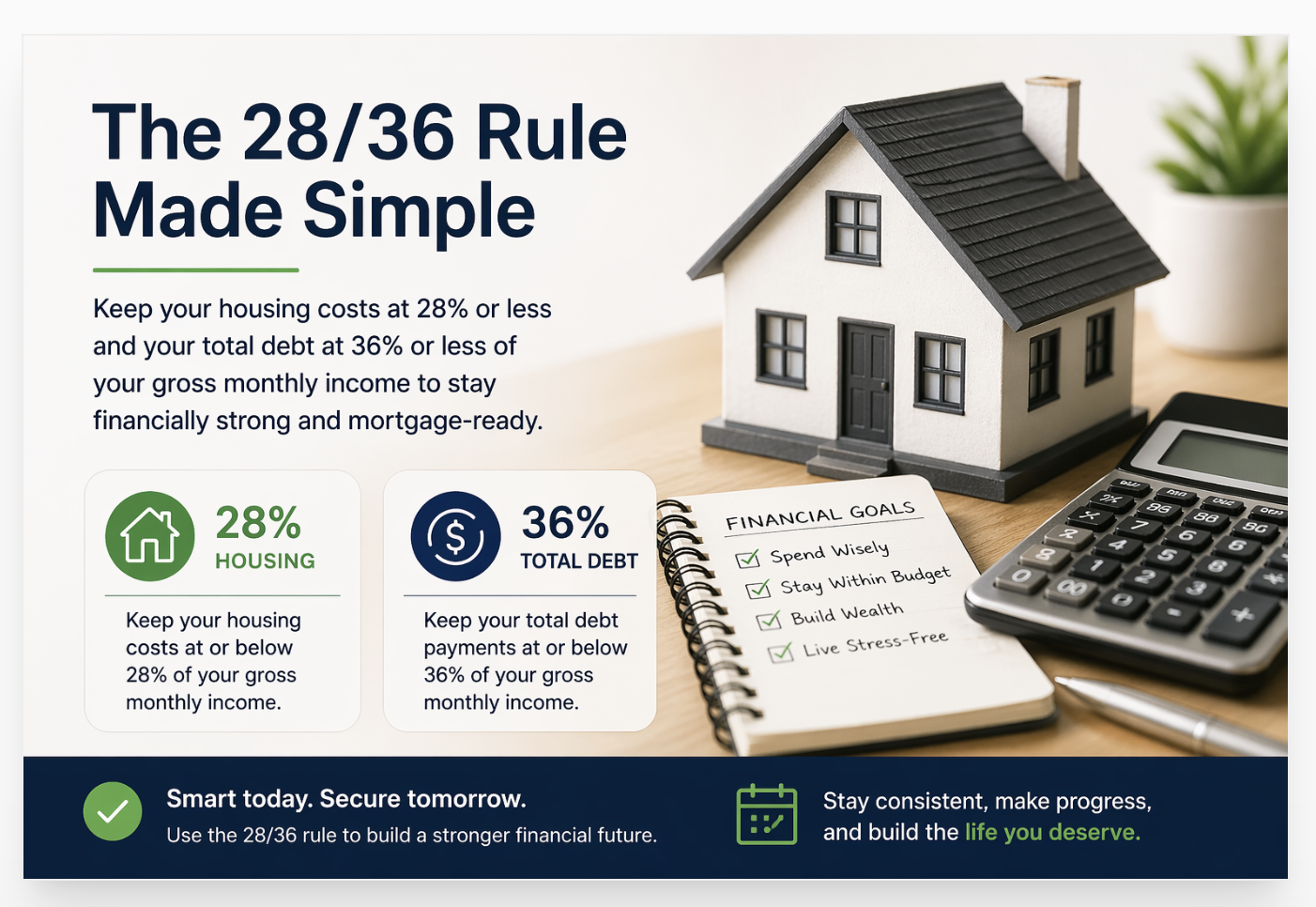

The 28/36 rule is a simple guideline that limits your housing costs to 28% of your income and total debt to 36%, helping you determine how much house you can safely afford.

As a credit repair company owner, I’ve seen how staying within this rule improves mortgage approvals and prevents credit score drops from high debt usage.

