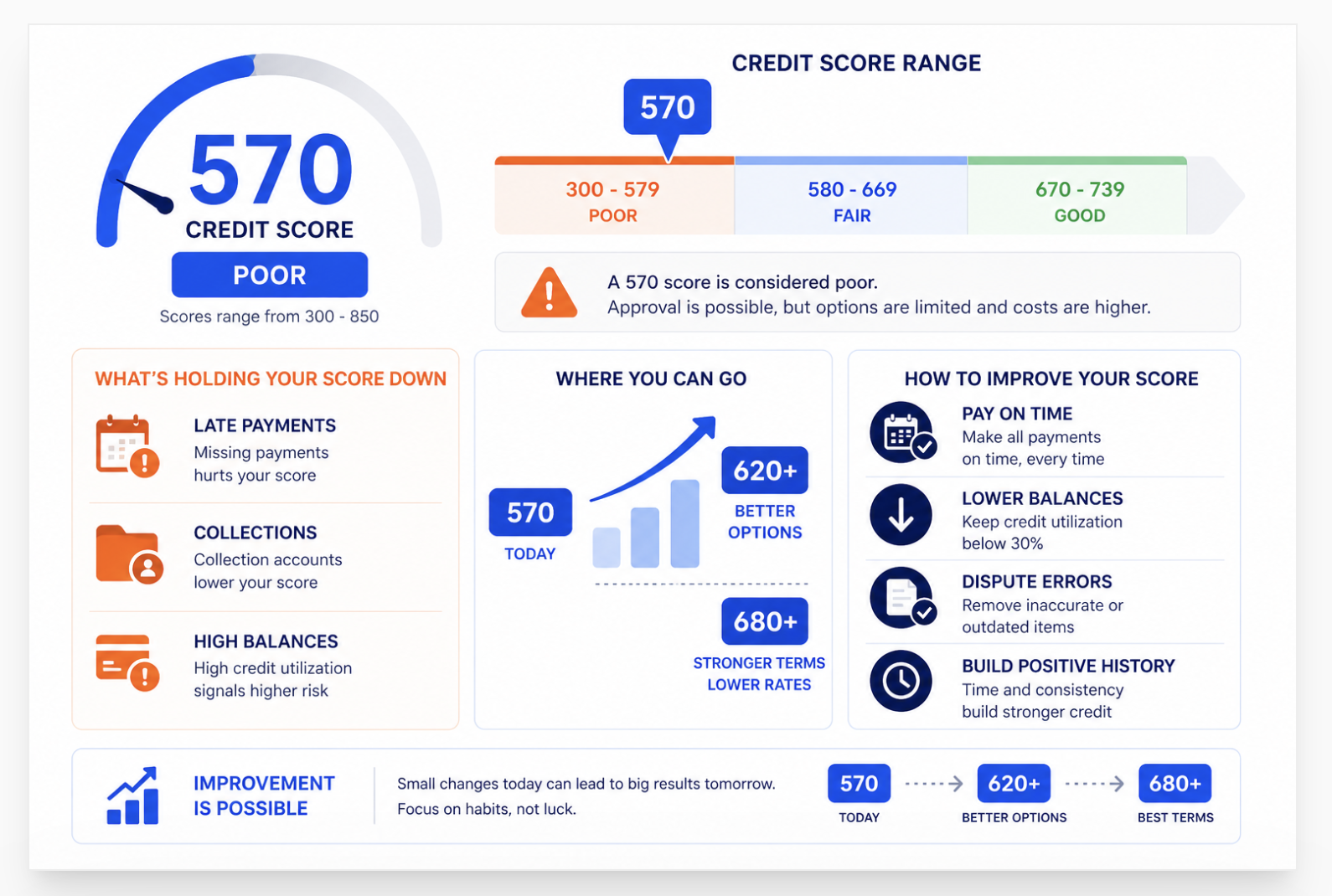

Is 570 a good credit score? No, it's not.

