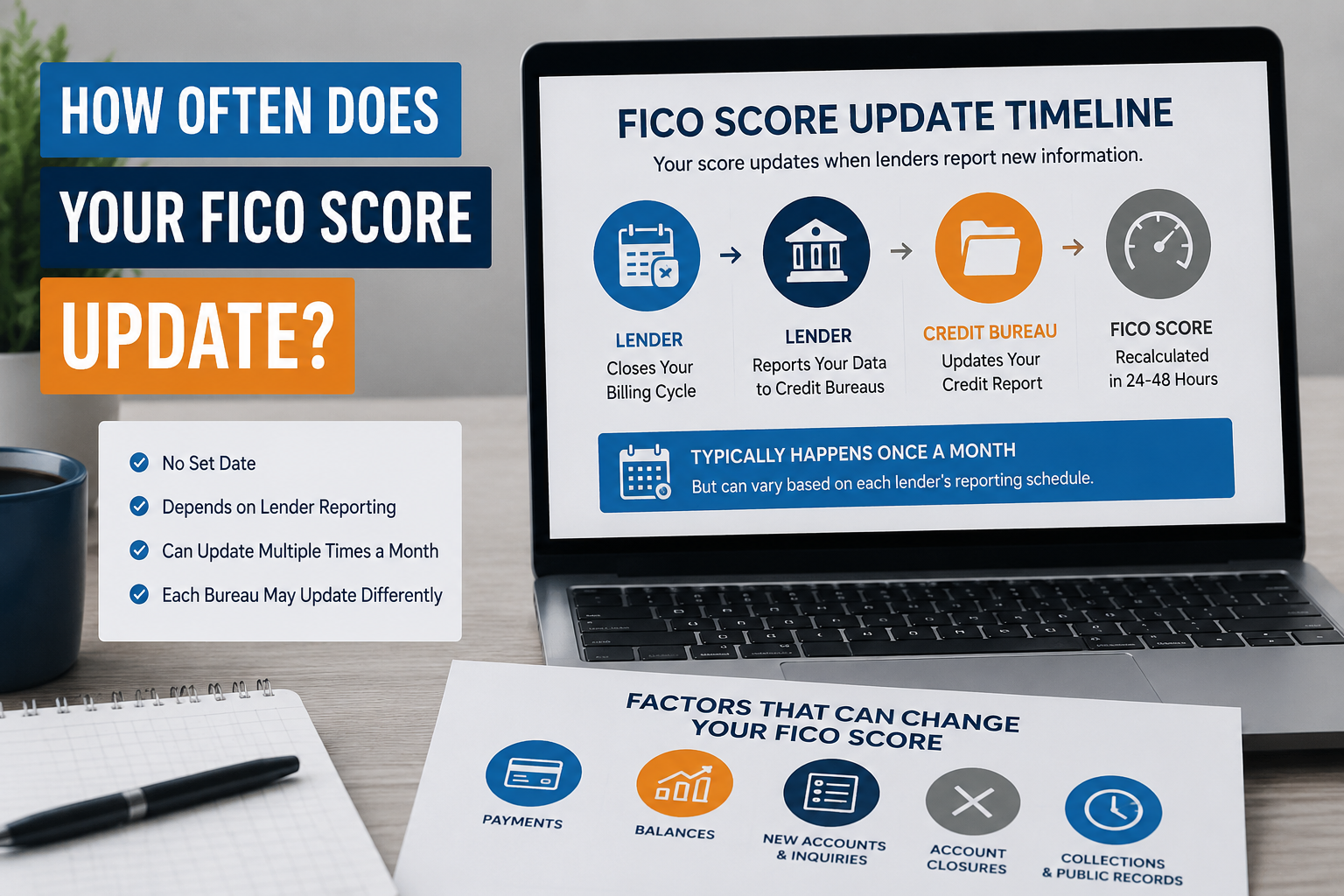

How Often Does Your FICO Score Update? As often as once a month, but there is no single set date when it happens. The update depends entirely on when your lenders report new data to the three major credit bureaus: Equifax, Experian, and TransUnion. Once a bureau receives that data, FICO recalculates your score within 24 to 48 hours.

Running a credit repair company, I see this confusion every week. One of the most common things clients tell me is that they paid off a balance, but their score "didn't move." The issue is rarely the credit bureau; it is the reporting lag from the lender. Just last quarter, over 40 clients came to us frustrated after paying off credit card balances, only to wait 30 or more days to see any score change. Timing is everything here.

A r/personalfinance thread on Reddit with hundreds of upvotes captures this perfectly: users consistently report waiting 30 to 45 days before a major balance payoff showed up in their scores, not because FICO is slow, but because their lenders report on their own monthly schedule. (Reference: r/personalfinance) According to the Consumer Financial Protection Bureau, creditors are not legally required to report to all three bureaus, and many report only once per billing cycle (source: consumerfinance.gov).

How Often Does Your FICO Score Update?

