Do other countries use credit scores?

Yes, but the US is far more obsessed with them than most places.

In America, your credit score follows you everywhere. Want a car loan? Credit score. New apartment? Credit score. Credit card, mortgage, sometimes even insurance rates? Same story.

That is why a lot of Americans assume the whole world works the same way.

It does not.

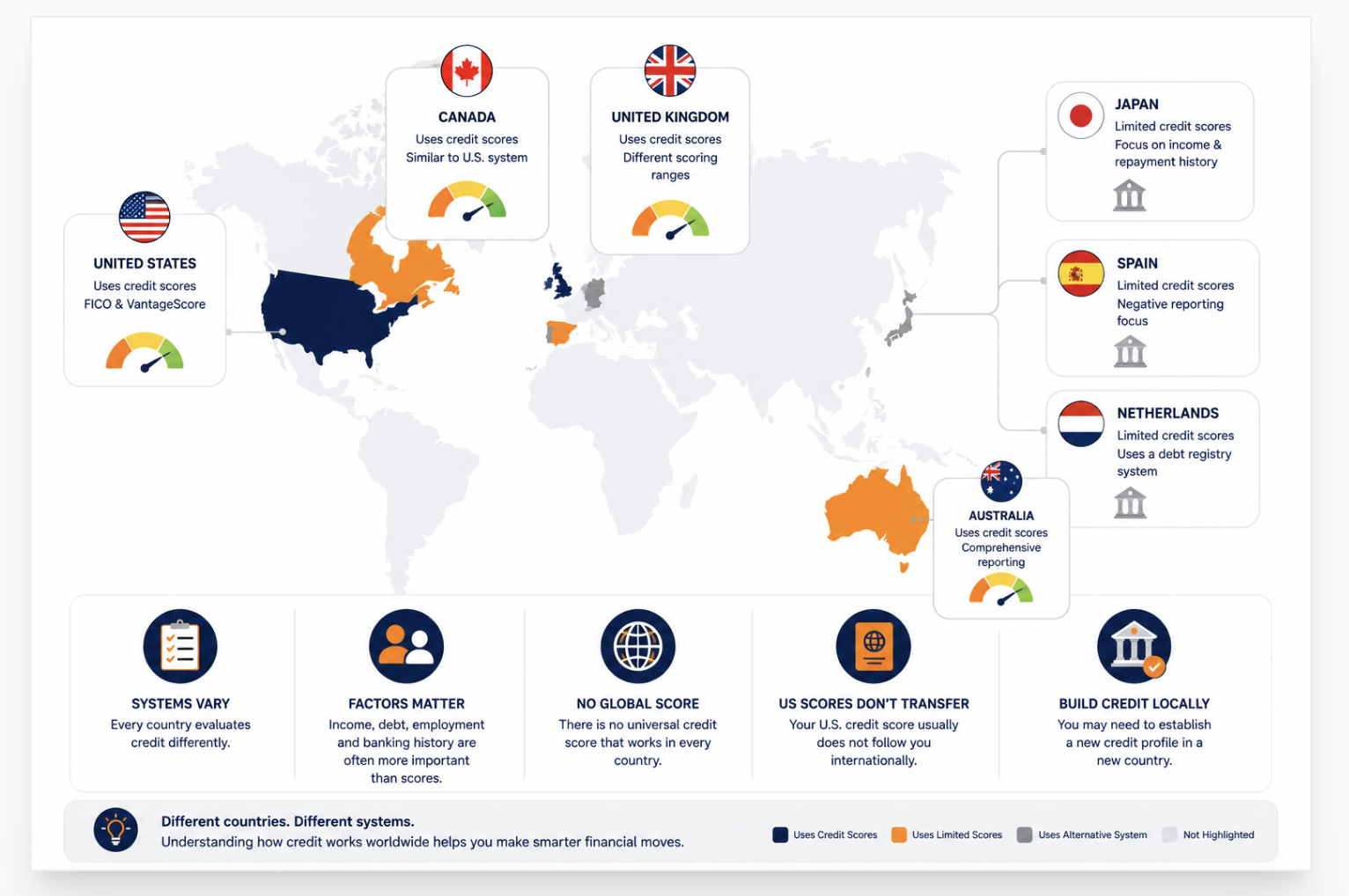

Some countries use systems that look close to the US model. Canada and the UK are good examples. But other countries care more about things like income, existing debt, repayment history, or your relationship with the bank itself.

And this is where people get caught off guard.

Someone can have an excellent 800 score in the US, move overseas, and suddenly realize that score means almost nothing there. In many cases, lenders abroad cannot even see the history tied to US credit bureaus.