In most lending models, 570 is considered poor credit, not good credit. It can still qualify for some financing, but approval options are narrower, rates are higher, and lenders often review the full file more closely. A 570 credit score usually signals missed payments, high balances, limited history, collections, or a mix of these issues.

I own a credit repair company, and scores in the 500 range are some of the most memorable files we work on because they often have the clearest path for improvement. I remember one client who came in frustrated after being denied for a basic credit card. Her score was in the mid-500s, but the problem was not only the score. It was maxed-out cards, two recent late payments, and one collection account that was reporting inaccurately. Once those issues were addressed, the file changed faster than she expected. That pattern is common.

Real consumer behavior supports that. On personal finance forums like Reddit communities focused on credit rebuilding, many users with scores near 570 report that lowering credit utilization often creates the first noticeable score jump. Resources from the Consumer Financial Protection Bureau point to payment history and amounts owed as two of the largest factors in credit scoring. Those are usually the first areas to review.

That is why the better question is not simply “Is 570 good?”

It's better to ask, "What is holding the 570 score down, and how fast can that change?

This article breaks down what a 570 credit score means. See what approvals may still be possible, and what steps usually create the fastest improvement.

Last quarter alone, we reviewed 28 client files starting at 560-580. The most common finding: at least one inaccurate entry per file. In 9 of those 28 cases, a single dispute removal moved the score above 580 within 35 days. Nine clients cleared the FHA 3.5% threshold without making a single payment to a creditor. The error was on the report. The cost was zero.

Is 570 a Good Credit Score?

No. FICO classifies 570 as Poor (300-579). It falls at the top of the lowest FICO tier, just 10 points below the 580 threshold that separates two entirely different sets of mortgage options. About 16% of Americans currently score below 580. At 570, the loans you access come with the highest available interest rates in each product category.

FICO's five score tiers run from Poor (300-579), to Fair (580-669), to Good (670-739), to Very Good (740-799), to Exceptional (800-850). A 570 score sits at the top of the lowest tier. That position matters for one specific reason: the FHA 580 boundary.

The Federal Housing Administration draws a hard line at 580. Above it, borrowers qualify for 3.5% down. Below it, the minimum down payment jumps to 10%. Ten points from 570 to 580 costs or saves an additional 6.5% in down payment on a home purchase. On a $300,000 home, that is $19,500 in cash needed at closing. That gap is the most consequential single score threshold for most 570-score borrowers.

According to Experian's mortgage rate data, the average FHA loan borrower carries a 674 FICO score at a 6.41% rate. A 570-score borrower accessing the same FHA product faces a higher rate, higher mortgage insurance premiums, and stricter underwriting conditions even after clearing the 500 minimum that technically allows access.

The chart shows the rate drop that accelerates above 600 and again above 660. A 570-score borrower sits in the second-highest rate band. Moving to 600 produces a meaningful rate improvement. Moving to 660 produces the largest single-step improvement available on the chart. Each score milestone unlocks a different rate tier, not just a slightly better number on the same tier.

A 570 FICO score sits in the Poor tier (300-579), 10 points below the FHA 580 boundary and 50 points below the conventional loan 620 minimum. Auto loan rates at this score run 16-21% APR. Over 50% of unsecured credit card applications below 580 get rejected. The score is recoverable. The 580 threshold is the first and most financially meaningful target.

What Can You Get with a 570 Credit Score?

