When Was the Credit Score Invented? The Full History from 1841 to FICO in 1989

The credit score was invented in 1989, when Fair Isaac Corporation (FICO) and Equifax launched the first general-purpose consumer credit score, called BEACON. Before that year, no single, standardized number determined whether you could get a loan, rent an apartment, or buy a car. That three-digit number you check today is less than 40 years old.

Running a credit repair company, I hear a version of the same story almost every week. A client comes in, blindsided by a loan denial, and says: "I had no idea my score was this low." One of the most striking accounts I recall is a client who had been using credit for 15 years, thought she had a solid history, and discovered two accounts on her report that were never hers. That kind of situation is far more common than people think.

According to a 2024 Consumer Reports Credit Checkup investigation, 44% of participants found at least one error on their credit report, and more than a quarter found serious mistakes that could actively damage their scores. That is not a fringe problem. That is nearly half of all people who bother to check.

Understanding where the credit score came from helps you understand why errors like these can go undetected for years, and what the system was actually built to do.

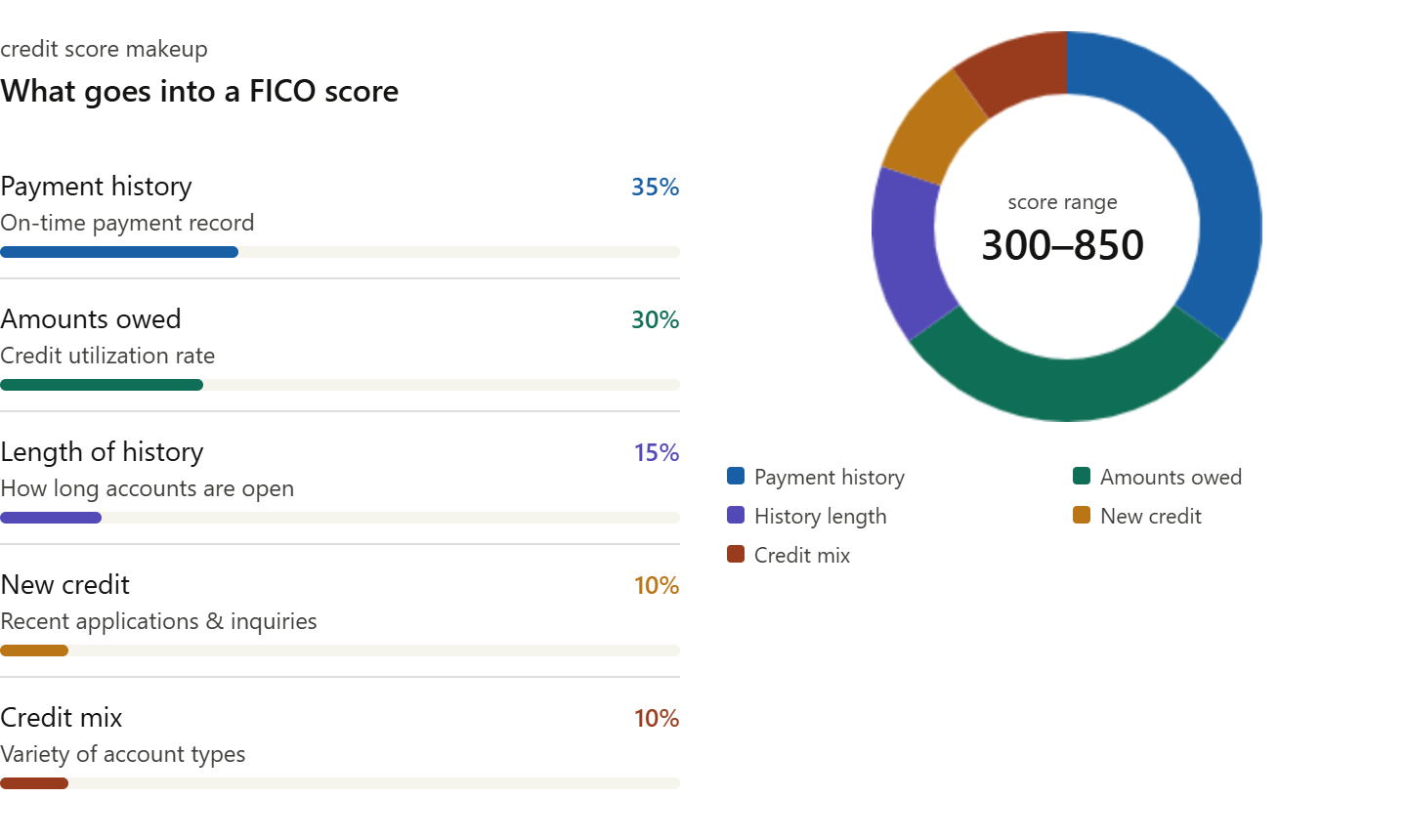

What Is a FICO Credit Score?

A FICO credit score is a three-digit number that ranges from 300 to 850. Higher numbers indicate lower lending risk. Lenders use the score to decide whether to approve you for a loan, and at what interest rate.

The Consumer Financial Protection Bureau (CFPB) notes that most top lenders still use FICO scores when deciding whether to offer a loan or credit card, and in setting the rate and terms.

When was the credit score invented?

The first credit scoring system was developed in 1956. Bill Fair and Earl Isaac founded Fair Isaac Corporation that year and began building algorithms to help lenders evaluate borrowers. However, major adoption was slow.

FICO pitched its scoring model to 50 large lenders in 1958. Only one company, American Investments, adopted it that year. The department store Montgomery Ward implemented it five years later. Credit card providers, auto lenders, and banks did not follow until the early 1970s.

The first true general-purpose consumer credit score did not arrive until 1989. That year, FICO and Equifax launched BEACON, the first credit score built to work across all lenders, not just one company's internal system. That is the birth of the credit score as most people know it today.

Who Invented the Credit Scoring System?

Bill Fair, an engineer, and Earl Isaac, a mathematician, invented the credit scoring system. They met at the Stanford Research Institute and co-founded Fair Isaac Corporation, later renamed FICO, in 1956.

