What credit score do you need for a $400,000 house?

It's 580 to 740+, depending on the loan type and how strong the rest of your file looks. But that range is wide for a reason. Mortgage approval is not based on score alone. Down payment, debt-to-income ratio, reserves, employment history, and what appears on your credit report all change the outcome.

I’ve seen borrowers with scores in the low 600s get approved because their file told a clean story. Stable income, low debt, and no recent late payments. I’ve also seen buyers with scores over 700 get worse terms because utilization was high or collections were still reporting. The score gets attention. The file gets approved.

Across homebuyer forums, one pattern shows up repeatedly: buyers are often surprised that the score they checked is not the score the lender uses. Many check a VantageScore app, only to find their mortgage FICO comes in lower at pre mortgage approval. That gap changes rates, monthly payments, and sometimes whether the deal moves forward at all. Mortgage lenders generally pull tri-merge bureau data and rely on mortgage-specific FICO models.

Calculating Credit Scores: How Lenders Measure Risk

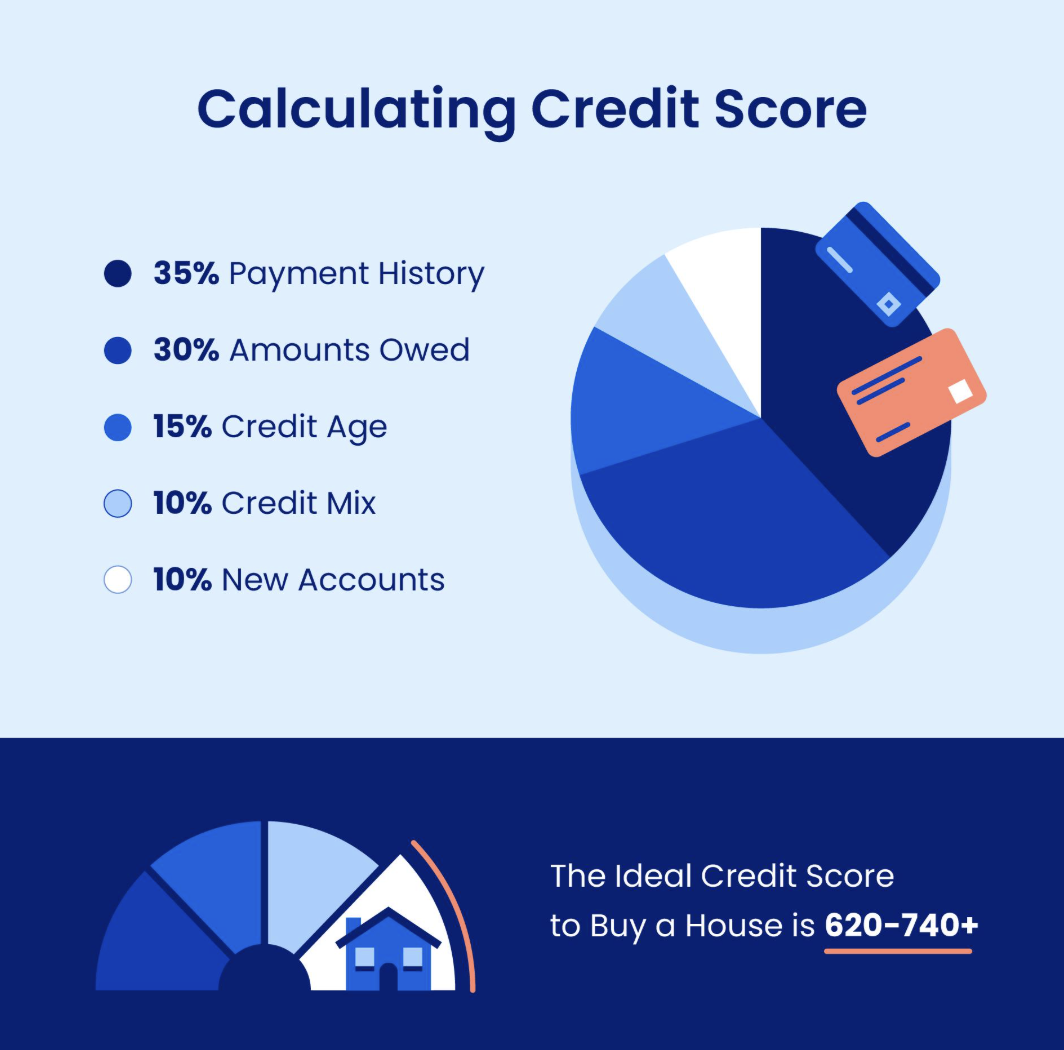

Credit scores are calculated using the information in your credit report, but not all factors carry equal weight. Mortgage lenders rely heavily on FICO mortgage scores, which analyze how you borrow, how consistently you repay, and how risky your current credit behavior looks. The number is mathematical, but what it measures is simple: how likely you are to pay as agreed.