According to Chase financial education resources, many countries use their own separate reporting systems instead of sharing one global score model. That means credit often does not transfer the way people expect.

Do Other Countries Use Credit Scores?

How Different Countries Handle Credit

The US treats the credit score like a financial report card that follows you everywhere. Other countries do not always work that way.

Canada uses a system nearly identical to the US, same bureaus, same basic factors, just a higher ceiling of 900 instead of 850. The UK has credit scores too, but the ranges are completely different and lenders there do not use FICO at all.

Australia now tracks both positive and negative credit behavior, which is something the US has always done but many countries still do not. Then you have places like France, the Netherlands, and Japan. They still evaluate borrowers carefully, but they focus more on income, employment stability, existing debt, and banking history instead of a single three-digit number.

The score concept exists across much of the world. How heavily it drives lending decisions varies a lot by country.

What Countries Use Credit Scores

Over 60 countries use some form of credit reporting or scoring system. The most developed systems are in the US, Canada, the UK, and Australia. China has both a government-run system and private scoring through Alibaba's Sesame Credit. India uses CIBIL scores (300-900). The systems differ significantly in what they measure, who runs them, and how heavily lenders rely on the number.

| Country | Credit Scores? | Main System | Score Range |

|---|---|---|---|

| United States | Yes | FICO, VantageScore , 3 major bureaus | 300-850 |

| Canada | Yes | Equifax Canada, TransUnion Canada | 300-900 |

| United Kingdom | Yes | Experian UK, Equifax UK, TransUnion UK | 0-999 (varies by bureau) |

| Australia | Yes | Equifax, Experian, Illion | 0-1,200 (Equifax) |

| India | Yes | CIBIL (primary), Experian India, Equifax India | 300-900 |

| Germany | Limited | SCHUFA (negative-weighted) | 0-100 (higher is better) |

| China | Limited | PBOC government registry + Sesame Credit | Varies by system |

| Japan | Limited | CIC, JICC, KSC (repayment history focus) | Not standardized |

| France | No score | Banque de France registry , income/bank based | No consumer score |

| Netherlands | No score | BKR , tracks negative events only | No consumer score |

| Spain | No score | CIRBE , loan registry, no consumer score | No consumer score |

The US is unusual in how deeply the credit score affects daily life.

Most countries use credit systems primarily for lending decisions , mortgages, car loans, credit cards. In the US, the score also influences apartment applications, insurance rates, and in some states, job applications. That level of integration is not common globally.

Countries That Use Credit Scores Similar to the US

Canada and Australia are the closest to the US model. Both use the same major bureaus , Equifax and TransUnion in Canada, Equifax and Experian in Australia. Both factor in payment history, utilization, and account age. The UK also uses credit scores but with different ranges and scoring agencies. India uses CIBIL scores on the same 300-900 scale as Canadian scores.

Equifax Canada and TransUnion Canada both operate. Payment history and utilization are the main drivers , same as the US. Canadian scores go up to 900 instead of 850. The threshold for "good" credit sits around 660-724. A score above 725 opens competitive lending products. The overall framework is nearly identical to the US model.

Australia adopted Comprehensive Credit Reporting (CCR) in 2018, adding positive payment data alongside negatives. Before CCR, only missed payments and defaults were tracked. Now repayment history on mortgages, personal loans, and credit cards all contribute. Three agencies: Equifax (0-1,200), Experian, and Illion (formerly Dun & Bradstreet). The scale is different but the underlying concept mirrors the US.

CIBIL (Credit Information Bureau India Limited) is the primary credit bureau, with Experian India, Equifax India, and CRIF High Mark also operating. Lenders typically require a CIBIL score above 750 for competitive rates. The 300-900 range mirrors Canadian scoring. The credit culture is growing fast as digital lending expands across India.

The UK has three credit reference agencies but uses different scoring scales than the US. Experian UK: 0-999. Equifax UK: 0-1,000. TransUnion UK: 0-710. UK lenders do not use FICO. The scoring factors are similar , payment history, debt levels, account age , but the scales confuse Americans who expect 300-850. A UK Experian score of 881-960 is "Good" there.

Countries That Do Not Use Traditional Credit Scores

France, the Netherlands, and Spain do not use a consumer credit score the way the US does. France relies on income documentation and bank history. The Netherlands uses the BKR, a registry that primarily tracks debt defaults and late payments , not a score. Spain's CIRBE system records outstanding loans but does not generate a borrower score. Many developing nations have no formal credit scoring infrastructure at all.

These countries still lend money. They still evaluate risk. They just do it differently.

Instead of a numeric score, lenders review documents directly. Bank statements showing income and spending patterns. Employment contracts. Employer references. Existing debt records from national registries. Length of time at the current address. Banking relationship length.

