CreditFresh can look like a lifeline when traditional lenders say no. However, fast money often comes with expensive math hidden in the fine print. For borrowers with poor credit, limited credit history, or urgent cash needs, CreditFresh offers something banks often do not: quick approval, same-day funding in many cases, and access to a revolving line of credit without a stated minimum credit score requirement. On the surface, that flexibility sounds helpful.

The real question is not whether CreditFresh is legitimate, because it is.

The question is what borrowing from CreditFresh actually costs over time, how its billing cycle charges compare to traditional APR loans, and whether using it helps or quietly hurts your long-term financial position. That is where many borrowers get surprised. A balance carried for months can cost dramatically more than expected, and minimum payments often move principal far slower than people assume.

After reviewing thousands of consumer credit files, one pattern stands out clearly: borrowers who use high-cost credit products as short-term bridge financing often recover fine. Borrowers who rely on them as long-term solutions usually pay far more than they planned. That distinction matters. The repayment strategy matters more than the approval itself.

Before you apply, run the math, compare alternatives, and understand exactly what lenders will see when CreditFresh appears on your credit report.

This guide breaks down how CreditFresh works. Understanding the real dollars cost, how it impacts your credit, who it makes sense for, and what lower-cost options may fit better.

I see CreditFresh accounts show up on client files regularly. The borrowers who used it for a 30-to-60-day bridge , covered an emergency, paid it down fast , generally came out fine. The borrowers who used it as a long-term credit solution paid two to three times what they borrowed before the balance moved significantly. This product fills a real gap. Banks turn away a large segment of Americans who need access to funds. CreditFresh serves that segment. But the math on slow repayment is brutal, and most people do not run it before they sign. Run the math first. Know your exit plan. Then decide if it makes sense for your situation.