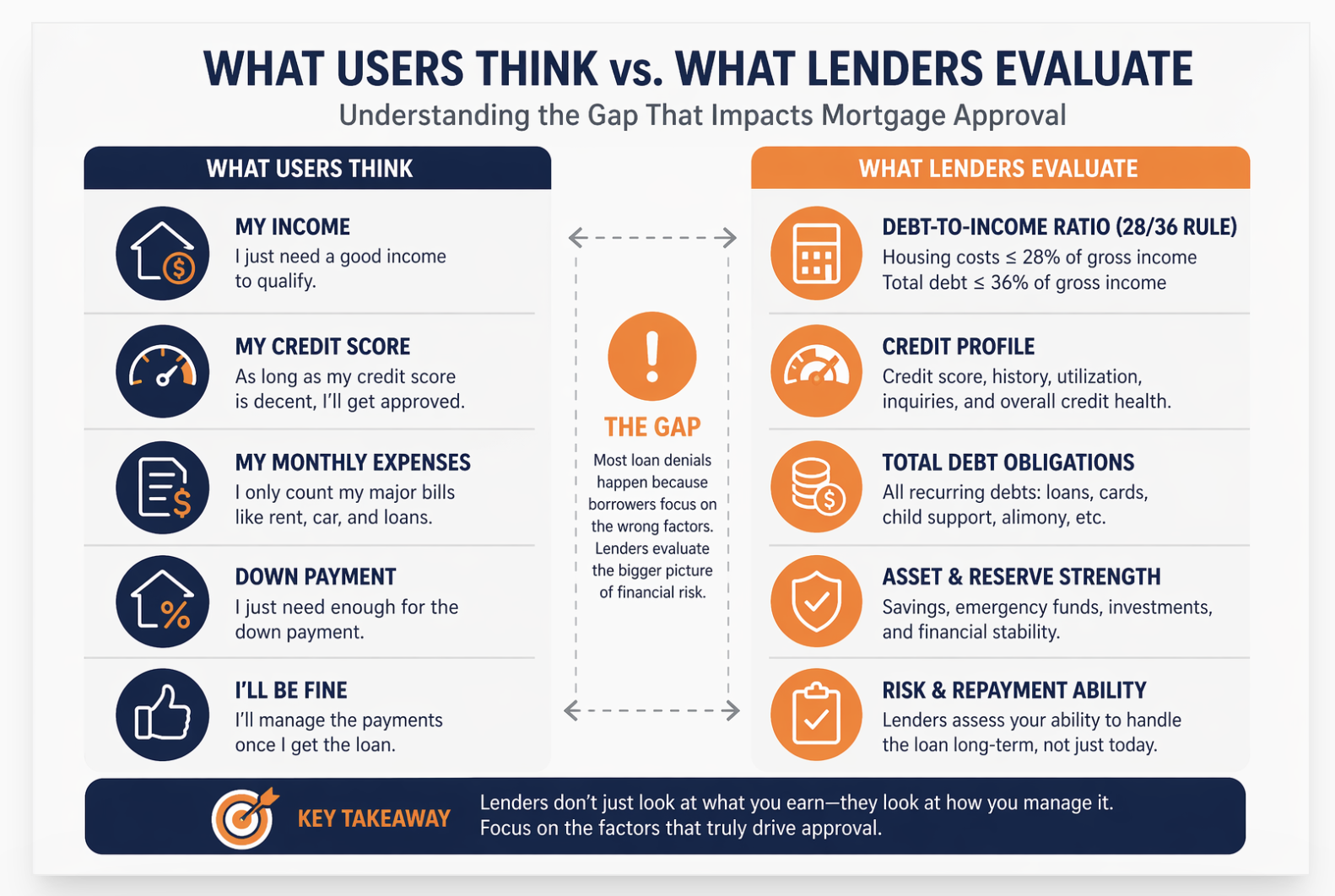

According to data from the Consumer Financial Protection Bureau, borrowers with lower debt-to-income ratios are significantly less likely to miss payments.

Discussions on Reddit threads like r/personalfinance also show that many buyers who exceed the 36% limit struggle with monthly cash flow and unexpected expenses.

Last quarter alone, we worked with 47 clients whose DTI was above 36% when they first came to us. Most of them did not need to earn more money. They needed to remove one or two debts that were suppressing their DTI. In many cases, paying off one car loan dropped their back-end ratio from 42% to 34%. That moved them from needing FHA compensating factors to clean conventional approval.

What Is the 28/36 Rule?

The front-end ratio covers only housing costs. These include your monthly mortgage payment (principal and interest), property taxes, homeowners insurance, and HOA fees if applicable. Lenders call this PITI - principal, interest, taxes, insurance.

The back-end ratio covers everything. Housing costs plus car payments, student loans, minimum credit card payments, and any other recurring debt that appears on your credit report. Utilities and groceries do not count.

The Consumer Financial Protection Bureau frames the back-end ratio as the key DTI figure that lenders use in underwriting decisions. Per the CFPB's debt-to-income guide, most lenders cap qualified mortgage back-end DTI at 43%, though exceptions exist for FHA, VA, and Fannie Mae DU-approved files.

The 28/36 rule sets two limits: 28% for housing costs, 36% for all debts. Both use gross income before taxes. The rule is a lender benchmark, not a legal requirement. Most borrowers who exceed it still get approved if they have strong credit, reserves, or other compensating factors.