For American borrowers moving to these countries, the adjustment can be significant. The idea of a quick score-based approval does not apply. Applications take longer and require more documentation.

Countries with minimal or no credit scoring

- France. No consumer credit score. The Banque de France operates a national credit register (FICP) that tracks defaults and banking bans. Lenders calculate debt-to-income ratios directly from income documentation. Most French mortgages require a DTI below 33%.

- Netherlands. The BKR tracks registered credit agreements and negative events , late payments, defaults, settled debts. A BKR registration is usually negative (a "black mark"). There is no positive credit score. Lenders access the BKR record and evaluate income separately.

- Spain. The CIRBE (Credit Risk Information Center) is run by the Bank of Spain and catalogs outstanding loans above 9,000 euros. It is a liability register, not a consumer score. Lenders query CIRBE and then assess the borrower's income and debt load individually.

- Germany. The SCHUFA system scores consumers on a 0-100 scale where higher scores indicate lower risk. Most creditworthy borrowers score above 97. SCHUFA is primarily negative-weighted , it tracks late payments, defaults, and insolvencies. A SCHUFA entry (negative mark) is a significant lending obstacle.

How Credit Scores Work in Canada

Canada's credit system uses the same two major bureaus as the US , Equifax Canada and TransUnion Canada. The scale runs from 300 to 900. Payment history and credit utilization drive the score the same way they do in the US. A score above 660 is generally considered good in Canada. Above 725 opens competitive lending rates. The biggest difference from the US is the scale ceiling: 900 instead of 850.

The mechanics are nearly identical to what US consumers know.

Pay on time, keep balances low, avoid too many new applications, keep old accounts open. The five factor categories match the FICO model: payment history, amounts owed, length of history, new credit, and credit mix.

What does not transfer: your US credit file. Equifax Canada and Equifax US are separate entities. Moving from the US to Canada means your US payment history stays in US systems. Canadian lenders cannot access it. You start from zero in Canada, even with a perfect US score.

Nova Credit offers a "credit passport" service that can translate a US credit history into a Canadian-equivalent report for some lenders. A small number of Canadian financial institutions accept this. Most do not.

How Credit Scores Work in the UK

The UK uses three credit reference agencies: Experian UK, Equifax UK, and TransUnion UK. Each uses a different scoring scale. Experian UK scores run 0-999. Equifax UK runs 0-1,000. TransUnion UK runs 0-710. UK lenders do not use FICO. The factors are similar to the US , payment history, credit utilization, account age, and recent applications , but the ranges require a mental reset for American borrowers.

UK credit has a few differences that catch Americans off guard.

Electoral roll registration matters. Being registered on the electoral roll (voter registration) in the UK is a positive factor in credit scoring. UK lenders use address verification through the electoral roll as a fraud-prevention and identity check. Not being registered is a disadvantage.

Financial associations affect your score. If you share finances with a partner who has poor credit, that association can affect your own credit file in the UK. This works differently from the US, where joint accounts impact both files but being associated with someone does not automatically link credit profiles.

The "thin file" problem is severe. A new American arrival in the UK typically has no UK credit history at all. UK lenders treat this the same as having bad credit for approval purposes. Opening a basic bank account, getting on the electoral roll, and applying for a secured card are the first three steps most financial advisors recommend for US expats arriving in the UK.

As Experian's guide to protecting credit while living abroad confirms, keeping US accounts active and paid while building local credit history in the new country is the optimal strategy for Americans living overseas.

Does Europe Use Credit Scores

Europe does not use a single unified credit score. Each country manages credit independently. The UK is closest to the US model. Germany uses SCHUFA. France uses income documentation. The Netherlands uses the BKR. No EU-wide credit score exists, and GDPR privacy laws in Europe impose strict restrictions on how personal financial data can be shared across borders.

The European Union's General Data Protection Regulation (GDPR) is part of why no Europe-wide credit system exists.

GDPR restricts how personal financial data can be processed and transferred between countries. Building a pan-European credit bureau would require navigating privacy laws across 27 different member states, each with its own regulatory interpretation. The political and legal complexity makes a unified European credit score practically impossible in the near term.

Country-by-country breakdown in Europe

- Germany (SCHUFA). Germany's SCHUFA is one of Europe's most developed credit systems. Scores run 0-100, with most creditworthy consumers scoring 97 or above. A SCHUFA-Einmeldung (negative registration) for a missed payment or default is a significant obstacle for loans and even apartment applications in Germany. SCHUFA scores are not publicly disclosed by default , consumers must request their own report annually.

