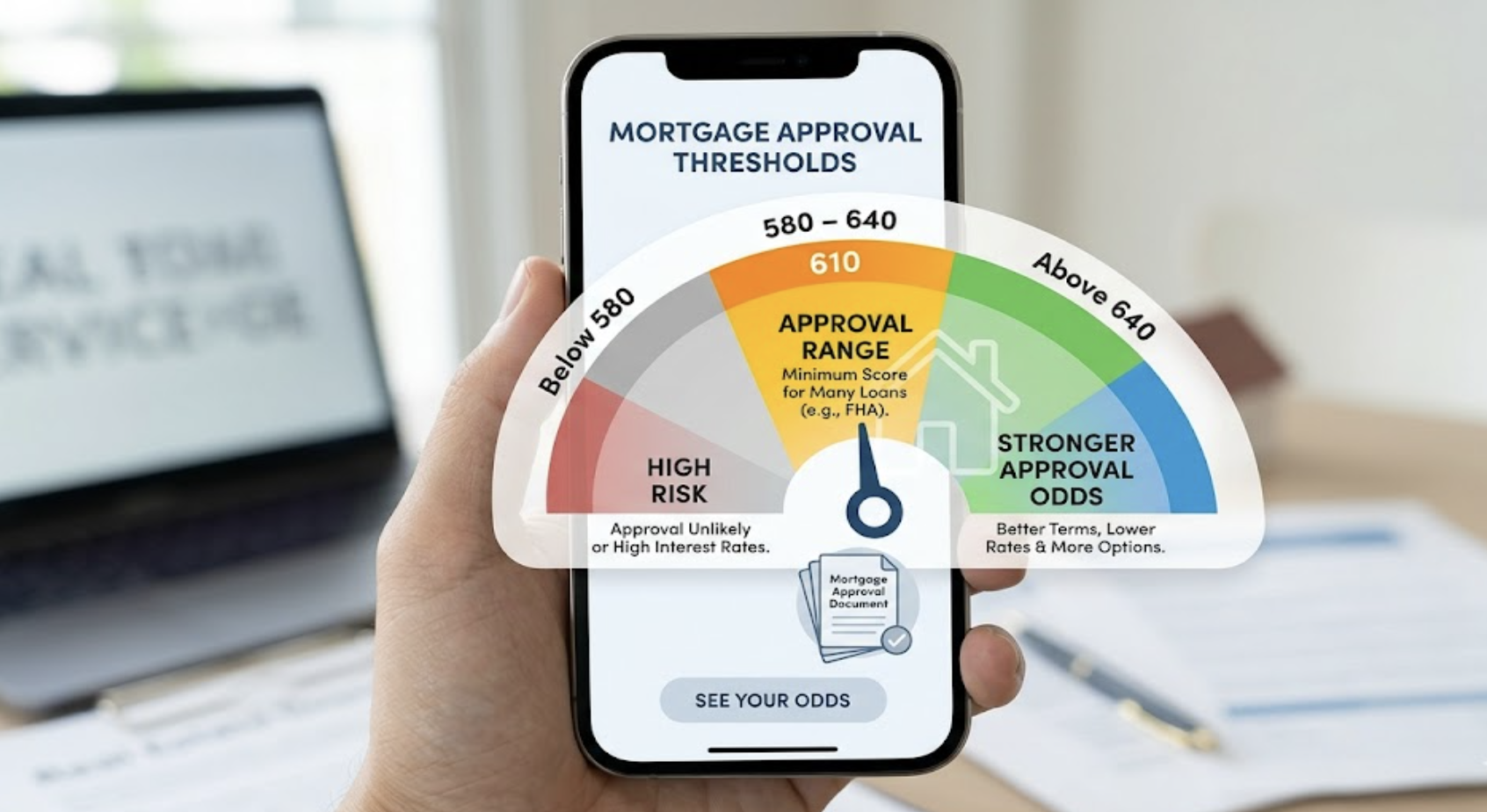

The credit score needed for a zero-down mortgage depends on the loan type. But in practice, I'd say that most approvals fall into a narrow range.

VA and USDA loans are the main zero-down options. Neither program sets a strict minimum score, but lenders usually require around 580 to 640, depending on the file.

In real applications, this is where expectations break. Many people see “no minimum score” and assume approval is flexible. It is not. Files under 580 rarely move unless there are strong compensating factors like stable income, low debt, or cash reserves. Most approved buyers cluster closer to 620, even for zero-down programs, because lenders apply their own risk standards on top of the base guidelines.

