A tri merge credit report is one of the most important reports in mortgage lending because it often decides whether you get approved, what rate you receive, and how risky lenders think you are.

Most buyers assume lenders pull one score. That is not true. Mortgage underwriting looks at all three major credit bureaus, comparres the data, and merges those files into one consolidated report.

You have to know this because your Experian, Equifax, and TransUnion reports are often not identical. One bureau may show a collection account, the others do not. One may report a higher balance. One may generate a lower mortgage FICO score. When lenders combine all three, hidden weaknesses surface fast.

We at ASAP Credit Repair USA compared files where borrowers thought they were mortgage ready. All because a free app showed a 690 score, then saw a tri merge report produce a middle mortgage score in the low 640s.

That difference changed approval terms. It increased monthly payment rates, In worse cases, delayed closing.

Across mortgage forums, borrowers repeatedly say the same thing after preapproval: the score they checked was not the score the lender used.

That is why understanding tri merge credit reporting matters before applying, not after underwriting starts.

Tri Merge Credit Report Explained for Home Buyers

What Is a Tri Merge Credit Report

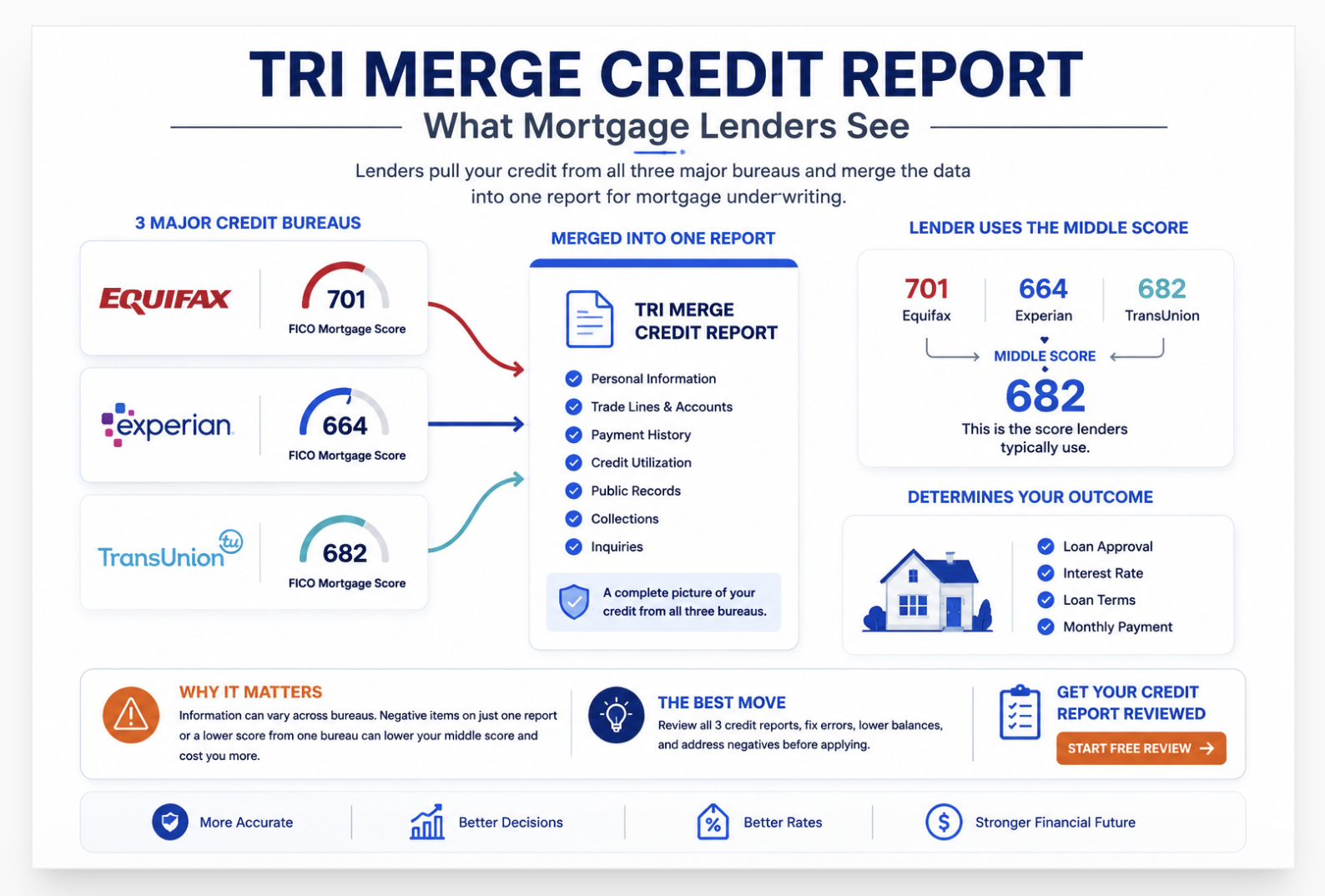

A tri merge credit report combines Equifax, Experian, and TransUnion credit data into one consolidated mortgage underwriting document. Lenders use it because each bureau holds independent data that frequently differs. The tri merge surfaces all three bureau files simultaneously, generating three mortgage FICO scores. The middle score determines mortgage qualification and rate pricing.

Most people think lenders pull one credit score. That is not how mortgage underwriting works.

A tri merge credit report is specifically a mortgage product. Your credit card issuer pulls one bureau. Your auto lender likely pulls one bureau. But a mortgage lender pulls all three simultaneously, merges the data into a single underwriting file, and generates three distinct mortgage FICO scores from the merged data. That file is the tri merge.

The reason lenders need all three comes down to bureau independence. Equifax, Experian, and TransUnion each maintain separate databases. Creditors choose which bureaus to report to and some report to only one or two. A collection account your doctor's billing department reported to Experian may not appear on your Equifax or TransUnion file. A student loan servicer reporting to TransUnion may not appear on Experian. The tri merge catches all of it.