- France. No consumer credit score. The Banque de France FICP tracks payment incidents and banking bans. Lenders assess income, assets, and employment contracts directly. French mortgage rules typically cap debt-to-income at 35%. Income documentation matters more than any numeric score.

- Netherlands. The BKR registers all consumer credit agreements above 250 euros. Negative registrations for late payments and defaults are the primary data points. There is no positive credit scoring. A clean BKR history means no bad marks , it does not mean a strong score.

- Spain. The CIRBE tracks outstanding loans for Spanish residents. Lenders access CIRBE for liability data and independently assess income. Credit cards, mortgages, and personal loans all register in CIRBE above the threshold amount.

- Nordics (Sweden, Norway, Denmark). Credit bureaus exist in Scandinavian countries. Sweden uses UC (Upplysningscentralen) and Creditsafe. Denmark and Norway have similar agencies. Scores or creditworthiness assessments exist, but the systems are less embedded in daily life than in the US.

Why US Credit Scores Usually Do Not Transfer

There is no global credit score system. US credit data lives inside US-specific databases at Equifax, Experian, and TransUnion. When you move abroad, foreign lenders cannot access those databases. They have no local record of your US credit behavior. From their perspective, you have no credit history. That is treated the same as having bad credit for most approval decisions.

This surprises more Americans than it should.

The three major US bureaus operate globally as business-data providers, but their consumer credit files are country-specific. Equifax Canada and Equifax USA are legally separate entities with separate databases. Moving from Dallas to Toronto does not move your file.

A few exceptions exist.

Nova Credit partners with credit bureaus in select countries , including the UK, Canada, Australia, India, Mexico, and several others , to create a "credit passport." This translates a foreign applicant's home-country credit file into a US-compatible format for US lenders. It works in one direction: bringing foreign credit into the US. Reverse translation , taking a US credit file abroad , is not widely supported.

Some international banks with US operations (like HSBC or Barclays) may consider a US customer's existing banking relationship when opening accounts abroad. This does not transfer the credit score but may ease account opening.

The result: an American with an 800 FICO score moves to Germany and starts with nothing. A German national with an established SCHUFA history moves to the US and starts with nothing. Both arrive in the new country as credit invisible.

Understanding what credit score you start with from zero applies to any new market , whether you are a young adult in the US or an American arriving in a new country without local credit history.

What Lenders Look at Outside the US

In countries without strong credit scoring systems, lenders rely more on income documentation, employment history, bank account activity, savings balances, existing debt records, and relationship history with the bank. The income-to-debt ratio (DTI equivalent) matters more than any score. Employment stability , how long you have worked for the same employer, the size of the company, the type of contract , is a major factor in many European and Asian markets.

Here is what lenders in score-light countries actually review.

- Income documentation. Tax returns, pay stubs, and employer letters. France typically requires three months of pay stubs. Germany often requests two years of tax filings. Many countries want proof of employment type , permanent contracts matter more than temporary contracts.

- Bank account history. How long you have banked with the institution. Average daily balance. Overdraft frequency. Regular income deposits. Lenders in relationship-banking cultures like Japan and South Korea place significant weight on banking tenure.

- Debt-to-income ratio. Most countries cap this explicitly. France at 33-35%. Germany typically requires 40% or below. Spain varies. The calculation is similar to the US but the thresholds differ.

- Negative registries. Even in countries without positive credit scores, negative events , missed payments, defaults, court judgments , are tracked and visible to lenders. A clean negative registry is the baseline requirement.

- Collateral and assets. In markets where credit history is thin, lenders ask for more collateral. Property, savings, investments. The less credit data available, the more the lender relies on tangible assets.

As Bankrate's international credit score guide explains, the best practices for building credit abroad , making regular payments on time, managing debt responsibly, and maintaining stable banking relationships , reflect the same financial behaviors that work in any credit system globally. The specific score may not transfer, but the habits do.

Understanding the full range of factors lenders check beyond the credit score explains why two borrowers with the same score can receive completely different decisions , and why lenders in score-light countries can make accurate lending decisions without a three-digit number at all.

Can You Build Credit Internationally

Yes. Most countries allow foreign nationals to build local credit, though the starting point is always from scratch. The strategy is the same in most markets: open a bank account, get a secured or basic credit card, pay on time every month, keep balances low, and let the account age. The timeline is typically 12-24 months to build a meaningful local credit profile in most developed markets.

Banking history is the foundation in most non-US markets. Open an account with a major local bank as soon as possible after arriving. Even basic accounts build a banking relationship record that lenders reference when you apply for credit later. In countries like Japan and South Korea, this banking tenure matters significantly.