Working with credit profiles, preparing for mortgage approval, the difference is not just the score. It is how the report is structured. Two people can both have a 620, but one gets approved, and the other does not. Late payments, high utilization, or recent collections can block approval even when the score technically qualifies.

A 0 down mortgage is possible with average credit, but approval comes down to how clean and stable the report looks when the lender reviews it.

This article breaks down the actual score ranges, what lenders look for beyond the number, and how to position your credit to qualify.

Zero Down Mortgage · Credit Score for USDA Loan · VA Loan Credit Requirements · No Down Payment Home Loan · First-Time Home Buyer

Updated April 2026 · Sources: Home Mortgage Disclosure Act (HMDA) 2024 data, Veterans United loan analysis, The Mortgage Reports 2026, USDA Rural Development guidelines, FICO Score Credit Insights Fall 2025

- Two true zero-down mortgage programs exist: VA loans and USDA loans. Both are government-backed. Neither requires a down payment.

- The VA does not set a minimum credit score, but most lenders require 580 to 620. VA borrowers averaged a 725 FICO score in 2024.

- The USDA does not set a minimum credit score, but most lenders require 620 to 640. The 640 cutoff triggers automated approval. USDA borrowers averaged 700 in 2024.

- In November 2025, Fannie Mae and Freddie Mac dropped their hard 620 minimum for conventional loans, but conventional loans still require a down payment for most buyers.

- Zero down does not mean zero cash needed. Closing costs still apply to both VA and USDA loans, though both can be partly financed or covered by seller concessions.

If you want to buy a home with no money down, two government programs make it possible: VA loans and USDA loans. Both are real programs with real approvals happening every day. But neither one is a guarantee. You still have to qualify, and your credit score is a key part of that process.

This article breaks down exactly what credit score you need for each zero-down program, what the data shows about actual approved borrowers, and what to do if your score is not there yet.

What Credit Score Is Needed for a Zero Down Mortgage?

Here is how each program compares on credit score requirements:

| Loan Program | Down Payment | Govt. Min. Score | Typical Lender Min. | Avg. Borrower Score (2024) |

|---|---|---|---|---|

| VA Loan | 0% | None | 580-620 | 725 |

| USDA Guaranteed Loan | 0% | None | 620-640 | 700 |

| FHA Loan | 3.5% (or 10%) | 500 / 580 | 580 | 692 |

| Conventional (Fannie/Freddie) | 3%+ | None (as of Nov. 2025) | 620-700+ | 755 |

The gap between the "program minimum" and the "average borrower score" tells you something important. While a VA loan technically allows a 580 score with the right lender, most VA borrowers in 2024 had scores around 725. That is because lenders apply their own overlays, and competing borrowers tend to be better-qualified. A score of 620 may qualify you on paper for a VA loan, but it makes approval harder, not just in theory but in practice.

Who Qualifies for a VA Loan with No Down Payment?

The VA loan is widely considered the best mortgage program available for eligible borrowers. It offers true zero-down purchase financing, no private mortgage insurance, and competitive rates even with lower scores. The only VA-specific upfront cost is the VA Funding Fee, which ranges from 1.25% to 3.3% of the loan amount depending on down payment size and whether it is your first VA loan. The fee can be rolled into the loan balance, so it does not require cash at closing.

To confirm your eligibility, you will need a Certificate of Eligibility (COE). You can request one through your lender, who can often obtain it directly from the VA through an online system in minutes.

That experience lines up with what lenders report: a VA borrower below 640 can still close, but the debt-to-income ratio becomes more of a deciding factor. The VA's guideline for DTI is 41%, but lenders can approve beyond that with compensating factors such as strong cash reserves, stable long-term employment, or a history of paying housing costs above the new mortgage amount.

Before you apply for any mortgage program, it helps to understand whether your credit and financial profile reflect the signs that lenders look for. Our breakdown of the signs that you are ready for a mortgage covers the income stability, credit history, and debt ratio benchmarks that lenders actually evaluate beyond the minimum score requirement.

Who Qualifies for a USDA Loan with Zero Down?

The phrase "rural area" is broader than most buyers expect. The USDA's eligible area map includes many suburbs near mid-size cities, small towns, and rural communities across 97% of U.S. land area. Before assuming you do not qualify on location, check the USDA's eligibility map at USDA.gov with a specific address.

USDA loans also come with two fees that replace private mortgage insurance:

- Upfront guarantee fee: 1% of the loan amount. Can be rolled into the loan.

- Annual guarantee fee: 0.35% of the remaining loan balance, paid monthly. This stays for the life of the loan unless you refinance into a conventional loan.