Here is a breakdown:

Payment History — 35%

Payment history carries the most weight in FICO scoring. This includes:

on-time payments

30/60/90-day late payments

collections

charge-offs

bankruptcies

foreclosures

One missed payment can cause a sharp drop, especially if you previously had strong credit. In mortgage underwriting, recent late payments matter far more than older issues because lenders focus heavily on recency of risk.

Across real mortgage forums, buyers often report being denied despite decent scores because one recent 30-day late payment appeared within the last 12 months. By contrast, older negatives with 24+ months of clean history are viewed much differently.

What lenders see: Do you consistently pay your bills on time?

Amounts Owed / Credit Utilization — 30%

This is the second biggest scoring factor. It measures how much revolving debt you use compared with your total credit limits.

Example:

$10,000 total credit limit

$7,000 balance

= 70% utilization (high risk signal)

Mortgage lenders generally like to see utilization below 30%, and below 10% is even stronger.

One common surprise from homebuyer forums is borrowers pay off cards after applying, not realizing the lender pulled balances before those payments reported. Timing matters because utilization updates based on reporting cycles. Not when you make payment.

What lenders see: Are you overextended right now?

Length of Credit History — 15%

This measures:

age of oldest account

average age of all accounts

age of newest account

A longer credit history gives lenders more behavior data. Someone with a 12-year payment history generally looks more predictable than someone whose oldest account is only 18 months old.

Closing old accounts can hurt this category over time because it reduces average account age and total available credit.

What lenders see: How established is your borrowing history?

New Credit / Hard Inquiries — 10%

Opening multiple new accounts in a short period can lower your score because it signals elevated borrowing activity.

This includes:

new credit cards

personal loans

financing accounts

hard inquiries from applications

However, mortgage shopping works differently. Multiple mortgage pulls within a focused shopping window are usually treated as one inquiry under FICO scoring models.

Forum borrowers commonly make one mistake here: opening furniture financing, appliance credit, or a new car loan while waiting to close on a home. That changes debt ratios and can kill approval late in underwriting.

What lenders see: Are you suddenly taking on new debt?

Credit Mix — 10%

Lenders like seeing responsible management across different account types:

credit cards (revolving)

auto loans

mortgages

student loans

installment loans

A healthy mix shows broader borrowing experience. This is the smallest major scoring factor, but it still helps strengthen an otherwise clean file.

What lenders see: Can you handle different kinds of debt responsibly?

Here is what I want to say to anyone sitting at a 620 or 640 score right now, looking at a $400,000 home and wondering if they qualify. You probably do qualify. The question is what you will pay for it. At 620 versus 760, you are looking at the same house, the same lender, the same neighborhood , and a rate that could cost you $200 more per month for 30 years. That is not a small number. Sixty days of focused work on your credit file can move a 640 to a 700 in situations where inaccurate entries or high utilization are the cause. I have seen it happen in our office more times than I can count. Do not rush the application if you are close. The rate difference at 700 versus 640 pays back every day you spent improving your score.