| Product | Access at 570 | Conditions | What Changes at 580 |

|---|---|---|---|

| FHA Mortgage | Qualified , 10% down | 10% down required. Rate ~8%+ at this tier. Very few lenders serve below-580 FHA. Strict manual underwriting. | Down payment drops to 3.5%. On $300K home, saves $19,500 at closing. |

| Conventional Mortgage | Closed | Fannie Mae and Freddie Mac require 620 minimum. 50 points short. | Needs 620, not just 580. Target for bigger picture planning. |

| VA Loan | Possible if veteran | No VA minimum, but most lenders set 580-620. 570 may require a sympathetic lender. | At 580, far more VA lenders willing to approve. Shop 3+ lenders. |

| Auto Loan (new) | Qualified , subprime rates | 16-21% APR typical for 500-589 range (Experian Q3 2025). BHPH and subprime lenders most accessible. | Near-prime rate tier (601-660) offers ~12% APR. $89-$120/mo difference on $25K loan. |

| Credit Card | Secured only | Secured cards with $200-$500 deposit. Over 50% of unsecured applications rejected below 580 (NY Fed). | At 580, some unsecured starter cards accessible. At 620+, broader product access. |

| Personal Loan | Credit union / subprime lender | 15-30% APR. Credit unions most flexible. Many banks decline below 600. | Slightly better odds at 580+. Real improvement at 640+. |

The 10-Point Gap: Why 570 to 580 Matters More Than Any Other 10 Points

Most score improvements produce gradual changes: a slightly better rate, a marginally easier approval. The jump from 570 to 580 produces a structural change in mortgage access.

Below 580: FHA requires 10% down. Very few FHA lenders offer loans below 580 at all. The ones that do use manual underwriting, which takes longer and involves more scrutiny of every financial detail.

At 580: FHA drops to 3.5% down. Dozens more lenders participate. The approval process moves closer to standard automated underwriting. Per Bankrate's 2026 FHA rate data, the average 30-year FHA rate sits at 6.30% APR as of April 2026. Reaching 580 puts you into that mainstream FHA lending pool instead of the narrow subprime FHA segment.

For buyers planning a home purchase, zero down mortgage credit score requirements cover the VA and USDA paths that 570-score borrowers sometimes qualify for depending on their specific lender and service history. Both programs offer routes that look past the 570 score if other factors are strong.

The Fastest Path from 570: Hitting the Thresholds That Matter

The 570-score rebuild has two distinct phases. Phase one targets 580 , the FHA 3.5% down threshold. Phase two targets 620 , the conventional loan floor. Both are reachable faster than most people expect.

Most 570-score borrowers reach 580-620 within 60-90 days. Some reach it faster. The speed depends entirely on what is currently suppressing the score.

Pull all three reports at AnnualCreditReport.com. Look for wrong dates, wrong balances, accounts you do not recognize, or collection accounts with an incorrect original delinquency date. File disputes at Equifax, Experian, and TransUnion simultaneously. Each bureau has 30 days to investigate. A removed collection or corrected date can produce a 30-60 point gain. In our client files at 560-580, we find at least one disputable entry in 9 out of every 28 files reviewed. That entry, when removed, clears the 580 threshold without any payment.

30-45 days | Up to 60 points per removed itemUtilization is 30% of your FICO score. It updates every billing cycle. Pay card balances down before the statement date, not the due date. The balance that posts on your statement is what reports to the bureaus. Getting every card below 30% is the first target. Below 10% produces the maximum gain. A card at 80% utilization contributing to a 570 score can add 20-40 points in a single cycle when paid to near zero.

1 billing cycle (25-35 days) | 20-40 points possibleAsk a parent, spouse, or trusted friend to add you to their credit card as an authorized user. The account must be at least 5 years old, have no missed payments, and carry low utilization. Their full account history appears on your report within one statement cycle. You do not need to use the card. The account adds positive payment history, available credit, and account age to a file that often has very little of any of these at 570.

30-60 days | 20-50 points possibleA secured card builds payment history (35% of FICO) month by month. Choose a card that reports to Equifax, Experian, and TransUnion , not all secured cards do. Keep the balance below 10% of the limit. Pay in full before the statement date. This is slower than steps 1-3 but builds the positive payment history foundation that sustains score improvement after the dispute and utilization gains are complete.

3-6 months | 20-40 points over timeRunning steps 1, 2, and 3 simultaneously instead of one at a time compresses the timeline from 90+ days to 35-60 days. Most borrowers start with utilization because it feels like something they can control today. Disputes often produce bigger score movements faster. Doing both at once produces the fastest result.

