Yes, you can get dental loans with poor credit. However, the approval depends on income, debt levels, credit history, and the financing company’s underwriting rules. Many borrowers with lower scores qualify through medical credit cards, dental office payment plans, secured loans, co-signers, or lower cost treatment alternatives like dental schools and nonprofit clinics.

Dental pain creates financial urgency, and urgency makes people take expensive money fast.

That is where many borrowers with poor credit get trapped. When you need a root canal, implant, crown, dentures, or emergency oral surgery, waiting may not be realistic. Infection spreads. Pain worsens. Health risks grow. But financing becomes harder when lenders see a low credit score, recent collections, maxxed out cards, or unstable repayment history.

What I would like to share with you is that poor credit does not automatically mean no options.

It means different options.

Approval may come from healthcare financing lines, in-house payment plans, secured borrowing, nonprofit dental clinics, dental schools, or staged treatment planning that lowers immediate cost.

Being in the industry for alsmost 20 years, I know that one emergency expense pushed borrowers deeper into debt because they financed dental work the wrong way. Deferred interest products, high APR installment loans, and predatory payment plans can solve pain today but create credit damage tomorrow.

Funding treatment matters. Funding it smart matters more.

Across Reddit finance threads, one pattern repeats constantly. That's borrowers denied for traditional financing often find workable alternatives through second opinions, university dental clinics, soft-pull financing prequalification, or structured office payment plans that avoid hard credit denials.

Dental Loans With Poor Credit

How to Pay for Dental Work When Your Credit Score Is Bad

Can You Get Dental Loans for Poor Credit

Yes. Dental loans for poor credit exist through multiple channels. Approval depends more on income, debt-to-income ratio, and recent payment behavior than on a credit score threshold alone. A 580-score borrower with stable employment and low utilization often gets approved where a higher-score borrower with recent late payments and maxed cards does not. Poor credit changes the options available. It does not eliminate them.

Let me be direct about what poor credit actually changes in dental financing, because most articles give the same generic "yes you can" answer without explaining the mechanics.

Poor credit raises your cost and narrows your channel. Traditional bank personal loans typically require 620 or above and offer lower APRs. Subprime lenders and medical financing platforms take applications from 580 and below but price the loan at 20-35% APR. In-house dental office payment plans often bypass the credit check altogether and approve based on employment verification and income. Dental schools and community health centers bypass financing entirely by reducing the cost of care.

The goal is not to find any dental loan. The goal is to find the lowest-cost path to treatment that fits your specific income, score, and repayment capacity. That path looks different for a 580-score borrower with stable income than for the same score borrower with spotty employment history and two recent collections.

As NerdWallet's medical loan analysis confirms, lenders in the healthcare financing space use income and employment verification heavily alongside credit score , meaning borrowers with lower scores but consistent paychecks find more approval options than the score alone would suggest.