As Experian's mortgage credit score guide confirms, mortgage lenders pull the specific FICO versions designed for mortgage decisions , not the FICO 8 or VantageScore you see on a free dashboard. The tri merge is how lenders access those specialty mortgage FICO scores from all three bureaus at once.

How a Tri Merge Credit Report Is Built

A tri merge credit report does not come from the bureaus directly. It comes from a Consumer Reporting Agency (CRA) , a third-party credit reporting vendor authorized to pull from all three bureaus simultaneously and merge the output into a single formatted report for mortgage underwriting use.

Here is what happens in sequence when a mortgage lender initiates a tri merge pull:

The lender sends an inquiry to a CRA with the borrower's name, Social Security number, date of birth, and address history. The CRA simultaneously queries Equifax, Experian, and TransUnion. Each bureau responds with that borrower's credit file from its own database. The CRA merges the three files, deduplicates tradelines where the same account appears across multiple bureaus, flags discrepancies where the same account shows different information at different bureaus, and formats the combined output into the standardized tri merge report. The lender receives one consolidated document that displays the three bureau files side by side with the three mortgage FICO scores appended.

The hard inquiry from a tri merge pulls appears on all three bureau files simultaneously. Under FICO's rate-shopping rules, multiple mortgage inquiries within a 45-day window count as one inquiry for score purposes. Shopping multiple lenders within that window costs the same as a single pull.

What Is Included in a Tri Merge Credit Report

Full legal name, aliases, prior names, Social Security match verification across all three bureaus, current and previous addresses, and employment history. Discrepancies in name spelling or address matching across bureaus appear as flags in the tri merge.

Mortgages, credit cards, auto loans, student loans, personal loans, and home equity lines , from all three bureaus, deduplicated where the same account appears on multiple files. Accounts appearing on only one bureau show as unique to that bureau.

