When people have multiple collection accounts, the same idea usually comes up.

"What if I take out one personal loan and pay everything off?"

On the surface, it sounds smart.

One payment.

One lender.

No more collection calls.

The problem is that debt consolidation does not automatically solve the reason the score dropped in the first place.

I've seen borrowers improve their situation dramatically with consolidation. I've also seen people replace several bad debts with one large new loan and end up in a worse position six months later.

Before applying for a personal loan, it helps to understand what collections actually do to a credit report. Also, its worth discussing whether consolidation will solve the real problem.

Should You Use a Personal Loan to Pay Off Collections?

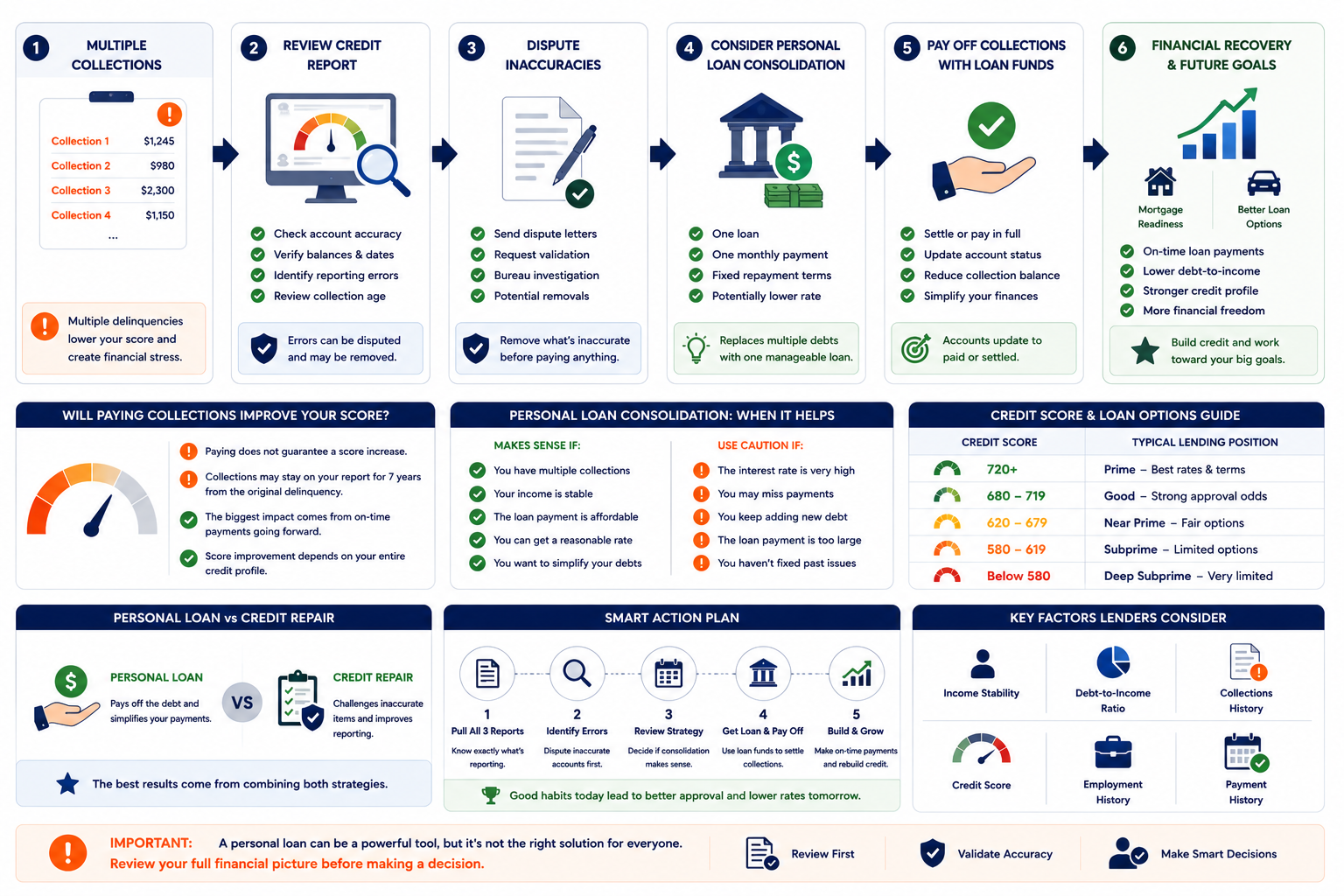

A personal loan can simplify multiple collection accounts into one monthly payment, but it is not always the right solution. Before applying, review your credit report, verify collection accounts, and understand how consolidation could affect your credit score, loan approval odds, and long-term financial goals.