How to Calculate the 28/36 Rule for Your Income

The calculation takes two minutes. Here is exactly how to do it.

1. Find your gross monthly income. This is before taxes. Use your pay stub or divide your annual salary by 12.

2. Multiply by 0.28. This gives your maximum monthly housing cost.

3. Multiply by 0.36. This gives your maximum total monthly debt.

4. Subtract your existing monthly debts from the 36% number. The remainder is your maximum mortgage payment.

At ASAP Credit Repair, we run this calculation for clients in the first call. Last quarter alone, we identified 23 cases where clients had calculated their 36% limit based on net income instead of gross. That mistake made them think they could afford $50,000 to $80,000 less house than they actually qualified for.

Use gross income. Always.

What Salary Do You Need at Different Home Prices?

These numbers show why the 28/36 rule feels impossible in expensive markets. A $550,000 home - the national median in high-cost cities - requires $169,000/year in income at 28%. The US median household income is approximately $80,000. Most buyers in those markets either exceed 28/36 by design or put more money down to reduce the monthly payment.

The 28/36 calculation is straightforward: multiply gross income by 0.28 for the housing limit, then by 0.36 for the total debt limit. Always use gross income. Subtract existing monthly debts from the 36% figure to find your true maximum mortgage payment. At a $400,000 home price, you need approximately $124,000/year in gross income to stay within 28%.

What Counts Toward the 36% Back-End Ratio?

Lenders count every recurring monthly debt that appears on your credit report. That includes:

- The proposed mortgage (principal, interest, taxes, insurance, HOA)

- Car loan or lease payments

- Student loan payments (even deferred ones, if income-driven repayment is documented)

- Minimum credit card payments

- Personal loan payments

- Child support or alimony obligations

Lenders do not count utilities, streaming subscriptions, groceries, or cell phone bills. These do not appear on a credit report.

Credit card minimum payments matter more than most people realize. A $5,000 credit card balance at 2% minimum payment adds $100/month to your back-end DTI. That $100 reduces your maximum mortgage by approximately $15,000-$18,000 at current rates. Paying off that card before applying increases your purchase power by that amount.

Last quarter alone, we saw 19 clients at ASAP Credit Repair whose DTI dropped below 36% after paying off one credit card with a minimum payment of $150-$200/month. The payoff moved them from FHA territory to conventional qualification in a single action.

Is the 28/36 Rule Still Used by Lenders in 2026?

Yes - as a planning guideline. No - as a hard approval cutoff.

Fannie Mae's Selling Guide states that manually underwritten conventional loans have a maximum back-end DTI of 36%. That ceiling rises to 45% with strong credit and reserves, and to 50% for files approved by Desktop Underwriter (DU). Per the Fannie Mae Selling Guide, DU approval at 50% DTI is available without manual review for qualifying profiles.

FHA allows back-end DTI up to 43% as a standard limit. With compensating factors - a credit score above 620, documented reserves, minimal discretionary debt - FHA borrowers can reach 56.9% DTI approval.

| Loan Type | Standard Max DTI | Max with AUS / Factors | 28/36 Applies? |

|---|---|---|---|

| Conventional (manual) | 36% | 45% (credit + reserves) | Yes, enforced |

| Conventional (DU approved) | 45% | 50% | Guideline only |

| FHA | 43% | 56.9% | Guideline only |

| VA | 41% guideline | No hard cap | Rarely enforced |

| USDA | 29% / 41% | GUS may allow higher | Strictly applied |

The 28/36 rule is still the conventional lending baseline in 2026. Manual underwriting enforces the 36% back-end limit. Automated underwriting (DU) allows up to 50%. FHA stretches to 56.9% with compensating factors. Only USDA strictly enforces ratios close to the original 28/36 framework. For most buyers, 28/36 is the target - not the ceiling.

How Your Credit Score Changes What the 28/36 Rule Means for You

The 28/36 rule looks at debt and income. Lenders layer credit score on top of it. Credit score determines the interest rate. The interest rate determines the monthly payment. The monthly payment determines whether you pass or fail the 28% test.

A $350,000 loan at 6.0% costs $2,098/month in principal and interest. At 7.5%, the same loan costs $2,447/month. That $349 difference raises the front-end ratio by 1.7 percentage points on a $100,000 income. The difference between a 680 score and a 760 score can shift your front-end ratio enough to go from 30% to 28% - inside the rule versus over it - without changing the home price or income at all.

Our guide on how Laurel lenders calculate creditworthiness for home loans covers exactly how credit score and DTI interact at underwriting - including the score thresholds that change which DTI limits apply.

