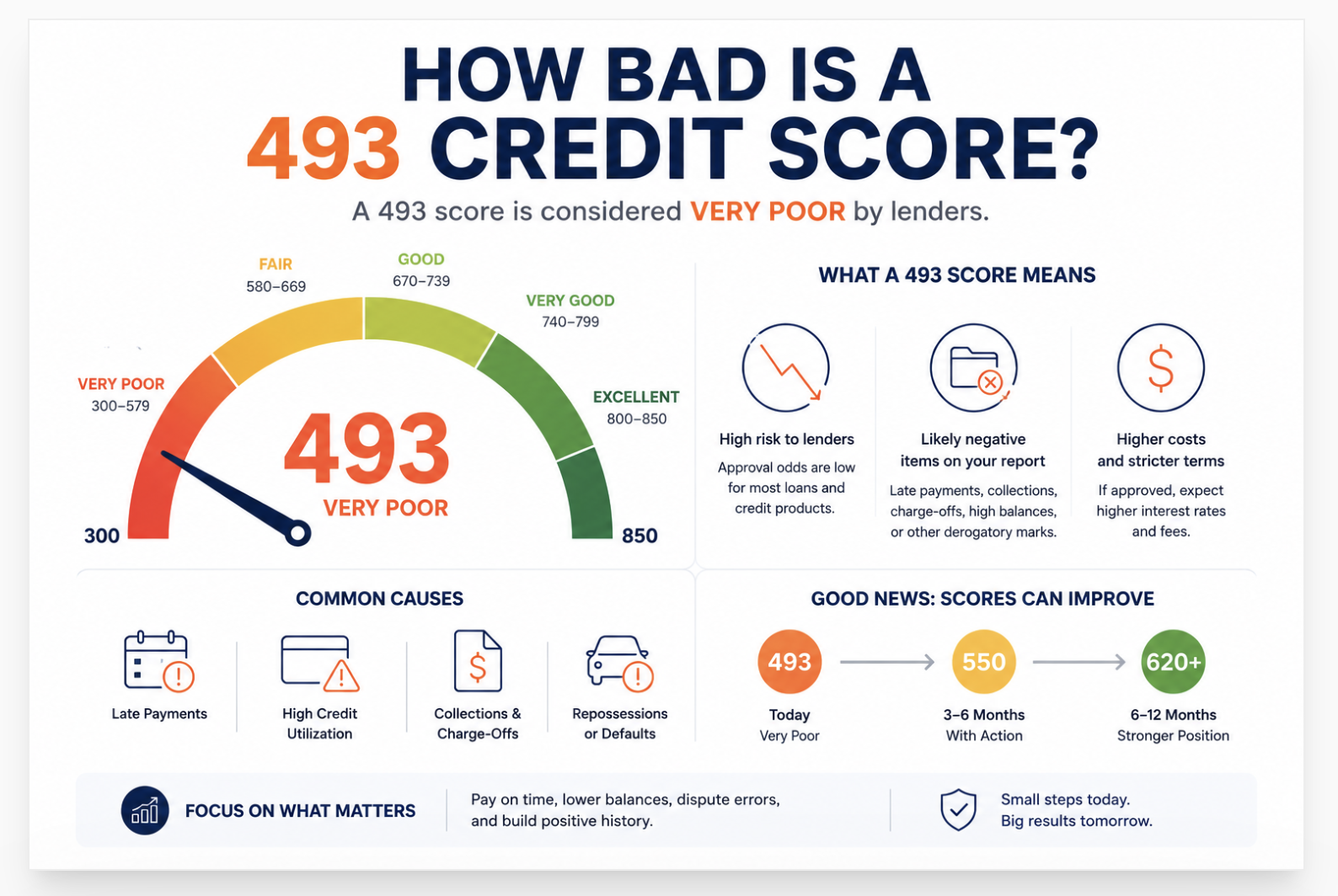

How bad is a 493 credit score? Bad enough that lenders immediately see elevated risk.

At 493, you sit deep in subprime territory.

Meaning, its below what most banks consider lendable for standard financing. This does not automatically mean financial doors are closed, but it does mean borrowing gets expensive, approvals get harder, and simple things like renting an apartment, opening utilities, or qualifying for favorable insurance rates can become more difficult.

A 493 credit score usually does not happen because of one mistake. It is often the result of stacked damage such as collections, charge offs, missed payments, maxed out cards, repossessions, or high utilization over time. The score becomes a reflection of what lenders believe is unstable repayment behavior.

I have seen files in this range where consumers felt stuck, but one pattern shows up often. Low scores usually have obvious drag points. Collections that should have been disputed. Credit card balances sitting near the limit. Old reporting errors never corrected. Late payments that snowballed. That matters because when damage is concentrated, recovery can happen faster than most people think.