The visual below shows when a personal loan may help, when it may create new risks, and the steps to take before making a decision.

Can You Get a Personal Loan If You Have Collections on Your Credit Report?

Yes, it is possible to get a personal loan while collections appear on your credit report. However, approval depends on income, credit profile, debt-to-income ratio, and lender requirements.

Can You Get a Personal Loan With Collections on Your Credit Report

Yes. Some lenders approve personal loans when collections appear on the credit report. Approval depends on the number and recency of the collections, income, employment stability, and debt-to-income ratio. Mainstream banks often decline. Online subprime lenders, credit unions, and some fintech lenders work with borrowers who have collection accounts , but at significantly higher rates.

The lender's evaluation works this way.

Collections flag the file as elevated risk. The lender then asks: does everything else in the file compensate for that risk? Strong income, stable employment, low existing monthly obligations, and a modest loan request relative to income can offset the collection concern. Multiple recent collections with unstable income is a harder case to make.

- Online subprime lenders (Upgrade, LendingPoint, Avant). These specifically serve borrowers with challenged credit. Many approve applicants with one or two collections when income is sufficient. Rates are high , often 20-35% APR. Origination fees may apply.

- Credit unions. Member-owned, not-for-profit institutions. They often apply more flexibility to existing members with challenging credit histories. A credit union relationship of 12+ months with direct deposit history helps the case significantly.

- Secured personal loans. When an unsecured loan is unavailable, a secured loan backed by a savings account, CD, or vehicle equity may be approved with collections on file. The collateral reduces the lender's risk.

- Mainstream banks. Most decline files with multiple collections. Chase, Bank of America, Wells Fargo, and similar institutions typically require scores above 640 and clean collections history for unsecured personal loans.

Why People Use Personal Loans to Pay Off Collections

Three main reasons. First: simplification. One fixed monthly payment replaces multiple collection accounts, calls, and variable balances. Second: potentially lower total monthly obligation. Third: psychological relief from active collections and the credit damage they represent. These are real benefits. They do not, however, automatically translate to score improvement , which is the misconception most people bring to this decision.

- One payment replaces multiple. Three or four collection accounts at different companies, with different balances and different collection tactics, consolidate into one predictable monthly payment. Simpler to manage. Less chance of a missed payment on one slipping through.

- Fixed repayment timeline. Collections linger. Collectors may settle, disappear, or sell the debt again. A personal loan creates a defined payoff date. Borrowers know when the debt ends.

- Stops collection calls and letters. Paying off collection accounts ends the collector's right to continue pursuing the debt , though the credit bureau entry remains.

- Debt-to-income improvement. Removing multiple small collection payment obligations and replacing them with one personal loan payment may lower the effective monthly debt obligation used in mortgage underwriting calculations.

Will Paying Collections Improve Your Credit Score

Not significantly under the most widely used scoring models. Paying a collection changes the status from unpaid to paid. The entry stays on the credit report for seven years from the original delinquency date. Under FICO Score 8, which most lenders use, paid and unpaid collections of the same age produce similar score suppression. Deletion produces dramatically more improvement. This is the most important misconception in debt consolidation strategy.

As Experian directly confirms, paying a collection does not automatically improve credit scores because the collection entry remains on the credit report. The meaningful improvement comes from having the account removed entirely.

The common belief: pay the collection, watch the score jump.

The reality: the entry stays. The derogatory mark stays. The lender who pulls your credit next month still sees the collection account , it just shows "paid" in the status field instead of "unpaid."

FICO Score 8, which most lenders use for credit decisions, calculates the collection account as a negative event regardless of payment status. The age of the collection and the balance matter. Whether it is paid or unpaid matters very little in FICO 8.

This is why debt consolidation without credit cleanup first often disappoints borrowers who expected a score increase after paying everything off. The debts are gone. The credit report entries are not.

When Debt Consolidation Makes Sense

Debt consolidation makes the most sense when: multiple collections are valid and verified (not disputable), income is stable and the monthly payment is affordable, the consolidation loan rate is better than what the collectors would accept in settlement, and the goal is to simplify payments rather than primarily to raise the score. Consolidation is a debt management tool. It is not a credit repair tool.

- Multiple valid, verified collections. After disputes produce outcomes and the remaining collections are accurate, consolidated repayment at a known monthly payment is better than multiple open-ended collector relationships.