Compare that to FHA loans, which charge 1.75% upfront and 0.55% annually. The USDA fees are lower, which is one reason mortgage professionals often recommend USDA over FHA for buyers who qualify on location and income.

That story reflects two things the data confirms: a 638 score can get approved through manual underwriting, and closing costs are the practical hurdle even when the down payment is zero. Seller concessions are allowed up to 6% of the loan amount under USDA guidelines, which gives buyers real negotiating room to cover those costs.

The orange bars show the average credit score of borrowers who actually got approved. For VA loans, that is 725. For USDA, it is 700. The blue bars show where most lenders set their floor. The gap between those two numbers is where the competition lives. A 620 score qualifies you on paper for a USDA loan, but the average approved USDA borrower is at 700. That means a 620-score borrower is competing against stronger applications and faces more lender scrutiny.

Can You Get a Mortgage with 0 Down and Bad Credit?

The term "bad credit" means different things in different mortgage programs. In conventional lending, a score below 620 used to block you entirely. In VA and USDA lending, it means harder, not impossible. The lender looks at your complete picture: your payment history over the last 12 months, your debt-to-income ratio, how long you've held your job, and whether any negative marks are isolated events or a pattern.

One thing that does not help: a very recent negative event. A 30-day late payment from last month carries more weight than a collection account from four years ago. If you know you are borderline, spend three to six months building a clean recent payment record before applying. Every month of clean payments after a negative event reduces its weight in an underwriter's manual review.

If your credit score is currently below 600 and you are targeting a zero-down mortgage, the most efficient path is not to apply now and get denied. A denial with a hard inquiry on your report costs you points and starts a clock. A better path is to address the issues in your report first. Our guide on getting a mortgage approved with bad credit walks through how lenders evaluate damaged credit files, which negative marks cause the most friction with VA and USDA underwriters, and what moves make the most difference before you apply.

How to Qualify for a Zero Down Mortgage: Step by Step

- Confirm which zero-down program you qualify for. VA loans require military service documentation and a Certificate of Eligibility. USDA loans require the home to be in a USDA-eligible area and your household income to fall below the area limit. Check USDA.gov's eligibility map with a specific property address before you tour a home. These requirements do not flex based on how much you want the property.

- Pull all three credit reports and check your middle score. Mortgage lenders use the middle of your three bureau scores. If your Experian score is 645, your TransUnion is 628, and your Equifax is 619, the lender uses 628. Pull free reports from AnnualCreditReport.com. Look for errors, wrong late payment dates, and accounts you do not recognize. Dispute any inaccurate entry before you apply.

- Calculate your debt-to-income ratio and reduce it if needed. Divide your total monthly debt payments by your gross monthly income. Both VA and USDA guidelines target 41% or below. If you are above 41%, pay down credit card balances or eliminate a small installment loan before applying. Each debt payment you remove changes the ratio materially at lower income levels.

- Get pre-approved with a lender that specializes in your target program. For VA loans, Veterans United, Navy Federal Credit Union, and USAA are established specialists. For USDA loans, Neighbors Bank is among the top USDA lenders by volume. Pre-approval letters show sellers you are financially qualified and ready to close, which matters in competitive markets even for zero-down buyers.

- Plan for closing costs separately from the down payment. Zero down means no down payment, not no cash required. USDA closing costs typically run 3% to 6% of the loan amount. The 1% upfront guarantee fee can be rolled into the loan. VA closing costs are similar, with the funding fee (1.25% to 3.3%) also rollable. Use seller concessions, gift funds, or a down payment assistance program to cover what remains. Both VA and USDA allow sellers to contribute toward closing costs.

After you close, the structure of your mortgage can matter as much as getting approved. Understanding tools like a mortgage recast can help you reduce your payment later without refinancing. Our mortgage recast guide explains how this works, when it makes financial sense, and which loan types are eligible, which matters if you receive a lump sum after closing and want to reduce your monthly obligation.

What Happens If Your Credit Score Is Too Low Right Now?

As The Mortgage Reports documents, the most common factors that push borderline applicants over the approval line are: a consistent 12-month history of on-time payments, credit utilization kept below 30% across all cards, and no new derogatory marks in the six months before application. These are all things you control directly.

The fastest credit gains at the 580 to 620 range typically come from paying credit card balances below 10% of each card's limit. Utilization is 30% of your FICO score and recalculates every billing cycle. A single billing cycle of low utilization can add 30 to 50 points. That may be the difference between a denial and a pre-approval.