Across credit forums, borrowers moving from the 400s into the 600s often describe the same turning point. They stopped trying random fixes and started attacking the largest negative factors first. That is how real score rebuilding starts.

A 493 credit score is bad by every standard measure , it sits in FICO's Very Poor range (300-579), placing the borrower below 99% of the US consumer population. It falls 7 points below the FHA mortgage minimum of 500, which means even the most accessible home loan product closes at this score. Most traditional lenders decline applications at 493 outright. The score is recoverable. Most borrowers at 493 see 60 to 100 points of improvement within 90 days when inaccurate entries, high utilization, or both are addressed simultaneously.

I want to say something direct to anyone reading this with a 493 score. This number tells me one of three things about your file. Either you have gone through a real financial crisis , a job loss, medical event, divorce , and legitimate negatives landed on your report. Or you have inaccurate entries suppressing your true score below where your actual behavior would place it. Or both. In my experience, it is often both. We saw that last quarter when we pulled 23 files in the 480-510 range. Nineteen of those 23 had at least one inaccurate entry. Fourteen of those 19 saw their score cross 500 within 45 days of the first dispute round. A 493 is not a life sentence. For many borrowers, it is a suppressed file waiting to be corrected.

How Bad Is a 493 Credit Score

That is the right question, and the honest answer has two parts.

The first part: it is very bad on paper. FICO's Very Poor tier runs from 300 to 579. A 493 sits in the lower half of that tier, closer to the floor than to Fair territory. According to Experian's 493 credit score data, approximately 99% of US consumers score higher than a 493. About 62% of borrowers in the Very Poor range are likely to become seriously delinquent on a payment within the next two years, which is the primary reason lenders set their floors where they do.

The second part: how bad it feels in practice depends entirely on which products you are trying to access and how quickly you need them.

For a mortgage, 493 is closed , even FHA requires 500. For an auto loan from a traditional bank, 493 is likely closed. For a rewards credit card, a personal loan, or renting a car, 493 is closed. Those are real limitations. But a 493 score borrower can still open a secured credit card today, start a credit builder loan this week, dispute inaccurate entries at all three bureaus in the next 30 minutes, and begin building toward 500, 580, and 620 in a sequence that most people reach faster than they expected when they started.

What a 493 Score Closes and What Stays Open

| Product | Access at 493 | What Changes at 500 | What Changes at 580 |

|---|---|---|---|

| FHA mortgage | Closed , need 500 | Opens at 10% down ($40K on $400K home) | Drops to 3.5% down ($14K on $400K) |

| Conventional mortgage | Closed , need 620 | Still closed | Still closed (620 needed) |

| Auto loan (bank or CU) | Closed at most lenders | Some credit unions may consider | Near-prime lenders open up |

| Buy-here-pay-here auto | Available , 25-35% APR | Same access, may improve rate slightly | Standard subprime lenders open |

| Secured credit card | Accessible now | Wider selection available | Some starter unsecured cards open |

| Credit builder loan | Accessible now | Same access | Same access |

| Unsecured credit card | Closed at mainstream issuers | Rarely accessible | Some starter unsecured cards possible |

| Apartment rental | Varies , co-signer may be required | Some landlords still require co-signer | Most landlords approve with deposit |

A 493 score closes even FHA by 7 points. That gap is smaller than most people realize. A borrower with one credit card balance above 80% utilization who pays it down before the statement close date can generate 10-20 points in a single billing cycle. Seven points from 493 to 500 is achievable faster than a full dispute cycle.

What Causes a 493 Credit Score

Understanding the cause changes the fix. A 493 from different file profiles has a different fastest path forward.

Missed payments and delinquencies drive the single biggest factor: payment history at 35% of FICO. A pattern of 30, 60, or 90-day lates , especially recent ones within the last 12 months , can alone push a score into the 490s from a much higher starting point. One 30-day late payment costs 60-110 points depending on the starting score.

High utilization is the second most common driver. Experian data on 493-score holders shows an average utilization rate of 93.8%. Most cards near or at their limits. Utilization controls 30% of the FICO score and updates every billing cycle. Unlike late payments , which stay on the report for seven years , utilization changes the moment you pay down a balance and the new statement posts. It is the fastest lever.

Collection accounts and charge-offs each add their own weight. A charge-off stays on the report for seven years from the original date of first delinquency. A collection account from the same debt follows a separate 7-year clock. Both drag the score independently. Multiple collections from the same period of financial difficulty can stack into a 100-200 point combined impact.