30, 60, and 90-day late marks, charge-offs, account delinquencies, and current status per bureau. The tri merge shows where the same late payment appears differently across bureaus , a critical area for underwriter review because bureau-specific derogatory marks affect the score at that bureau alone.

Each revolving account's current balance, credit limit, and utilization percentage per bureau. High balances lower mortgage scores fast , and because each bureau may report a different balance depending on when the creditor last reported, utilization can differ across the three files in the tri merge. Our breakdown of how the credit utilization ratio affects scoring covers why paying down cards before the statement close date , not the due date , changes what the tri merge shows.

Medical collections, charged-off debt collections, and third-party collection accounts by bureau. A collection that only one bureau received creates a bureau-specific drag on that bureau's score. The tri merge reveals which bureau holds the derogatory mark and which do not , directly informing dispute strategy.

Bankruptcies by filing date and chapter type. Hard inquiries from mortgage, auto, and credit card applications , all three bureaus simultaneously. Credit reporting errors in public record sections can drag the middle score down when they appear on only one or two bureaus. The 609 letter process and the dispute framework address exactly those kinds of credit reporting errors that affect your middle mortgage score.

Why Mortgage Lenders Use Tri Merge Reports

Lenders use tri merge reports for one fundamental reason: completeness. No single bureau has a complete picture of any borrower's credit history because creditors are not required to report to all three bureaus.

A lender who pulled only Experian would miss every account and derogatory mark that a creditor chose to report only to TransUnion or Equifax. In mortgage lending, where the loan amount can reach six or seven figures, an incomplete credit picture creates real risk. The tri merge closes that information gap by pulling all three simultaneously.

The tri merge also serves as a verification document. When the same account appears on two bureaus with different balances, different payment statuses, or different account numbers, the underwriter sees the discrepancy directly in the merged file. That discrepancy may indicate a reporting error , which the borrower can dispute before the loan closes , or it may indicate a data lag where one bureau received a more recent update than the others.

Finally, the tri merge determines rate pricing through the middle mortgage FICO score. Because different lenders have access to different rate tiers based on score, the middle score from the tri merge locks in the pricing for the entire loan. A score one tier below a threshold , 679 versus 680, for example , changes the rate enough to cost tens of thousands of dollars over a 30-year term. As Bankrate's mortgage credit score guide shows, the interest rate difference between a 640-tier and a 720-tier borrower on a $400,000 loan can exceed $100,000 over the full loan term. The tri merge determines which tier applies.

How Mortgage Lenders Use the Middle Credit Score

Mortgage lenders use the middle of the three mortgage FICO scores from the tri merge report. Not the highest. Not the average. The middle value. For joint applications, lenders use the lower middle score between the two borrowers. This middle score determines loan eligibility, rate tier, and qualifying loan program.

Here is the joint application version that catches co-borrowers off guard.

| Borrower | Bureau 1 Score | Bureau 2 Score | Bureau 3 Score | Middle Score |

|---|---|---|---|---|

| Primary borrower | 719 | 704 | 688 | 704 |

| Co-borrower | 680 | 658 | 671 | 671 , used for pricing |

The practical implication is significant. A couple where one partner has a 750 middle score and the other has a 640 middle score qualifies at 640. The 750 score carries no weight on the rate. Both income streams count toward DTI. Only the lower middle score counts toward rate pricing. Whether to add a co-borrower , and which partner takes the primary versus co-borrower role , sometimes matters more than which loan program to choose. Understanding the middle score mechanism shapes that decision. Our guide on how the mortgage score directly changes approval odds on a $400,000 home shows the dollar impact of each 20-point band across the qualifying score range.

Why Your Three Credit Scores Are Different

Your three bureau scores differ for reasons that are structural, not random.

Selective creditor reporting is the biggest driver. No law requires creditors to report to all three bureaus. Many report to one or two. If your best payment history account only reports to TransUnion and Experian, Equifax builds your score without that positive data. The inverse applies to negative marks. A collection that the debt buyer only reported to Experian drags your Experian mortgage FICO while leaving Equifax and TransUnion unaffected.

