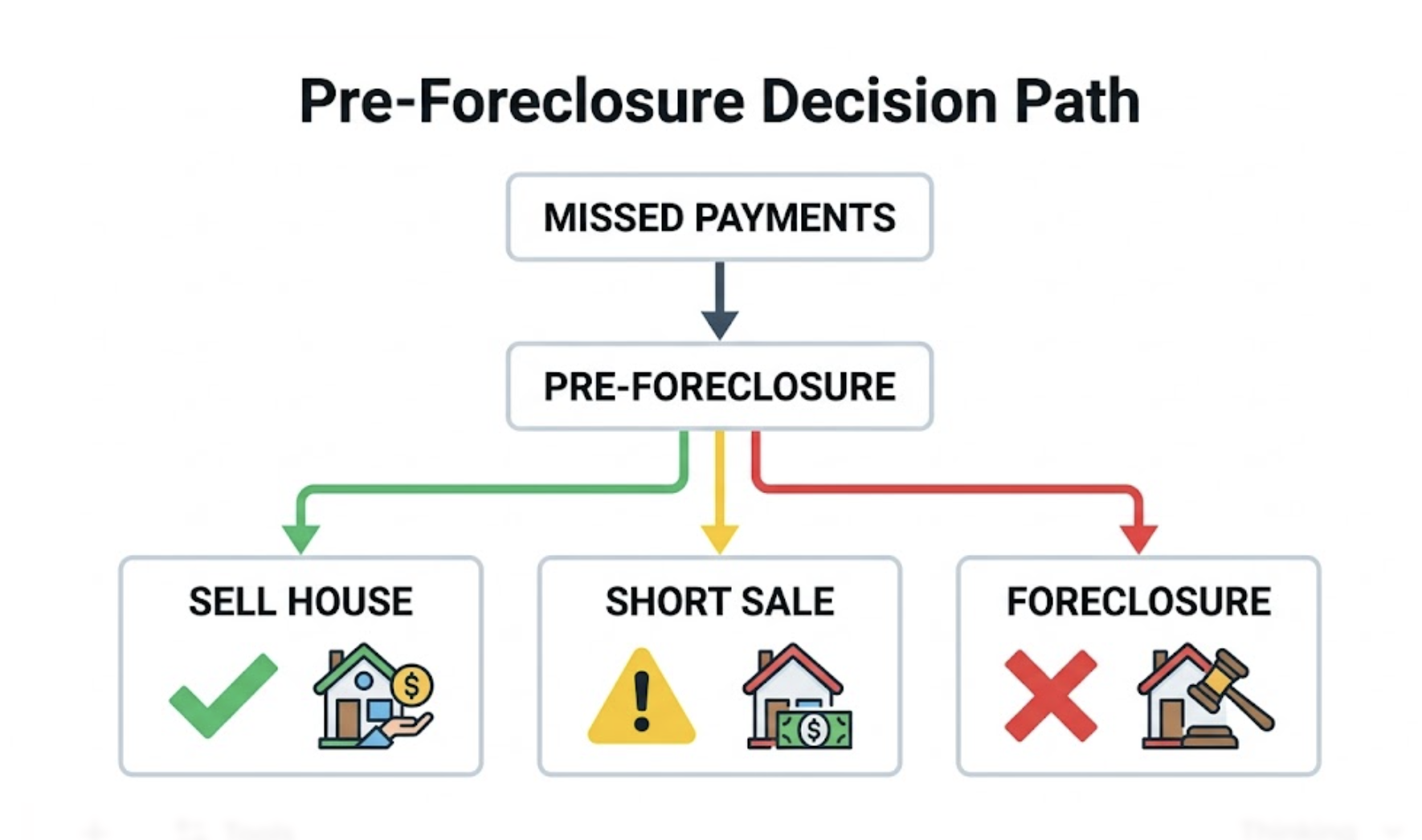

Pre-foreclosure is the stage where a homeowner has missed mortgage payments, but the lender has not yet completed the foreclosure process. During this period, the property can still be sold.

Mortgage delinquency data from the Mortgage Bankers Association shows that a large portion of loans enter early-stage delinquency before foreclosure is finalized, which creates a window where homeowners retain control of the property. In this stage, selling the home is one of the primary ways to resolve the debt, either by paying off the loan balance or through a lender-approved short sale.

