Debt causes stress in ways that leads to hopelessnes. Sometimes it starts with a few credit cards. Then a personal loan. Then a collection account. Before long, the total becomes so large that people stop asking how to fix it and start wondering if they're financially ruined.

The other day, I was reading through a Reddit thread from a 23-year-old who was asking a question that caught my attention.

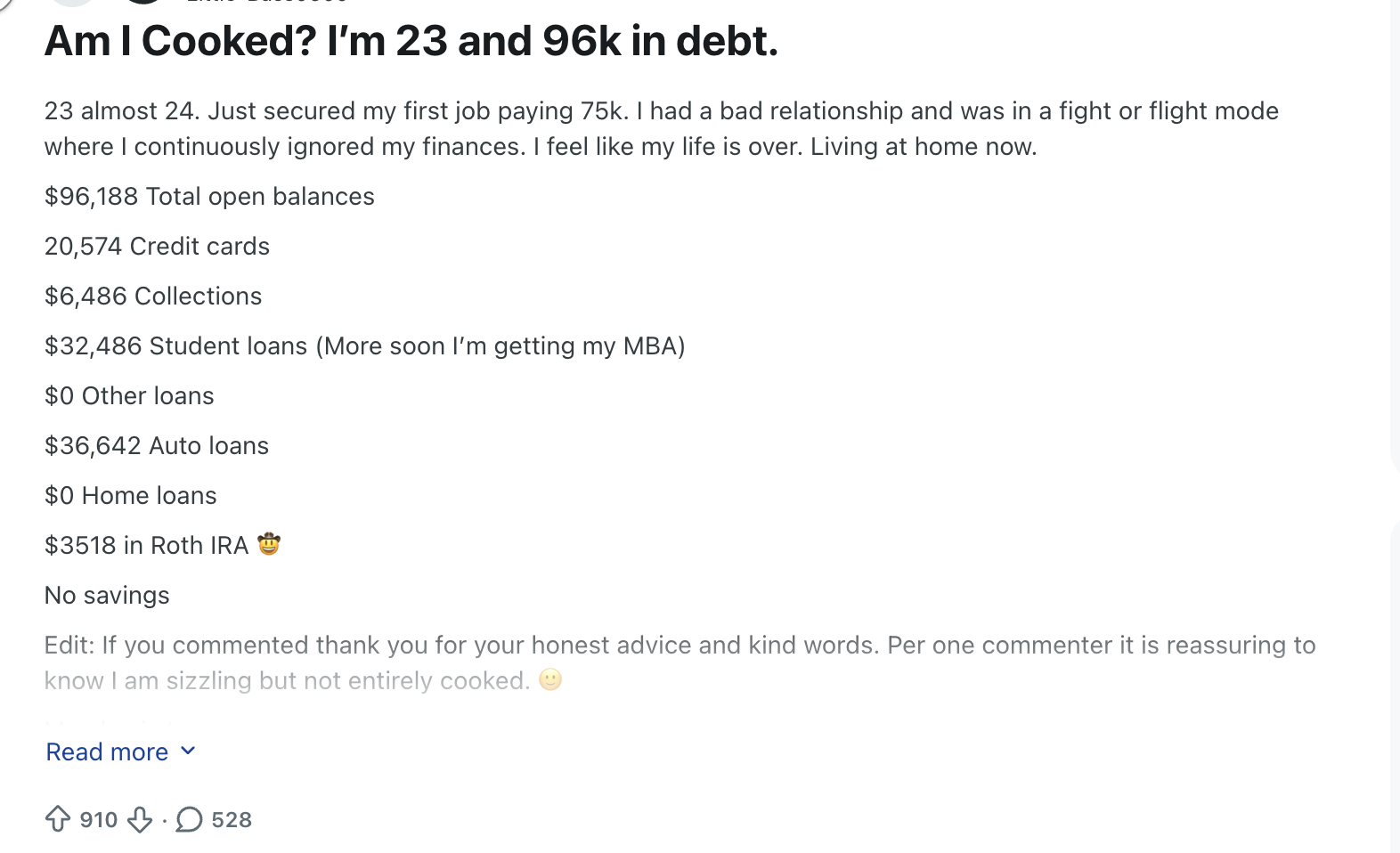

He was carrying nearly $100,000 in debt and genuinely believed his financial life might already be over.

The comments were exactly what you would expect.

Some people told him he was doomed.

Others told him it wasn't that bad.

A few shared their own stories about climbing out of debt.

What stood out to me wasn't the amount.

It was the feeling behind the question.

I've seen the same thing happen with people who contact our credit repair company.

Someone has $15,000 in collections and feels hopeless.

Someone else owes $80,000 and thinks they'll never qualify for a mortgage.

Another person has a credit score in the low 500s and assumes they ruined their future.

The reality is that debt and financial ruin are not always the same thing.