If you have gone through a financial hardship that damaged your credit and you are asking whether homeownership is realistic again in the near term, look at the actual benchmarks. Our guide on the signs you are ready for a mortgage is built around the real criteria lenders use, not the aspirational ones. It gives you a checklist grounded in what actually gets loans approved.

Is a Zero Down Mortgage a Good Idea?

The trade-off is real. A zero-down buyer on a $250,000 USDA loan at a competitive rate pays more each month than someone who put 10% or 20% down, because the loan balance is larger. The monthly USDA guarantee fee of 0.35% also stays for the life of the loan unless refinanced away later.

That said, for a buyer who would otherwise rent for three to five more years while saving a down payment, the math can favor buying now. Home prices have risen significantly over the past five years. Waiting to save may cost more than the interest premium from a slightly higher loan balance.

The right comparison is not "zero down vs 20% down." It is "zero down mortgage payment vs. rent plus five more years of saving." Run both numbers for your specific market before deciding.

Know Your Credit Score Before the Lender Does

A free 3-bureau audit shows every entry across your Experian, TransUnion, and Equifax reports. It identifies errors that are dragging your score below VA or USDA thresholds, and which items may be disputable before you apply for a mortgage.

Get My Free Credit Audit → Secure · 2 minutes · No credit card requiredFrequently Asked Questions

What credit score do you need for a zero down mortgage?

For a VA loan, the VA sets no minimum, but most lenders require 580 to 620. For a USDA loan, the USDA sets no minimum, but most lenders require 620 to 640. The 640 USDA threshold matters because it unlocks the automated underwriting system. Below 640, the loan goes to manual underwriting, which is slower but still approves qualifying borrowers.

What is the lowest credit score to buy a house with no money down?

Through a VA loan, some lenders accept scores as low as 540. Guild Mortgage publicly advertises VA approval with 540 credit scores. For USDA loans, manual underwriting can approve borrowers with scores below 620 if they have compensating factors such as stable employment, low debt-to-income ratio, and clean recent payment history. In practice, most zero-down approvals happen at 600 or above.

Can you get a mortgage with 0 down and bad credit?

Yes, through a VA loan if you are eligible based on military service. VA loans have no government minimum score, and some lenders approve borrowers in the 580 to 600 range. USDA loans are harder with bad credit because most lenders require 620 to 640, and below that, you need a strong compensating factors case for manual underwriting. Neither program eliminates the credit check entirely.

What credit score is needed for a USDA loan?

The USDA does not set a minimum. Most lenders require 620 to 640. The 640 score matters because it is the cutoff for the USDA's automated Guaranteed Underwriting System. Borrowers below 640 go through manual underwriting. The average USDA borrower had a 700 credit score in 2024, according to HMDA data.

Does a VA loan require a down payment?

No. VA loans require no down payment for eligible borrowers. There is also no private mortgage insurance requirement. The VA Funding Fee, which ranges from 1.25% to 3.3% of the loan amount, is the only VA-specific cost, and it can be rolled into the loan balance. Borrowers with service-connected disabilities may be exempt from the funding fee entirely.

Is it better to get a USDA loan or VA loan?

If you qualify for both, a VA loan is generally better. It has no income limits, no location restrictions, no monthly mortgage insurance, and more flexible credit requirements than USDA. USDA loans are the better choice if you do not qualify for a VA loan and are buying in an eligible rural or suburban area within the income limits. Both offer zero down payment and government backing.

-

How to Go From 500 to 700 Credit Score Fast If your score is below the VA or USDA lender minimums, this covers the specific steps that produce the fastest gains: utilization paydown, error disputes, authorized user additions, and the AZEO method used by top FICO scorers.

-

Loan Modification vs Refinancing: Which Is Right for You? After you close on a zero-down mortgage, your options for adjusting the terms later depend on whether you pursue modification or refinancing. This breaks down the differences, eligibility requirements, and credit impact of each.

-

How to Stop Foreclosure Without Paying the Full Balance For homeowners in financial hardship after closing on a zero-down loan, this covers the legal options available before a foreclosure auction, including short sale approval, deed in lieu, and how to get the foreclosure process suspended while a sale is pending.

Closing

There is no single credit score that guarantees a 0 down mortgage. Most approvals fall between 580 and 640, but the score alone does not decide the outcome. Lenders look at the full profile, including payment history, balances, and recent activity.

If the score is below range, the focus should be on removing negative accounts, lowering utilization, and stabilizing reporting before applying. If the score is already in range, the goal is to avoid new issues and keep the file consistent until closing.

Approval is not about hitting a number. It is about presenting a file that the lender can approve.