Their core idea was simple but powerful. Instead of letting loan officers judge borrowers based on personal impressions, Fair and Isaac wanted a data-driven formula. A formula that treated every applicant the same way, based only on their financial behavior.

The credit bureaus eventually recognized the value of this approach. Equifax, Experian, and TransUnion partnered with FICO to build a shared national scoring model. That model launched in 1989 and became the industry standard.

When Did the Credit Score Era Start?

The credit score era officially started in 1989, but the groundwork was laid nearly 150 years earlier. Formal credit reporting in the United States began in 1841, when Lewis Tappan founded the Mercantile Agency in New York City. It was the country's first commercial credit reporting agency.

Tappan built the agency after the financial crisis of 1837, which was partly caused by reckless credit extension. He hired correspondents across the country to gather information on borrowers: character assessments, debt history, marital status, and even racial background. The information was highly subjective and often biased, but it was the beginning of organized credit tracking.

By the 1960s, more than 2,000 local credit bureaus operated across the United States. Each one kept paper files in filing cabinets. Over the following two decades, larger companies bought up these local bureaus, computerized the records, and consolidated the market. Today, three major bureaus dominate: Equifax, Experian, and TransUnion.

What Was Used Before Credit Scores?

Before credit scores, lenders made decisions based on personal judgment. A loan officer might interview a business owner in the community, or ask around town about an applicant's reputation. Race, gender, social status, clothing, and personality all played a role in those decisions.

In the 1930s, some department stores began assigning point values to customer data to better estimate who would pay. This was a crude early form of quantitative credit assessment, but it varied by store and had no standardized structure.

The problem with all of these methods was inconsistency. Two lenders could look at the same borrower and reach opposite conclusions. Discrimination was widespread. There was no way for a consumer to know what information lenders were using or how to challenge it.

That inconsistency is exactly what Bill Fair and Earl Isaac set out to fix.

Why Was the Credit Score Invented?

Credit scores were invented to solve three specific problems in the lending industry.

Personal bias — Lenders made decisions based on race, gender, and social class. A standard formula removed those factors from the equation.