- Stable income that supports the payment. A consolidation loan only helps if the payments are made on time consistently. Missing payments on a new personal loan creates a new negative item on top of the existing collections.

- The consolidation rate beats the alternative. Some collection balances grow with fees and interest. If a $2,000 collection is accruing $50 in monthly fees, a personal loan at even 25% APR may be cheaper over a 12-month payoff period. Run the math before deciding.

- Mortgage preparation with a specific lender requirement. Some FHA lenders require collections over $1,000 to be resolved before closing. If dispute options are exhausted and the collection is valid, a consolidation loan that pays the balance , combined with a pay-for-delete agreement , can satisfy the lender requirement and remove the bureau entry simultaneously.

When Debt Consolidation Can Make Things Worse

Debt consolidation makes things worse when the underlying credit problems are not addressed first. Taking a 30% APR consolidation loan to pay collections a dispute could have deleted produces new debt at high cost without meaningful score improvement. If the collections are inaccurate, paying them before disputing waives the strongest dispute argument available.

- Paying collections that are inaccurate. If the collection reports wrong dates, wrong balances, or belongs to someone else , paying it before disputing removes the best path to deletion. Dispute inaccurate accounts before any payment decision.

- Taking a high-rate loan that extends debt obligations. A 30% APR consolidation loan on $10,000 over 60 months costs $15,000 in total repayment. If the underlying collections settle at 30-40 cents on the dollar or disputed successfully, the loan creates more total cost than the problem it solved.

- Missing payments on the new consolidation loan. A new personal loan with missed payments creates a fresh negative item on all three bureaus , on top of the existing collections. This compounds the problem. Only consolidate when the monthly payment is reliably affordable.

- Collections near the 7-year removal window. If a collection is 5-6 years old, it is approaching automatic removal from the credit report. Paying it now extends the collection's life as an actively updated account and may reset certain bureau reporting timelines. Wait for it to age off rather than paying.

What Credit Score Do You Need for a Consolidation Loan

Most lenders set minimum scores between 580 and 660 for unsecured personal consolidation loans. Below 580, options narrow to subprime online lenders, credit unions, and secured loan options. Above 660, rates become more competitive and approval odds improve significantly. The score alone does not determine approval , income and debt-to-income ratio often outweigh the score at the lower tiers.

| Credit Score | Lending Position | Typical Rate Range | Best Path |

|---|---|---|---|

| 720+ | Prime , wide lender options | 8-15% APR | Any major lender or bank |

| 680-719 | Good , competitive options | 12-20% APR | Credit unions, online lenders |

| 620-679 | Near Prime , fewer options | 18-26% APR | Online lenders, secured loans |

| 580-619 | Subprime , limited options | 22-30% APR | Subprime lenders, secured loans |

| Below 580 | Deep subprime , very limited | 28-36%+ APR | Credit unions, secured loans only |

As LendingTree's 2026 bad credit debt consolidation guide confirms, the key question before applying is not whether you can qualify but whether the loan rate is actually better than what you are currently paying. If the collection balances carry no accruing interest (many charged-off accounts do not), a 30% APR consolidation loan may cost more than the collections it replaces.

Can Debt Consolidation Help You Qualify for a Mortgage

Sometimes. A consolidation loan that replaces multiple collection accounts with one personal loan payment may help the debt-to-income ratio in mortgage underwriting. But it only helps if: the new monthly loan payment is lower than the sum of the collection payments it replaced, and the collection bureau entries are actually removed (not just paid). A consolidation loan that pays collections but leaves the entries on the report does not clear the underwriting concern , the underwriter still sees the derogatory accounts.

Mortgage underwriters evaluate two things regarding collections.

First: the credit score. Collections suppress it. Second: the actual account entries in the file. An underwriter who sees three collection accounts and a personal loan is looking at a different file than one who sees three accounts deleted and a loan in good standing.

The mortgage-ready consolidation strategy: before applying, negotiate pay-for-delete agreements. Get the collector to agree in writing that payment triggers bureau deletion. Pay. Confirm deletion before submitting the mortgage application. That sequence , payment plus deletion , satisfies both the underwriting concern about unresolved debt AND removes the derogatory bureau entry.

Without the deletion agreement, payment satisfies the debt but the collection entry stays visible to every future lender for seven years.

Should You Pay Collections Before Applying for a Mortgage

Not without a strategy. Before paying any collection toward a mortgage goal: dispute inaccurate accounts first (free, and may produce deletion without payment), challenge obsolete accounts past seven years (mandatory removal), and then negotiate pay-for-delete on valid collections. Only then determine which remaining accounts the mortgage lender specifically requires resolved , because not all loan types and lenders require every collection to be paid before closing.