What Is Credit Fresh and How Does It Work

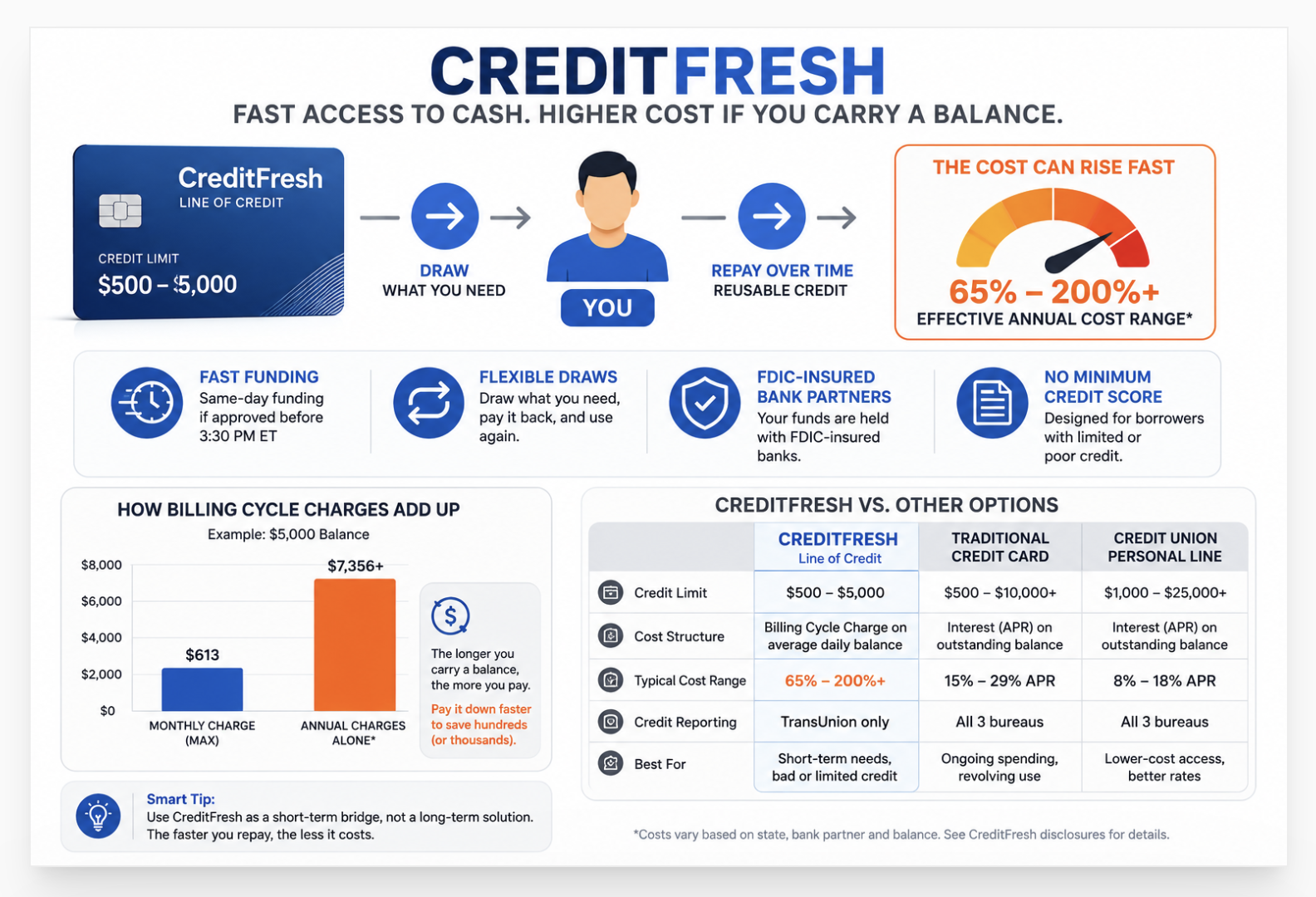

CreditFresh is a revolving personal line of credit platform that connects borrowers with FDIC-insured bank partners. You apply online, get a credit limit between $500 and $5,000, and draw funds as needed. You pay a Billing Cycle Charge on your average daily balance each payment period rather than a standard interest rate. There is no minimum credit score requirement.

Think of CreditFresh as a revolving account that works similar to a credit card. You get a credit limit. You draw what you need from it. You repay over time. As your balance drops, your available credit goes back up and you can draw again without reapplying.

The distinction from a credit card is the cost structure. Credit cards charge APR on the balance you carry. CreditFresh charges a Billing Cycle Charge , a flat fee per payment period based on your average daily balance. The higher the balance and the longer you carry it, the more you pay per cycle.

CreditFresh itself does not lend money directly. The actual credit lines come from FDIC-insured bank partners: CBW Bank (Kansas State Chartered Bank), First Electronic Bank (Utah Chartered Bank), and Column N.A. (a nationally chartered bank for their FreshLine product). CreditFresh handles the platform, application process, and account management. The banks handle underwriting, approval, and funding.

Propel Holdings Inc., the parent company behind CreditFresh, trades on the Toronto Stock Exchange under the ticker PRL. Being a publicly traded company adds a layer of regulatory accountability that privately held lenders do not carry. This matters when assessing whether the platform is legitimate.

The Application Process Step by Step

Start at creditfresh.com and submit basic information , name, address, income, employment. CreditFresh runs a soft credit inquiry at this stage. It does not affect your credit score. You see whether you pre-qualify and get an estimate of your potential credit limit before committing to the full application.

If you move forward, CreditFresh runs a hard credit inquiry. This is the official application submitted to the bank partner. The hard pull temporarily affects your credit score by a few points. Approval decisions typically arrive quickly , in some cases within minutes.

Approved applicants receive a credit limit between $500 and $5,000 based on the bank partner's assessment of income, bank history, and individual circumstances. The limit varies by state and the specific bank partner funding your account.

Request a draw from your available credit through the CreditFresh platform. Funds transfer to your checking account. Same-day funding is available for applications approved before 3:30 PM ET on business days. Subsequent draws come from available credit as you repay your balance.

CreditFresh is a revolving credit line, not a personal loan. You draw as needed, pay billing cycle charges on your balance, and access funds again as you repay. FDIC-insured bank partners fund the accounts. The platform is legitimate, publicly traded, and regulated. The cost structure differs significantly from traditional lending products.

CreditFresh Rates , Understanding the Billing Cycle Charge

Let me walk through what the billing cycle charge actually looks like in practice, because this is the piece that catches most CreditFresh borrowers off guard.

Say you draw $1,500. Your payment schedule is biweekly. Each biweekly payment includes a small mandatory principal contribution plus an $85 billing cycle charge. Over the first three months , six payment periods , you pay $510 in billing charges alone. Your balance at the end of that period drops by significantly less than $510 because each payment primarily covers the billing charge, with a small slice going to principal.

For comparison, a $1,500 balance on a standard credit card at 24% APR costs approximately $20 in interest per month. A credit union Payday Alternative Loan (PAL) at 28% APR costs about $23 per month. CreditFresh at the same balance costs $170+ per month in billing charges on a biweekly payment schedule. That is six to seven times the cost of a credit card at the same balance.