Recent bankruptcy or foreclosure produces the steepest drops , 130-240 points from a bankruptcy filing. A borrower who enters bankruptcy with a 680 score typically surfaces in the 430-550 range at discharge. Over two to three years of consistent positive behavior post-discharge, most borrowers rebuild to 580-640.

Inaccurate entries are the factor that separates a true 493 from a suppressed one. In our office, last quarter, 19 of 23 client files in the 480-510 range contained at least one inaccuracy. Wrong dates, wrong balances, duplicate accounts, or entries belonging to someone with a similar name. Each one is disputable under the FCRA. Each successful removal produces score gains that no payment or behavioral change can produce on the same timeline.

The Milestone Map from 493

Rebuilding from 493 works faster when you target specific thresholds rather than a vague "higher score." Each milestone unlocks something concrete.

The 7-point gap to 500 is the first target. The 87-point gap to 580 is the second. The 127-point gap to 620 is the third. Each of these is a concrete financial threshold , not a round number goal , and each unlocks something specific. For context on what opening a $400,000 home purchase looks like from each scoring threshold, our breakdown of what credit score you need for a $400,000 house shows exactly how the down payment requirement, interest rate, and monthly payment change at each milestone.

How to Move from 493 , The Fastest Actions in Order

Go to AnnualCreditReport.com. Pull Equifax, Experian, and TransUnion separately , they maintain independent files. Look for wrong dates, wrong balances, accounts you do not recognize, duplicate entries from the same debt, and accounts already paid that still show unpaid. Each inaccuracy is a dispute target. As Bankrate's credit rebuilding guide notes, disputing errors is the highest-return action available to any borrower in the deep subprime tier because removals produce immediate score gains that years of positive behavior cannot replicate on the same timeline.

Cost: Free | Timeline: Same day | Potential gain: 30-60 pts per removed item in 30-45 daysEach bureau has 30 days to investigate independently. Filing at one and waiting, then filing at the next, stretches 30-day windows into 90 days. File all three simultaneously at equifax.com, experian.com, and transunion.com. If the furnisher cannot verify the entry within the 30-day window, the bureau must remove it. Include any supporting documentation , a payment receipt, an insurance EOB, a creditor letter. Vague disputes ("this is wrong") produce slower results than specific disputes ("the original delinquency date is listed as March 2023. My records confirm the account went delinquent in September 2021. The incorrect date extends the 7-year reporting window beyond its legal endpoint").

Cost: Free | Timeline: 30-45 days | All three bureaus simultaneouslyThe balance that appears on your monthly credit card statement is what the bureau receives. Not the balance the day you make a payment , the balance at statement close. Pay before that date, not the due date. At an average utilization of 93.8%, getting even one card below 30% produces a score gain in the next billing cycle. Getting all cards below 10% produces the maximum available gain from this factor. The statement close date is printed on every statement. Mark it and pay 2-3 days before it.

Cost: Requires cash to pay balances | Timeline: One billing cycle (25-35 days) | Potential gain: 20-40 ptsA secured card uses your cash deposit as the credit limit. No credit check required at most issuers. Use it for one small recurring charge each month , a streaming subscription, gas once. Pay in full before the statement close date. Zero utilization on a secured card does not build the file as effectively as a small balance paid in full. Aim for 5-8% utilization on the card. The card then reports a positive payment to all three bureaus monthly, building the payment history that controls 35% of the FICO score. Cards from Capital One, Discover, and Self all report to all three bureaus. Confirm this before opening any card.

Cost: Security deposit ($200-$500) | Timeline: First mark posts in 30-35 days | Builds 12 positive marks per yearAsk a parent, partner, or close friend with a credit card at least 5 years old, zero missed payments, and low utilization to add you as an authorized user. You do not need to use the card. Their account history posts to your credit report within one statement cycle. A 9-year-old card with a perfect payment record adds account age, positive payment history, and available credit to a file that typically has very little of any of these at the 493 level. This is one of the fastest ways to move a thin or damaged file past the 500 mark without paying anything to a creditor. To understand why the credit age question matters so much to lenders, see how we discuss it in our breakdown of what extreme credit scores actually require , the same longevity factor that takes scores to the ceiling helps most during a rebuild from the floor.

Cost: Free | Timeline: 30-60 days | Potential gain: 20-50 ptsWhat Borrowers at 493 Typically Get Wrong

Three mistakes appear in almost every 493 client file we review at ASAP Credit Repair.

Paying collections without negotiating deletion. Paying a collection changes the status from unpaid to paid. FICO Score 8, used by 90% of lenders, treats paid and unpaid collections almost identically. The score improvement from paying without deletion runs 5-10 points at most. The improvement from a negotiated deletion of the same account runs 30-60 points. Before paying any collector, send a validation letter. If the debt is valid and you choose to pay, negotiate deletion in writing first. The distinction between paying and negotiating deletion is the difference between a slow rebuild and a fast one.