In actual cases, homeowners who act during pre-foreclosure have more options compared to those who wait until foreclosure proceedings advance. The ability to sell depends on equity, loan balance, and lender approval, but the opportunity exists before legal repossession is completed.

Let's discuss…

Pre-Foreclosure · Sell House Before Foreclosure · Foreclosure Timeline · Short Sale · Home Equity · Credit Impact

Updated April 2026 · Sources: ATTOM Year-End 2025 Foreclosure Market Report, Nolo foreclosure selling guide, Consumer Financial Protection Bureau 120-day rule (12 CFR 1024.41), Marketplace.org foreclosure data, HomeLight pre-foreclosure analysis

Pre-foreclosure gets misunderstood. Many homeowners assume that once a lender sends a Notice of Default, the house is already gone. It is not. The notice is the start of a legal process that takes months, sometimes over a year, to complete. That time is yours to use.

Can You Sell Your House While in Pre-Foreclosure?

Federal law requires lenders to wait at least 120 days after your first missed payment before they can start foreclosure, under 12 CFR 1024.41, the CFPB's mortgage servicing rule. That is roughly four months before a lender can even file the first foreclosure document. After that, judicial foreclosure states (where a court must approve the sale) add months more. ATTOM's 2025 data shows the national average time from first filing to completed foreclosure auction was 592 days. That is a lot of time to sell.

The question is not whether you can sell. The question is how much time you have left, and whether your home's current market value covers what you owe.

Why Don't Pre-Foreclosure Homeowners Sell If They Have Equity?

This is the question the Reddit r/RealEstate community returns to often. The thread titled "Why don't pre-foreclosure people sell the property, especially if there is equity?" produced over 100 comments. The answers from that discussion are consistent with what housing counselors and attorneys report.

The financial reality is this: in 2024, U.S. homeowner equity totaled approximately $30 trillion, according to Marketplace.org's reporting on the mortgage market. Most homeowners in pre-foreclosure today bought before 2022 and have meaningful equity. The homes have not lost value. What happens is that homeowners wait too long, the auction is scheduled, and the sale becomes a foreclosure rather than a voluntary transaction.

The Quora user's confusion is common and understandable. The legal process creates documents with intimidating names - Notice of Default, Lis Pendens, Notice of Sale - that sound like loss of ownership. They are not. They are notifications of a process that has started, not one that has finished. Until the gavel comes down at the foreclosure auction, you own the house.

Is It Better to Sell Your House Before Foreclosure Starts?