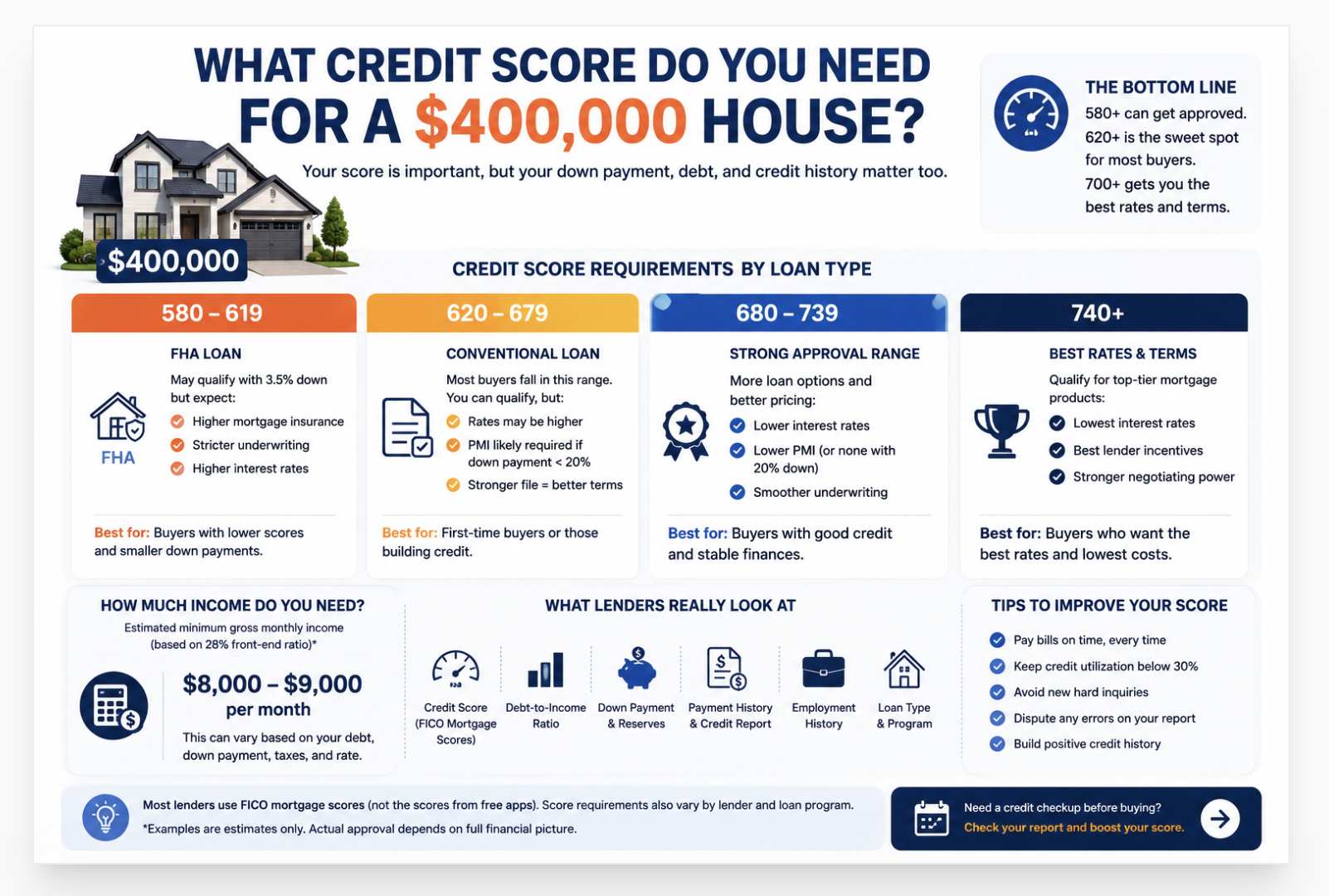

What Credit Score Do You Need for a $400,000 House

The minimum credit score to buy a $400,000 house is 580 for an FHA loan (3.5% down) or 620 for a conventional loan. A score of 700 or above gets you competitive rates. A 740+ score gets you the best available pricing. The specific score you need depends on loan type, down payment size, and how much interest cost you are willing to carry over the loan term.

Let me walk through this the way I would explain it to someone sitting across from me for the first time.

The word "need" has two meanings in this context. There is the floor score , the minimum number that gets any lender to approve you. Then there is the practical score , the number that produces a loan term worth signing. Both matter, and they are not the same.

For a $400,000 home, the FHA floor is 580. Conventional is 620. Those are the thresholds that open the door. The score that gets you through the door at a rate you will not regret for the next 30 years starts at 700 and gets better from there.

| Loan Type | Min Score | Down Payment on $400K | Notes |

|---|---|---|---|

| FHA (580+ score) | 580 | $14,000 (3.5%) | Lifetime MIP required. FHA limit in most counties is $541,287 in 2026. |

| FHA (500-579 score) | 500 | $40,000 (10%) | Very few lenders approve below 580 in practice despite the program minimum. |

| Conventional | 620 | $12,000-$20,000 (3-5%) | PMI required under 20% down. PMI cancels when equity reaches 20%. |

| Conventional (no PMI) | 620 | $80,000 (20%) | Best long-term cost with 20% down. No PMI. Lower monthly payment. |

| VA Loan | None (VA) / 580-620 (most lenders) | $0 | For eligible veterans and active military. No down payment. No PMI. |

| USDA Loan | 640 (most lenders) | $0 | Rural and suburban properties only. Income limits apply. |

