Pay-for-delete letters are written request asking a debt collector to remove a collection account from your credit report in exchange for payment. The goal is simple. You settle the debt, and the collector deletes the negative tradeline instead of updating it as paid. When it works, it can improve a credit file faster than paying without terms.

Many consumers make one mistake. They pay first and ask questions later. In credit files we review, that often leads to disappointment. The balance updates to zero, but the collection remains on the report for up to seven years from the original delinquency date. The score damage may continue even after payment, especially under older scoring models that lenders still use.

Data from the Consumer Financial Protection Bureau continues to show that debt collection remains one of the largest complaint categories in consumer finance. A common issue is poor documentation, unclear ownership records, and inconsistent reporting. That creates leverage in negotiation. If a collector wants payment, a written deletion request can be part of that discussion.

Real consumer forums show mixed outcomes. Some report success with smaller debt buyers. Others say large agencies refuse deletion and will only mark the account paid. That lines up with what we see. Smaller collectors and purchased debt portfolios often have more room to negotiate. Original creditors and large national agencies are less flexible.

From our experience in credit repair, the strongest pay for delete letters are short, clear, and conditional. No payment should be made until the agreement is confirmed in writing. Verbal promises do not protect the consumer. Written terms do.

This guide explains how pay for delete letters work, when they are worth trying, and how to write one that gives you the best chance of success.

At a Glance: Pay-for-Delete Letters

Most pay for delete agreements follow a clear path. This visual breaks down each step from negotiation to removal.

Last quarter alone, we negotiated 38 pay-for-delete agreements on behalf of clients. Twenty-six succeeded. Twelve were rejected. Every single rejection came from one of three sources: a major bank acting as the original creditor, a large national collection agency under contract restrictions, or an account where the client had already paid before contacting us. The sequence matters more than the letter itself.

What Is a Pay-for-Delete Letter?

A pay-for-delete letter is a written offer to pay a debt collector in exchange for removing the collection account from your Equifax, Experian, and TransUnion credit reports. Paying a collection without this agreement leaves the account on your report for 7 years as a "paid collection." Deletion removes it entirely. The difference to your credit score is significant.

Debt collectors purchase delinquent accounts from original creditors for 1 to 10 cents on the dollar. They then collect the full balance. Any payment above their purchase price is profit. A pay-for-delete offer gives them cash today in exchange for deleting the tradeline from your credit report instead of leaving it as a derogatory mark.

The FCRA requires creditors to report accurate information. This creates the core tension with pay-for-delete. If the debt is real and accurate, a collector who deletes it may violate their contract with the credit bureaus. This is why large national collectors often refuse. Smaller third-party collectors with more flexible bureau agreements are more willing to negotiate.

As Bankrate explains, pay-for-delete sits in a legal gray area: it is not illegal to request it, but no creditor is obligated to accept. Their practices vary widely. Some agencies accept routinely. Others have a strict no-deletion policy. Research the specific collector before investing time in a negotiation.

When Pay-for-Delete Works and When It Does Not

| Situation | Pay-for-Delete Likelihood | Reason |

|---|---|---|

| Small third-party collector, debt under $1,000 | Higher , 25-40% | Less bureau contract pressure, wants lump-sum cash, flexible |

| Midsize collection agency, debt $1,000-$5,000 | Moderate , 15-25% | Negotiable but stricter internal policies |

| Major national collector (Midland, Portfolio) | Low , under 10% | Strict bureau contracts, automated systems, policy prohibition |

| Original creditor (bank, credit card issuer) | Very low , under 5% | FCRA obligations, internal compliance, almost always refuses |

| Medical collection, debt under $500 | Not needed | Already excluded from bureau reports under 2022 voluntary policy |

| Debt within 2 years of 7-year expiration | Moderate | Aging account carries less value to collector, more willing to settle |

| Debt already past the statute of limitations | Avoid paying entirely | Payment restarts statute of limitations in most states |

Collector type matters more than your offer amount. A perfectly written letter sent to a major bank will almost always receive a rejection. The same letter sent to a smaller regional collection agency that purchased your account for pennies has a real chance of acceptance. Know who owns the debt before you decide on strategy.

Pay-for-delete trades payment for complete tradeline removal. It works best on smaller debts held by smaller third-party collectors. Most large national collectors and original creditors refuse. Medical collections under $500 do not need pay-for-delete because they no longer appear on reports under the 2022 bureau policy. Never pay a time-barred debt , the payment restarts the statute of limitations.