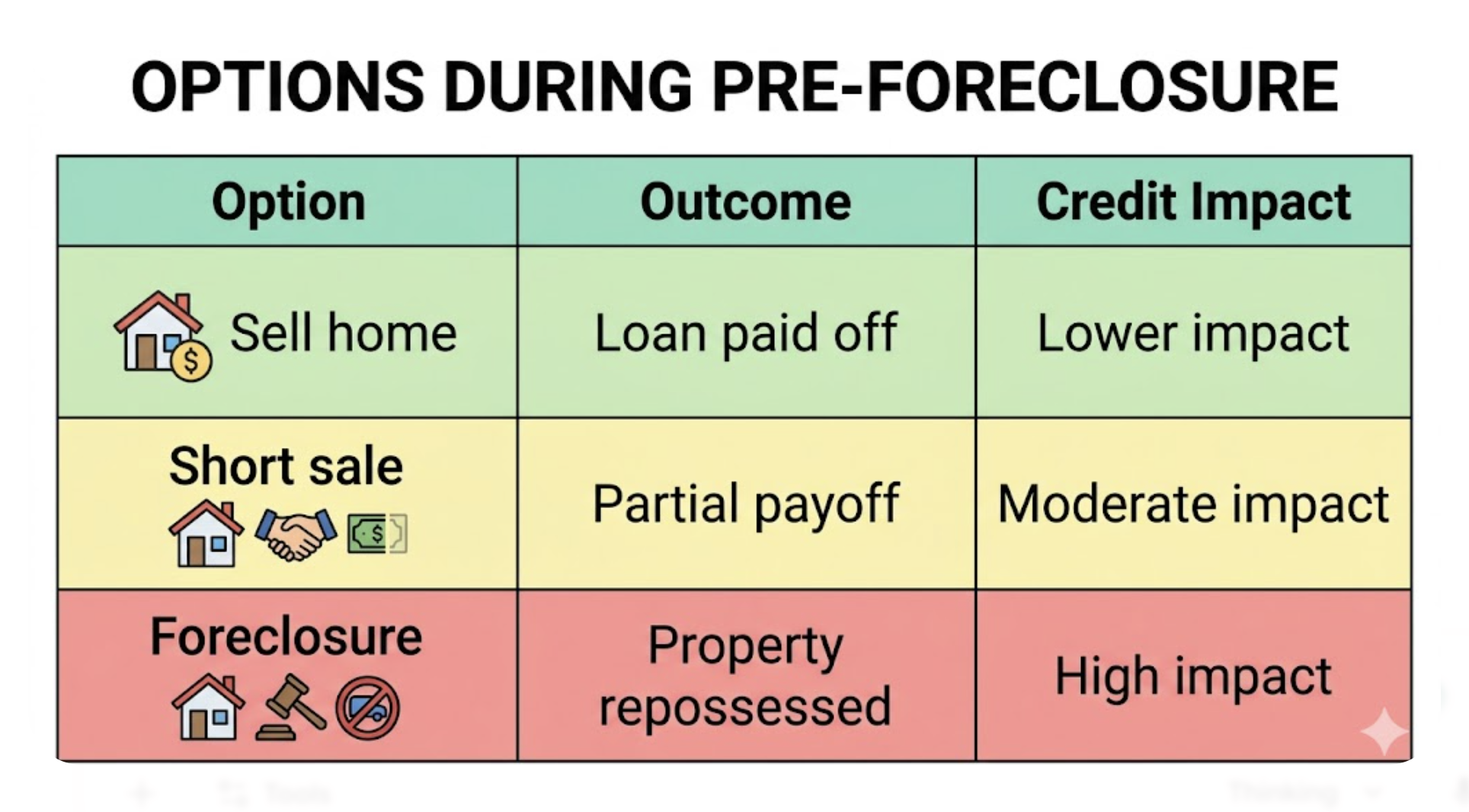

The credit damage follows the same logic. According to data published by Nolo's foreclosure selling guide, a completed foreclosure typically drops a credit score by 100 to 160 points and stays on your credit report for seven years. A short sale, where the home sells for less than the mortgage balance and the lender forgives the rest, results in a drop of 85 to 130 points. A traditional pre-foreclosure sale where the sale price covers the full mortgage leaves your credit largely intact once payments resume, since the loan is paid in full at closing.

The chart shows what housing counselors tell clients: the earlier the resolution, the less the credit damage. The difference between a traditional pre-foreclosure sale and a completed foreclosure is roughly 140 points. That gap determines whether you qualify for a new mortgage in two years or seven years. For someone who plans to buy again, that difference is the most practical reason to act in pre-foreclosure rather than waiting.

There is also the question of how you will handle the mortgage while preparing to sell. If you are already behind on payments and unsure what options exist besides selling, the breakdown of what to do when you cannot pay your mortgage covers forbearance, loan modification, and deferral programs that can buy you time while you prepare a sale, without triggering the full foreclosure clock.

What Happens to Your Equity If You Sell During Pre-Foreclosure?

One Quora response to "What is the best time to sell a house, before or after going into foreclosure?" framed the equity question clearly: "If you have equity, waiting for the bank to auction the house is the most expensive decision you can make. They are not selling it for you. They are selling it to recover their loan. Any surplus above what you owe goes through a legal process that not every former homeowner navigates successfully."

The math is straightforward. Assume your home is worth $320,000. Your mortgage balance is $240,000. You are six months behind with $15,000 in late fees and legal costs added. Your payoff is $255,000. A pre-foreclosure sale at $315,000 (5 percent below list for speed) nets you approximately $60,000 after the payoff and standard closing costs. A foreclosure auction may sell the home for $240,000 to a cash investor, pay the bank, and leave you with zero and a foreclosure on your credit for seven years.

