choosing voluntery surrender may save money on fees. It does not save the credit score.As NerdWallet's voluntary vehicle surrender guide confirms, both voluntary surrender and involuntary repossession cause harm to your credit score. The former may give more control over the situation and timing , but the credit damage is nearly identical regardless of which path the borrower takes.

Can Credit Acceptance Sue for a Deficiency Balance

Direct AnswerIn most states, yes. After the vehicle is sold and the deficiency balance is calculated, Credit Acceptance has the right to pursue the remaining amount. They can do this directly, through a collection agency, through a debt buyer, or through a civil lawsuit. If they win a lawsuit, they get a court judgment. That judgment can lead to wage garnishment, bank levies, and liens on property. Whether they sue depends on the balance size, state law, and the statute of limitations in your state.

The statute of limitations on debt collection varies by state. Most states set 3 to 6 years for auto loan deficiency balances. After this period, the debt still exists but a lawsuit becomes legally vulnerable to a statute of limitations defense.

If you receive a lawsuit summons from Credit Acceptance or a debt buyer they sold the deficiency to, respond before the court deadline. Missing the deadline produces a default judgment automatically , without any court hearing.

Can a Credit Acceptance Repossession Be Removed From Your Credit Report

Direct AnswerAn accurate repossession cannot be removed just because it hurts. But removal is possible when specific reporting errors exist. The most common errors in repossession reporting: wrong original delinquency date (which affects the 7-year removal clock), wrong payment history on the account, inaccurate balance or charge-off amount, or a deficiency collection account that the debt buyer cannot validate. Each of these is a dispute opportunity under the FCRA.

Joe Mahlow | What ASAP Looks for in Repo Files"When we review a Credit Acceptance file, we look for three things first. One: is the original delinquency date correct? If it's wrong by even a month, the 7-year removal timeline is wrong. That's disputable. Two: does the deficiency balance show up as a collection from a debt buyer who can't validate the chain of ownership from CAC? Debt buyers frequently lack complete documentation. Three: are there duplicate entries for the same underlying balance , one from Credit Acceptance and one from the collection company , when only one should be reporting active? These aren't exotic situations. We see them often in repo files."

What can be disputed when errors exist:

- Wrong original delinquency date. If the date is wrong, the 7-year removal timeline is wrong. A date reported 6 months later than actual means the entry stays 6 months longer than it should. FCRA dispute corrects this and may result in deletion if the date makes the entry obsolete.

- Wrong payment history. Incorrect 30/60/90-day markings, payments reported as missed when they were made, or account status showing as active when the loan ended.

- Deficiency collection from unverifiable debt buyer. If Credit Acceptance sold the deficiency balance to a debt buyer, that buyer must validate the account when asked. Incomplete chain-of-sale documentation frequently creates validation failure , which produces dispute grounds for the collection entry.

Have a Credit Acceptance Repossession on Your Report?Joe Mahlow's team at ASAP Credit Repair reviews all three bureau reports for reporting errors in the repossession entry, the delinquency date, the payment history, and any collection accounts tied to the deficiency balance. The review is free and identifies what can be disputed.

Get a Free Credit Report Review →

How to Rebuild Credit After a Credit Acceptance Repossession

Direct AnswerRebuilding after a repossession takes time and consistent action. The repossession ages and loses scoring weight over time as positive history builds. The fastest actions: bring all current accounts to good standing, pay all credit card balances to under 10% of the limit, open a secured credit card and pay it in full each month, and dispute any reporting errors in the repossession or collection entries. After 12 to 24 months of clean payment history, most borrowers see meaningful score improvement even while the repossession remains on the report.

- Pay every current account on time. Payment history is 35% of the FICO score. Every on-time payment builds a track record that eventually outweighs the repossession in scoring weight. Set every remaining bill to autopay minimum.

- Reduce credit card utilization to under 10%. If other credit cards are at high balances, they compound the damage from the repossession. Getting cards to under 10% of their limits before the statement closes produces score improvement in 30 days. The mechanics of how available credit affects credit scores explain exactly why this is the fastest rebuilding action available after a repossession.