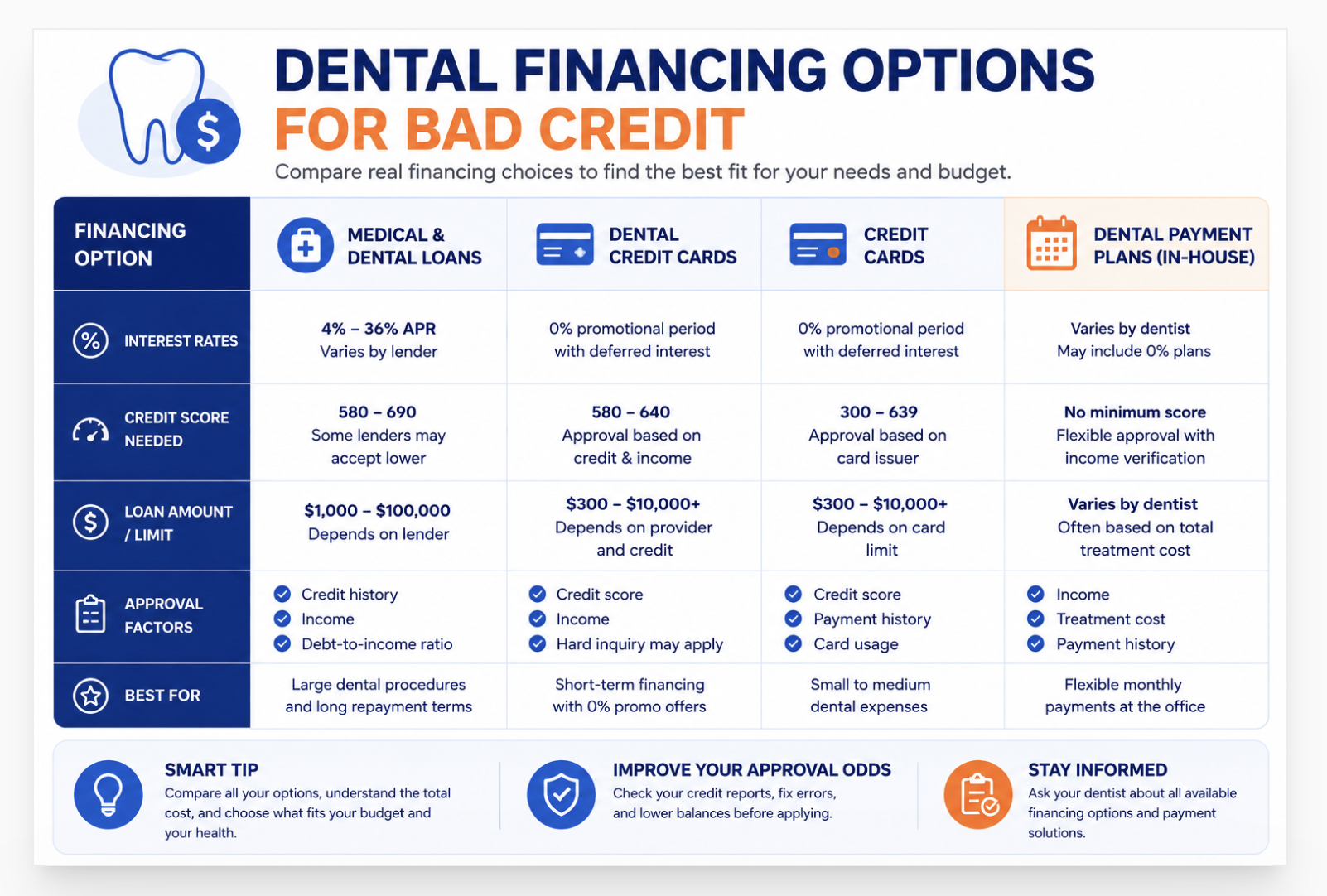

What Credit Score Do Dental Financing Companies Want

| Financing Type | Typical Score Threshold | Key Approval Factors Beyond Score |

|---|---|---|

| In-house dental payment plan | Often no minimum , soft pull or no pull | Down payment amount, employment verification, consistency of income |

| CareCredit / Sunbit (medical credit cards) | 600-620 commonly approved | Income, DTI, recent derogatory marks, hard inquiry impact |

| Subprime personal loan (online lenders) | 580+ | Income, employment length, DTI, bank account history |

| Secured personal loan | Any score , secured by asset | Value and type of collateral, income to service the loan |

| Co-signer personal loan | Primary borrower score + co-signer's stronger profile | Co-signer's income, score, and DTI determine the rate tier |

| Traditional bank personal loan | 620-660 minimum at most banks | Account relationship, income, DTI, employment history |

| Dental school or community clinic | No credit check | Income (for sliding scale programs), waitlist availability |

The contrarian reality worth naming: a 580 score with stable income and 20% credit card utilization often beats a 640 score with 90% utilization and a recent 30-day late. Lenders review more than your score , they evaluate the full underwriting picture, and the debt-to-income ratio, recent derogatory pattern, and payment behavior of the last 12 months carry significant weight alongside the score number.

Best Dental Loan Options for Poor Credit

In-House Dental Payment Plans

In-house payment plans are the most accessible dental financing option for borrowers with poor credit. The dental office acts as the lender directly, eliminating the third-party underwriting process that triggers hard inquiries and credit score thresholds.

Most in-house plans require a down payment of 25-50% of the treatment cost, with the remainder paid over 3-12 months in equal installments. Some offices charge no interest. Others charge a flat administrative fee. The payment structure appears directly on the office's accounts receivable , not in any credit bureau file , as long as payments stay current.

The credit risk appears when payments are missed. A dental office that sends a delinquent account to a collection agency creates a collection tradeline on the patient's credit report. That tradeline reports the same way any other collection does , with the original delinquency date, balance, and collection agency name , and stays on the report for seven years.

Before asking a dental office about in-house financing, ask these specific questions: Does approval require a credit check? If yes, is it a soft pull (no score impact) or a hard pull (costs 5-10 points)? What is the interest rate or fee structure? What happens if a payment is missed , does the office report to credit bureaus or send to collections directly?

