Credit repair is better than settling debt in 2026 for most Americans dealing with damaged credit scores, inaccurate report entries, and blocked access to loans. Debt settlement sounds like relief. But for the majority of clients who walk through our doors, it makes the credit problem worse before it gets better, and sometimes permanently.

I run a credit repair company. One of the most unforgettable cases we handled last year was a woman who had settled three accounts, thought she was done, and then found out she owed thousands in taxes on the forgiven amounts. Her score had dropped over 120 points during the settlement process. She came to us with errors on top of the settlement damage. That story is not unusual.

Real data backs this up. The CFPB received over 2.7 million credit and consumer reporting complaints in 2024, a 182% jump over the prior two-year monthly average (source: CFPB 2024 Consumer Response Annual Report). The single most common complaint? Incorrect information on credit reports. That means millions of Americans are being harmed by errors they may not even know exist.

Is Credit Repair Right for You?

Credit repair is right for you if your credit score is low because of inaccurate, outdated, or unverifiable negative items on your report.

Under the Fair Credit Reporting Act (FCRA), every consumer has the right to dispute wrong items. Credit repair is the process of exercising that right. A legitimate credit repair company reviews your Equifax, Experian, and TransUnion reports, identifies errors, and submits formal disputes.

Common items credit repair can address:

Accounts that do not belong to you

Duplicate negative entries

Wrong account statuses (e.g., listed as open when closed)

Outdated items past the 7-year reporting period

Incorrect balances or payment history

Collection accounts with inaccurate details

Fraudulent accounts from identity theft

Credit repair works best when the problem is what is reported, not what is owed. If your debts are manageable but your score is blocking you from a mortgage or apartment, credit repair is the right tool.

Should I Get Debt Relief or Credit Repair?

This is the most important question to answer before spending money on either option.

Choose credit repair if:

Your reports contain errors or items you do not recognize

Your debt is manageable, but your score is low

You have been a victim of identity theft or fraud

You want to qualify for better loan rates or housing

Choose debt relief if:

You carry more than $10,000 in unsecured debt with no realistic payoff path

You are already 90+ days delinquent across multiple accounts

You are weighing settlement against bankruptcy

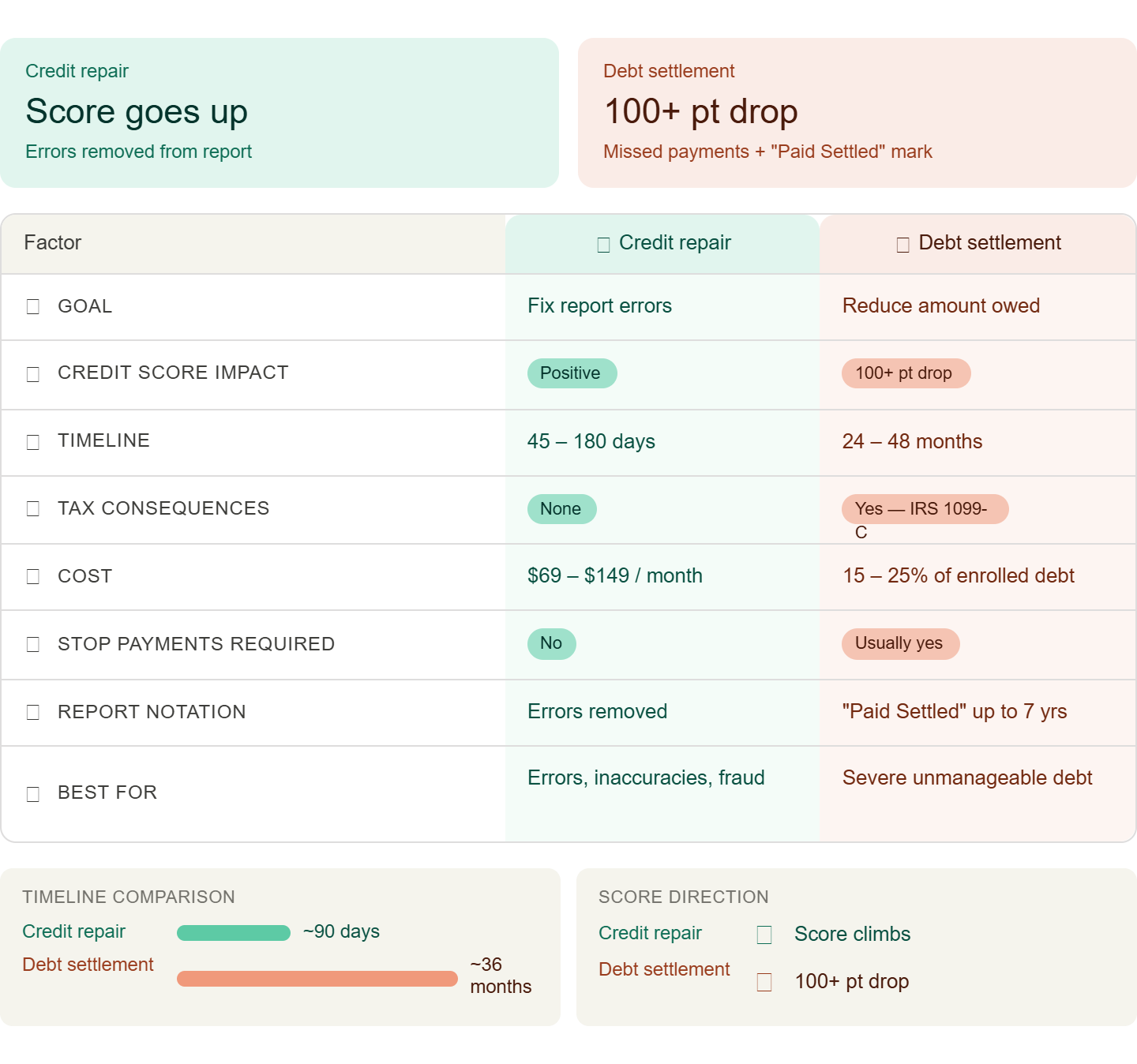

The key difference: credit repair targets what your report says. Debt settlement targets how much you owe. They solve different problems. Mixing them up leads to bad outcomes.