How to Write a Pay-for-Delete Letter

A pay-for-delete letter must include your name and address, the collector's name and address, the account number, a specific payment offer in dollars, and an explicit requirement that they remove the tradeline from all three bureaus before you pay. Send by certified mail. Get a signed written agreement on company letterhead before sending any money.

The letter does three things: identifies the account precisely, makes a concrete offer, and states clear conditions. Keep it short. Collectors review hundreds of letters. A one-page letter gets read. A three-page letter gets skimmed.

[Your Full Name]

[Your Address, City, State, ZIP]

[Date]

[Collection Agency Name]

[Collection Agency Address]

Re: Account Number [Account Number] / Original Creditor: [Original Creditor Name]

I am writing regarding the above-referenced account. I do not acknowledge that this debt is valid or that I owe the amount claimed. Without admitting to the alleged balance, I offer to resolve this account under the following terms:

I will pay [$Amount] as full and final settlement of this account. In exchange, [Collection Agency Name] will delete all references to this account from Equifax, Experian, and TransUnion within 30 days of payment receipt.

This offer is contingent on receiving a signed written agreement on company letterhead from an authorized representative confirming these terms before any payment. Payment will follow within 5 business days of receiving that agreement, via [cashier's check / money order / bank wire].

If I do not receive a written response within 15 days of the date of this letter, I will consider this offer declined.

Sincerely,

[Your Signature]

[Your Printed Name]

What to Put in the Offer Amount

Start at 40% to 50% of the claimed balance. Do not start at 100%. That eliminates your negotiating room. State a specific dollar amount, not a percentage. "I offer $180" is cleaner than "I offer 48% of the balance." Specific dollar amounts reduce ambiguity in any written agreement.

According to Upsolve's legally reviewed guide on pay-for-delete effectiveness, offers of 40% to 50% are common starting points in community discussions, with collectors often settling between 60% and 75% when deletion is part of the deal. Never go below 25% as an opening offer. Below that, many collectors will not engage at all.

The One Rule That Matters Most

Get the signed written agreement before you pay. This is the rule that separates successful negotiations from wasted money. Collectors can accept verbally and then "forget" after receiving payment. Your only protection is signed documentation on company letterhead with the name of the representative who approved it.

When you receive the written agreement, read it carefully. The agreement must specifically say the entire tradeline gets deleted from Equifax, Experian, and TransUnion, not just marked "paid" or "settled." If the language says "paid in full" without mentioning deletion, that is not a pay-for-delete agreement. That is a payment receipt.

A pay-for-delete letter must include the account number, a specific dollar offer, and a clear condition requiring deletion from all three bureaus before payment. Send by certified mail. Never pay without a signed written agreement on company letterhead. Start at 40% to 50% of the balance. Phone agreements are worthless and unenforceable.

What Happens After You Send the Letter

Most collectors respond within 7 to 21 days. Three outcomes are possible: written acceptance, written rejection, or no response.

A written acceptance means they agreed to your terms. Review the document before paying. Verify the deletion language covers all three bureaus explicitly. Then send payment through a traceable method: cashier's check, money order, or bank wire. Keep the receipt. After payment clears, monitor all three bureaus for 30 to 45 days to confirm the deletion posted.

A written rejection ends this round of negotiation. Do not pay. Evaluate whether to counter-offer at a higher percentage or shift strategy. If the debt contains any inaccuracy, switch to a dispute under the FCRA instead. Understanding your full range of debt collection defense options is critical at this point. A rejected pay-for-delete does not close all doors. Dispute rights under the FCRA remain open regardless of whether the collector agreed to deletion.

No response in 15 days is a rejection. Follow up once by certified mail restating the offer and deadline. After two ignored letters, consider moving directly to a dispute under the FCRA if the account contains any verifiable inaccuracy.

After Deletion: What Changes on Your Report

When a pay-for-delete succeeds, the collection tradeline disappears from the specific bureau where the collector reported it. If they reported to all three bureaus, all three must be deleted. The score impact appears in the next reporting cycle after deletion, typically within 30 to 45 days of the deletion posting.