How Your Credit Score Changes the Monthly Payment on a $400,000 Home

The $433 monthly gap between the bottom tier (580-639) and the top tier (760+) on the same $400,000 home represents $155,880 over 30 years , nearly 40% of the original purchase price paid purely in additional interest from a lower score.

As NerdWallet's 2026 FHA loan requirements guide confirms, a 580 score qualifies but the rate pricing at that level adds substantial long-term cost compared to borrowers who take a few months to push into the 700 range before applying.

On a $400,000 home with 3.5% FHA down payment, the monthly payment difference between a 580 score and a 760 score runs approximately $433 per month at 2026 rate levels. Over 30 years that gap totals more than $155,000. The minimum score opens the door. The target score determines what buying that house actually costs.

How Much Income Do You Need for a $400,000 House

To buy a $400,000 house at 2026 mortgage rates with 3.5% down, you need approximately $9,500 to $11,000 in gross monthly income ($114,000 to $132,000 per year). This assumes a 6.8-7% 30-year rate and uses the standard 28% front-end DTI guideline. Other debts, property taxes, insurance, and HOA fees all raise the income floor.

Lenders evaluate two numbers when it comes to income. The front-end ratio covers housing costs only , mortgage principal, interest, taxes, insurance, and HOA. The back-end ratio covers all monthly debts. Most conventional lenders want the front-end below 28% and the back-end below 36-45%.

Total estimated housing cost at these figures runs approximately $3,012 to $3,400 per month depending on property taxes, homeowners insurance, and HOA. To keep that within 28% of gross income, you need $10,757 to $12,143 per month , or $129,000 to $145,700 per year.

Income type matters too. A W-2 employee qualifies on gross salary. A self-employed borrower qualifies on net income after deductions, typically using a two-year average of Schedule C net income. Two years of consistent self-employment income is the standard requirement. A borrower making $150,000 gross as a freelancer with $60,000 in deductions qualifies on $90,000 , not $150,000.

Understanding how lenders calculate your qualifying income before they review your credit report helps you walk into the pre-approval process prepared. Our guide on credit repair for first-time home buyers covers both the credit and income documentation preparation steps most buyers skip , which is part of why first-time applications get denied at a higher rate than repeat buyers.

The Score Tier That Matters Most at $400,000

Looking at the $400,000 price point specifically, the most impactful score boundary is the gap between 679 and 680. That crossing moves a borrower from Fannie Mae's C-tier pricing to B-tier. The rate improvement at that crossing saves approximately $100 per month on a $386,000 loan at 2026 rates.

The second most impactful boundary is 739 to 740. That crossing enters the pricing tier where lenders compete with their best available offers. The monthly savings versus a 680 score borrower run approximately $90 additional dollars per month on the same loan.

Combined, moving from 620 to 740 on a $386,000 loan produces a monthly payment reduction of roughly $200-$250 and a 30-year interest savings of $72,000 to $90,000 depending on the specific lender and market conditions at application time.

Here is the timeline math for borrowers who think they cannot afford to wait. Say you are at 640 right now and the target score is 720. That gap typically takes 60 to 90 days with focused action , disputes on inaccurate entries, utilization paydown to below 10%, and authorized user addition. During those 90 days, a $400,000 home at the rates discussed above costs roughly $9,000 in monthly payment you have not made. The rate drop from 7.4% to 6.5% saves approximately $189 per month, which means the break-even on waiting 90 days is less than 4 years. On a 30-year mortgage, that math strongly favors waiting.

As LendingTree's 2026 minimum mortgage requirements guide explains, the score tier you land in at application determines your rate tier , and most lenders do not renegotiate rates once the loan is underway unless you refinance. The application score is fixed into the loan terms.

What Else Lenders Check Beyond the Credit Score

The credit score opens the conversation. The rest of the file closes it.