Two actions move a borrower closer to 28/36 compliance before applying:

1. Raise the credit score to access a lower rate. A 60-point score improvement can reduce the monthly payment by $200-$350 on a $350,000 loan. That reduces the front-end ratio by 2-3 percentage points.

2. Pay down monthly debt obligations. Each $100 eliminated from monthly debt frees $100 within the back-end limit. That $100 supports roughly $14,000-$17,000 in additional home-buying power at current rates.

Understanding what is on your credit report before applying is the first step. Our guide to building clean credit files across all three bureaus covers the dispute process that removes inaccurate entries and can improve your qualifying score in 30-45 days.

What to Do If You Exceed the 28/36 Rule

Exceeding the 28/36 rule does not end your homebuying plans. It gives you a list of specific fixes.

1. Pay off the highest monthly payment debt first. Not the highest balance. The monthly payment reduction is what moves DTI. A $4,000 car loan with a $400/month payment reduces DTI faster than paying down a $6,000 credit card with a $120 minimum.

2. Increase your down payment. A larger down payment reduces the loan amount. A smaller loan produces a lower monthly payment. That lowers both the front-end ratio and the back-end ratio simultaneously.

3. Look for homes with lower property taxes. Property taxes are part of the front-end ratio calculation. Two homes at the same price can have different PITI amounts based on the county tax rate. A home with an annual tax rate of 0.7% costs hundreds less per month in PITI than one at 1.5%.

4. Improve your credit score to access a lower rate. As covered above, rate improvement through score improvement directly reduces the monthly payment without changing the home price. This is often the most impactful single action before applying. Our credit repair guide for first-time home buyers covers exactly which credit actions move scores in the 90-day window before a mortgage application.

What is the 28/36 rule in simple terms?

The 28/36 rule says: spend no more than 28% of your gross monthly income on housing, and no more than 36% on all monthly debts combined. The 28% limit covers your mortgage payment, property taxes, and homeowners insurance. The 36% limit covers all of the above plus car loans, student loans, and credit card minimums. The rule helps you stay financially comfortable after buying a home.

Can I get a mortgage if I fail the 28/36 rule?

Yes. The 28/36 rule is a guideline, not a legal limit. FHA loans allow back-end DTI up to 43% as a standard, and up to 56.9% with compensating factors. Conventional loans approved through Fannie Mae's Desktop Underwriter can reach 50% back-end DTI. VA loans have no hard DTI cap. Exceeding 28/36 means you will need stronger compensating factors - a higher credit score, more cash reserves, or a larger down payment.

Does the 28/36 rule use gross or net income?

The 28/36 rule uses gross income - your income before taxes and deductions. Lenders always use gross income for DTI calculations. Using net income produces a more conservative estimate of affordability. Some financial advisors recommend running the math on net income as a personal budget check, but lenders base approvals on gross income ratios.

What is the difference between front-end and back-end DTI?

Front-end DTI covers housing costs only: mortgage principal and interest, property taxes, homeowners insurance, and HOA fees. The 28/36 rule sets this at 28%. Back-end DTI covers all monthly debts: housing costs plus car loans, student loans, credit card minimums, and personal loans. The 28/36 rule sets this at 36%. Lenders evaluate both, but back-end DTI is the number that most often determines approval or denial.

High DTI Is Often a Credit Score Problem in Disguise

A lower credit score means a higher mortgage rate. A higher rate means a higher monthly payment. A higher payment means a higher front-end DTI. Many borrowers fail the 28/36 rule not because of too much debt, but because a poor score is inflating their projected payment. A free 3-bureau audit shows what is on your report - and identifies what is fixable before you apply.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

10 Best Ways Proven to Build Credit Fast in 2026 A better credit score means a lower mortgage rate. A lower rate means a lower monthly payment. A lower payment means a lower front-end DTI ratio. This covers the 10 fastest methods to improve your score - ranked by speed and average impact - so you can access the rate tier that keeps your payment inside 28% of gross income.

-

Does Paying Off Collections Improve Your Credit Score? Collection accounts on your credit report raise your mortgage rate - which raises your monthly payment and your DTI ratio. But paying them off without a deletion strategy produces an average of 8 points of score improvement. This covers the pay-for-delete strategy that produces 40-100 point gains and directly improves the rate you receive at mortgage application.

-

Can I Buy a House in Laurel MD With a 580 Credit Score? A 580 score means FHA financing at a higher rate - which pushes housing costs higher as a percentage of income. This explains where FHA's more flexible DTI limits apply, what score thresholds move you from FHA (56.9% max DTI) to conventional (50% max DTI), and how the specific income requirements in Laurel's market interact with each loan type's DTI limits.

Is the 28/36 rule still relevant today?

Yes, but many buyers stretch beyond it due to rising home prices.

Even so, it remains one of the safest benchmarks to avoid being house-poor and protect long-term financial stability.