As LendEDU's 2026 CreditFresh review confirms, the billing cycle charge structure makes CreditFresh much more expensive than traditional personal loans over time , particularly for borrowers who carry a balance across multiple billing cycles rather than paying it down aggressively.

Who Should Use CreditFresh

CreditFresh fits a narrow use case. If you need funds within 24 hours, cannot qualify for a personal loan, and plan to pay the balance in full or near-full within 30 to 60 days, the billing cycle charges are manageable. The math changes dramatically when balances persist for months.

Here is the honest version of who this product serves and who it does not.

| Situation | CreditFresh Makes Sense | A Better Option Exists |

|---|---|---|

| Emergency expense, can pay off in 30-60 days | Yes | No better fast option at this credit level |

| Need credit building across all 3 bureaus | No | Secured credit card , reports to all 3 |

| Rejected by every traditional lender | Possibly | Credit union PAL or secured card first |

| Carrying the balance 6+ months | No | Personal loan at a credit union |

| Want to avoid payday loan cycle | Yes | CreditFresh is lower cost than most payday lenders |

| Rebuilding after bankruptcy or collections | With caution | Secured card builds credit at lower cost |

CreditFresh uses a Billing Cycle Charge instead of APR. The effective annual cost runs 65% to 200%+. On a $1,500 balance, the monthly cost is 6-7 times higher than a standard credit card at 24% APR. Short-term borrowers who pay quickly face manageable charges. Long-term minimum-payment borrowers pay significantly more than the amount they originally borrowed.

Does CreditFresh Build Credit

Yes, but only with TransUnion. CreditFresh reports payment activity to TransUnion only, not Equifax or Experian. On-time payments will strengthen your TransUnion credit file. However, CreditFresh does not improve your scores at two of the three major bureaus. A secured credit card that reports to all three bureaus typically costs less and produces broader credit improvement.

CreditFresh is one of the few alternative lending products that reports to any credit bureau at all. Payday lenders typically do not report payment activity. This gives CreditFresh an advantage in the credit-building category compared to other high-cost short-term products.

The limitation is significant though. Mortgage lenders pull a tri-merge report combining all three bureaus and use the middle score. If your TransUnion score improves from CreditFresh payments but Equifax and Experian remain unchanged, your middle score for a mortgage application may not reflect the improvement. The credit building story with CreditFresh is real but incomplete.

From a cost perspective, building credit through CreditFresh is also expensive. Carrying a $1,000 balance for 12 months at CreditFresh billing cycle charges costs roughly $800 to $1,200 in fees alone, depending on balance and payment frequency. A secured credit card with a $200 deposit, used for a small recurring charge and paid in full monthly, builds credit at all three bureaus at zero interest cost. The secured card produces a stronger, broader credit file at a fraction of the cost.

If your goal is to improve your credit score before a mortgage application or major loan, our guide on how lenders read your credit report explains the specific signals underwriters focus on and why three-bureau payment history matters more than single-bureau history in most lending decisions.

CreditFresh Pros and Cons

Those two outcomes show the same product functioning in entirely different ways based on repayment speed. The first borrower paid it off quickly and walked away with a manageable total cost. The second borrowed more, paid minimums, and watched the balance grow. CreditFresh did not change between the two cases. The repayment behavior did.

CreditFresh vs Alternatives

Before applying for CreditFresh, run this comparison against the options you actually qualify for. Many borrowers assume CreditFresh is the only accessible product at their credit level. It is rarely the case.

| Product | Access at Low Credit | Effective Cost | Credit Building |

|---|---|---|---|

| CreditFresh | Yes , no minimum FICO | 65-200%+ APR equivalent | TransUnion only |

| Secured credit card | Yes , deposit required | 0% if paid in full monthly | All 3 bureaus |

| Credit union PAL | Yes , credit union member | Up to 28% APR max (NCUA cap) | Usually all 3 bureaus |

| Credit builder loan | Yes , no minimum score | 5-15% APR typical | All 3 bureaus |

| Personal loan (bank) | Limited , usually 580+ needed | 7-25% APR depending on score | All 3 bureaus |

| Payday loan | Yes , minimal requirements | 300-400%+ APR equivalent | Usually none |

As SuperMoney's CreditFresh comparison notes, borrowers who qualify for a credit union Payday Alternative Loan face a maximum APR of 28% under NCUA guidelines , less than half of CreditFresh's minimum effective rate. If you belong to a credit union, exhaust that option before applying for CreditFresh.