Balance reporting timing creates temporary differences. When you pay down a credit card, the new balance posts to each bureau only when the creditor submits their next monthly data file. Creditors submit files at different times in the month. The same card can show $4,200 at Experian and $2,800 at TransUnion on the same day if TransUnion received the updated balance after a payment that Experian has not yet processed.

Inaccurate entries at one bureau create score discrepancies that lenders see but borrowers often do not know exist until the tri merge surfaces them. A wrong late payment date at Equifax, a duplicate collection at Experian, or a wrong balance at TransUnion each affect only that bureau's score. The tri merge shows all three simultaneously, which is why reviewing all three reports before applying matters more than checking a single consumer app score. When a credit reporting error drags your middle score down, the dispute process under the FCRA is the direct fix. Understanding how underwriters evaluate risk when they read a credit report shows why bureau-specific discrepancies flag differently in manual versus automated underwriting review.

How a Tri Merge Credit Report Affects Mortgage Approval

The tri merge affects mortgage approval through four direct mechanisms.

Qualifying score and rate tier. The middle mortgage FICO from the tri merge determines which rate tier applies. Most lenders segment pricing into bands: below 620, 620-639, 640-659, 660-679, 680-699, 700-719, 720-739, 740 and above. Each band carries a different interest rate. The tri merge is the document that places a borrower in one of those bands.

Derogatory mark discovery. The tri merge surfaces bureau-specific negative entries the borrower may not have known existed. A collection showing at one bureau but not the other two appears in the merged file and triggers underwriter questions. The automated underwriting system (AUS) , either Fannie Mae's Desktop Underwriter or Freddie Mac's Loan Product Advisor , processes the tri merge data and flags accounts with recent derogatory history, high balances, or disputed entries.

Bureau discrepancy flags. When the same account shows different information at different bureaus, the tri merge flags the discrepancy. An underwriter reviewing a flagged discrepancy may require a letter of explanation, additional documentation, or resolution of the discrepancy before issuing a clear to close. Discrepancies that cannot be explained can delay closing while the buyer works with the CRA and bureaus to resolve conflicting data.

Loan program eligibility. Certain loan programs have score floors based on the middle score the tri merge produces. FHA requires a 580 middle score for 3.5% down. Conventional requires 620. CalHFA requires 660-680. VA has no official floor but most lenders set overlays at 580-620. If the tri merge produces a middle score that falls below a program's floor, that program closes and the buyer either addresses the score or finds a program with a lower minimum. Our breakdown of the difference between mortgage FICO scores and consumer scores covers why the mortgage lenders use different FICO scoring models than what appears on free apps , and why the model version matters as much as the score number.

How to Improve Your Tri Merge Credit Profile Before Applying

Improving a tri merge credit profile requires addressing all three bureau files simultaneously, not just the one a free app shows. The middle score is only as strong as the weakest of the three middle candidates , and since lenders use the middle, any single bureau's weak score can determine the qualifying tier.

Step 1. Pull all three bureau files before any lender does

AnnualCreditReport.com provides free access to Equifax, Experian, and TransUnion reports. Pull all three and read them side by side. Look for accounts that appear on some bureaus but not others, balances that differ across bureaus, payment status discrepancies, and any entries you do not recognize. This review identifies the specific bureau-level problems that will appear on the tri merge.

Step 2. Dispute inaccurate entries at the specific bureaus that show them

A collection appearing at Equifax only requires a dispute filed at Equifax. A late payment marked incorrectly at TransUnion requires a dispute at TransUnion. File disputes at each bureau independently on the same day, targeting only the inaccurate entry at the bureau where it appears. Each bureau has 30 days to investigate. A successful removal adds back the score points the entry was suppressing at that specific bureau , potentially moving the middle score to a better tier.