- FHA loans. Most FHA-approved lenders require collections over $1,000 to be resolved or in a payment plan before closing. Some FHA lenders are more flexible. Shop multiple FHA lenders , requirements vary by institution, not just by program.

- Conventional loans. Fannie Mae guidelines allow individual non-medical collections under $2,000 to be excluded from DTI calculations. Lender overlays may impose stricter requirements. Smaller collections under conventional may not require payment at all.

- VA loans. More underwriter discretion. Collections do not automatically block VA approval. The underwriter evaluates the full credit picture and the borrower's explanation.

Personal Loan vs Credit Repair , What Is the Difference

A personal loan pays debt. Credit repair challenges inaccuracies. They solve different problems. A personal loan consolidates what you owe. Credit repair removes what should not be on your report or is reported incorrectly. For most borrowers with multiple collections, some combination of both is the answer , but credit repair comes first, because disputing and deleting collections before paying them produces better outcomes than paying first.

- Pays off collection balances , debt is resolved

- Simplifies multiple payments into one fixed monthly amount

- Stops collection calls and collection account accrual

- Does NOT automatically remove bureau entries

- Does NOT significantly improve score when collection entries remain

- Requires credit qualification , not available to everyone at reasonable rates

- Disputes and removes inaccurate collection entries from the report

- Targets accounts that never validated under FDCPA requirements

- Removes obsolete accounts past the 7-year FCRA window

- Does NOT pay the underlying debt , only challenges reporting accuracy

- Produces score improvement through deletion, not payment

- Works on collections regardless of current credit score or income

The borrower with four collections often needs both.

Two of the four collections may be disputable , wrong dates, insufficient validation, or balances that do not match original creditor records. Those get disputed first. The remaining two, if valid and verified, become candidates for pay-for-delete negotiation or consolidation loan repayment.

Starting with the consolidation loan and skipping the credit repair step costs money and misses the better outcome.

Understanding exactly what collectors must provide when you request validation , and what gaps in their response mean for dispute strategy , is covered in detail in the debt validation guide. That process is the credit repair step that should precede any consolidation loan decision.

What Lenders Look at Besides Your Credit Score

The credit score determines the risk tier and the rate range. Everything else determines whether the approval happens within that tier. Income, employment history, debt-to-income ratio, collection recency, and loan-to-income ratio all carry significant weight at the lower credit score tiers where collection accounts exist.

- Income verification. Pay stubs, bank statements, tax returns. Most lenders require $1,500-$2,000/month minimum verified income for personal loans. Higher loan amounts require proportionally higher income. Inconsistent income documentation is the most common reason for denial beyond the credit score.

- Debt-to-income ratio. Total monthly debt obligations divided by gross monthly income. Most personal lenders want under 40-45% DTI. A borrower with strong income and low existing obligations can qualify with collections that would block someone at higher DTI.

- Employment stability. Two or more years at the same employer , or same field , signals reliable income. Frequent job changes or recent self-employment transition increases the risk the lender assigns to an already challenged file.

- Recency of collections. A collection from three years ago is less damaging to approval odds than one from six months ago. Recent collections signal ongoing financial difficulty. Older collections may be viewed as resolved history.

- Loan amount relative to income. Requesting a $20,000 consolidation loan on $2,800/month income at 580 credit score is a very different file than requesting $5,000. Scale the loan request to what the income genuinely supports.

The Smartest Way to Handle Multiple Collections

Get reports at AnnualCreditReport.com. List every collection: the original creditor, the collection company, the balance, the original delinquency date, and the account status. This is the baseline before any other decision. Most borrowers discover at least one collection they did not know existed , often a duplicate, re-aged account, or debt that was sold and re-reported incorrectly.

Free | Required first step | All three bureausThe original delinquency date controls the 7-year FCRA reporting window. Any collection past that date is obsolete and must be removed. Dispute obsolete accounts before doing anything else. They are legally required to come off the report regardless of whether the underlying debt is still owed. Do not pay an obsolete collection , there is no reason to. Dispute it.

Past 7 years = dispute immediately | No payment requiredFor each collection within the 7-year window: compare the reported information against original creditor documentation. Wrong dates, wrong balances, accounts that are not yours, and collections where the debt buyer cannot prove ownership are all disputable inaccuracies. Send debt validation requests to each collection agency. File FCRA disputes with the bureaus for accounts with gaps. Deletion from a successful dispute is the best possible outcome.