Lenders buying a $400,000 mortgage look at six factors beyond the score. Down payment size: a larger down payment reduces the loan-to-value ratio and strengthens the file regardless of score. Employment history: two consecutive years at the same employer or in the same field is the standard. Cash reserves: most conventional lenders want to see 2 months of mortgage payments in the bank after closing costs. Debt-to-income: front-end ideally under 28%, back-end under 43-45%. Property condition: the home must appraise at or above the purchase price and meet program-specific condition standards. And recent credit behavior: the last 12 months carry more weight than older history.

A borrower at 700 with strong reserves, 24 months of employment stability, and low utilization looks different from a 700 borrower with zero savings, a job switch 8 months ago, and three cards above 60% utilization. The score is the same. The underwriting decision may not be. Our breakdown of all the factors lenders check beyond the credit score covers each one specifically, including which factors carry the most weight in manual underwriting for borderline applications.

As Bankrate's mortgage credit score guide notes, lenders pull FICO mortgage models , FICO 2, 4, and 5 , which weight factors differently from the FICO 8 you see on consumer apps. Your VantageScore on Credit Karma may read 690. Your FICO mortgage model may read 668. The score the lender sees is the one that matters, and it is not always the one you see for free online.

What credit score do you need for a $400,000 house?

The minimum credit score to buy a $400,000 house is 580 for an FHA loan with 3.5% down ($14,000) or 620 for a conventional loan. In practice, most lenders apply stricter overlays above the program minimums, and many FHA lenders require 620-640 even though the FHA program technically allows 580. A score of 700 or above qualifies for competitive rates. A score of 740 or higher produces the best available pricing on a conventional loan at this price point.

Can I buy a $400,000 house with a 580 credit score?

Yes, with an FHA loan and 3.5% down ($14,000). The FHA loan limit for most US counties sits at $541,287 in 2026, well above $400,000. A 580 score qualifies for FHA 3.5% down financing. The trade-off includes FHA mortgage insurance that applies for the life of the loan if you put down less than 10%, and a higher interest rate compared to borrowers in the 700-plus range. At 580, a $400,000 home is accessible. It carries significantly higher lifetime costs than the same purchase made at 720 or above.

How much is a down payment on a $400,000 house?

Down payment on a $400,000 house depends on your loan type. FHA with 580+ score: $14,000 (3.5%). FHA with 500-579 score: $40,000 (10%). Conventional first-time buyer programs (HomeReady, Home Possible): $12,000 (3%). Standard conventional: $20,000 (5%). 20% conventional to eliminate PMI: $80,000. VA and USDA loans for eligible borrowers require zero down. Down payment assistance programs in many states can reduce or eliminate these requirements for qualifying buyers.

Does a joint mortgage use both scores?

No. For a joint mortgage application, lenders pull three credit scores for each borrower and use the middle score. They then use the lower of the two middle scores for the loan's qualifying rate. If one spouse has a 740 middle score and the other has a 640 middle score, the loan prices off the 640. Some couples choose to apply with only the higher-score borrower to get better rate terms, provided that borrower's income alone qualifies for the loan amount needed.

Know Your Actual Mortgage Score Before You Apply for a $400,000 Home

The score lenders see for a mortgage is FICO 2, 4, or 5 , not the VantageScore on your free app. Inaccurate entries may be suppressing your mortgage-specific FICO by 20-50 points. A free 3-bureau audit shows exactly what Equifax, Experian, and TransUnion report right now, so you know whether you are at the score tier you think you are before the lender pulls your file.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

Factors Lenders Check Beyond the Credit Score Your score gets you to the table. DTI, reserves, employment history, and the property itself determine whether you leave with approval or a denial. This covers all six underwriting factors lenders evaluate on a $400,000 mortgage application and which ones are fastest to strengthen before applying.

-

Credit Score Range , What Each Tier Means for Borrowing Knowing which tier your score sits in tells you which loan products you qualify for and what rate tier to expect. This covers the full range from Deep Subprime to Exceptional, what products open at each threshold, and the specific score movements that cross you from one pricing tier into a better one on a mortgage application.

-

647 Credit Score Guide , What It Gets You on a Mortgage A 647 score sits in the Fair tier, 27 points below the first major mortgage rate improvement at 674 and 93 points from the 740 tier where best available rates begin. This covers exactly what a 647 qualifies for on a $400,000 home, what rate tier to expect, and the 60-to-90-day action plan that moves a 647 into the competitive zone before a mortgage application.