The calculation is rarely that simple in practice - there may be a second mortgage, HOA liens, or other encumbrances - but the principle holds. Equity earned through years of mortgage payments does not disappear in pre-foreclosure. It disappears at the auction if you let the clock run.

How to Sell Your House During Pre-Foreclosure

- Get your exact payoff amount from your lender. Call the loss mitigation department and request a 30-day payoff statement. This includes the principal balance, accrued interest, late fees, and any attorney fees already charged. This number changes daily as interest accrues. Know it before you price the home.

- Get a current market value estimate from a real estate agent. A Comparative Market Analysis from an agent will show what comparable homes have sold for in the last 90 days. Compare this to your payoff. If the market value exceeds the payoff, a traditional sale with equity is possible. If it does not, a short sale requires lender approval before the house can close below what is owed.

- Notify your lender that you intend to sell. Call your servicer's loss mitigation department and tell them you are listing the property. In many cases, lenders delay foreclosure proceedings when they know a legitimate sale is underway. They prefer a clean payoff over the cost of completing a foreclosure. Get the contact name and confirm in writing.

- List with an agent experienced in distressed or pre-foreclosure sales. Timeline is everything. You need an agent who understands how to attract cash buyers and buyers with pre-approval, close in 21 to 30 days when necessary, and communicate with the lender if any delays arise. A standard residential agent who normally works 45-day closes may not have the right tools for this situation.

- Price for speed, not for maximum return. A price 3 to 5 percent below comparable homes will generate offers fast. Every week the home sits on the market while the foreclosure clock runs is a week closer to the auction. A home that sells at a small discount in 14 days is better than one priced at full market value that sits for 60 days.

- Confirm all liens are cleared at closing. The title company will run a full title search. Every outstanding lien - first mortgage, second mortgage, HOA arrears, judgment liens - must be paid or negotiated before the title transfers cleanly to the buyer. Do not assume your first mortgage is the only claim on the property.

If your lender has already moved to a law firm for collections or foreclosure proceedings, the firm handling your case now has authority to negotiate. Our breakdown of how to stop foreclosure without paying the full balance covers the legal options available after a law firm takes over the file, including short sale approval timelines, deed in lieu negotiations, and how to get a foreclosure suspended while a sale is pending.

What Are Your Options If the Sale Price Won't Cover the Mortgage?

Short sales are not guaranteed. The lender has to agree to the discount. They typically do when they calculate that the short sale proceeds plus the reduced legal costs outperform what they would net from a foreclosure auction. Lenders rarely want to own houses. The foreclosure process costs them legal fees, property maintenance during the REO period, and eventual auction costs. A negotiated short sale at 85 cents on the dollar is often better for them than the full foreclosure process, which is why approval rates for well-documented short sale applications are reasonably high.

The credit impact of a short sale is significant, roughly 85 to 130 points and reported as "settled for less than the full amount" on your credit report. But the timeline for recovery is shorter than a foreclosure. Conventional mortgage programs typically require a two-year waiting period after a short sale before you can qualify again, compared to seven years for a completed foreclosure.

If your property is secured through a credit union rather than a traditional bank, the loss mitigation process may look different. Credit unions have more flexibility on some modification and short sale structures. Our overview of whether credit unions can take your house in foreclosure explains the distinctions between credit union foreclosure procedures and those of conventional mortgage servicers, including the differences in timelines and negotiation approaches.

The ATTOM 2025 year-end foreclosure report confirms that most homeowners in pre-foreclosure today are not underwater. Homeowner equity has remained at historically high levels, meaning most pre-foreclosure situations are ones where the homeowner has options. As ATTOM's CEO noted in the 2025 report: "Strong equity positions and more disciplined lending are continuing to limit risk." The equity is there. The question is whether the homeowner acts while they still have time to use it.

Selling in Pre-Foreclosure Protects More Than Just Your Home

A completed foreclosure drops your credit score 100-160 points and stays on your report for 7 years. A traditional pre-foreclosure sale, where the mortgage is paid in full, leaves your credit largely intact. A free 3-bureau audit shows you where your credit stands today and what a foreclosure would cost you in future borrowing power.

Get My Free Credit Audit → Secure · 2 minutes · No credit card requiredFrequently Asked Questions

Can you sell your house while in pre-foreclosure?