In the UK, get on the electoral roll immediately. In Germany, register your address (Anmeldung) with the local authorities , address registration is legally required and also helps lenders verify your identity. In Australia, confirm your file exists at the three bureaus by requesting a free annual report.

Secured credit cards exist in most developed markets. The deposit model works the same way it does in the US , your deposit becomes the limit, approval is easier, and the card reports to local credit agencies. This is the fastest way to start building a local credit file in Canada, the UK, or Australia.

Do not close US credit accounts when you move. Keep them active with small purchases and autopay. Your US credit file keeps aging, payment history keeps building, and the account age compounds. If you return to the US, you want to find a strong file waiting for you , not a closed file with thin history.

Verify that your local accounts are reporting correctly. Check for errors in the same way you would in the US. Most countries offer at least one free annual credit report from each bureau. Catching reporting errors early prevents them from suppressing your emerging local credit profile.

As NerdWallet's guide on applying for credit while living abroad notes, banking systems vary widely across countries, and what works in one market may not work in another. Research the specific credit system in your destination country before you arrive, not after the first denial.

The fundamental behaviors behind what makes a good credit score , paying on time, keeping utilization low, and building account history over time , apply in virtually every credit system in the world. The score range changes. The bureaus change. The window for "good" credit changes. The behaviors that earn it do not.

Do all countries use credit scores?

No. Many countries use credit systems but not all use numeric scores. France uses income documentation instead of a score. The Netherlands tracks negative credit events through the BKR registry without generating a consumer score. Spain's CIRBE records outstanding loans without scoring borrowers. Dozens of developing nations have limited or no formal credit scoring infrastructure. Even among countries with credit scores, the systems vary so significantly in scale and method that they cannot be directly compared.

Can you use your US credit score internationally?

No. There is no global credit score system. US credit data stays in US-specific bureau databases. Foreign lenders cannot access US credit files. Moving abroad requires rebuilding credit in the new country from scratch, regardless of how strong the US score was. Nova Credit offers a credit passport service that translates select foreign credit histories for use with US lenders , not the reverse. A few international banks with US operations may recognize an existing relationship, but this does not transfer the score.

Does the UK use FICO scores?

No. The UK does not use FICO scores. Three credit reference agencies operate there , Experian UK, Equifax UK, and TransUnion UK , each with its own scoring scale. Experian UK scores run 0-999. Equifax UK runs 0-1,000. TransUnion UK runs 0-710. The factors driving UK scores are similar to US FICO factors, but the scales are different. An American arriving in the UK starts with no local credit history regardless of their US FICO score.

Does moving abroad reset your credit?

Your US credit score does not reset , it stays in US bureau databases as long as your US accounts remain open and active. What resets is your credit in the new country. You arrive with no local credit file. The local equivalent of a "starting score" is essentially zero , you are credit invisible to local lenders. To protect the US side, keep US accounts active, set up autopay for all US accounts, and maintain a US mailing address with a trusted contact.

Is there a worldwide credit score?

No. No worldwide credit score exists. FICO operates in some countries outside the US, but not as a global unified system. Each country has its own bureaus, scales, and rules. The closest attempt at cross-border credit translation is Nova Credit's credit passport, which works in limited country pairs with a small number of US lenders. Building a genuine global credit score would require solving for dramatically different privacy laws, data-sharing agreements, and financial regulatory frameworks across more than 190 countries.

Before You Move Abroad , Check Where Your US Score Stands

Your US credit file is the financial foundation you leave behind and potentially return to. A free 3-bureau audit shows exactly what Equifax, Experian, and TransUnion currently report so you know your starting point before you go , and can protect it while you are away.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

Good Credit Building Credit Cards That Can Help Raise Your Score When you arrive in a new country and start your credit from scratch, a credit building card is usually the fastest first move. This covers the specific secured and unsecured card options that report to all three bureaus, how to use them to build a meaningful score in 6-12 months, and the single biggest mistake that keeps people stuck with a low score even when they think they are doing everything right.

-

701 Credit Score , What It Means and What You Can Qualify For Building to 701 is a common milestone in both the US and the Canadian credit system (where the Good tier also starts around 660-680). This covers what a 701 score opens in the US , mortgages, auto loans, credit cards , the rate differences between 701 and 740, and the specific actions that move the score from the Good tier into Very Good territory fastest.

-

501 Credit Score , What It Means and How to Improve It Starting over in a new country often means starting with a very thin or very poor credit profile. A 501 score in the US represents the bottom of what qualifies for FHA financing. This covers the specific products accessible at 501, the fastest path from 501 to 580 and 620, and how the improvement timeline maps to the same behavioral principles that build credit in any country's scoring system.