- Open a secured credit card. A secured card with a $200 to $300 deposit reports monthly positive history to all three bureaus. After 12 months, many secured cards convert to unsecured. This builds new tradeline history on top of the damaged file.

- Dispute any errors in the repossession reporting. Pull all three reports at AnnualCreditReport.com. Check the original delinquency date, the payment history, and any collection accounts tied to the deficiency balance. File FCRA disputes for any inaccuracies found.

- Evaluate the deficiency balance before it reaches a collection or lawsuit. Ignoring the deficiency balance allows it to grow, reach collections, and potentially become a court judgment. Understanding the options for handling collection balances , including negotiating settlements below the full amount , can prevent a second round of score damage from the deficiency.

The full recovery path from a score in the 500s to a score that qualifies for financing is covered in the credit score improvement guide for borrowers starting near 593. The same actions that move a 593 score to 650 apply equally to someone rebuilding after a repossession , utilization reduction first, dispute work second, positive history building throughout.

Can I get another car loan after a Credit Acceptance repossession?

Yes, but the terms will be worse immediately after the repossession. Buy Here Pay Here dealers and some subprime lenders may approve financing within 6 to 12 months of a repossession. Mainstream lenders typically want 12 to 24 months of clean history after the event and a score above 580 to 620. Interest rates at the first post-repossession approval are usually in the 19 to 22% range. After 12 to 18 months of on-time payments on the new loan, refinancing at a better rate becomes possible as the score improves and the repossession ages.

Is a repossession worse than a collection account?

Both are serious derogatory events. A repossession is typically considered more severe because it represents a secured loan where the lender had to physically recover the asset , signaling a more complete failure to repay than a collection on an unsecured debt. The compounding effect also makes repossession more damaging: the repossession entry comes with late payments, a default, a charge-off, and often a collection, each of which suppresses the score separately. A single collection account from an old unpaid utility bill creates one negative entry. A repossession typically creates five or more.

What is a deficiency balance and can I dispute it?

A deficiency balance is the amount remaining on a loan after a repossessed vehicle is sold. If the vehicle sells at auction for less than what the borrower owed plus fees, the difference becomes a deficiency balance the lender can still collect. The deficiency balance itself cannot be disputed away , it reflects a real remaining debt. However, the collection account reporting the deficiency CAN be disputed if the debt buyer cannot validate chain-of-ownership documentation. This is a common success point in repossession credit repair work , the balance was real, but the collection reporting it is unverifiable.

Repossession on Your Credit ReportGet a Free Credit Analysis and See What Can Be AddressedJoe Mahlow's team reviews all three bureau reports for reporting errors in the repossession entry , wrong dates, wrong payment history, unverifiable deficiency collections. The free analysis identifies what is disputable, what requires a different approach, and what the realistic score recovery timeline looks like for your specific file. No cost for the review.Get My Free Credit Analysis → CROA Registered | 20 Years in Business | Free, No ObligationRelated Posts

If you are facing a Credit Acceptance repossession, understanding what happens to your credit report is important before making decisions about payments, settlements, or credit repair.

According to Experian, vehicle repossessions are among the most damaging negative events that can appear on a credit report because they are typically associated with multiple missed payments, collection activity, and charge-offs. Consumers often experience a credit score drop of 50 to more than 150 points depending on their existing credit profile.

Many borrowers focus on losing the vehicle. The larger financial consequence is often the long-term damage to credit scores, future loan approvals, interest rates, and housing applications.

This guide explains how Credit Acceptance repossessions are reported. How they affect credit scores. Whether you can still owe money after the vehicle is sold, and what options may exist for rebuilding your credit afterward.

Credit Acceptance Repossession and Credit Score Impact

Credit Acceptance repossessions often follow multiple missed payments, creating layered credit score damage. Looking at the image below, you can see a drop in credit score from 720 to 580 due to missed payments, repossession and charge off collections.