Speed — Manual credit reviews took too long and cost too much. Automated scoring allowed lenders to process applications faster.

Accuracy — A consistent model produced more reliable predictions of repayment risk than a loan officer's gut instinct.

The goal was a fairer, faster, more objective system. Whether it fully achieved that goal is a separate debate. Researchers have noted that structural inequalities, like the history of redlining, still affect the credit histories of many minority borrowers today. But the intention behind the credit score was to eliminate individual bias from lending decisions.

How Did the Credit Score Change Over Time?

The credit score did not become dominant overnight. Even after the 1989 FICO launch, many lenders were slow to adopt it. The real turning point came in 1995, when Fannie Mae and Freddie Mac made FICO scores mandatory for residential mortgage applications.

That requirement changed everything. Fannie Mae and Freddie Mac together support roughly 70% of the U.S. mortgage market. Once they required a FICO score, lenders across the country followed. By the late 1990s, the three-digit score had become a permanent fixture in American financial life.

A key milestone before that point was the Fair Credit Reporting Act (FCRA) of 1970. The FCRA was the first federal law to regulate credit bureaus. It gave consumers the right to access their credit reports, dispute errors, and have outdated negative information removed after seven to ten years. The law also removed race, sexuality, and disability from credit reports.

In 2003, Congress passed the Fair and Accurate Credit Transactions Act (FACTA), giving every American the right to one free credit report per year from each bureau.

What Is VantageScore and How Does It Compare to FICO?

VantageScore is a competing credit scoring model. Equifax, Experian, and TransUnion created it together in 2006. The three bureaus built it as an alternative to FICO, one they could control and update without relying on a third party.

VantageScore started with a different scoring range (501 to 990), but later adopted the 300 to 850 scale that FICO uses. The most current version, VantageScore 4.0, uses trended credit data, meaning it tracks credit behavior over 24 months rather than a single snapshot. It also excludes paid medical debt from its calculations.

In practice, most top lenders still use FICO. VantageScore is more commonly used by banks and credit card issuers, and it is the score shown in many free credit monitoring apps.

In our office alone, we have seen cases where a client's FICO score and VantageScore differ by 40 to 60 points. That gap matters when you are applying for a mortgage and your lender pulls FICO while you have been tracking VantageScore.

How Accurate Are Credit Scores Today?

Credit score accuracy depends entirely on the accuracy of the underlying credit report. If the data in your report is wrong, your score is wrong.

The numbers on this are not small. The FTC's landmark study found that one in five Americans has at least one error on one of their three credit reports. One in ten has an error significant enough to lower their score. That study covered more than 1,000 participants and nearly 3,000 credit reports.

Last year alone, credit report complaints to the CFPB totaled 644,839, more than twice the number filed in 2021. Complaints about incorrect information specifically numbered 443,321 in 2023, compared to 165,129 two years earlier. Those are not small jumps. That is a system under real strain.

Common errors include accounts that were paid off but still show as delinquent, the same loan listed twice, and accounts belonging to someone else entirely. These mistakes do not fix themselves. You have to catch them and dispute them.

Errors on Your Credit Report Could Be Hurting Your Score

Credit scores have shaped lending decisions for decades — but inaccurate accounts and reporting errors can still lower your score today. Get a professional review of your credit report and see what may be hurting your approval odds.

Check Your Credit Report NowNo obligation • Fast review • Understand what may be impacting your credit score

What Credit Scores Mean for You Right Now

Credit scores touch more of your life than most people realize. Mortgage lenders, car loan companies, landlords, and even some employers use them. A lower score means higher interest rates. A score with errors means you may be paying more than you should for years without knowing why.

The credit scoring system was designed in the 1950s to eliminate bias. The universal FICO score was launched in 1989 to create consistency. The FCRA of 1970 gave you legal rights over your own credit data. Each of these milestones was built to protect you, but only if you use them.

Check your credit reports regularly at AnnualCreditReport.com, the only federally authorized source for free reports from all three bureaus. Dispute any account you do not recognize. Do not wait for a loan denial to find out something is wrong.

The credit score has a 35-year history as a consumer tool. That history only works in your favor if you stay active in it.