Yes. You retain legal ownership of your home throughout pre-foreclosure. You can list, negotiate, and close a sale any time before the foreclosure auction. The sale proceeds pay off the mortgage and any other liens at closing. Any amount above your total debt goes to you. Selling during pre-foreclosure is one of the most effective ways to avoid the full credit impact of a completed foreclosure.

Is it better to sell your house before foreclosure starts?

Yes. Selling before or early in the foreclosure process gives you the most time to prepare the home, price it at or near market value, and close on your schedule. Waiting until after an auction date is set leaves you with weeks to close rather than months. Earlier action also means less credit damage, since a traditional sale paid in full at closing does not result in a derogatory mark on your credit report.

Why don't pre-foreclosure homeowners sell if they have equity?

The most common reasons are emotional attachment to the home, denial that the situation is serious, and the belief that pre-foreclosure means selling is no longer an option. Many homeowners wait for a loan modification or reinstatement that does not come, losing the window for a market-price sale. By the time the auction is scheduled, the only option left is a fast cash sale at a discount or the auction itself.

What is the best time to sell a house, before or after going into foreclosure?

Before, and as early in the process as possible. Once a foreclosure auction is scheduled, you lose control of pricing, timing, and who buys the home. Selling before the Notice of Default is filed gives you the most flexibility. Selling after the Notice of Default but before the Notice of Sale is still viable. Selling after the Notice of Sale is possible but requires a fast close, typically 21 to 30 days. After the auction, it is too late.

How long do you have to sell a house in pre-foreclosure?

It depends on your state and the type of foreclosure. Federal law requires lenders to wait 120 days after the first missed payment before filing. After filing, judicial foreclosure states typically take 8 to 12 months to reach an auction. Non-judicial states can move much faster, sometimes 90 to 120 days from Notice of Default to auction. ATTOM's 2025 data shows the national average time to complete a foreclosure was 592 days from first filing, though this varies significantly by state and lender.

What happens to your equity if you sell during pre-foreclosure?

You keep it. The title company pays all outstanding liens - mortgage balance, late fees, attorney fees, any other claims - from the sale proceeds at closing. Whatever remains after those payoffs goes to you. If your home sells for $340,000 and your total payoff is $270,000, you receive approximately $70,000 after standard closing costs. Waiting for the foreclosure auction eliminates this outcome, since the bank's goal is to recover its loan, not to maximize your net proceeds.

-

Bank Account Frozen But I Never Got Served: Is That Legal? If a creditor has frozen your bank account alongside a foreclosure judgment, this explains the legal process, your rights to challenge a default judgment, and the specific steps to protect exempt funds within the 10-day window.

-

What Is Credit Gardening? How to Grow Your Score the Smart Way After resolving a pre-foreclosure situation, credit gardening is the structured approach for rebuilding your score over 12 to 24 months, targeting the milestones needed to qualify for a new mortgage.

-

Can a Company Send You to Collections Without Notice? If HOA fees, second mortgage arrears, or other debts connected to your home have gone to collections, this covers your rights under the FDCPA, the validation notice requirement, and how to respond to collection accounts before they become judgment liens on the property.

Choosing the Right Path: Impact on Credit and Future Borrowing

Deciding between a traditional sale, a short sale, or allowing a foreclosure to proceed is essentially an exercise in damage control. While all three options signal a major life transition, their impact on your credit score and your "public record" status varies significantly.

Key Factors to Consider:

Equity vs. Debt: Do you have enough home value to pay the bank in full, or do you need to negotiate a "short" payoff?

Credit Recovery: A foreclosure is often considered the "nuclear option" for a credit report, while a proactive sale or even a negotiated short sale can often be framed more favorably to future lenders.

Deficiency Judgments: Depending on your state, some paths protect you from the bank coming after you for the remaining balance, while others leave you vulnerable.

To help you visualize how these three paths differ in terms of both the immediate outcome and the long-term credit consequences, refer to the comparison breakdown below.

Closing🔚

A house can be sold during pre-foreclosure because ownership remains with the borrower until foreclosure is completed. Acting during this stage allows the debt to be resolved, reduces financial loss, and prevents the full impact of foreclosure on the credit profile.