Dispute before paying | Payment removes dispute optionsFor collections that cannot be deleted through dispute , because they are accurate, properly documented, and within the reporting window , negotiate a written pay-for-delete agreement before paying anything. The collector confirms in writing that payment triggers removal from all three bureaus. This produces both debt resolution and score improvement. Without this agreement, payment resolves the balance but leaves the entry on the report for the full 7-year window.

Written agreement required before payment | Get it confirmedAfter disputes are filed and pay-for-delete negotiations are underway, evaluate whether a consolidation loan makes financial sense for any remaining balances. Calculate the total interest cost of the consolidation loan versus settling directly with each collector. Many collectors settle for 30-50 cents on the dollar , which may be cheaper than a 25-30% APR consolidation loan used to pay the full balance. Compare both paths before choosing the loan.

Compare loan cost vs direct settlement | Run the math first| Your Situation | Best First Step | Consolidation Loan? |

|---|---|---|

| Collections with inaccurate reporting | Dispute first | Only after dispute outcome |

| Collections past 7 years from original delinquency | Obsolete dispute immediately | Not needed , free removal |

| Multiple valid, accurate collections | Pay-for-delete negotiation | Consider if DTI benefit justifies rate |

| Stable income, preparing for mortgage | Case-specific review | Depends on lender requirements |

| High-rate consolidation loan offer (28%+) | Calculate full cost first | May be more expensive than direct settlement |

| Score improvement is the primary goal | Dispute and delete | Not the right tool , deletion improves scores |

As Bankrate's debt consolidation guide explains, the primary test before any consolidation loan is whether the new loan rate is genuinely lower than the effective rate on the existing debts. For collection accounts, which are often charged-off and no longer accruing interest, the calculation differs from active credit card balances.

Can I remove collections without paying them?

Yes , through the dispute process. If a collection reports inaccurate information (wrong dates, wrong balances, accounts not yours), the FCRA dispute process can produce deletion without payment. If the collection is past 7 years from the original delinquency date, it is legally required to come off regardless of payment status. Debt buyers who cannot produce complete chain-of-title documentation often cannot verify accounts during bureau investigation windows , which results in deletion. Dispute first. Pay only what cannot be deleted.

Is debt consolidation better than credit repair?

They solve different problems. Debt consolidation addresses what you owe. Credit repair addresses what the credit report says. For borrowers with multiple collections, credit repair often produces better outcomes because it targets deletion , which improves scores more than payment. A consolidation loan at 25-30% APR that pays collections leaving bureau entries on the report costs money without the score benefit. The most effective approach uses credit repair first, then consolidation for remaining valid debts that cannot be deleted.

Will a personal loan to pay collections hurt my score?

Applying for a personal loan creates a hard inquiry , typically 5-10 point temporary score drop. Opening the new loan may also temporarily lower average account age. These are short-term effects. If the loan is paid on time consistently, the positive payment history eventually outweighs the initial impact. The risk is if payments on the new consolidation loan are missed , that creates a new negative event on top of the existing collections, compounding the credit damage.

How much will my score improve after paying all collections?

Minimal improvement under FICO Score 8, which most lenders use. Payment changes account status from unpaid to paid , the bureau entries remain for seven years from the original delinquency. FICO 8 treats paid and unpaid collections of the same age with similar scoring weight. Score improvement from paying a collection is typically 5-10 points at most. Score improvement from deleting a collection through a dispute or pay-for-delete agreement: 30-80 points depending on the collection's age and size. Target deletion, not just payment.

-

What Is a Good Credit Score? Understanding where each score tier sits , and what financial decisions become available at 580, 620, 660, and 700 , gives the collections cleanup strategy a concrete target. This covers the credit score ranges in detail: what each tier means for loan approvals, mortgage rates, and auto financing. Knowing where the score needs to go makes every dispute and pay-for-delete negotiation more purposeful.

-

How Your Credit Score Affects Daily Life Collections affect more than just loan approvals. This covers how credit scores affect rental applications, insurance premiums, employment background checks, and utility deposits , the daily financial friction that borrowers with multiple collections face even outside the mortgage and loan context. Understanding the full scope of what a collection-damaged score costs makes the decision to pursue repair rather than just consolidation more clear.

-

What Is Credit Repair and How Does It Work? The credit repair step that should precede any consolidation loan decision is explained here: what the dispute process involves, what collectors must provide when requested to validate, how bureau investigation windows work, and what outcomes are realistic. For borrowers weighing personal loan consolidation against credit repair, this is the guide that explains exactly what credit repair can and cannot do , so the choice between the two strategies is an informed one.