Medical Credit Cards and Deferred Interest Risks

Medical credit cards like CareCredit and Sunbit are widely marketed to dental patients as promotional financing. The offer sounds straightforward , 0% interest for 12, 18, or 24 months. The reality requires reading the fine print carefully.

The term is "deferred interest," not "0% interest." These are fundamentally different products. During the promotional period, interest accrues at the full APR (often 26.99%) on the entire original balance , it simply does not get charged unless the balance remains unpaid when the promotional window closes. If you borrow $3,000 for a crown and root canal, pay $2,800 by month 18, and have $200 remaining when the promotion ends, the full 18 months of deferred interest on $3,000 posts to your account simultaneously. Not interest on $200. Interest on $3,000 for the full promotional period.

One forum user described the experience precisely: they paid consistently for two years, thought they were almost paid off, and then received a statement showing they owed more than the original dental work because the deferred interest triggered on a small remaining balance. This is not an edge case. It is the design of the product.

CareCredit does report payment activity to credit bureaus. Adding the card adds a hard inquiry and increases your revolving utilization, which affects your score in two directions simultaneously. Regular on-time payments build payment history. But if the balance runs high relative to the credit limit, the utilization ratio suppresses the score independently of the clean payment record. High balances can lower approval odds fast , a point that applies whether the high balance is on a standard credit card or a CareCredit account.

Personal Loans for Dental Work With Low Credit

A personal loan for dental work differs from a medical credit card in one key way: the interest rate is fixed and visible from day one. No deferred interest trap. No promotional window to miss. The APR on the loan determines the cost of borrowing for the full term.

For poor credit borrowers, subprime personal loan lenders , Upstart, OneMain Financial, Avant, and LendingClub among others , offer installment loans with approval thresholds starting around 580. The APR for subprime borrowers typically runs 20-36%. At 25% APR on a $3,000 dental loan over 24 months, the monthly payment runs approximately $161 and total interest paid reaches $864.

As Bankrate's personal loan for medical expenses guide notes, income and employment stability matter significantly alongside credit score for subprime personal loan approvals. A borrower at 580 who provides six months of bank statements showing consistent direct deposits, a long-standing employer relationship, and low existing monthly debt obligations often qualifies for amounts dental office in-house plans would not cover.

Use soft-pull prequalification before applying. Most online subprime lenders offer a prequalification check that shows estimated rate and term with no hard inquiry impact. This lets you compare real offers across multiple lenders before choosing, then apply with only one hard pull. Applying at multiple lenders without prequalifying first generates multiple hard inquiries , each costing 5-10 points , before you know which one will approve you.

For borrowers considering larger loan amounts for complex dental work , multiple implants, full mouth restoration, or orthodontics combined with restorative work , understanding how to get approved for a $20,000 loan with poor credit covers the full underwriting picture lenders evaluate when the loan amount rises above what medical credit cards typically extend.

Dental Schools and Low-Cost Clinics

Dental schools and federally qualified health centers (FQHCs) represent the most overlooked path for borrowers who need dental work but cannot qualify for financing or cannot afford the payment structure of most dental loans.

Dental schools operate accredited clinics where dental students perform procedures under faculty supervision. The procedures are identical , the same fillings, crowns, root canals, dentures, and implants performed in private practice. The cost runs 30-60% below private practice rates. A crown costing $1,400 at a private dentist may run $500-$700 at a dental school clinic.

FQHCs receive federal funding to provide care on a sliding scale fee structure based on household income. Some patients pay a nominal flat fee of $20-$40 per visit. Dental services are covered under the HRSA mandate for comprehensive primary care. The HRSA facility finder at findahealthcenter.hrsa.gov locates the nearest federally qualified health center by zip code. Many people with dental emergencies do not know this resource exists or that it applies to dental care.

| Low-Cost Option | Cost vs Private Practice | Credit Required? | Typical Wait |

|---|---|---|---|

| Dental school clinic | 30-60% lower | None | 1-4 weeks for appointments |

| Federally Qualified Health Center (FQHC) | Sliding scale , sometimes near-free | None | Varies , sometimes same week |

| Nonprofit dental clinic | 50-80% lower for qualifying patients | None | Waitlists for complex work |

| Cash negotiation with private dentist | 10-20% lower for full cash payment | None | Immediate |

| Dental discount plans (not insurance) | 10-60% lower depending on procedure | None | Immediate after enrollment |

What Happens If You Finance Dental Work and Miss Payments

Missing payments on dental financing produces three consequences: a late mark on your credit report if the account goes 30 or more days past due (costs 60-110 points), retroactive full-APR interest charges if the missed payment falls inside a deferred interest promotional window, and potential account charge-off and collection transfer if multiple payments are missed. A collection from a dental debt reports identically to any other collection and stays on your report for seven years.