In the last quarter alone, we received dozens of cases from clients who had tried debt settlement first, damaged their scores, and then needed credit repair to clean up the aftermath. That sequence adds months and money to the recovery process.

Can a Credit Repair Service Improve Your Credit Score?

Yes. When a credit repair service successfully removes inaccurate negative items, your score goes up. The improvement depends on what gets removed and what remains.

Here is why it matters. A single account reported as 90 days late can drop a FICO score by up to 133 points. For a borrower applying for a $400,000 mortgage, that score drop can mean a higher interest rate, a larger monthly payment, and over $58,000 more paid over the life of the loan. Removing that inaccurate mark reverses the damage.

Credit repair cannot improve your score by removing accurate, verified negative items. The FTC is clear: no company can legally remove current, accurate, negative information from your credit report (source: FTC Consumer Advice). Anyone who claims otherwise is running a scam.

Legitimate credit repair works within the FCRA law. The results are real when the dispute is valid.

Can a Low Credit Score Be Repaired?

Yes. A low credit score can be repaired, and the timeline is faster than most people expect when errors are driving the damage.

Credit bureaus must investigate disputes within 30 days. Many clients see score movement within 45 to 90 days of filing accurate disputes. Complex files with many items may take 6 months or more.

The path to score recovery through credit repair:

Pull all three credit reports for free at AnnualCreditReport.com

Review each report line by line for errors or unrecognizable accounts

File formal disputes with supporting documentation

Track bureau responses within the 30-day window

Follow up on incomplete or rejected disputes

Working with a professional credit repair company speeds this process. Experienced specialists know how to escalate disputes, challenge non-compliant bureau responses, and handle high-volume files.

Why Debt Settlement Damages Your Credit in 2026

Debt settlement creates three layers of credit damage that most consumers do not anticipate.

Layer 1: Missed payments. Settlement companies typically ask you to stop paying your creditors to build leverage. Every missed payment gets reported as delinquent. These marks drop your score before any settlement is reached.

Layer 2: The "Settled" notation. Once a debt settles, it is marked "Paid Settled" on your report, not "Paid in Full." Lenders view this negatively. That notation stays on your report for up to seven years from the original delinquency date.

Layer 3: Tax liability. The IRS treats forgiven debt as taxable income. If a creditor forgives $600 or more, they file Form 1099-C. On a $20,000 debt settled for $10,000, you may owe taxes on the $10,000 difference. That surprise can cost $1,200 to $3,700 or more, depending on your tax bracket.

The CFPB warns consumers directly: " Debt settlement may well leave you deeper in debt than you were when you started" (source: consumerfinance.gov). Score drops of 100 points or more are common during the process.

The Credit Reporting Accuracy Problem Is Bigger Than Most People Know

Understanding why credit repair matters in 2026 requires understanding how broken the credit reporting system is.

Credit reporting complaints to the CFPB hit an all-time high of over 2.5 million in 2024, representing 80 to 85% of all complaints the agency received. The top issue: incorrect information on reports. This was not a one-year spike. From 2022 to 2024, monthly complaint volume rose 182%.

A 2024 Consumer Reports study found that 44% of participants who checked their credit reports found at least one error. That is nearly half of all consumers. Industry data from Bridgeforce Data Solutions shows that 15 to 25% of trade lines submitted to credit bureaus without automated quality controls contain errors.

These are not edge cases. There are systemic failures in a data infrastructure that decides whether you can rent an apartment, buy a car, or get a mortgage.

Last year, over 60 of our new clients came in thinking their poor scores were entirely their fault. After auditing their reports, most had at least one disputable item. Several had accounts from creditors they had never done business with.

What Debt Settlement Cannot Do (That Credit Repair Can)

Debt settlement reduces what you owe. It does nothing for what your report says. These are separate problems.

If your score is low because of an error, a collections account that was already paid but still showing, or an account that was discharged in bankruptcy but still reporting as open, settling a different debt will not fix any of that. Your score stays low. Your loan applications keep getting denied.

Credit repair addresses the report directly. Debt settlement does not.

Settlement programs also carry risks that credit repair does not:

Creditors can sue you during the settlement period

Not all creditors agree to negotiate

Fee structures (15 to 25% of enrolled or forgiven debt) add a high cost

Programs run 24 to 48 months with no guarantee of results

Credit repair carries no tax consequences and does not require you to stop paying creditors. It works within consumer protection law, not against it.

Is Credit Repair Better Than Debt Settlement? The Direct Answer

Credit repair is better than debt settlement in 2026 for consumers whose primary problem is credit report inaccuracy. It protects your score, carries no tax risk, costs less, and produces results faster.

Debt settlement is appropriate only when debt is truly unmanageable, and bankruptcy is the alternative. Even then, consumers must enter with clear expectations: score damage is certain, the process takes years, and tax liability is likely.

Most people who contact us are not in that situation. They have manageable debt and damaged scores caused by errors. For them, credit repair is not just better. It is the only tool that actually solves their problem.

Quick Reference: Credit Repair vs. Debt Settlement in 2026