Your FICO score updates every time a lender sends new information to a credit bureau. That typically happens once per month, usually at the end of your billing cycle. So in practice, your FICO score can change once or even multiple times a month, depending on how many accounts you have and when each lender reports.

Here is the step-by-step sequence:

Your lender closes your billing statement.

The lender sends your updated balance, payment status, and credit limit to one or more credit bureaus.

The bureau adds that data to your credit report.

FICO pulls from the updated report and recalculates your score within 24 to 48 hours.

If you have three credit cards and a car loan, each with different billing cycles, your score can update several times throughout the same month. If you have only one account, you may see just one update per month or fewer.

The key takeaway: FICO does not sit on a fixed update schedule. Your lenders' reporting schedules control the timing.

How Often Do Credit Scores Update Across All Three Bureaus?

Each bureau updates your credit report independently. One lender might report to Experian on the 10th, to TransUnion on the 18th, and to Equifax on the 25th. Because of this, your FICO score from each bureau can show a different number at any point in the month.

This also explains why two people can have the same accounts and still see different update timelines. It comes down to which bureaus their lenders report to and how often.

Credit reporting is voluntary. Not every lender reports to all three bureaus. Some report to only one or two. That means your Equifax FICO score can sit unchanged for weeks while your Experian FICO score moves up or down.

The three credit bureaus now give consumers access to their credit reports once per week as a courtesy, per the Fair Credit Reporting Act. But getting a weekly report does not mean your score changed weekly; it just means you can check more often.

When Will My FICO Score 8 Be Updated?

FICO Score 8 is the most widely used version. 90% of top U.S. lenders use FICO Scores when making lending decisions, and FICO Score 8 remains the standard most of them pull.

Your FICO Score 8 updates the same way as any other FICO version: it recalculates once new data lands on your credit report from a lender. There is no separate schedule for FICO Score 8 vs. FICO Score 9 or FICO Score 10. The model version does not affect update timing; the lender's reporting cycle does.

If your credit card issuer reports at the end of your statement period, your FICO Score 8 will refresh within a day or two after that data reaches the bureau. For most people, that means one meaningful update per account per month.

Capital One and Discover pull bureau files nightly and can show score changes the day after a large balance shift, provided the underlying data was already reported. Most other major banks, Chase, American Express, and Bank of America, update FICO Score 8 once per statement period and push the new number to your portal a few days later.

How Often Does My Credit Score Change?

Your credit score can change daily in theory, but in practice, it changes when your underlying credit report changes. The age of your accounts alone causes minor movement over time, even if you make no new purchases or payments.

More significant changes come from:

A new payment was posted by your lender.

A balance reduction or payoff.

A new hard inquiry from a credit application.

An account opening or closing.

A collection account has been added or removed.

A late payment is newly reported (usually after 30 days past due).

Negative changes tend to appear faster than positive ones. A missed payment can show up in your credit report within days of the 30-day mark. A balance payoff, on the other hand, waits for your lender's next scheduled report to the bureau.

This asymmetry frustrates a lot of people. In our office alone, we regularly see clients whose collections appeared almost immediately, but whose dispute resolutions took 30 to 60 days to reflect in the score.

Why Did My FICO Score Not Update After I Paid Off Debt?

Paying off a debt does not instantly trigger a credit report update. Your lender has to report the payoff to the bureau first. Until that happens, your score stays the same even if your balance is zero.

The typical wait is 30 to 45 days from the payoff date, sometimes longer if your lender reports only at the end of the billing cycle.

Two things can help you move faster:

Check your lender's reporting schedule. Some lenders report weekly or even daily. Ask your lender directly when they report to each bureau.

Request a rapid rescore. If you are in the middle of a mortgage application, your loan officer can submit a rapid rescore request to the bureau. The bureau processes it in a few days. This option is not available to consumers directly; you must go through a lender.

Rapid rescoring is not a credit repair tool. It does not remove negative items or fix errors. It only fast-tracks verified, recent data that has not been reported yet.

Does Checking Your FICO Score Affect It?

Checking your own FICO score does not affect it. This is a soft inquiry, which has zero impact on your score. You can check your score daily on myFICO.com or through your bank's dashboard without any penalty.

In April 2025, FICO reported a nearly 70% increase in consumers checking their FICO Score 8 for free through myFICO.com over the prior year. That surge shows more people are monitoring their scores regularly, and that is the right move.

Hard inquiries, the type that happen when a lender checks your credit during an application, do affect your score. A single hard inquiry typically lowers your FICO score by a few points and stays on your report for two years, though its scoring impact fades after 12 months.