The sequence matters. Missing one payment by a few days typically triggers a late fee from the lender but not a credit bureau report , most creditors report late only at 30 days past due. If you realize the payment failed and correct it within 29 days, the credit impact is zero (beyond the late fee from the lender).

At 30 days past due, a late mark posts. That mark costs 60-110 points depending on your starting score , a higher score loses more from the same mark. The late payment stays on your credit report for seven years from the date of the missed payment, though its negative impact on the score diminishes over time.

At 90-180 days past due, most lenders charge off the account. A charge-off means the lender writes the balance off as a loss , it does not mean you stop owing the debt. After charge-off, the account may transfer to a third-party debt collection agency, adding a second negative tradeline to your report. The original charge-off and the collection account both appear independently. Both stay for seven years. Both suppress the score.

Understanding what lenders see when they read your full credit file helps contextualize why a dental debt that goes to collection can close doors you did not know you were opening. The collection not only damages the score , it appears in the derogatory section of any tri-merge mortgage report, triggers underwriter questions, and in some cases requires letter of explanation or payoff before a home loan will close. For borrowers already dealing with very poor credit where even the financing options are limited, a dental collection compounds an already constrained file.

Bad Credit Is Not Always the Biggest Problem

Poor credit borrowers sometimes get denied dental financing for reasons that have nothing to do with their score. High utilization closes doors faster than a low score does for many healthcare financing platforms. A borrower at 580 with three maxed credit cards gets denied where a borrower at 560 with 15% utilization and stable direct deposit income gets approved. Recent late payments within the last 12 months trigger hard denials at many medical credit card underwriters regardless of score. A thin credit file with few accounts produces the same "insufficient credit history" denial that a damaged file does, even though the underlying financial behavior may be responsible. And a high debt-to-income ratio from existing monthly obligations , car payments, student loans, child support , limits the monthly payment capacity lenders are willing to extend new financing toward, independently of score. The score is one input. The full underwriting profile determines the outcome.

How to Improve Approval Odds Before Applying

Use soft-pull prequalification first

Most online lenders and some medical financing platforms offer prequalification with no hard inquiry. Submit basic income and identity information. The lender returns an estimated rate and approval likelihood without pulling a hard inquiry. Compare offers across multiple lenders through prequalification, then submit one formal application with a hard pull. Stacking hard inquiries from multiple applications without prequalifying first costs 5-10 points per inquiry. Because different lenders use different scoring models, the score they see may vary from the consumer score you checked, making prequalification feedback more informative than self-reported score comparisons.

Reduce credit card utilization before applying

Paying credit card balances below 30% , ideally below 10% , before the statement close date can produce 20-40 points of score improvement within one billing cycle. That improvement posts to the bureaus before any new application generates a hard inquiry. Lower utilization also improves the debt-to-income calculation that healthcare financing underwriters evaluate alongside the credit score.

Address credit reporting errors before any application

Inaccurate entries on your credit report suppress scores below where your real payment history would place them. A wrong late payment date, a duplicate collection, or an account balance that did not update after a payoff all appear in any hard inquiry the dental financing lender pulls. Credit reporting errors may be suppressing approvals before the actual application even processes. Dispute inaccuracies at all three bureaus 30-45 days before applying. A successful removal during that window can shift a borderline denial into an approval.

Consider staged treatment to reduce the financed amount

Lenders set maximum approval amounts based on your income and DTI. A borrower who needs $6,000 in dental work but only qualifies for $3,000 in financing can negotiate a treatment sequence with the dentist , addressing the most urgent need first, financing only that portion, then addressing the rest after the first balance is paid down or the credit profile improves. Staged treatment does not solve every dental situation, but for work that is painful but not an immediate medical emergency, it reduces both the financed amount and the underwriting risk the lender evaluates.

Better Alternatives to High-Interest Dental Loans

Before signing any dental loan with a 25-36% APR, these alternatives deserve consideration:

Negotiate cash pricing with the dentist directly. Most private dental practices charge a higher rate because they factor in insurance company negotiations and administrative overhead. A patient who offers to pay the full amount in cash at the time of service frequently receives 10-20% off the standard rate without financing. Ask specifically: "What is the cash price if I pay today?"