Some people have large balances but a clear path forward.

Others have smaller balances that create bigger problems because they don't have a plan.

Before deciding whether your debt situation is serious, it helps to understand what lenders, creditors, and credit scoring systems actually look at.

Am I Financially Ruined by Debt?

No. Having significant debt does not automatically mean you are financially ruined. Many people recover from collections, charge-offs, repossessions, and large balances by improving cash flow, prioritizing debt strategically, and rebuilding their credit profile over time.

If every person with above-average debt were financially ruined, the entire American middle class would face ruin. Most do not. Most carry the same weight you feel right now. The goal is not to have no debt. The goal is to manage it in a way that keeps the future open.

How Do You Know If Your Debt Problem Is Serious

The seriousness of a debt problem is not measured by the total balance. It is measured by cash flow. If monthly obligations exceed income consistently, that is serious. If debt is growing faster than it can be paid down, that is serious. If basic needs are going unpaid while minimum payments are being made, that is serious. Large debt with stable income and a functioning payment plan is very different from smaller debt with negative monthly cash flow.

Each missed payment adds a new negative item to the credit report, lowers the score, and increases the likelihood of collection activity. One missed payment is an event. Consistent missed payments indicate a cash flow problem that needs structural attention.

When credit is used for necessities because cash runs out before the end of the month, the debt grows even when income is stable. This is a cash flow warning sign , not a character flaw , and it requires a budget intervention, not just a payment plan.

Multiple active collections signal that accounts are past the point of lender patience. The credit damage is already registering. The path forward shifts from prevention to recovery , dispute, validate, negotiate deletion.

No available credit means no emergency buffer. Any unexpected expense forces another missed payment. Getting even one card to 10% utilization creates an emergency cushion while also improving the credit score.

If total monthly expenses and minimum payments exceed take-home pay, the debt grows automatically even without new spending. This is the most serious signal , and it cannot be addressed through debt repayment alone. Income increase, expense reduction, or both are required.

The Biggest Mistake People Make When They Feel Overwhelmed

They stop opening statements. Stop checking credit reports. Stop calling creditors back. Avoidance feels like relief in the short term. It is the most expensive thing a person in debt can do. Late fees compound. Collections accelerate. Credit scores fall further. The problem grows faster when ignored than when engaged , even imperfectly.

Debt avoidance is completely understandable. Nobody wants to look at numbers that feel unmanageable.

But here is what avoidance costs.

A $1,400 unpaid credit card balance that goes to collections. The collector adds fees. The balance becomes $1,900. Two years of avoidance turns a small problem into a significant one. The credit score drops 80 points. A mortgage that was three years away is now five years away.

The antidote to avoidance is not perfect financial management. It is one specific action per week. Pull one credit report. Make one phone call. Pay one bill even partially. Movement creates momentum.

Why Debt Feels Worse Than It Actually Is

Debt feels worst when looking at the total balance. Lenders do not care about your total balance the way your anxiety does. They care about monthly payment patterns, debt-to-income ratio, payment history, and whether obligations are being met. A borrower with $96,000 in debt who makes every payment on time and has a DTI under 40% often qualifies for credit. The number is not the obstacle. The behavior around the number is what determines outcomes.

As NerdWallet's 2026 household debt study confirms, nearly 1 in 4 Americans with revolving credit card debt has no clear plan for paying it off. Feeling overwhelmed by debt is not a personal failure. It is the most common financial reality in the country.

The people who feel most "ruined" are often focused on the total number.

$96,000. $104,000. $140,000.

Lenders do not think in totals. They think in monthly payments, payment patterns, and ratios. A borrower with $96,000 in debt making every payment on time is a more attractive borrower than someone with $30,000 in debt who missed three payments in the last year.

What Should You Pay First

Pay high-interest revolving debt first. Credit cards above 30% utilization suppress the credit score and generate the highest interest costs simultaneously. After credit cards, address collections that are affecting specific financial goals , not all collections, and not before attempting dispute first. Never pay a collection before requesting validation and checking whether it can be deleted rather than just paid.

| Debt Type | Priority | Why |

|---|---|---|

| High-utilization credit cards | Highest | Improves score AND reduces monthly cash drain simultaneously. Fastest score movement available. |

| Collections blocking goals | High | Dispute inaccurate ones first. Negotiate pay-for-delete on valid ones. Do not pay without a strategy. |

| Personal loans | Medium | Reduces DTI when paid off. Check reserve impact before large payoffs. |

| Auto loans | Situational | Positive installment tradeline. Only pay off if near end of term AND reserves stay intact. |

| Student loans | Lower | Large balance, low relative monthly payment. Enroll in income-driven repayment to reduce the DTI number rather than depleting savings. |

| Low-interest installment debt | Lowest | Not worth depleting cash reserves to eliminate. Time and consistent payments handle these. |

Can You Recover From Collections and Charge-Offs

Yes. This is the most common recovery path we see at ASAP Credit Repair. Collections can be removed through debt validation requests and FCRA disputes when the collector cannot produce complete ownership documentation. Charge-offs can be deleted when the reporting is inaccurate. Both take time. Neither is guaranteed. But the success rate when the process runs correctly is high , and the score improvement from a single deleted collection is far greater than from paying it.