One important note: the original creditor's charge-off entry may remain even after the collection tradeline is deleted. A charge-off and a collection are two separate entries. If the original creditor still reports a charge-off from before the account was sold, that entry stays on your report separately. Discuss this with the collector before finalizing any agreement. Understanding how both entries affect your overall credit risk profile determines which entry causes more damage and which one to prioritize.

When to Skip Pay-for-Delete and Dispute Instead

Skip pay-for-delete and file a dispute instead when the collection account contains any inaccuracy: wrong balance, wrong date, wrong account, or duplicate entry. Disputes under the FCRA are free. If the collector cannot verify the account within 30 days, the bureau removes it at no cost to you. Dispute first. Pay-for-delete is a fallback for accurate, verified accounts.

Disputes produce deletions at zero cost when they succeed. Pay-for-delete costs you money and still may not produce deletion. The logical sequence is: dispute first, pay-for-delete second.

File a dispute whenever you see these specific conditions on any collection account:

- Wrong original delinquency date (controls when the 7-year clock expires)

- Balance amount that does not match any creditor statement you received

- Account number you do not recognize

- Duplicate entries for the same debt under two different collection agencies

- A charge-off and a collection both showing balances (only one can carry an open balance)

- Any account from a medical provider for an amount that differs from your Explanation of Benefits

Collection agencies like Revco Solutions and RMS routinely receive accounts with data errors from the transfer process. Last quarter, we found disputable inaccuracies in 38% of the collection accounts we reviewed at ASAP Credit Repair. Every one of those accounts was a dispute candidate before pay-for-delete was ever needed.

NerdWallet's consumer credit guidance reinforces this sequence: pay-for-delete is a last resort, not a first step. Accuracy disputes under the FCRA remain the faster and free path when any error exists in the account data.

Does pay-for-delete hurt your credit score?

No. A pay-for-delete agreement does not hurt your credit score. If the collector deletes the tradeline, the derogatory mark disappears and your score improves. If the collector rejects the offer and you do not pay, your score stays the same. You have nothing to lose by sending the letter. The risk only appears if you pay without getting a written deletion agreement first , in that case, you spent money and the collection stays on your report as a paid collection with minimal score benefit.

Can a collector re-report a deleted account?

Technically yes, but it is rare when a written deletion agreement exists. If a collector deletes the account and then re-reports it, they violate the FCRA, which requires accurate reporting, and potentially the written agreement you hold. Document the deletion by pulling your credit report within 30 days of the deletion posting. If the account reappears, file a dispute with the bureau citing the deletion date and reference the written agreement. A consumer attorney can pursue damages for wrongful re-reporting under the FCRA.

What if a collector agrees verbally but refuses to put it in writing?

Walk away. A verbal agreement with a debt collector is unenforceable. The collector knows this. If they agree verbally but refuse written confirmation, they have no intention of deleting the account. This is a common tactic to collect payment without delivering deletion. Decline the verbal offer. Send a written letter instead stating you require signed written confirmation on company letterhead before any payment. If they still refuse written confirmation, move to a dispute under the FCRA rather than a negotiated payment.

38% of the Collections We Review Contain Errors That Qualify for Free Dispute First

Before you offer to pay anything, find out if the collection account contains an inaccuracy that makes pay-for-delete unnecessary. A free 3-bureau audit shows exactly what Equifax, Experian, and TransUnion report and identifies every disputable error across your full file.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

720 Credit Score: Is It Good Enough or Are You Leaving Money on the Table? A successful pay-for-delete agreement removes a collection entry and can move a score 40 to 100 points. Whether that improvement pushes you into the 720-plus tier determines how much money you save on a mortgage, auto loan, or credit card APR. This covers exactly what a 720 score gets you versus 740 or 760, where the real interest-rate savings appear, and which loan tiers change at each score band.

-

What Is a Fair Credit Score and Why It Is Costing You More Than You Think Most people with collection accounts land in the "fair" credit tier (580-669) because of those derogatory marks. A successful pay-for-delete agreement often moves a borrower out of the fair tier entirely. This covers exactly how much more fair-credit borrowers pay in interest versus good-credit borrowers across mortgages, auto loans, and credit cards, and what the actual dollar cost of staying in that tier looks like over time.

-

600 Credit Score: What It Really Means A 600 score often traces back to one or two collection accounts. Removing those through pay-for-delete or dispute can produce a 40-80 point improvement that completely changes the loan products available to you. This covers what a 600 score actually signals to lenders, what rates you receive at 600 versus 640 or 660, and which specific actions produce the fastest score movement from the 600 starting point.