For the specific path from the Poor tier toward Fair and beyond, our detailed analysis of how to move from 500 to 700 covers the exact behavior patterns at each 50-point interval, including what changes in lender behavior and product access at 580, 620, and 650 specifically.

How a 570 Score Affects Real Costs

The interest rate penalty at 570 is not small. Here is what borrowers at this score range pay more than prime-tier borrowers over the life of common loan products.

| Loan | At 570 (subprime) | At 720 (prime) | Extra Cost |

|---|---|---|---|

| Auto loan , $25,000 / 60 months | ~17% APR = $623/mo | ~6.4% APR = $490/mo | $133/mo, $7,980 total |

| FHA mortgage , $280,000 / 30yr (10% down) | ~8.1% APR = $2,082/mo P+I | FHA at 674 avg = ~6.41% | ~$200/mo, ~$72,000 over 30yr |

| Secured credit card , $500 limit / annual fee | 25-29% APR + $75-$100 fee | No fee rewards card at 18% APR | $75-$100/yr fee plus higher APR on balance |

| Personal loan , $5,000 / 36 months | 20-28% APR typical | 7-12% APR typical | $1,000-$2,200 extra over 36 months |

These numbers show why the fastest return on a 570-score borrower's time is not finding the least-bad loan at 570. It is improving the score by 10-50 points before applying. A 90-day delay in buying a car that allows the score to move from 570 to 625 saves $80-$130 per month over the entire 60-month loan term. That 90-day wait returns $4,800-$7,800 in total savings.

For context on where 570 sits relative to the next milestone up, our breakdown of what a 621 credit score means covers the lending landscape at the Fair tier, showing exactly which products open and at what rates once you clear 580 and then 620.

Is 570 a good credit score?

No. FICO classifies 570 as Poor (300-579). It sits at the top of the lowest tier, 10 points below the FHA 580 boundary that determines whether you need 3.5% or 10% down on a mortgage. Auto loans are available at subprime rates of 16-21% APR. Most unsecured credit cards are not accessible. The score is recoverable. A 10-point gain produces the most immediate financial change of any score movement near this level.

What can I get with a 570 credit score?

FHA mortgage with 10% down (3.5% requires 580), VA loan from some lenders if you qualify for VA benefits, auto loans at 16-21% APR, secured credit cards with a cash deposit, and personal loans from credit unions or subprime online lenders. Conventional mortgages, rewards credit cards, and competitive loan rates are not accessible at 570. Each product that approves you at 570 carries the highest rate available in its category.

How long does it take to raise a 570 credit score to 620?

For most borrowers, 60-90 days with parallel action: dispute inaccurate entries at all three bureaus (30-45 days for results), reduce credit card utilization below 10% (one billing cycle), and get added as an authorized user on an aged account (30-60 days). If the score sits at 570 due to inaccurate entries alone, the timeline can shorten to 35-45 days. If the 570 reflects accurate recent late payments with no errors, the timeline extends to 6-18 months of clean payment behavior.

Can I buy a house with a 570 credit score?

Yes, with FHA financing and 10% down. A $300,000 home requires $30,000 down at 570, compared to $10,500 at a 580 score. Very few FHA lenders serve below-580 borrowers, so expect to shop 5-10 lenders before finding a willing one. Expect a rate above the national FHA average and higher mortgage insurance costs. For most buyers, the better financial decision is taking 30-60 days to push the score above 580 before applying, which cuts the down payment by 6.5% and expands lender options significantly.

9 in 28 Clients at 560-580 Had a Removable Error Holding Them Below 580

Before you accept a 10% down FHA requirement or a 17% auto loan rate, find out if an inaccurate entry on one of your three bureau reports is what keeps your score below 580. A free 3-bureau audit shows every entry across Equifax, Experian, and TransUnion and identifies what is disputable right now.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required