Collections are not permanent. That is the most important thing to understand.

Every collection has a maximum 7-year reporting life from the original delinquency date. Many collections cannot be fully validated because documentation degrades at each debt sale. Many collection entries contain inaccurate dates or balances that create FCRA dispute grounds.

At ASAP Credit Repair, removing collection accounts is what we do. We have reviewed over 100,000 credit files. We have filed thousands of FCRA disputes and debt validation requests. The majority of collectors , especially debt buyers who purchased accounts from other collectors , cannot produce the complete chain-of-title documentation the FCRA requires to sustain a dispute challenge.

Understanding what collectors must prove when you challenge them is the beginning of the removal process. The debt validation guide covers exactly what documentation collectors must supply and what gaps in their response mean for the dispute.

What If Your Credit Score Is Already Damaged

Damaged credit scores rebuild. The timeline is 12 to 36 months for most borrowers who start a structured plan. The fastest gains come from utilization reduction (30-60 days), reporting error disputes (30-90 days), and collection deletions (3-12 months). The slowest gains come from waiting for negative items to age off , which happens automatically without any action, but takes longer. Active dispute accelerates what time alone accomplishes slowly.

- Score in the 400s. Achievable to reach 550-580 within 12-18 months with utilization reduction, one or two dispute wins, and consistent on-time payments. That range opens FHA mortgage options.

- Score in the 500s. The 580 FHA threshold is typically 6-18 months away depending on what is causing the score suppression. Utilization alone can close that gap in 30-60 days if that is the primary cause.

- Score in the low 600s. The 620 conventional mortgage threshold and 680 competitive rate threshold are the near-term targets. Getting from 600 to 680 typically takes 12-24 months of consistent action.

- Multiple collections and charge-offs. Each deletion produces a score jump. Three deletions over 12 months compounds significantly. A 490 score with six collections can become a 620 score within 18 months if four of those collections are successfully deleted through dispute.

As Experian's credit rebuilding guide confirms, consistent on-time payments , even on secured cards or credit builder accounts , begin improving credit scores within a few months, and the improvement compounds over time as positive history accumulates alongside any dispute wins.

How Long Does Debt Recovery Usually Take

| Problem | Typical Recovery Timeline | Key Action |

|---|---|---|

| High utilization | 30 to 90 days | Pay cards to under 10% before statement close |

| Reporting errors | 30 to 90 days | FCRA dispute with all three bureaus |

| Collection accounts | 3 to 12 months | Validate, dispute, or pay-for-delete |

| Charge-offs | 6 to 24 months | FCRA dispute for inaccuracies; pay-for-delete if valid |

| Major credit rebuild | 12 to 36 months | Secured card + credit builder + consistent on-time payments |

Should You Consider Debt Consolidation

Debt consolidation can help , but it is not the first step. The first step is identifying which debts can be deleted through dispute. A personal loan that pays collections while those collections can still be disputed and deleted costs money for an outcome that a free dispute could have produced. Consolidation works best after dispute outcomes are known , consolidating what remains after cleanup, not instead of it.

The consolidation question usually comes up when dealing with multiple collectors feels overwhelming.

One payment instead of five. One rate instead of five. One lender instead of five collectors calling.

Those are real benefits. But the order matters.

Dispute the inaccurate accounts first. Free process. Can produce deletion. Challenge the obsolete accounts (past 7 years from original delinquency). Required removal. No payment. Then evaluate whether a consolidation loan for remaining valid debts makes financial sense at the available rate.

At 500-580 credit scores, consolidation loan rates average 25-30% APR. That is expensive debt to pay more expensive debt. Run the full cost calculation before committing.

Can You Still Buy a House Someday

Yes. In most cases, debt delays homeownership , it does not permanently prevent it. FHA loans require 580 minimum credit score. Most borrowers who start credit repair from a score in the 500s reach FHA-eligible status within 18 to 24 months of consistent action. The path is: delete collections, reduce utilization, establish positive payment history, maintain stable income. Mortgage lenders evaluate who you are financially at the time of application , not who you were at your worst.

The borrowers who reach out to ASAP Credit Repair often say the same thing.

"I just want to own a house someday."

That goal is realistic from almost any starting point. The timeline depends on how much cleanup the credit file requires. Three collections and 90% utilization = roughly 18-24 months to FHA eligibility with focused work. A bankruptcy from four years ago = the seven-year mark brings natural recovery alongside active credit building.