Step 3. Reduce utilization at all three bureaus before the statement close date

Credit card balances update at each bureau when the creditor submits their monthly data file. Pay balances below 10% on every card before the statement close date , not the due date. The statement balance is what reports. If your utilization is high at two bureaus and low at one, the two high-utilization bureaus generate lower mortgage FICO scores. Reducing all cards simultaneously to below 10% before the statement close date produces synchronized score improvement across all three bureaus within the same reporting cycle.

Step 4. Avoid new credit applications in the 90 days before applying

Each new credit application triggers a hard inquiry at one or more bureaus. Hard inquiries cost 5-10 points each and stay on the file for 12 months of score impact. At the tri merge stage, a cluster of inquiries from the past 6 months signals to underwriters that the borrower sought credit aggressively in the recent term. The automated underwriting system factors recent inquiry patterns into the risk assessment independently of the score itself.

Step 5. Request a rapid rescore if you are close to a score tier after applying

Rapid rescore is a service available through mortgage lenders that updates the tri merge score within 3-5 business days after a qualifying change , a paid-off balance, a removed collection, or a corrected inaccuracy. This is not available directly to consumers. The lender orders it through the CRA. If your middle score sits within 20-30 points of the next rate tier, rapid rescore after a targeted paydown or successful dispute can move the qualifying score before the rate lock expires.

Your Free Credit App Is Often Misleading for Mortgage Purposes

Most consumers check Credit Karma, a bank app score, or a free VantageScore dashboard. Mortgage lenders use older, more conservative FICO mortgage models , not VantageScore, not FICO 8. Your consumer score may show 710. Your mortgage middle score may come back at 664. That is not a failure of the system. It is a difference in model design. Mortgage FICO models weight payment history and derogatory marks more heavily than consumer models. A late payment from three years ago that barely dents your FICO 8 can cost 40 points on your FICO 5. The gap is real, documented, and responsible for the preapproval surprise that forum discussions repeat consistently. The rule is simple: check your mortgage-specific FICO before assuming your consumer score reflects what a lender will see on the tri merge.

As NerdWallet's guide on mortgage credit score models confirms, the FICO versions lenders use for mortgage underwriting are specifically FICO Score 2 from Experian, FICO Score 4 from TransUnion, and FICO Score 5 from Equifax. These are not the same as any score shown on Credit Karma, Mint, or the FICO 8 score banks sometimes display to customers. The tri merge pulls all three mortgage-specific scores. The middle one prices your loan.

Common Tri Merge Credit Report Mistakes Buyers Make

Applying without reviewing all three bureau files first. Most buyers check one score on one app before applying. A surprise collection at one bureau, a wrong balance at another, or a payment status discrepancy across bureaus all affect the tri merge middle score in ways a single consumer check cannot detect. Pull all three bureau reports before any lender sees your tri merge.

Adding a co-borrower without checking both middle scores. A co-borrower with a lower middle score prices the joint application at the lower of the two middle scores. Adding a lower-score co-borrower can move the loan from a 740-tier rate to a 660-tier rate. Run both borrowers' bureau data through the middle-score calculation before deciding whether adding the co-borrower improves or hurts the overall application.

Opening new accounts in the months before applying. Each new account reduces average account age, adds a hard inquiry, and temporarily suppresses scores across the bureaus where the inquiry or new tradeline posts. Any new account opened within 12 months of a mortgage application appears as a recent account in the tri merge and may generate underwriter questions about the borrower's credit behavior leading up to the purchase.

Assuming a rapid balance paydown will immediately update all three bureaus. A credit card balance paid down today updates each bureau only when the creditor submits its next monthly data file to each bureau. That submission happens at the creditor's own cycle, which may be different for each bureau. A balance paid down in full today may still show the old balance at Equifax 20 days from now if the creditor has not yet submitted the updated file to Equifax. Rapid rescore through the lender is the only way to accelerate that update in the tri merge context.