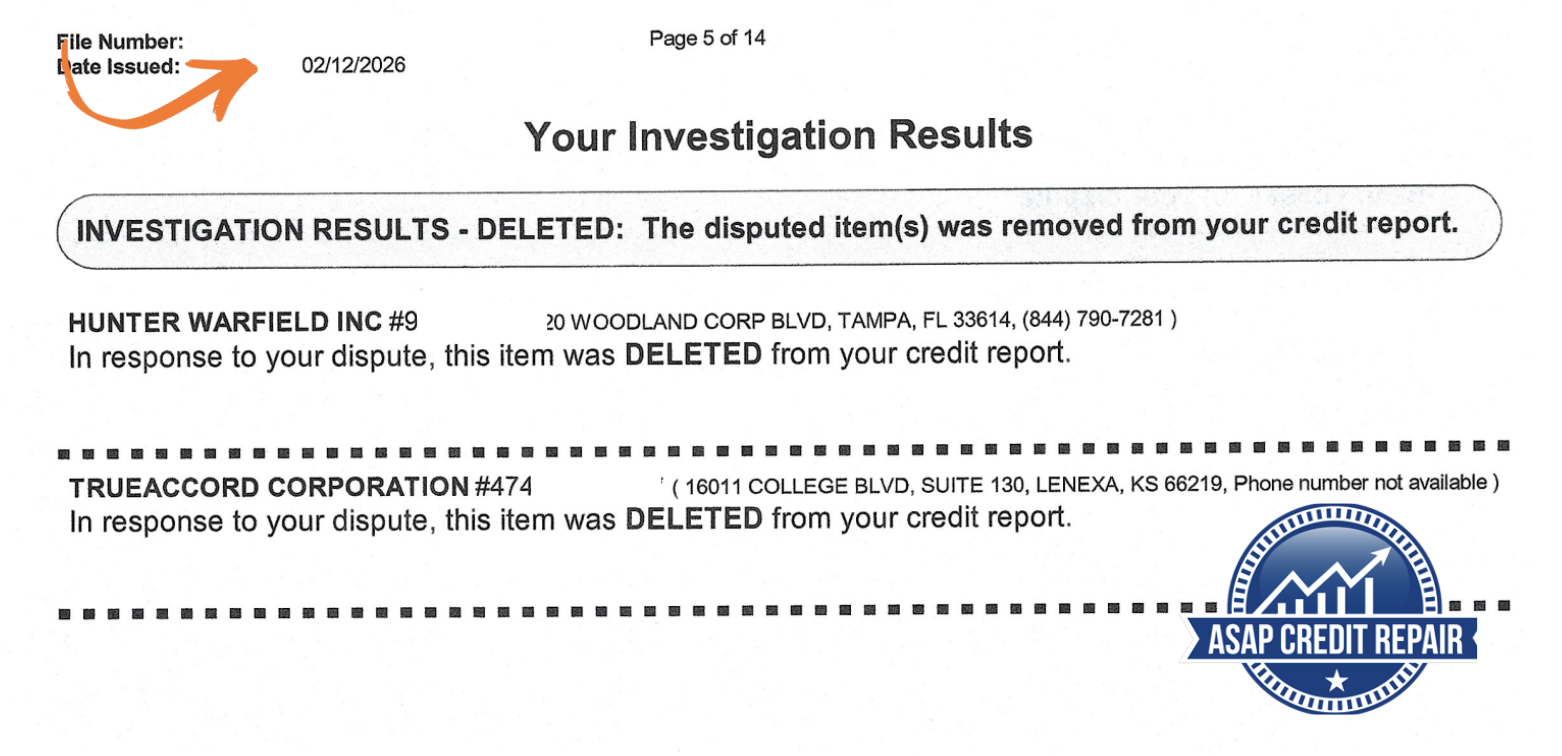

Real Pay-for-delete Letter Removal In Action

The strategy discussed above is not only theory. It is based on real files we work on.

Here is an example of collection removal results from an actual client case.

What This Result Shows

The disputed accounts were verified for deletion and removed

Collection tradelines no longer appeared as active negative marks

The credit file became stronger for future underwriting review

Proper dispute work can remove accounts when reporting cannot be maintained accurately

Educational example only. Personal details removed. Results vary based on reporting history and account conditions.