The key is starting now rather than later. Every month of delay is a month of credit building time that does not compound.

The guides on what mortgage rates look like once the score starts to improve , and why each 20-point gain saves real money , can be found in the 630 credit score mortgage guide. That destination is closer than most borrowers starting at 490-520 think.

What Does a Debt Recovery Plan Actually Look Like

Free at AnnualCreditReport.com. Write down every account: the type, the balance, the status, the original delinquency date, and which bureaus show it. This is the baseline. Most people doing this for the first time discover accounts they had forgotten about. Some discover accounts that do not belong to them at all.

Check each negative account: Is the original delinquency date more than seven years ago? Dispute as obsolete. Does the balance match your records? If not, dispute the inaccuracy. Is this a debt buyer who cannot have complete chain-of-title documentation? Request validation. Many borrowers discover that two or three of their collection accounts are either obsolete, inaccurate, or unverifiable. Those come off without any payment.

This is the fastest score movement available. Even getting one maxed-out card to 30% produces visible score improvement in the next billing cycle. Paying before the statement closes ensures the lower balance reports to the bureaus. If money is tight, start with the highest-utilization card first , not the highest-balance card.

A secured credit card with a $200-$300 deposit reports as a revolving account. Keep the balance under 10% of the limit. Pay in full every month. After six months of perfect history, the positive payment record begins contributing meaningfully to the score. A credit builder loan at $5-$10/month adds installment history without a hard inquiry.

One new missed payment after starting the repair process undoes months of work. It adds a fresh negative item to all three bureaus. Set every bill to autopay for the minimum. That single habit , catching everything before it misses , protects the momentum that everything else builds. The minimum payment prevents damage. Extra payments accelerate the goal.

As the FTC's managing debt guide confirms, identifying all debts, prioritizing payments strategically, and seeking help when the load becomes unmanageable are the same steps that financial professionals recommend. The path from overwhelmed to stable follows a consistent pattern , and that pattern is learnable and executable without perfection.

Signs You Are Making Progress

The 23-year-old with $96,000 in debt asking "am I cooked?" is carrying less than the average American household balance. Collections can be removed. Credit scores rebuild. Mortgages become possible. The deciding factor was never the amount owed. It was always whether someone had a plan and worked it. That plan starts with a single audit of what each bureau actually shows.

Am I financially ruined if I have collections on my credit report?

No. Collections are removable. Many are inaccurately reported and can be disputed and deleted through the FCRA process. Others can be resolved through pay-for-delete agreements. Even collections that remain on the report lose their scoring impact over time , and at seven years from the original delinquency, they must be removed entirely. A 2026 credit report with four collections can become a clean report by 2027 or 2028 with consistent dispute work.

Can I recover financially at 23 with $96,000 in debt?

Yes. Especially at 23. Time is the most powerful asset in financial recovery , and at 23, there is significant time. The $96,000 balance is also below the national average household debt of $105,444 (Q1 2026). The path forward is a structured plan: identify disputable accounts, pay down high-utilization credit cards, establish consistent payment history, and work toward the score milestones that open mortgage and other financing options. Most borrowers starting this process at 23 are in a home before 30.

What is the fastest way to recover from overwhelming debt?

Two parallel actions produce the fastest results: (1) pay credit card balances to under 10% of each card's limit , this improves the credit score within 30 days and reduces monthly cash drain, and (2) file FCRA disputes for any inaccurate collections or charge-offs , deletion of even one collection can add 30-70 points in 30-90 days. These two actions running simultaneously often produce 50-100 point score improvements within 90 days , faster than any other credit repair strategy.

-

Should You Use a Personal Loan to Pay Off Collections? When the debt feels overwhelming and consolidation feels like the answer, this covers the critical question: should you consolidate before or after pursuing collection removal? The answer is almost always after , because paying collections before disputing them forfeits the dispute grounds that could have produced free deletion. This covers the full framework: when consolidation helps, when it creates more cost, and why the dispute-first approach consistently outperforms payment-first for most borrowers.

-

Should I Pay Off Debt Before Applying for a Mortgage? For borrowers who want to know what happens after the recovery , specifically, what the mortgage path looks like from a debt-heavy starting point , this covers which debt to pay first, when paying debt can actually hurt approval by depleting reserves, and the 90-day pre-mortgage strategy that produces the best file. The bridge from "overwhelmed by debt" to "mortgage-ready" is more direct than most people assume once the sequence is clear.

-

How Long Does It Take to Raise a Credit Score? Realistic Timelines The recovery timeline chart in this article shows each debt type and how long resolution takes. This covers the full action-by-action improvement breakdown , from utilization reduction in 30-60 days through collection deletion in 3-12 months to full credit rebuild in 12-36 months , with point estimates for each action. For someone starting from an overwhelmed place, this is the planning guide that turns "someday" into a specific month and year.