Applying for credit they cannot get. A 493-score borrower applying for a personal loan at a traditional bank, a rewards credit card, or a standard auto loan generates a hard inquiry and a denial. Both hurt the score. The denial adds no positive information. The inquiry costs 5-10 points that take months to recover. Apply only for products you know you can access at 493. Secured cards and credit builder loans are the two. Everything else waits.

Using sequential rather than parallel action. The borrower who disputes first, waits 45 days for results, then pays down utilization, then opens a secured card takes six months to accomplish what a borrower who runs all three simultaneously accomplishes in six weeks. Parallel action produces faster results. The dispute clock, the billing cycle, and the authorized user addition all run simultaneously. None of them interfere with the others.

For context on the broader scoring landscape and what each tier means for real lending decisions, our coverage of what the lowest credit scores mean and how they are classified explains where 493 sits relative to the floor of the scale and why the distance from 493 to 580 produces a proportionally larger financial return than almost any other 87-point improvement available anywhere on the 300-850 range.

The NerdWallet guide on raising your credit score confirms that dispute removal and utilization reduction are the two fastest-moving factors , both because they update quickly and because each factor carries substantial FICO weight at 35% and 30% respectively.

How bad is a 493 credit score?

A 493 credit score is in the Very Poor tier (300-579), 7 points below the FHA 500 loan minimum and 99th percentile from the top of the consumer distribution. About 1% of Americans score at or below 499. At 493, mortgage access closes completely. Standard auto loans and unsecured credit cards close. Secured products remain accessible. The score is recoverable , most borrowers at 493 see 60-100 points of improvement within 90 days when disputes, utilization reduction, and positive account additions run simultaneously.

Can you buy a house with a 493 credit score?

No. The minimum credit score for any mortgage product in the US is 500, which is the FHA floor for 10% down financing. A 493 score falls 7 points short of that threshold. No FHA lender, no USDA lender, and no conventional lender offers mortgage financing at 493. The fastest path to mortgage access from 493 is crossing the 500 threshold , achievable through utilization reduction in one billing cycle for many borrowers , then building toward 580 where the down payment drops from 10% to 3.5%.

How long does it take to go from 493 to 600?

A 107-point improvement from 493 to 600 typically takes 3 to 6 months with focused parallel action. For borrowers whose score sits at 493 primarily due to inaccurate entries, disputes alone can produce 60-80 points in a single 30-45 day cycle. Adding utilization reduction, a secured card, and an authorized user simultaneously compresses the timeline further. For borrowers with accurate negative history from a recent bankruptcy or multiple recent lates, the timeline extends to 12-18 months of consistent positive behavior.

Is a 493 credit score permanent?

No. Every negative entry on a credit report has a clock. Late payments drop off after 7 years from the date of the missed payment. Collection accounts drop off after 7 years from the original date of first delinquency. Chapter 7 bankruptcies drop off after 10 years from the filing date. Foreclosures drop off after 7 years. A credit file that produces a 493 today looks different in 2 years and very different in 5 years if positive behavior starts immediately. Inaccurate entries can drop off far sooner , within 30-45 days of a successful dispute.

19 of 23 Files in the 480-510 Range Had at Least One Inaccuracy

A 493 with inaccurate entries is not a true 493. Fourteen of those 19 crossed 500 within 45 days of the first dispute round , without paying a single creditor. A free 3-bureau audit shows exactly what each bureau reports on your file right now and identifies every entry that a dispute could remove or correct.

Get My Free 3-Bureau Audit → Secure · 2 minutes | No credit card required-

Credit Score Ranges , What Is Good, Fair, and Poor A 493 score sits in the Very Poor tier, but understanding the full 300-850 scale shows exactly how far each threshold is from the next practical lending milestone. This covers each tier with specific numbers on what lenders offer at each one, where the biggest rate and access changes occur, and which score targets produce the fastest financial returns from a deep subprime starting point.

-

Credit Score Range Explained Moving from 493 requires knowing exactly which score crosses which threshold. This covers the FICO tiers (Poor through Exceptional), what each one means for mortgage qualification, auto loan rates, and credit card access, and why the 580 and 620 thresholds from a 493 starting point produce a disproportionately large financial return compared to any other 87 or 127 points on the full scale.

-

Maximum Credit Score Guide , What 850 Really Means Understanding where the ceiling is clarifies the climb from the bottom. This covers what a perfect score requires, why the financial benefits plateau around 760-780, and what the borrowers at the top of the scale did differently over decades compared to borrowers stuck in the deep subprime range. The contrast between what drives 850 and what keeps a score at 493 points to the specific behaviors that matter most.