The credit building comparison matters too. When CreditFresh appears on your file, lenders see a high-cost revolving product. A secured credit card on the same file tells a different story , one of disciplined revolving credit management at zero interest cost. Our overview of how the debt collection process works covers what happens when any revolving credit product defaults, which is relevant for any borrower who may struggle with CreditFresh's billing cycle structure.

What Happens If You Default on a CreditFresh Account

A defaulted CreditFresh account follows the standard debt collection process. When payments stop, CreditFresh or its bank partner will attempt collection internally first. If collection fails, the account transfers to a third-party collection agency, which then reports a separate collection tradeline to the credit bureaus.

At that point, two negative marks appear on your credit report: the original CreditFresh account showing a delinquency, and a new collection tradeline from the collection agency. Both affect your credit score independently and both can stay on your report for seven years from the original date of first delinquency.

Understanding how collection agencies operate after a default matters for any borrower using high-cost credit products. Our breakdown of how Revco Solutions and similar collection agencies handle accounts walks through the validation process, your dispute rights under the FCRA, and the pay-for-delete strategy that sometimes removes the collection tradeline entirely rather than simply marking it paid.

For borrowers who received a collection notice related to any debt , including from companies like Marcam Associates , our Marcam Associates debt collection guide covers the consumer rights framework that applies to every third-party collector, regardless of which original account produced the debt.

As WalletHub's CreditFresh user review database shows, the borrowers who ran into default situations often carried balances for extended periods on minimum payments before the billing charges outpaced their ability to repay. The pattern is preventable with a clear repayment plan before the first draw.

Is CreditFresh a payday loan?

No. CreditFresh is a revolving line of credit, not a payday loan. Payday loans require repayment in full on your next payday, typically within two weeks. CreditFresh gives you a reusable credit limit with scheduled payments over time. The similarity is cost , both products carry higher rates than traditional lending. CreditFresh's effective APR of 65-200% is lower than most payday loan products at 300-400%+ APR equivalent. CreditFresh also reports to TransUnion, which most payday lenders do not.

Does CreditFresh affect your credit score?

Yes, in two ways. The eligibility check uses a soft pull , no score impact. The full application triggers a hard pull, which typically costs 5-10 points temporarily. Once the account opens, CreditFresh reports payment activity to TransUnion monthly. On-time payments gradually improve your TransUnion score. Missed payments damage it. The account does not affect Equifax or Experian scores because CreditFresh does not report to those bureaus.

Can I pay off CreditFresh early?

Yes, and you should if possible. CreditFresh charges no prepayment penalty. Paying the balance in full early eliminates all future billing cycle charges. The faster you pay, the less you spend in total. This is the key strategic insight with CreditFresh. Every additional billing cycle you carry a balance generates another billing charge. Paying the full draw back in one or two cycles limits total cost to one or two billing charges , far more manageable than minimum-payment math over months.

Is CreditFresh available in my state?

CreditFresh is not available in all states. Availability depends on the bank partner assigned to your state and state-level lending regulations. Check your eligibility at creditfresh.com , the soft pull pre-qualification step confirms whether the product is available in your location before any hard inquiry runs. States with strict usury laws may limit high-cost lending products like CreditFresh from operating.

High-Cost Credit Has a Cost on Your Credit File Too

A CreditFresh account on your credit report signals to lenders that you borrowed at a high-cost product. Before applying for any alternative credit product, understand what your credit file actually shows right now. Inaccurate entries may be blocking you from traditional lending products at far lower rates. A free 3-bureau audit shows exactly what lenders see.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

Tek Collect Inc , Who They Are and What You Can Do When a CreditFresh account defaults and transfers to a collection agency, understanding how to handle the collector matters as much as understanding the original debt. This covers the debt validation process, your FDCPA rights, pay-for-delete negotiation, and how to remove inaccurate collection entries from all three bureau reports.

-

How Lenders Read Your Credit Report Before deciding whether CreditFresh makes sense for your situation, understand what lenders actually see when they pull your file. This covers the five report sections lenders weight, how FICO models score revolving credit differently from installment credit, and why a high-cost revolving product creates a different signal than a secured credit card in manual underwriting.

-

FICO Score vs Credit Score , What Is the Real Difference CreditFresh reports to TransUnion only. Your TransUnion score, Equifax score, and Experian score are separate numbers built from separate data sets. This covers why those scores differ, which model version each lender type pulls, and why the score you see on a free app is often not the same score your lender sees during a mortgage or auto loan application.