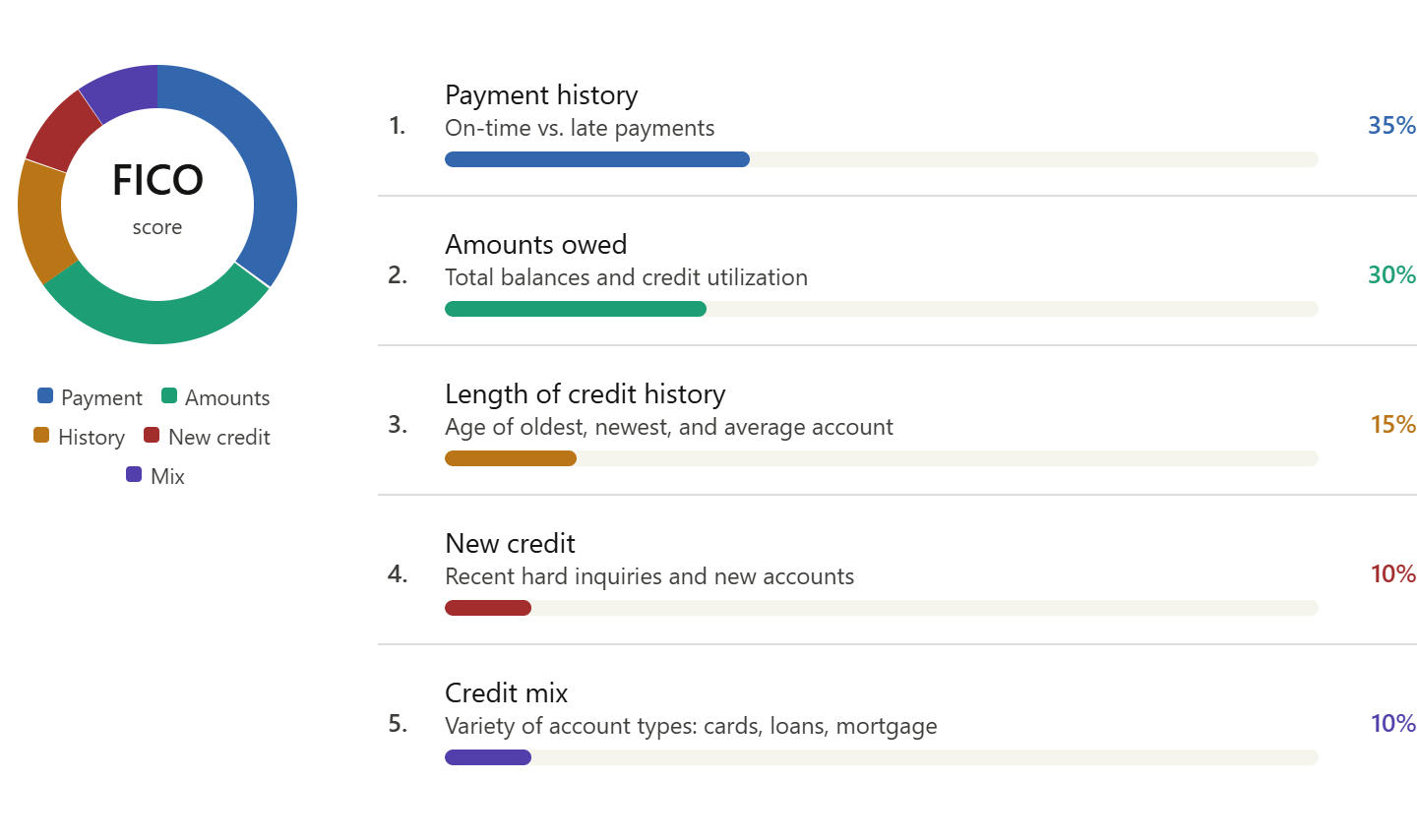

What Actually Triggers a FICO Score Change?

FICO Score 8 weighs five factors when calculating your score:

The biggest short-term triggers are credit utilization changes and payment status changes. Pay down a $5,000 balance to $500, and you drop your utilization significantly, which feeds directly into the 30% "amounts owed" factor and can move your score by double digits in one reporting cycle.

Opening or closing a credit card also changes your available credit, which shifts your utilization ratio. This is why closing an old card, even one you do not use, can cause your score to dip temporarily.

Waiting for Your FICO Score to Update?

If you paid off debt, disputed an account, or lowered your credit card balance, and your score still has not moved, the issue may be lender reporting delays. We can help you review what is holding your credit back.

Get Your Free Credit Report ReviewKnow what changed, what did not, and what to fix next.

How to See Your FICO Score Update Faster

You cannot force a lender to report sooner than their cycle. But you can do a few things to shorten the effective wait:

Pay balances early before the statement's close date, not just before the due date. Balances get reported at statement close, so a lower balance at that moment means a lower utilization ratio reported to the bureaus.

Monitor your credit report weekly at AnnualCreditReport.com. Each bureau now allows weekly free access.

Set up credit monitoring through myFICO.com, Experian, or your bank. Most send alerts within 24 hours of any report change.

Ask your lender which bureau they report to and on what date. Many customer service reps can tell you this directly.

Consistent monitoring is the one habit that separates people who build strong credit from those who are always reacting to surprises. A good score is not built by checking it once a year; it is built by knowing exactly what is on your report and when new data lands.