Apply for a dental discount plan. Dental discount plans (not insurance) charge an annual membership fee of $100-$200 and provide discounted rates at member dentists , typically 10-60% below standard pricing. No underwriting. No credit check. Same-day access after enrollment. For patients with ongoing dental needs, the annual savings can far exceed the membership cost.

Use an existing low-APR credit card if available. If you already carry a credit card with available credit and a sub-20% APR, using it for dental work produces a lower effective cost than a new subprime dental loan at 30% APR. This approach avoids the new account inquiry, the new account utilization spike, and the underwriting process entirely.

Check employer and union dental assistance programs. Some employers offer emergency financial assistance or healthcare expense loans to employees. Some unions run hardship funds that cover dental emergencies. These programs are interest-free and do not report to credit bureaus.

For borrowers rebuilding credit while managing existing debt, understanding how new credit obligations affect your overall credit profile matters across every lending context. The same principles that affect dental loan approval , utilization, DTI, payment history, recent inquiries , affect auto loan approval. Our breakdown of how bad credit affects car loan approval and what to do covers the same underlying file factors that dental financing underwriters evaluate, showing why addressing the root credit issues before any major financing decision produces better outcomes across multiple product types simultaneously.

Can I get a dental loan with poor credit?

Yes. Options include in-house dental office payment plans, medical credit cards (CareCredit, Sunbit), subprime personal loans, secured loans, and co-signer loans. Dental schools and FQHCs eliminate financing entirely by reducing the cost of care. Approval for financing depends on income and debt-to-income ratio alongside the credit score. A 580 borrower with stable income often qualifies where a higher-score borrower with recent derogatory marks and maxed cards does not.

What is the easiest dental financing to get with bad credit?

In-house dental office payment plans are the easiest to access with poor credit. They often involve no hard credit check, no third-party underwriting, and approval based on a down payment and proof of income. They do not build credit history because the office typically does not report to credit bureaus. But they provide treatment access without the hard inquiry stack or score threshold that medical credit cards and personal loans require.

Will applying for dental financing hurt my credit score?

Most formal dental financing applications trigger a hard inquiry that costs 5-10 points. Medical credit cards report a new revolving account to the credit bureaus, which raises utilization and temporarily reduces average account age. Soft-pull prequalification does not affect your score. Applying through multiple lenders within a short window generates multiple hard inquiries. Using in-house payment plans or dental school services avoids any credit inquiry entirely.

What is the cheapest way to pay for dental work with poor credit?

Dental schools charge 30-60% below private practice rates with no credit check. FQHCs use a sliding scale fee based on income , sometimes near-zero for qualifying patients. Negotiating a cash payment with a private dentist often produces a 10-20% reduction from the standard rate. Dental discount plans reduce costs by 10-60% for a small annual membership fee. All of these paths reduce the amount that needs financing or eliminate the need for a loan entirely.

Credit Reporting Errors May Be Blocking Your Dental Financing Approval

Inaccurate entries at one or more bureaus suppress your score below where your real payment behavior would place it. A free 3-bureau audit shows exactly what Equifax, Experian, and TransUnion report right now , and identifies every disputable entry that a lender sees when they pull your file for dental financing, a personal loan, or any other credit application.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

Tri Merge Credit Report , What Mortgage Lenders Really See When dental debt goes to collections and that collection appears on your credit file, it surfaces in a tri-merge mortgage report the same as any other derogatory mark. This covers how lenders see all three bureau files simultaneously, why a single-bureau collection can suppress your middle mortgage FICO score, and what the dispute and removal process looks like before a home loan application.

-

How to Get Approved for a $20,000 Loan With Poor Credit Complex dental work , implants, full-mouth restoration, orthodontics combined with restorative procedures , sometimes requires loan amounts that exceed what medical credit cards extend. This covers the full underwriting picture for larger personal loan applications, including what documentation subprime lenders require, how co-signer underwriting works, and the secured loan path when the credit score alone would not qualify a solo application.

-

Can Bad Credit Stop a Car Loan , What to Do The same credit file factors that affect dental loan approval , utilization, DTI, recent derogatory marks, and the specific FICO model the lender uses , affect auto loan decisions in the same order of priority. This covers how lenders read a poor credit file for installment loan products, what compensating factors matter most, and how to prepare the file before any financing application rather than responding to denials after the fact.