Not disputing bureau-specific errors before applying. A collection account, a wrong late payment date, or an incorrect balance at one bureau that does not appear at the other two is a disputable inaccuracy , and a direct suppressor of the score at that bureau. Credit reporting errors can drag your middle score down when they appear on even one bureau file. Disputing before the tri merge pull removes the error before it affects the qualifying score. Disputing after the pull requires a rapid rescore to update the middle score, which takes 3-5 days and only applies if the lender coordinates it before the rate lock expires.

A tri merge credit report is the full mortgage underwriting credit document combining all three bureau files into one. The middle mortgage FICO score from the tri merge determines rate tier and loan eligibility. Consumer app scores and mortgage FICO scores frequently differ by 10-60 points because they use different scoring models. The gap between what a buyer expects and what the tri merge shows is the most common preapproval surprise in mortgage lending.

What is a tri merge credit report?

A tri merge credit report is a mortgage underwriting document that combines credit data from Equifax, Experian, and TransUnion into one consolidated file. Lenders use it to see all three bureau files simultaneously, compare data, identify discrepancies, and generate the three mortgage FICO scores used to determine qualifying. The middle of the three scores sets the rate and loan program eligibility.

What mortgage FICO scores appear on a tri merge credit report?

A tri merge report generates FICO Score 2 from Experian, FICO Score 4 from TransUnion, and FICO Score 5 from Equifax. These are industry-specific mortgage FICO models that use different weighting and factor calculations than FICO Score 8 or VantageScore. All three are older, more conservative models that weight derogatory marks and payment history more heavily. The middle value among the three becomes the qualifying score.

How does a tri merge report affect my mortgage rate?

The middle score from your tri merge report places you in a lender pricing tier. Most lenders segment rates into bands , 640-659, 660-679, 680-699, 700-719, 720-739, 740 and above , with each band carrying a different interest rate. The middle score from the tri merge locks you into one of those bands. A score one point below a tier threshold costs the same as a score 20 points below it, because the rate bands apply per tier. Being close to the next tier up before applying makes rapid rescore or targeted paydown worth evaluating.

How can I see what my tri merge credit report will show?

Pull all three bureau reports separately from AnnualCreditReport.com to see the underlying data. For the mortgage FICO scores specifically, myFICO.com offers access to FICO Score 2, 4, and 5 , the exact models used in a tri merge. Reviewing your three bureau files and mortgage FICO scores before any lender initiates a tri merge pull gives you the clearest possible picture of what the underwriter will see, and time to address any discrepancies or score suppressors before the pull counts.

Know What the Tri Merge Will Show Before the Lender Pulls It

The score on your consumer app is not the score on your tri merge report. Inaccurate entries, bureau-specific collections, and balance discrepancies across the three bureaus all affect your middle mortgage FICO in ways a single-bureau check cannot reveal. A free 3-bureau audit shows exactly what each bureau currently reports before any lender's tri merge pull puts it in front of an underwriter.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

What Are the Requirements to Buy a House for the First Time The tri merge credit report is the document that applies every mortgage requirement , score threshold, derogatory mark rules, bureau discrepancy flags , in a single underwriting review. This covers the full set of first-time buyer requirements that the tri merge evaluates, including employment history, gift funds, waiting periods after major derogatory events, and the pre-approval process that generates the tri merge pull.

-

Does Autopay Build Credit The payment history that appears on all three bureau files in a tri merge comes from autopay and manual payments on reporting accounts. This covers which accounts build credit history through payment, how autopay protects the payment marks that appear in the tri merge, and the account types where years of autopay produce no tri merge-visible credit history because they never report to bureaus.

-

Minimum Credit Score to Buy a House in California California's high purchase prices, CalHFA assistance program score requirements (660-680), and the prevalence of jumbo loans (requiring 700-720 middle scores) make the tri merge particularly consequential for California buyers. This covers the specific score thresholds by loan type and California region, the CalHFA qualification details, and the 60-day score improvement plan most California buyers use to cross a target threshold before the tri merge pull.